Current and Recent Fiscal Policy (HSC SSCE Economics): Revision Notes

Current and Recent Fiscal Policy

Overview of Australia's fiscal policy approach

Fiscal policy typically plays a supporting role in managing the economy. For most of the business cycle, monetary policy acts as the primary tool for macroeconomic management. Governments prioritise medium-term fiscal goals when the economy is growing steadily, rather than using the budget to influence short-term economic activity.

However, during major economic downturns—which occur roughly once per decade—governments use fiscal policy actively to restore economic growth. Recent examples include responses to the Global Financial Crisis (2008) and the COVID-19 pandemic (2020).

The relationship between fiscal and monetary policy is complementary: monetary policy (controlled by the Reserve Bank) handles day-to-day economic management through interest rates, while fiscal policy (controlled by the government through the budget) provides powerful support during severe economic crises when monetary policy alone is insufficient.

Net public sector debt trends

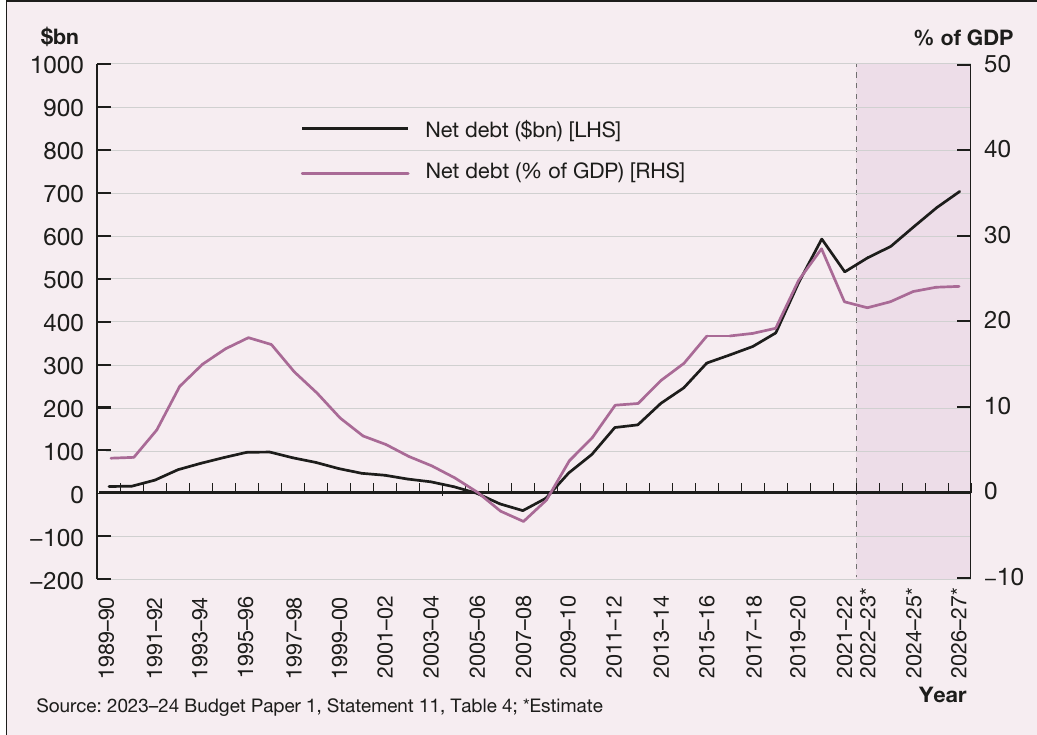

Australia's net public sector debt has varied significantly over recent decades. The government briefly achieved negative net debt (that is, net assets) in the mid-2000s. Following the Global Financial Crisis, net debt increased sharply, and the COVID-19 pandemic caused another substantial rise.

Key distinction: Public sector debt differs from foreign debt. Foreign debt includes borrowings by both public and private sectors from overseas lenders. Australia's foreign debt is much higher than public debt, with most consisting of private sector borrowings. The government generally borrows domestically in Australian dollars, avoiding exchange rate risks that could increase debt servicing costs.

Fiscal strategy before COVID-19

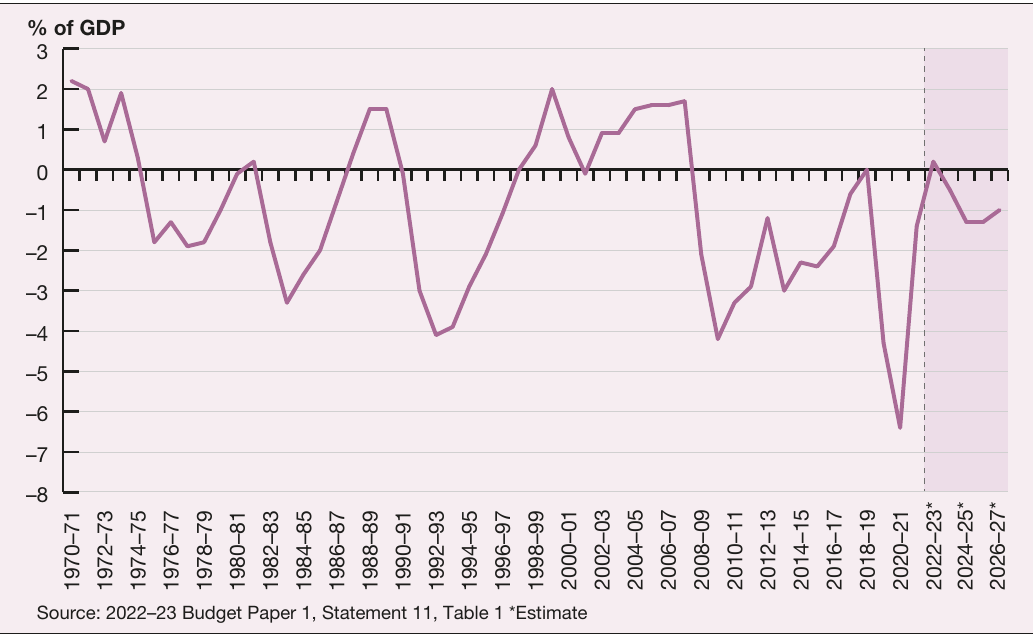

Between 2013 and 2019, the Coalition Government aimed to achieve budget surpluses. However, it only managed to balance the budget once, in 2018-19. The government also committed to keeping tax receipts below 23.9% of GDP.

During the 2010s, the budget outcome improved gradually but more slowly than in previous recoveries. This slower progress occurred because government expenditure continued rising as a share of GDP, despite commitments to offset new spending with cuts elsewhere. Tax revenue recovery was also slow, meaning it took 10 years after the Global Financial Crisis for the budget to return to balance.

The slow recovery in the 2010s contrasted sharply with previous post-recession periods. This prolonged adjustment reflected both rising expenditure commitments (particularly in social services) and weaker-than-expected tax revenue growth, highlighting the challenges of returning to budget balance without strong economic growth.

The COVID-19 fiscal response

The pandemic prompted a dramatic shift in fiscal strategy with long-lasting effects. The Morrison Government introduced comprehensive policies to cushion the economic impact of lockdowns and business closures.

Major policy measures included:

- JobKeeper Payment: a wage subsidy that at one point supported approximately one-third of the workforce

- Direct cash support payments to households

- Investment allowances for businesses

- Industry support measures

- Increased health and infrastructure expenditure

This aggressive expansionary stance caused significant budget deterioration. After being balanced in 2018-19, the budget recorded a deficit of $134 billion (6.5% of GDP) in 2020-21. Net public sector debt increased by nearly 50% in just two years, rising from 19.2% to 28.6% of GDP between 2018-19 and 2020-21.

This deterioration resulted from both discretionary policy measures (like JobKeeper) and automatic stabilisers (lower tax receipts and increased welfare payments). The combined impact was unprecedented in Australia's modern economic history.

Recovery and current fiscal stance

As economic recovery reduced unemployment from 2021-22 onwards, fiscal policy became mildly contractionary. The medium-term strategy focused on sustaining growth, stabilising and reducing debt, and advancing longer-term government priorities.

The Albanese Government's approach differs from previous strategies by not explicitly targeting a return to surplus. Instead, it commits to improving the budget balance over time while reducing debt as a share of the economy.

Cyclical factors influencing recent fiscal policy

Four key cyclical influences:

- Slow pre-pandemic recovery: Economic growth below the medium-term rate and consistently below-forecast wage growth resulted in slower tax receipt growth.

- COVID-19 downturn: The fastest economic contraction since the Great Depression triggered automatic stabilisers. Treasury estimated cyclical factors caused a $105 billion budget deterioration over 2019-20 and 2020-21.

- Terms of trade improvement: Strong commodity prices—particularly iron ore and liquefied natural gas—provided a positive cyclical influence. The budget temporarily returned to surplus in 2022-23 due to revenues from the commodity price surge following Russia's invasion of Ukraine.

- Faster-than-expected recovery: Better economic performance improved budget outlook through persistently high iron ore prices, increased income tax receipts, lower unemployment benefit payments, and lower-than-expected costs for COVID-19 policies. The 2023-24 Budget forecast a $67 billion increase in tax receipts over two years.

Cyclical factors can work both ways: negative shocks (like COVID-19) dramatically worsen budget outcomes, while positive developments (like commodity price surges) can temporarily improve them. This volatility makes medium-term fiscal planning challenging, as governments must distinguish between temporary cyclical effects and permanent structural changes.

Structural factors influencing recent fiscal policy

Three key structural influences:

- Trend increase in government spending: Federal government spending rose from 22.5% of GDP in 2013-14 to 24.9% in 2018-19. This reflected sustained real increases across defence, the National Disability Insurance Scheme (NDIS), unemployment benefits, education, healthcare, and aged care.

- Tax policy changes: During the mining boom, governments implemented large personal income tax reductions that reduced revenue growth after the Global Financial Crisis. The 2018-19 Budget introduced phased personal income tax reductions through to 2024-25, expected to reduce revenue by over $30 billion annually once fully implemented.

- Ageing population: Population ageing contributes to slower revenue growth (more retirees) and increased spending pressures (healthcare and aged care). The Parliamentary Budget Office estimated that by the late 2020s, aged care needs would add $36 billion per year to government spending—more than the total annual expenditure on Medicare.

Unlike cyclical factors that reverse with economic recovery, structural factors represent permanent changes to the budget landscape. The combination of rising spending commitments (particularly NDIS and aged care) and constrained revenue growth creates long-term fiscal challenges that require sustained policy responses.

Looking ahead: the 2023 Intergenerational Report

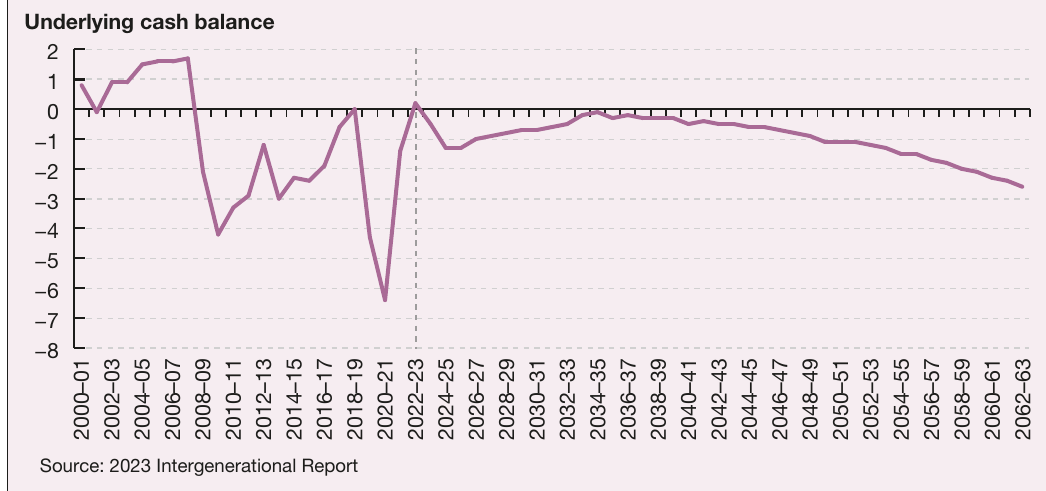

The Intergenerational Report (IGR) provides 40-year economic and fiscal projections, updated approximately every five years. The 2023 IGR projected economic trends to 2062-63.

Key projections:

Real Gross National Income (GNI) per person will grow at 1.0% annually over the next 40 years, compared to 2.1% in the preceding 40 years. Living standards will be 50% higher by 2063, but annual growth will be half the historical rate. This slower growth reflects expected lower terms of trade gains, leaving the economy reliant on the "three Ps":

- Productivity: Assumed to grow at 1.2% annually, similar to the past 20 years but below the 30-year average of 1.5%.

- Participation: Projected to decline from 66.8% in 2023 to 63.8% by 2062-63, primarily due to population ageing. This decline is milder than earlier projections, partially offset by continued increases in women's workforce participation.

- Population: Projected to reach 40.5 million by 2062-63, with 1.1% annual growth (below historical average) due to lower fertility rates and migration levels.

The IGR projected the budget to remain in deficit every year until 2062-63. Budget outcomes are expected to improve during the 2020s but worsen from the 2030s as spending pressures increase for health, aged care, NDIS, defence, and debt interest payments. The government's ceiling on tax revenues prevents revenue from keeping pace with expenditure growth.

Impact on economic growth

Since the 1990s, fiscal policy has only actively managed economic cycles during major downturns. The introduction of inflation targeting meant monetary policy became the primary demand management tool. The 2023 Review of the Reserve Bank concluded this strategy had been effective and should continue.

Before 2020, fiscal policy's limited role was reflected in long-term tax reduction plans. The Morrison Government legislated reductions in business and personal tax rates, aiming to provide incentives for work, investment, and job creation by allowing individuals and companies to retain more of their income and profits.

The pandemic changed this dramatically. Based on Keynesian economic theory, the government used expansionary fiscal policy to accelerate growth. Treasury estimated that government budget measures (up to July 2020) would result in economic activity being 4.5% higher in 2021-22 than otherwise.

Key COVID-19 investment measures:

- Immediate expensing: Allowed businesses to write off the full cost of investments immediately, rather than claiming depreciation over 5-10 years

- Loss carry-back: Enabled businesses to claim refunds against tax paid in previous years by carrying back current losses

The 2023-24 Budget aimed to manage conflicting objectives: reducing inflationary pressures while supporting households struggling with cost-of-living challenges. Cost-of-living measures included electricity bill subsidies and wholesale energy price caps. Treasury estimated these would reduce headline inflation by 0.75 percentage points in 2023-24, potentially reducing the need for further interest rate increases.

Impact on unemployment and workforce participation

Expansionary fiscal policy stimulates aggregate demand, helping to reduce unemployment or moderate cyclical unemployment increases during downturns. The primary goal of COVID-19 fiscal measures was preventing large-scale unemployment.

Worked Example: JobKeeper's Impact on Unemployment

The JobKeeper Payment subsidised wages for approximately 3.5 million Australians at a cost of $90 billion. Treasury estimated this prevented a 5 percentage point rise in unemployment.

Without preventing these job losses, the recession would have been much longer and more severe, given the time required for recruitment and job-seeking. This demonstrates how targeted fiscal policy can stabilise labour markets during economic shocks.

With unemployment falling rapidly after the pandemic, fiscal policy's labour market role returned to pre-pandemic priorities: addressing skills shortages, fostering career transitions, and retraining older workers.

Recent labour market measures:

- Australian Apprenticeships Incentive System ($2.8 billion): Streamlined apprenticeships and created places in priority areas

- Skills and Training Boost ($550 million): Provided 20% bonus tax deductions for small businesses upskilling employees

- Child Care Subsidy increase ($4.7 billion): Increased subsidies to 90% for eligible families, improving work incentives for second-income earners

- Paid Parental Leave expansion ($532 million): Extended leave to 26 weeks from 2026

Impact on resource allocation

Governments now influence resource allocation less actively than in the past. Beyond correcting market failures, they generally rely on market forces for efficient resource allocation. During the 1990s and after, most public trading enterprises were privatised, direct industry subsidies declined to under $4 billion annually, and governments allowed some industries to close entirely (like car manufacturing in 2013).

However, some expenditure areas still significantly affect resource allocation:

- Clean energy transition: The 2023-24 Budget allocated an additional $4 billion for renewable energy, bringing total funding commitments to $40 billion

- Defence industry: Tens of billions committed to building submarines in Australia under the AUKUS alliance

Governments also influence resource allocation through regulations, tax concessions, and exemptions. The Renewable Energy Target successfully required approximately 23% of energy generation to come from renewable sources by 2020, demonstrating how policy frameworks can reshape industry structure without direct spending.

Impact on national savings and the current account

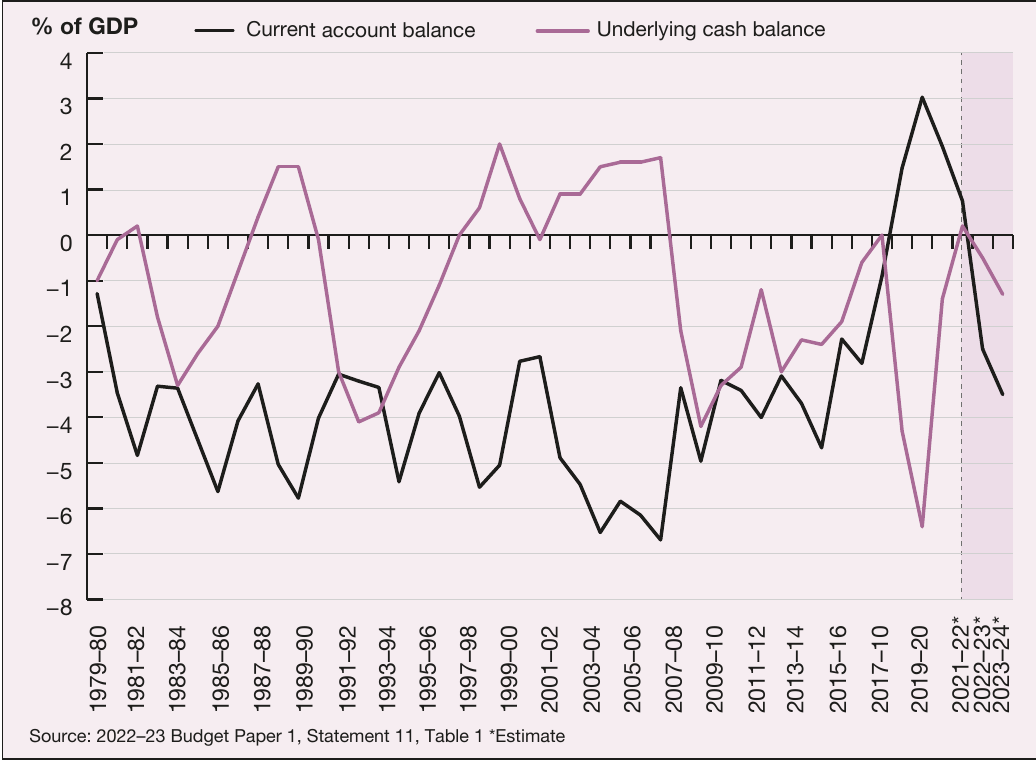

Fiscal policy influences national savings through budget surpluses (increasing savings) or deficits (detracting from savings). Rather than directly addressing Australia's large current account deficit, recent government strategy has pursued medium-term budget surpluses so the government doesn't add to the savings imbalance. Over time, this should help improve external balance.

The "twin deficits" hypothesis—suggesting budget deficits lead to current account deficits—has been debated in Australia since the 1980s. In reality, many factors influence the current account, with budget deficits being just one.

The chart shows no direct linkage between budget outcomes and current account deficits. Sometimes the current account deficit increases during sustained budget surpluses (mid-2000s). At other times, the current account moves to surplus while the budget moves sharply into deficit (recent years).

This reflects that while budget outcomes influence national savings, and national savings influence external balance, many other factors are simultaneously at work. Nevertheless, higher public savings (lower budget deficit) likely results in a lower current account deficit over the long term—though the relationship is long-term, not short-term, and influenced by many factors.

Impact on income distribution

Fiscal policy decisions significantly impact income distribution, with distributional effects often central to budget policy debates. The budget affects distribution through specific tax and revenue measures, as well as through broader impacts on economic conditions.

COVID-19 distributional measures:

The government aimed to prevent large-scale job losses that could widen income inequality:

- JobKeeper Payment: Subsidised wages for 3.5 million Australians ($90 billion)

- Coronavirus Supplement: Temporarily increased unemployment benefits by $550 per fortnight ($16.8 billion) with relaxed access requirements

- Direct cash support: $1,500 payments to pensioners, income support recipients, carers, and students ($9.4 billion)

These measures provided assistance to lower-income earners.

2023-24 cost-of-living support:

- $3 billion in electricity bill subsidies for five million households

- $20 per week increase in JobSeeker payment

- 15% increase in rent assistance payments

Concerns about tax progressivity:

The income tax reductions phased in from the late 2010s to 2024-25 were widely criticised for making the tax system less progressive. The Grattan Institute's 2019 analysis concluded the tax package would make Australia's system the least progressive since the 1950s.

Key findings:

- Middle-income earners would see tax rates increase by 3.7% by 2030

- The top 15% of income earners would see tax rates fall by 1%

- Middle-income earners' share of total income tax paid would rise from 32% (2017-18) to 35% (2029-30)

- Australia would fall from 12th to 19th in OECD rankings for tax system progressivity by 2024-25

Remember!

Key Takeaways:

-

Fiscal policy typically plays a supporting role to monetary policy, but becomes critical during major economic downturns like the Global Financial Crisis and COVID-19 pandemic

-

The COVID-19 fiscal response was unprecedented, with measures like JobKeeper causing the budget deficit to reach 6.5% of GDP in 2020-21, but successfully preventing much larger unemployment increases

-

Both cyclical factors (like terms of trade and economic recovery speed) and structural factors (like ageing population and spending commitments) influence budget outcomes

-

The 2023 Intergenerational Report projects ongoing budget deficits until 2063, with future growth reliant on the "three Ps": productivity, participation, and population

-

Recent fiscal policy has significantly impacted economic growth, unemployment, resource allocation, national savings, and income distribution, though debates continue about the appropriate balance between these objectives