Fiscal Policy and Budget Outcomes (HSC SSCE Economics): Revision Notes

Fiscal Policy and Budget Outcomes

Understanding budget outcomes is central to analysing how government fiscal policy affects the economy. The budget outcome reflects the overall balance between government revenue and expenditure, providing insight into the fiscal stance and its economic impact.

What is a budget outcome?

The budget outcome shows the net financial position of the Commonwealth Government's budget. It indicates whether the government is spending more or less than it collects in revenue during a financial year.

The budget outcome itself acts as an important instrument of fiscal policy, giving an indication of fiscal policy's overall impact on the economy.

Types of budget outcomes

There are three possible budget outcomes that determine the government's fiscal position:

Budget surplus

A budget surplus occurs when total government revenue exceeds total government expenditure. This can be expressed as:

where = total government revenue and = total government expenditure.

A surplus means the government is collecting more in taxes and other revenue than it is spending. This withdraws funds from the economy and represents a contractionary fiscal position.

Budget deficit

A budget deficit occurs when total government expenditure exceeds total government revenue:

A deficit means the government is spending more than it collects. This injects additional funds into the economy and represents an expansionary fiscal position. The government must borrow to finance the deficit.

Balanced budget

A balanced budget occurs when total government revenue equals total government expenditure:

A balanced budget means government spending exactly matches revenue collection. This represents a neutral fiscal position with no net injection or withdrawal from the economy.

Key Relationship:

The relationship between (total government revenue) and (total government expenditure) determines the budget outcome and indicates the government's fiscal stance. This is fundamental to understanding fiscal policy's impact on aggregate demand.

Measuring the budget outcome

The Commonwealth Government uses four different methods to measure the budget outcome. Each provides different insights into the fiscal position and serves distinct analytical purposes.

Underlying cash balance

The underlying cash balance is the government's preferred measure of the budget outcome. It shows the short- to medium-term impact of fiscal policy on economic activity.

Key features of this measure include:

- Uses cash accounting (records transactions when money actually changes hands)

- Shows the budget's immediate call on cash resources from other economic sectors

- Does not distinguish between capital spending (e.g. infrastructure) and recurrent spending (e.g. wages)

- Excludes net Future Fund earnings until superannuation liabilities are met

Limitation of Cash Accounting

Cash accounting doesn't reflect international accrual accounting standards and may not capture the full economic picture. This is because it only records transactions when money physically changes hands, potentially missing important economic obligations or commitments.

Headline cash balance

The headline cash balance equals the underlying cash balance plus net cash flows from government investments in financial assets and net Future Fund earnings.

This measure can differ significantly from the underlying cash balance due to one-off transactions:

- Asset sales (e.g. privatisations) increase the headline balance

- Asset purchases decrease the headline balance

Impact of Asset Sales:

Asset sales reduce the government's borrowing requirement but also mean lost future dividend income from those assets. This represents a trade-off between short-term budget improvement and long-term revenue capacity.

Fiscal balance

The fiscal balance calculates revenue minus expenses less net capital investment, using accrual accounting.

Key features of this measure include:

- Uses accrual accounting (records transactions when incurred/earned, not when cash changes hands)

- Provides a more accurate economic picture

- Still doesn't distinguish between capital and day-to-day spending

Worked Example: Accrual Accounting in Practice

If government superannuation obligations to public servants increase by $5 billion in one year, this increases the fiscal deficit by $5 billion immediately, even though the actual cash payment won't occur until years later.

This demonstrates how accrual accounting captures economic obligations when they are incurred, providing a more comprehensive view of the government's financial position.

Net operating balance

The net operating balance is considered the best measure of budget sustainability. It shows whether the government is meeting its recurrent (day-to-day) obligations from current revenue.

Key features that distinguish this measure:

- Uses accrual accounting

- Distinguishes between capital spending and recurrent spending

- Removes capital spending from the balance (resulting in a smaller deficit or larger surplus)

- Includes depreciation costs (the decline in value of existing assets)

Why This Distinction Matters

Separating capital from recurrent spending makes sense because capital spending adds to productive capacity and government assets, whereas recurrent spending must be funded from ongoing revenue. This allows for a clearer assessment of fiscal sustainability over time.

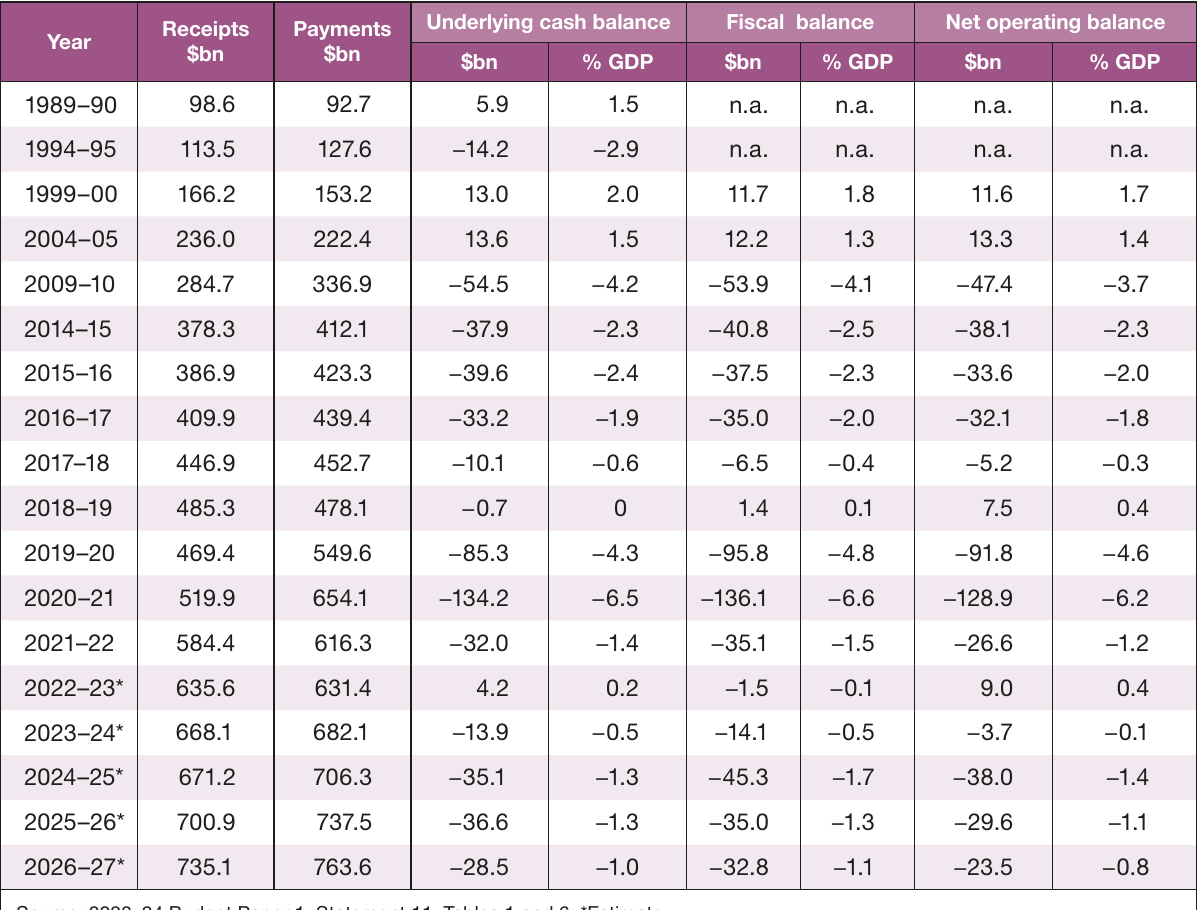

Historical budget outcomes

The historical data reveals several important trends in Australian fiscal policy that reflect the government's response to different economic conditions:

Early period (1989-90 to 2004-05)

The budget moved from surplus to deficit in the mid-1990s, then returned to sustained surpluses from 1999-2000 onwards. Surpluses averaged around 1-2% of GDP during the early 2000s, reflecting strong economic growth and disciplined fiscal management.

Global financial crisis impact (2009-10)

The underlying cash balance fell to a deficit of $54.5 billion (4.2% of GDP). This represented a significant expansionary fiscal response to the economic downturn, with all three measures showing substantial deficits.

The GFC response demonstrated how fiscal policy can be used aggressively to support economic activity during severe downturns, with the government accepting large deficits to stimulate aggregate demand.

Recovery and deterioration (2010-2019)

Deficits persisted through the 2010s but gradually improved. By 2018-19, the budget was close to balance, with the underlying cash balance showing a small deficit of $0.7 billion. This period reflected the slow recovery from the GFC and efforts to return to surplus.

COVID-19 pandemic impact (2019-20 to 2021-22)

The budget deficit exploded to $134.2 billion in 2020-21 (6.5% of GDP). This was even larger than the GFC response, as massive fiscal stimulus was deployed to support the economy during lockdowns. Recovery began in 2021-22 with the deficit reducing to $32.0 billion.

The COVID-19 fiscal response was unprecedented in scale, exceeding even the GFC stimulus. This demonstrated the government's willingness to accept very large deficits during economic crises to protect employment and incomes.

Recent and projected outcomes (2022-23 onwards)

A brief return to surplus in 2022-23 ($4.2 billion) was followed by projected return to deficit from 2023-24. Expected deficits of around 1-1.5% of GDP in the medium term reflect ongoing spending pressures and uncertain economic conditions.

The government's fiscal objective

The Commonwealth Government aims to achieve budget surpluses on average over the course of the economic cycle. This counter-cyclical approach means:

- Running surpluses during periods of strong economic growth

- Accepting deficits during economic downturns

- Balancing out over the full business cycle

The Treasury provides four-year forward projections and ten-year medium-term projections to track progress toward this objective. This allows for assessment of fiscal sustainability and policy planning over different time horizons.

Changes in budget outcomes

Budget outcomes change from year to year due to two distinct types of factors. Understanding the difference is crucial for analysing fiscal policy and its effectiveness.

Discretionary changes (structural component)

Discretionary changes involve deliberate government policy decisions to alter spending or taxation. These are conscious choices made by the government to influence economic activity.

Examples of discretionary changes include:

- Changing tax rates or introducing new taxes

- Increasing or cutting government spending programs

- Introducing new welfare payments or infrastructure projects

- Modifying tax concessions or rebates

These changes affect the structural component of the budget outcome. They reflect the government's active use of fiscal policy to achieve economic objectives such as stimulating growth or controlling inflation.

Worked Example: Discretionary Fiscal Stimulus

If the government deliberately increased infrastructure spending by $10 billion to stimulate demand during a recession, this would be a discretionary expansionary measure.

This represents a policy decision to inject additional spending into the economy, increasing aggregate demand through both direct government expenditure and multiplier effects.

Non-discretionary changes (cyclical component)

Non-discretionary changes occur automatically as a result of changes in economic conditions, without any deliberate policy change. The government does not need to make new decisions for these changes to occur.

These changes affect the cyclical component of the budget outcome. They occur because government revenues and expenditures are naturally sensitive to the level of economic activity.

Key Principle:

When the economy grows strongly, the budget outcome automatically improves. When the economy contracts, the budget outcome automatically deteriorates. This happens without any new policy decisions being made.

Automatic stabilisers

Automatic stabilisers are the specific mechanisms through which non-discretionary changes occur. They are built into the budget and activate automatically when economic conditions change, without requiring new government decisions.

The two main automatic stabilisers that operate in the Australian economy are:

1. Unemployment benefits

Unemployment benefits respond automatically to changes in the unemployment rate, providing counter-cyclical support.

During a recession:

- Economic activity falls

- Unemployment rises

- More people claim unemployment benefits

- Government expenditure automatically increases

During a boom:

- Economic activity rises

- Unemployment falls

- Fewer people claim unemployment benefits

- Government expenditure automatically decreases

This automatic response helps stabilise aggregate demand without requiring any policy decisions. As unemployment rises, increased benefit payments partially offset the fall in household income, supporting consumption spending.

2. Progressive income tax system

Australia's progressive tax system means people on higher incomes pay proportionally higher tax rates. This creates automatic stabilisation through the tax side of the budget.

During a boom:

- Employment and incomes rise

- Workers move into higher tax brackets

- Previously unemployed people start paying tax

- Tax revenue automatically increases

During a recession:

- Employment and incomes fall

- Workers may drop to lower tax brackets

- Some workers lose jobs and stop paying tax

- Tax revenue automatically decreases

The progressive nature of the tax system amplifies these stabilising effects. As incomes rise during a boom, not only do more people pay tax, but existing taxpayers move into higher brackets, increasing the average tax rate and withdrawing more from the economy.

The counter-cyclical role

Automatic stabilisers perform a counter-cyclical function that helps moderate economic fluctuations:

In a boom: They automatically slow economic growth by increasing tax revenue and reducing transfer payments. This helps prevent the economy from overheating by dampening aggregate demand.

In a recession: They automatically support economic activity by reducing tax revenue and increasing transfer payments. This helps cushion the economic downturn by supporting household incomes and consumption.

Important Limitation:

While automatic stabilisers help moderate economic fluctuations, they are rarely powerful enough on their own to fully counteract severe recessions or booms. Governments still need to use discretionary policy measures for effective macroeconomic management, as demonstrated during the COVID-19 pandemic when massive discretionary stimulus was required beyond the automatic stabilisers.

Budget stance and economic impact

The budget stance describes how fiscal policy affects the level of economic activity. It is distinct from the budget outcome itself and focuses on the direction of policy change.

Expansionary stance

An expansionary stance occurs when the government acts to increase economic activity through:

- Reducing taxation revenue, and/or

- Increasing government expenditure

This typically results in:

- A smaller surplus than the previous year, or

- A larger deficit than the previous year

Economic Effect:

Expansionary policy creates a multiplied increase in consumption and investment, stimulating aggregate demand and boosting economic growth. The initial injection of spending or tax cuts generates additional rounds of spending through the multiplier effect.

Contractionary stance

A contractionary stance occurs when the government acts to decrease economic activity through:

- Increasing taxation revenue, and/or

- Decreasing government expenditure

This typically results in:

- A larger surplus than the previous year, or

- A smaller deficit than the previous year

Economic Effect:

Contractionary policy creates a multiplied decrease in consumption and investment, dampening aggregate demand and slowing economic growth. This may be used to control inflation or reduce excessive economic growth.

Neutral stance

A neutral stance maintains approximately the same gap between revenue and spending as the previous year.

Economic Effect:

Neutral policy should have no significant impact on the overall level of economic activity, maintaining the existing fiscal position relative to GDP.

Understanding Budget Stance:

The budget stance depends on the change in the budget position, not the absolute level. For example, increasing a deficit from $20 billion to $30 billion represents an expansionary stance, even though both years show deficits. This is because the government is injecting additional stimulus into the economy.

Exam technique: analysing budget outcomes

Exam Analysis Framework:

When analysing budget outcomes in exam questions, follow this systematic approach:

-

Identify the type of outcome: State whether it's a surplus, deficit, or balanced budget, and quote figures as both dollar amounts and percentage of GDP.

-

Examine the measurement: Consider which measure is being used and why it matters. The underlying cash balance shows short-term impact, while the net operating balance indicates sustainability.

-

Distinguish discretionary from non-discretionary factors: Analyse whether changes resulted from deliberate policy decisions or automatic responses to economic conditions.

-

Link to economic conditions: Explain how the budget outcome relates to the economic cycle. Large deficits during recessions reflect both discretionary stimulus and automatic stabilisers.

-

Assess the stance: Determine whether fiscal policy is expansionary, contractionary, or neutral by comparing outcomes across years, not just looking at the absolute position.

-

Consider sustainability: Use the net operating balance to evaluate whether the government can sustain its spending patterns from current revenue.

Remember!

Key Points to Remember:

-

Budget outcomes can be a surplus (), deficit (), or balanced ()

-

The four measures provide different perspectives: underlying cash balance (short-term impact), headline cash balance (includes asset transactions), fiscal balance (accrual accounting), and net operating balance (sustainability)

-

Budget outcomes change due to discretionary factors (deliberate policy decisions affecting the structural component) and non-discretionary factors (automatic responses to economic conditions affecting the cyclical component)

-

Automatic stabilisers (unemployment benefits and progressive taxation) create counter-cyclical effects that help moderate economic fluctuations without requiring policy changes

-

The budget stance (expansionary, contractionary, or neutral) depends on the change in the budget position, not the absolute level, and indicates fiscal policy's impact on aggregate demand