Methods of Financing a Deficit (HSC SSCE Economics): Revision Notes

Methods of Financing a Deficit

Introduction

When a government plans to spend more than it receives in revenue during a financial year, it faces a budget deficit. This creates a funding gap that must be addressed through various financing methods. Understanding how governments finance deficits is crucial for analyzing fiscal policy's impact on the economy.

Understanding deficit financing methods is essential for comprehending how government fiscal policy affects economic growth, interest rates, and investment opportunities in the economy.

The Australian Government has several options available when financing a deficit:

- Borrowing from the domestic private sector

- Borrowing from overseas investors

- Borrowing from the Reserve Bank (printing money)

- Selling government-owned assets

In recent decades, the Australian Government has predominantly relied on borrowing from the domestic private sector to finance budget deficits.

Borrowing from the private sector

Treasury bonds and the tender system

The primary method for deficit financing involves selling Treasury Bonds to the domestic private sector through a competitive tender system. This process works as follows:

The government determines the total value of bonds it needs to sell, based on the size of the deficit requiring finance. Financial institutions and investors then submit tenders, indicating how much they wish to purchase and at what interest rate. The government accepts tenders starting with those offering the lowest interest rates, continuing through progressively higher rates until all bonds are sold.

How the Tender System Works

The competitive tender system ensures efficient price discovery in government bond markets. By accepting bids from lowest to highest interest rates, the government secures the best possible borrowing terms while ensuring all required funds are raised.

This system offers two key advantages:

- The government can reliably finance its entire deficit

- Market forces determine the interest rate on newly issued bonds

The crowding out effect

Crowding out effect occurs where government spending is financed through borrowing from the private sector, which puts upward pressure on interest rates and "crowds out" private sector investors who cannot borrow at the higher rates of interest.

Understanding the Crowding Out Mechanism

When the government borrows from domestic sources, it draws funds from Australia's pool of savings. This increased demand for funds can push interest rates upward, making it more expensive for private businesses to borrow. Consequently, private sector investment may decline as firms find borrowing costs prohibitive. Some businesses may need to seek funding from overseas markets instead.

The strength of this crowding out effect varies with economic conditions:

During recessions: The crowding out effect is minimal because private sector investment is typically low during economic downturns. Government borrowing fills the gap left by reduced private sector activity.

During economic expansions: When the economy is growing strongly and private sector investment is already high, government borrowing is more likely to crowd out private investment by competing for limited funds.

The role of overseas investors

In today's globalized financial markets, the crowding out effect has diminished significantly. Many institutions purchasing Australian government bonds on domestic markets are actually overseas-based financial organizations. These international investors are attracted to Australian government securities for several reasons:

- Australia's AAA credit rating reflects low investment risk

- Interest rate differences between Australia and other advanced economies can make Australian securities attractive

- Australia's stable political and economic environment

Globalization and Deficit Financing

The distinction between domestic and overseas borrowing has become increasingly blurred in modern financial markets. Overseas institutions actively participate in Australian bond markets, which helps reduce the crowding out effect on domestic businesses and provides the government with a broader pool of potential lenders.

However, the proportion of Australian government securities held by overseas investors has declined in recent years—from 76% in 2012 to approximately 45% in 2022. This shift occurred as Australia's interest rates became less attractive compared to rates in other countries.

Other methods of financing a deficit

Borrowing from overseas

Governments can raise funds directly from international financial markets, potentially borrowing in foreign currencies. This approach offers the advantage of minimizing the crowding out effect on the domestic economy while still providing economic stimulus.

In the modern era of global finance, the distinction between domestic and international borrowing has become less meaningful, as overseas institutions actively participate in Australian domestic markets. However, if overseas markets offer more favorable terms, the government retains the option to borrow directly from international sources.

When borrowing from overseas:

- The borrowing directly increases Australia's foreign debt

- Interest payments appear as debits on the net primary income account in the balance of payments

- The government must consider exchange rate risks if borrowing in foreign currencies

Borrowing from the Reserve Bank (monetary financing)

Monetary financing or "monetising the deficit" refers to the government borrowing directly from the Reserve Bank, which effectively means printing money to finance government expenditure.

Why Monetary Financing is Avoided

Since the financial sector deregulation in 1982, the Australian Government has not engaged in monetary financing. The key reasons for avoiding this approach include:

- Inflation risk: Printing money increases the money supply, which can fuel inflation

- Policy independence: Avoiding monetary financing ensures fiscal and monetary policies operate independently

- Economic stability: The separation prevents the government from creating money to fund spending, which could destabilize the economy

While fiscal and monetary policies now operate independently, their settings remain indirectly related in terms of overall economic management.

Selling assets

Rather than borrowing, governments can sell publicly-owned assets to raise funds. Examples of such assets include:

- Commonwealth land holdings

- Government stakes in businesses (such as Medibank Private or Australia Post)

- Infrastructure assets

Important Limitations of Asset Sales

Asset sales do not reduce the underlying cash deficit or net operating deficit, as budget calculations adjust for these one-off transactions. However, in cash terms, asset sales can create a headline budget surplus for a particular year.

Worked Example: Asset Sales and the Savings Pool

If the government raises $10 billion through asset sales, it simply needs to issue $10 billion less in Treasury Bonds. However, the overall demand on Australia's savings pool remains essentially unchanged because:

- Asset purchasers either reduce their savings by $10 billion, or

- Asset purchasers borrow $10 billion instead of the government borrowing that amount

The financing burden shifts from the public to the private sector, but the total effect on domestic savings remains similar.

Trade-offs of asset sales:

- Reduces future government borrowing and interest payments

- Eliminates potential dividend income from sold assets

- Does not address the underlying structural deficit

Using budget surpluses

When government revenue exceeds expenditure, a budget surplus results. The government can use surplus funds in three ways:

- Depositing with the Reserve Bank: The surplus can be held as deposits, effectively storing funds for future use

- Paying off public sector debt: Using surpluses to reduce existing debt decreases future interest payments and frees up funds in financial markets for other uses, potentially offsetting the contractionary effect of the surplus through increased private sector investment

- Investing in dedicated funds: Surplus funds can be placed in government-owned investment funds for specific purposes

Worked Example: The Future Fund

During the late 1990s and early 2000s, the Australian Government ran consistent budget surpluses and used these funds to reduce public sector debt. During this period, the government also established the Future Fund—a dedicated investment fund designed to meet the government's future superannuation liabilities.

By 2023, the Future Fund's assets were valued at $251 billion, demonstrating how strategic surplus management can create long-term financial security for future government obligations.

Public sector borrowing and debt

Understanding the full public sector impact

While changes in the Commonwealth Budget provide important signals about fiscal policy, they don't capture the complete picture of public sector activity. Australia's public sector includes:

- Commonwealth Government

- State governments

- Local governments

- Public trading enterprises (government business enterprises) such as Australia Post, Sydney Water, and Sydney Trains

The Comprehensive View of Public Sector Activity

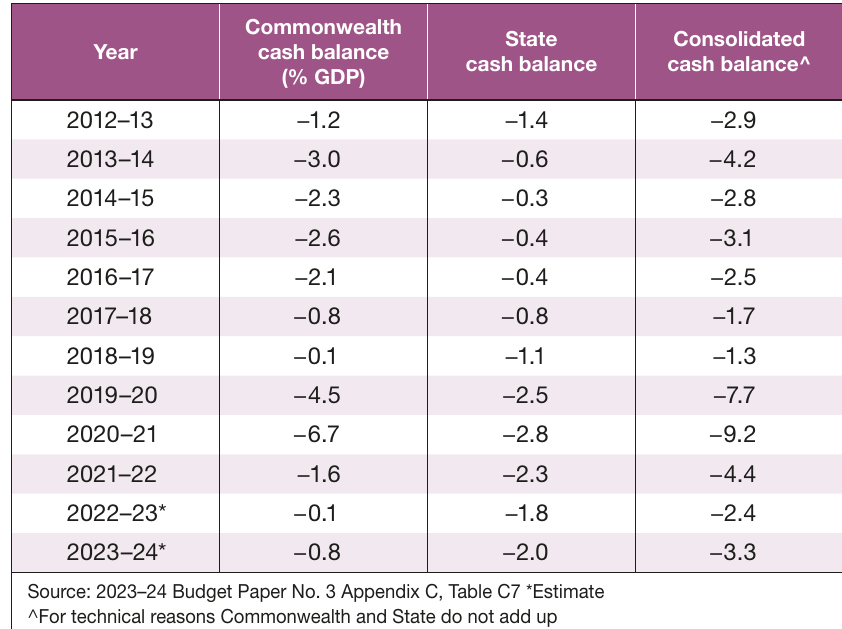

The public sector cash outcome measures the combined deficit or surplus across all these levels, showing total borrowing needs or surplus funds from the entire public sector. This provides the most comprehensive indicator of the public sector's current impact on the Australian economy.

The consolidated cash balance shows the overall public sector position. As the table demonstrates, the public sector has been in deficit throughout most of the period shown, with particularly large deficits during 2019-21 due to the COVID-19 pandemic response.

The net operating deficit reveals that in most years, the public sector's revenue has fallen short of its recurrent spending commitments.

Public sector debt accumulation

Public sector debt consists of the accumulated debt of the government sector, which is owed both domestically and overseas. This includes debt from:

- The Commonwealth Government

- State and local governments

- Government-owned businesses

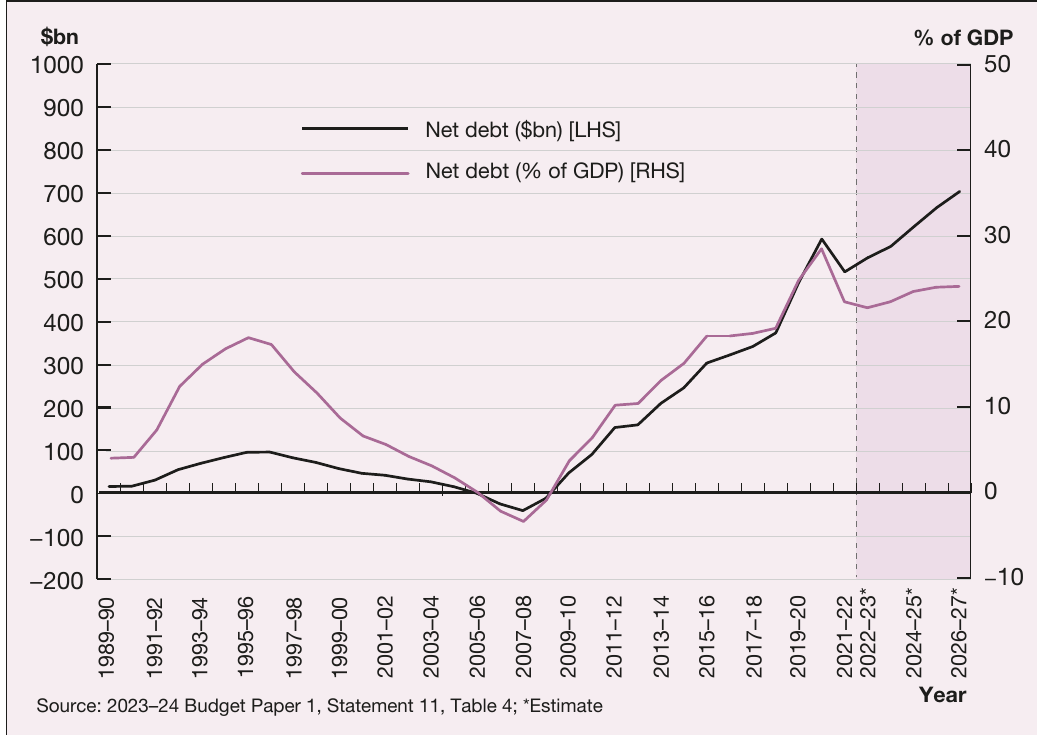

Running public sector deficits over time leads to debt accumulation. As the following chart shows, Australia's public sector debt has increased during three distinct periods:

The chart reveals three periods of significant debt growth:

- After the early 1990s recession

- Following the global financial crisis in 2008

- After the COVID-19 pandemic in 2020

During the late 1990s and early 2000s, sustained budget surpluses enabled the government to reduce public sector debt, even achieving negative net debt (net assets) around 2006-2008. This demonstrates that consistent fiscal discipline can reverse debt accumulation trends.

Public sector debt vs foreign debt

It's essential to distinguish between public sector debt and foreign debt:

- Public sector debt: Money owed by all levels of government

- Foreign debt: Total amount owed by both public and private sectors to overseas lenders

Critical Distinction: Public vs Foreign Debt

Australia's foreign debt significantly exceeds public sector debt, primarily consisting of private sector borrowings. When governments borrow, they typically source funds from domestic markets, although some participants in these markets are overseas-based institutions.

By borrowing on domestic markets in Australian dollars, governments avoid exchange rate exposure that could increase debt and interest servicing costs if exchange rates move unfavorably.

Remember!

Key Points to Remember:

-

The Australian Government primarily finances deficits by selling Treasury Bonds to the domestic private sector through a competitive tender system

-

The crowding out effect occurs when government borrowing pushes up interest rates and reduces private sector access to funds, but this effect is weaker in today's globalized financial markets

-

Monetary financing (printing money) has not been used since 1982 due to inflation concerns and the need to maintain policy independence

-

Selling assets shifts the financing burden from government to the private sector but doesn't reduce the underlying deficit

-

Budget surpluses can be used to deposit with the Reserve Bank, pay off debt, or invest in dedicated funds like the Future Fund

-

The public sector cash outcome provides the most comprehensive measure of all government activity's impact on the economy, including Commonwealth, state, and local governments

-

Public sector debt differs from foreign debt—Australia's foreign debt is much larger and mostly consists of private sector borrowing