Efficiency and Market Structure (Edexcel A-Level Economics A): Revision Notes

Efficiency and Market Structure

Introduction to efficiency

Efficiency is a crucial concept when evaluating how well markets operate. A society needs to find ways to use its limited resources as efficiently as possible. This involves making optimal decisions about production methods, output levels, and the mix of goods and services produced. The structure of a market - meaning the competitive environment in which firms operate - has a significant influence on efficiency outcomes.

Market structure is important because it affects how firms behave and make decisions. The degree of competition, the number of firms present, and the ease with which new firms can enter a market all play a role in determining overall economic efficiency.

The relationship between market structure and efficiency is fundamental to understanding economic outcomes. Different market structures create different incentives for firms, which in turn affect how efficiently resources are allocated in the economy.

Types of efficiency

Productive efficiency

Productive efficiency happens when firms select the best combination of factors of production and generate the maximum possible output from those inputs. In practical terms, this means producing at the minimum long-run average cost.

From a firm's viewpoint, the production decision involves three stages:

- Deciding the output level: The firm determines how much it wants to produce

- Choosing the factor combination: Given the intended production scale, the firm selects the appropriate mix of inputs

- Minimising production costs: The firm attempts to produce as much output as possible from the chosen inputs

When a firm begins this decision process, it considers current market conditions, expected future conditions, and the existing state of technology. An important distinction exists between the short run and the long run. Once a firm has chosen its desired production scale and invested in the necessary capital equipment, it becomes locked into that capital stock in the short run. If conditions change in the future, it will take time to implement adjustments.

In the short run, a firm may achieve static efficiency by choosing the minimum average cost given the circumstances at that particular moment.

Worked Example: Productive Efficiency in Practice

Consider a bakery that needs to produce 1,000 loaves of bread per day:

Step 1: Determine output level The bakery has decided to produce 1,000 loaves based on market demand.

Step 2: Choose factor combination The bakery must decide between:

- Option A: 3 workers + 2 ovens

- Option B: 5 workers + 1 oven

Step 3: Minimise costs If Option A costs $500/day and Option B costs $600/day, the bakery achieves productive efficiency by choosing Option A, producing the desired output at the lowest possible cost.

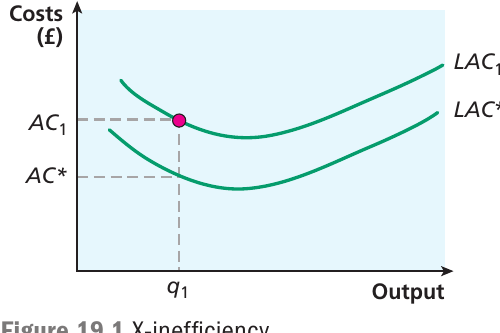

X-inefficiency

Will a firm always operate as efficiently as possible? The concept of X-inefficiency recognises that this may not always be the case. This situation was introduced when discussing the principal-agent problem - the idea that managers might not be fully accountable to a firm's owners, potentially leading to managerial slack.

X-inefficiency occurs when a firm does not operate at minimum cost, possibly due to organisational slack or other internal inefficiencies.

The principal-agent problem creates a real risk of X-inefficiency in firms. When managers (agents) are not fully accountable to owners (principals), they may not have sufficient incentive to minimise costs, leading to the firm operating above its most efficient cost curve.

The diagram above illustrates this concept. LAC* represents the most efficient long-run average cost curve for the firm at any output level. With X-inefficiency present, a firm might produce on a long-run average cost curve like LAC₁, which sits above the most efficient position. At output , for instance, the firm produces at an average cost of , whereas it could have achieved if it operated without X-inefficiency. The firm is therefore operating above its lowest possible long-run average cost curve.

Allocative efficiency

The notion of allocative efficiency addresses whether an economy distributes its resources to produce a balance of goods and services that matches consumer preferences. Within an individual market, this means firms should produce the ideal amount of each good that consumers wish to buy.

This concept connects to equilibrium in the demand and supply model, where prices act as signals to both consumers and producers, bringing demand and supply into balance. For an individual market, allocative efficiency occurs when the price charged equals marginal cost. This ensures that the marginal benefit received by society from consuming a good or service matches the marginal cost of producing it.

Price as a Market Signal

In efficiently operating markets, prices serve a dual role:

- They signal to consumers the relative scarcity and value of goods

- They signal to producers where resources should be allocated

When , this signalling mechanism ensures that resources flow to their most valued uses, achieving allocative efficiency.

Dynamic efficiency

The discussion of efficiency so far has focused on how to make the best use of existing resources, producing an appropriate mix of goods and services using factor inputs as efficiently as possible, given existing knowledge and technology. This represents a relatively static view of efficiency.

Dynamic efficiency goes further by recognising that knowledge and technology change over time. Investment in research and development means that production can be carried out more efficiently at some future date. Furthermore, the development of new products may mean that a different mix of goods and services may serve consumers better in the long term.

The concept of dynamic efficiency originated from the work of economist Joseph Schumpeter, who argued that a preoccupation with static efficiency might sacrifice opportunities for greater efficiency in the long run. In other words, there may be a trade-off between achieving efficiency today and improving efficiency tomorrow.

The Static-Dynamic Efficiency Trade-off

Schumpeter's insight reveals a fundamental tension in economics: pursuing perfect static efficiency today might prevent the innovation and development needed for greater efficiency tomorrow. For example, a firm might need to accept higher costs in the short run to invest in research that will dramatically reduce costs in the future.

This trade-off is particularly relevant when evaluating different market structures, as some may be better at fostering innovation despite being less statically efficient.

Exam tip: These notions of efficiency are important and will be central to discussions of market structures throughout this topic, so ensure you understand them before proceeding.

Market structure overview

Firms cannot make decisions without understanding the market environment in which they operate. In some markets, firms are such small players that they cannot influence the price at which they sell. In others, a firm may be the only seller, giving it much greater discretion in devising price and output strategies. Many intermediate situations exist where a firm has some control over price but must remain aware of rival firms in the market.

Economists have developed various models that allow different market structures to be analysed. The key characteristics of alternative market structures are summarised in the table below:

| Perfect Competition | Monopolistic Competition | Oligopoly | Monopoly | |

|---|---|---|---|---|

| Number of firms | Many | Many | Few | One |

| Freedom of entry | Not restricted | Not restricted | Some barriers to entry | High barriers to entry |

| Firm’s influence over price | None | Some | Some | Price maker, subject to the demand curve |

| Nature of product | Homogeneous | Differentiated | Varied | No close substitutes |

| Examples | Cauliflowers Carrots | Fast-food outlets Travel agents | Cars Mobile phones | PC operating systems Local water supply |

In many ways, we can view these as a spectrum of markets with different characteristics. The table compares market structures across several dimensions:

- Number of firms: Ranging from many in perfect competition to just one in monopoly

- Freedom of entry: From unrestricted in perfect competition to high barriers in monopoly

- Firm's influence over price: From none (price taker) in perfect competition to price maker in monopoly

- Nature of product: From homogeneous in perfect competition to no close substitutes in monopoly

Real-World Examples of Market Structures

Different industries exhibit characteristics of different market structures:

- Perfect competition: Agricultural products like cauliflowers and carrots

- Monopolistic competition: Fast-food outlets and travel agents

- Oligopoly: Cars and mobile phones

- Monopoly: PC operating systems and local water supply

Understanding which market structure best describes a particular industry helps predict how firms will behave and how efficiently resources will be allocated.

Perfect competition

At one extreme of the market spectrum is perfect competition. This is a market where each individual firm acts as a price taker, meaning no individual firm is large enough to influence the price, which is set by the market as a whole.

This situation arises when many firms operate in a market, each producing a product that is essentially identical regardless of which firm produces it. Think of a market for a particular type of vegetable, for example. One cauliflower is very similar to another, and it would not be possible for a particular cauliflower grower to charge a premium price for its product.

Such markets are also characterised by freedom of entry and exit. In other words, it is relatively easy for new firms to enter the market or for existing firms to leave if they wish to produce something else. The market price in such a market will be driven down to the level at which the typical firm just makes enough profit to stay in business. If firms make more than this, other firms will be attracted in, and supernormal profits will be competed away. If some firms do not make sufficient profit to remain in the market, they will exit, allowing price to drift up until the typical firm again just makes enough to stay in business.

Monopoly

At the other extreme of the market structure spectrum is monopoly. This is a market where only one firm operates. Such a firm has some influence over price and can choose a combination of price and output to maximise its profits. The monopolist is not entirely free to set any price it wants, as it must remain aware of the demand curve for its product. Nonetheless, it has the freedom to choose a point along its demand curve.

The nature of a monopolist's product is that it has no close substitutes - either actual or potential - so it faces no competition. In early 2022, Google's share of the UK search engine market was estimated at 92.88%, and it also held a global market share of 85.55% at this time.

Another condition of a monopoly market is the existence of barriers to entry for new firms. This means the firm can set its price to make profits above the minimum needed to keep the firm in business, without attracting new rivals into the market.

Case Study: Microsoft's PC Operating System Monopoly

In 1998, Microsoft was found to have a global monopoly on PC operating systems. The company's dominant market position allowed it to influence pricing without significant competitive pressure.

Key features of this monopoly:

- Microsoft held over 90% of the PC operating system market

- High barriers to entry due to network effects (most software was designed for Windows)

- No close substitutes available for most consumers

- Ability to maintain supernormal profits over extended periods

This case illustrates how barriers to entry can sustain monopoly power and allow firms to earn profits well above the competitive level.

Monopolistic competition

Between the two extreme forms of market structure are many intermediate situations where firms may have some influence over their selling price but still must account for other firms in the market. One such market is known as monopolistic competition.

This is a market with many firms operating, each producing similar but not identical products, allowing some scope for price influence, perhaps due to brand loyalty. However, firms in such a market are likely to be relatively small. They may find it profitable to ensure their product is differentiated from other goods and may advertise to convince potential customers of this differentiation. For example, small-scale local restaurants may offer different styles of cooking.

Oligopoly

Another intermediate form of market structure is oligopoly, which literally means 'few sellers'. This is a market where just a few firms supply the market. Each firm will make decisions with close awareness of how other firms in the market may react to their actions.

In some cases, firms may try to collude - working together as if they were a monopolist - thus achieving higher profits. In other cases, they may act as keen rivals, which will tend to result in supernormal profits being competed away. The question of whether firms in an oligopoly collude or compete has a substantial impact on how the overall market performs regarding resource allocation, and whether consumers are disadvantaged as a result of the actions of firms in the market.

The behaviour of oligopolistic firms is particularly complex because of strategic interdependence. Each firm must consider not just market conditions, but also how rival firms will respond to its decisions. This creates a game-theory situation where outcomes depend on the strategies chosen by all firms in the market.

Synoptic link: The characteristics of monopolistic competition and oligopoly are examined more fully in Chapter 20.

Barriers to entry

If firms in a market can make supernormal profits, this acts as an inducement for new firms to try gaining entry into that market to share in those profits. A barrier to entry is an obstacle that makes it difficult for new firms to join a market. The existence of such barriers is of great importance in influencing the market structure that will develop.

For example, if a firm holds a patent on a particular good, this means no other firm is permitted by law to produce the product, and the patent-holding firm thus has a monopoly. The firm may then be able to set price to make supernormal profits without fear of rival firms competing away those profits.

On the other hand, if no barriers to entry exist in a market, and if existing firms set price to make supernormal profits, new firms will join the market, and the increase in market supply will push price down until no supernormal profits are being made.

Worked Example: How Barriers to Entry Affect Market Outcomes

Scenario 1: High Barriers (Pharmaceutical Patent)

- A drug company holds a 20-year patent on a new medicine

- Production cost per unit: $5

- Price charged: $50

- Result: Supernormal profits sustained for the patent duration because no competitors can legally enter

Scenario 2: No Barriers (Agricultural Market)

- Farmers grow wheat with no legal restrictions

- Production cost per unit: $3

- Initial price: $6 (supernormal profits)

- Result: New farmers enter, supply increases, price falls to approximately $3.20 (just covering costs), and supernormal profits are competed away

This example demonstrates how barriers to entry determine whether supernormal profits can persist in the long run.

The model of perfect competition

The model of perfect competition has a special place in economic analysis. If all its assumptions were fulfilled, and if all markets operated according to its precepts, the best allocation of resources would be ensured for society as a whole. Although it may be argued that this ideal is not often achieved, perfect competition nonetheless provides a yardstick by which all other forms of market structure can be evaluated.

Assumptions of the model

The assumptions of the model of perfect competition are as follows:

-

Profit maximisation: Firms aim to maximise profits

-

Many participants: There are many participants (both buyers and sellers), none of whom is large enough to influence price

Synoptic link: The full model of perfect competition is analysed later in this chapter, after the discussion of monopoly and barriers to entry.

Key Points to Remember:

-

Productive efficiency occurs when firms choose optimal combinations of factors of production and produce at minimum long-run average cost

-

X-inefficiency arises when firms operate above their lowest possible cost curve due to organisational slack

-

Allocative efficiency is achieved when firms produce the appropriate bundle of goods and services relative to consumer preferences, occurring when price equals marginal cost ()

-

Dynamic efficiency recognises that innovation and technical progress can improve productive and allocative efficiency over time, potentially involving a trade-off between short-run and long-run efficiency

-

Market structure ranges from perfect competition (many firms, no barriers, price takers) through monopolistic competition and oligopoly to monopoly (one firm, high barriers, price maker), with barriers to entry playing a crucial role in determining which structure develops

Essential Understanding for Exam Success

These concepts of efficiency and market structure form the foundation for understanding how markets operate and allocate resources. Ensure you can:

- Define and distinguish between the different types of efficiency

- Explain the characteristics of each market structure

- Understand how barriers to entry affect market outcomes

- Evaluate the relationship between market structure and efficiency

These themes will recur throughout your study of market structures and competition policy.