The Main Causes of Inflation (HSC SSCE Economics): Revision Notes

The Main Causes of Inflation

Economists identify four primary causes of inflation: demand-pull, cost-push, inflationary expectations, and imported inflation. Two additional causes—government policies and excessive money supply growth—can also contribute to rising prices. Understanding these causes is essential for analysing inflationary pressures and evaluating policy responses.

Demand-pull inflation

Demand-pull inflation occurs when total spending in the economy exceeds its productive capacity. When aggregate demand grows faster than the economy's ability to produce goods and services, consumers compete for limited output by bidding prices upward.

How demand-pull inflation works

In a market economy, prices adjust to balance supply and demand. When aggregate demand increases beyond the economy's capacity to expand output in the short term, prices rise instead of production increasing. This happens because:

- Consumers are willing to pay higher prices to secure goods and services

- Firms cannot quickly increase production to meet demand

- Competition among buyers drives prices upward

- The economy operates at or near full capacity

The key mechanism behind demand-pull inflation is that output cannot expand quickly enough to meet increased demand. When the economy approaches or reaches full capacity, the only way to balance excess demand is through higher prices. This contrasts with periods when spare capacity exists—in those situations, increased demand leads to higher output rather than higher prices.

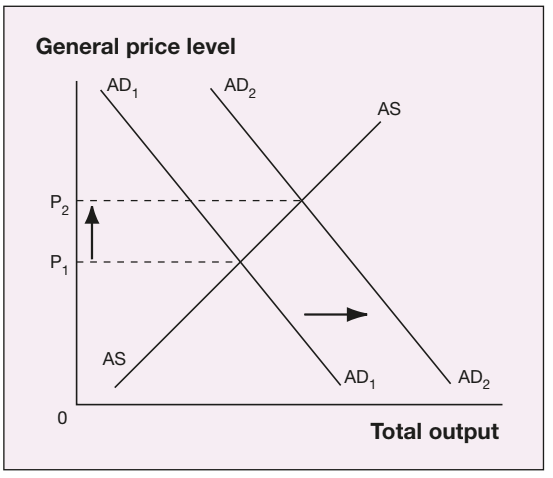

The diagram shows how a rightward shift in aggregate demand (from to ) leads to higher prices (from to ) when the economy approaches its productive limits. At higher price levels, consumers pay more for the same quantity of output.

Australian context

Demand-pull inflation was particularly prominent during the late 1980s when strong economic growth increased consumer spending beyond the economy's capacity. More recently, the commodities boom in the 2000s significantly boosted business investment and consumer confidence, creating demand-pull inflationary pressures through increased aggregate demand.

Exam tip: When analysing demand-pull inflation, always explain why output cannot expand to meet demand. Link your answer to the economy's productive capacity and short-term supply constraints.

Cost-push inflation

Cost-push inflation arises when production costs increase, forcing firms to raise prices to maintain profit margins. Unlike demand-pull inflation, cost-push inflation originates from the supply side of the economy.

The mechanism of cost-push inflation

When the costs of factors of production rise, firms face a choice: absorb the higher costs and accept lower profits, or pass them on to consumers through higher prices. Most firms choose the latter option, particularly when costs rise across an entire industry.

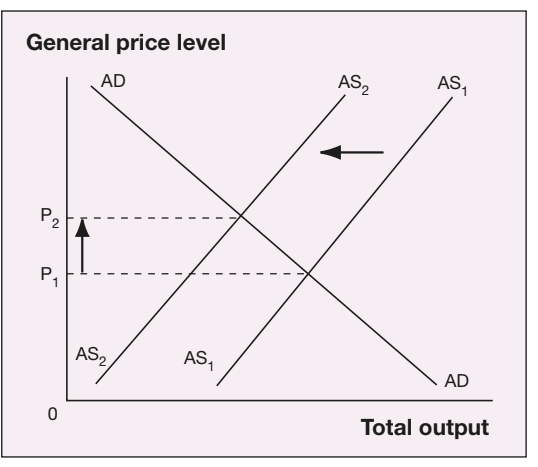

The diagram illustrates how rising production costs shift the aggregate supply curve leftward (from to ). At any given price level, firms now supply less output due to higher costs. This results in higher prices (from to ) and reduced total output.

Major sources in Australia

Two key sources of cost-push inflation affect the Australian economy:

Wages: Labour costs typically represent around 60% of a firm's total expenses. When wages increase faster than productivity growth, the cost per unit of output rises. Firms pass these increases on to consumers to preserve profitability. This becomes particularly problematic when wage rises occur across multiple industries simultaneously.

Raw materials: Price increases for essential inputs—especially fuel and oil—trigger cost-push inflation. Since most production processes require energy, higher fuel costs affect nearly all sectors of the economy. Firms increase final product prices to offset these higher input costs.

Understanding the pass-through mechanism:

Cost-push inflation works through a straightforward transmission process. When production costs rise, firms calculate their new cost structure and adjust prices accordingly. Unlike demand-pull inflation where consumers drive prices up through competition, in cost-push inflation firms actively raise prices to maintain their profit margins. This means the inflationary impulse originates from the supply side rather than excessive demand.

Recent Australian experience

The 2022–2023 inflation surge demonstrated cost-push pressures. Global supply chain disruptions raised the cost of imported inputs. Energy prices experienced their fastest rise in half a century due to the war in Ukraine. These cost increases forced Australian businesses to raise prices, contributing to inflation rates not seen in decades.

Exam tip: Distinguish clearly between demand-pull and cost-push inflation. Demand-pull stems from excessive spending; cost-push originates from rising production costs. Use AS-AD diagrams to show the different shifts involved.

Inflationary expectations

Inflationary expectations refer to what individuals and firms anticipate about future price increases. These expectations significantly influence actual inflation outcomes because they shape economic behaviour.

The self-fulfilling nature of expectations

When people expect higher inflation, their actions can bring about the very inflation they anticipate. This creates a self-fulfilling prophecy that challenges policymakers. Two mechanisms drive this process:

Consumer behaviour: If households expect prices to rise soon, they bring forward planned purchases to buy before prices increase. This surge in current consumption increases aggregate demand, creating demand-pull inflation. Similarly, firms expecting higher demand may raise prices preemptively to maximise profits, directly contributing to inflation.

Wage negotiations: Employees incorporate inflation expectations into wage bargaining. Since workplace contracts typically cover two to three years, workers demand higher wage increases to preserve their real purchasing power against expected future inflation. When firms grant these higher wages and pass the costs on to consumers, cost-push inflation results.

The expectations cycle:

Inflationary expectations create a powerful feedback loop:

- People expect higher inflation

- Workers demand higher wages to protect real income

- Consumers increase current spending to buy before price rises

- Firms raise prices in response to higher costs and demand

- Actual inflation rises, confirming initial expectations

- Expectations for future inflation increase further

This cycle demonstrates why managing expectations is crucial for controlling inflation. Once expectations become entrenched, inflation becomes self-perpetuating and difficult to reduce.

Policy challenges

Managing inflationary expectations presents a major challenge for the Reserve Bank of Australia. Once expectations become entrenched, they perpetuate inflation through the mechanisms described above. Breaking this cycle requires convincing the public that inflation will fall—but this credibility takes time to establish.

In 2023, the RBA announced increased frequency and clarity in its public communications specifically to manage expectations. By clearly explaining its inflation targets and policy actions, the RBA aims to anchor long-term expectations within its 2–3% target band.

Exam tip: When discussing inflationary expectations, explain both the consumer and wage channels. Emphasise how expectations become self-fulfilling and why central bank credibility matters for managing them.

Imported inflation

Imported inflation occurs when price increases are transmitted to Australia through international transactions. This reflects Australia's integration with the global economy.

Sources of imported inflation

Rising import prices: When overseas suppliers raise prices, Australian consumers and businesses pay more for imported goods and services. These price increases directly contribute to domestic inflation, measured in the Consumer Price Index alongside domestically produced items.

Currency depreciation: A fall in the Australian dollar's value makes imports more expensive in domestic currency terms. If the AUD depreciates by 10%, imported goods become approximately 10% more expensive for Australian buyers, all else equal.

Understanding currency effects:

The relationship between exchange rates and import prices is direct and mechanical. When the Australian dollar depreciates against foreign currencies, each unit of foreign currency becomes more expensive in AUD terms. Since importers must pay foreign suppliers in foreign currency, they need more Australian dollars to purchase the same quantity of imports. This cost increase is typically passed on to Australian consumers through higher prices.

For example, if a product costs US$100 and the exchange rate moves from 0.70 to 0.63 (AUD depreciation), the Australian dollar price rises from approximately $143 to $159—an increase of over 11%.

Pass-through effects

The extent to which import price rises translate into higher consumer prices depends on market conditions. When imports face competition from locally produced alternatives, importers may absorb some costs by reducing profit margins rather than passing the full price increase to consumers. However, when imports dominate a market or face little competition, price increases are more likely to be fully passed through.

Growing significance

Research by the Reserve Bank in 2015 found that imported inflation now accounts for a much larger share of variability in headline inflation than in previous decades. This reflects Australia's deeper integration with global markets through trade and investment.

The 2022–2023 inflation surge illustrated imported inflation's impact. Soaring fuel import prices directly affected households and raised production costs across industries. Global supply chain disruptions increased prices for manufactured goods and components. These external price shocks significantly contributed to Australia's highest inflation rates in decades.

Exam tip: Link imported inflation to exchange rate movements and terms of trade. Explain how currency depreciation amplifies the effect of overseas price rises. Consider market structure when analysing pass-through rates.

Other causes of inflation

Beyond the four main types, two additional factors can contribute to inflation in Australia.

Government policies

Government decisions directly influence price levels through several channels:

Indirect taxes: Changes to the Goods and Services Tax (GST), excise duties, or other consumption taxes immediately affect prices. The introduction of the GST in 2000 raised headline inflation sharply to 6.1% in 2001 as the 10% tax was added to most goods and services.

Regulatory measures: Government policies on competition, tariffs, price controls, and minimum wages all affect pricing. For example, during the COVID-19 lockdown in 2020, making childcare free for parents reduced the headline inflation rate below zero. Fair Work Commission decisions on minimum wages similarly influence labour costs and potentially inflation.

Competition policy: Regulatory reforms that increase or decrease market competition affect firms' pricing power and therefore inflation outcomes.

Worked Example: GST Impact on Inflation

When the GST was introduced in July 2000, it provided a clear example of policy-driven inflation:

Step 1: The 10% GST was applied to most goods and services Step 2: Businesses added this 10% tax to prices paid by consumers Step 3: The Consumer Price Index recorded these higher prices Result: Headline inflation rose sharply to 6.1% in 2001, with the GST accounting for approximately 2.8 percentage points of this increase

This demonstrates how government policy can directly and immediately affect the price level, even without changes in demand or production costs.

Excessive money supply growth

When money supply growth outpaces economic output growth, inflation can result. This occurs because:

- More money circulates in the economy chasing the same quantity of goods and services

- The increased money supply effectively raises aggregate demand relative to supply

- Prices rise to equate the nominal value of money with the real value of output

- This process is sometimes termed "monetary inflation"

The money supply mechanism:

Excessive money supply growth creates inflation through a straightforward channel. When the central bank increases the money supply faster than the economy produces goods and services, there is more money chasing the same amount of output. This excess liquidity increases aggregate demand without a corresponding increase in aggregate supply, leading to higher prices.

The relationship can be understood through the equation of exchange: , where is money supply, is velocity, is the price level, and is real output. If grows faster than (assuming stable ), then must rise.

Recent Australian example: During the COVID-19 pandemic, the Reserve Bank's quantitative easing program purchased almost $300 billion of government bonds from November 2020 to February 2022. This dramatically increased the money supply and reduced interest rates to support the economy during recession.

Research by the Bank for International Settlements in 2023 found that countries with high money supply growth during the pandemic experienced significantly higher subsequent inflation. While quantitative easing supported Australia's economic recovery, by early 2022 it had contributed to rising inflationary pressures. The Reserve Bank then began "quantitative tightening" to withdraw excess liquidity from the financial system.

Exam tip: When discussing money supply and inflation, explain the transmission mechanism clearly. Show how excess money growth translates into higher aggregate demand. Reference specific examples like quantitative easing to demonstrate understanding of real-world applications.

Historical patterns and recent trends

Different types of inflation dominate in different economic periods:

1970s–1980s: Cost-push inflation and inflationary expectations were prominent. Wage-price spirals created persistent inflation as workers demanded higher wages to compensate for inflation, which then fed back into higher prices.

Late 1980s: Demand-pull inflation predominated as strong economic growth and consumer confidence pushed spending beyond the economy's capacity.

2000s: The commodities boom increased business investment and consumer confidence, creating demand-pull pressures. The GST introduction in 2000 provided an example of policy-driven inflation.

2010s: Persistently low wage growth subdued inflationary expectations. Slower economic growth weakened demand-pull pressures, resulting in below-target inflation for extended periods.

2020–2023: The COVID-19 recession initially created deflationary pressures, with the first annual decline in inflation since the 1960s. However, the global recovery unleashed multiple inflationary forces: supply chain disruptions, high commodity prices, low unemployment, wage growth, rising rents, and surging energy prices from the Ukraine war. Australia's headline inflation peaked at 7.8% in December 2022, while underlying inflation reached 6.3%.

By 2023, the Reserve Bank noted that short-term inflation remained elevated but declining, while long-term expectations stayed anchored within the target band. This suggested market confidence that inflationary pressures would moderate over time, demonstrating the importance of managing expectations even during periods of high inflation.

Remember!

Key points:

- Demand-pull inflation occurs when spending exceeds the economy's productive capacity, causing consumers to bid up prices for limited goods and services

- Cost-push inflation arises from rising production costs (wages, raw materials) that firms pass on to consumers through higher prices

- Inflationary expectations become self-fulfilling as anticipated inflation shapes consumer purchases and wage negotiations, creating actual inflation

- Imported inflation is transmitted through rising import prices and currency depreciation, with increasing significance due to globalisation

- Government policies (taxes, regulations) and excessive money supply growth can also drive inflation

Key terms:

- Aggregate demand and supply

- Productive capacity

- Factors of production

- Self-fulfilling prophecy

- Pass-through effects

- Quantitative easing and tightening

- Wage-price spiral

Critical framework:

Use AS-AD diagrams to distinguish demand-pull (rightward AD shift) from cost-push (leftward AS shift) inflation. Analyse which type predominates in different economic scenarios.

Exam technique:

When asked to "discuss" inflation causes, evaluate the relative importance of different types in the given context. Use specific Australian examples and recent data to support your analysis. Connect inflation causes to appropriate policy responses (monetary or fiscal policy). Always explain transmission mechanisms clearly rather than simply listing causes.