The Implementation of Monetary Policy (HSC SSCE Economics): Revision Notes

The Implementation of Monetary Policy

Introduction to the cash rate

The Reserve Bank of Australia (RBA) implements monetary policy primarily through changes to the cash rate. The cash rate is the interest rate charged on overnight loans in the short-term money market – a financial market where banks lend to and borrow from each other, typically for very short periods (often literally overnight).

Why does the cash rate matter? The cash rate serves as the foundation for the entire interest rate structure in the Australian economy. When the RBA changes the cash rate, this influences many other interest rates throughout the economy, including mortgage rates, business loan rates, and personal loan rates. These broader interest rate changes then affect inflation and overall economic activity, allowing the RBA to achieve its economic objectives.

From 2024 onwards, the RBA's Monetary Policy Board meets eight times per year (on the first Monday and Tuesday of specific months) to set the target for the cash rate. The policy decision is announced immediately at the end of each meeting. The RBA then takes responsibility for ensuring the actual cash rate in the overnight money market stays consistent with the announced target.

How the cash rate is determined

Understanding how monetary policy works requires knowledge of three key mechanisms that determine the cash rate:

- Exchange settlement accounts

- The policy interest rate corridor

- Domestic market operations

Exchange settlement accounts

Commercial banks must hold a portion of their funds with the Reserve Bank in special accounts called exchange settlement (ES) accounts. These accounts serve a critical function: they enable banks to settle payments with each other and with the Reserve Bank.

Practical Example: Interbank Payment Settlement

When a Commonwealth Bank customer uses their debit card to purchase something from a business that banks with National Australia Bank, funds must flow from Commonwealth Bank to NAB to complete this transaction. Thousands of such interbank payments occur every day. These payments are processed by transferring funds between the banks' ES accounts at the RBA.

At the end of each trading day, some banks find themselves short of ES funds (they don't have enough to settle all their payment obligations), while other banks have surplus ES funds (more than they need). The overnight money market provides the solution to this imbalance. Banks with excess ES funds can lend to banks that need additional funds. This market ensures all banks can always meet their interbank payment obligations.

Like any financial market, the overnight money market operates through supply and demand. Banks that need funds (demand) interact with banks that have surplus funds (supply), and together they determine the market interest rate – the cash rate. However, unlike most other financial markets, the RBA can directly influence this market to ensure the actual cash rate aligns with the RBA's target rate.

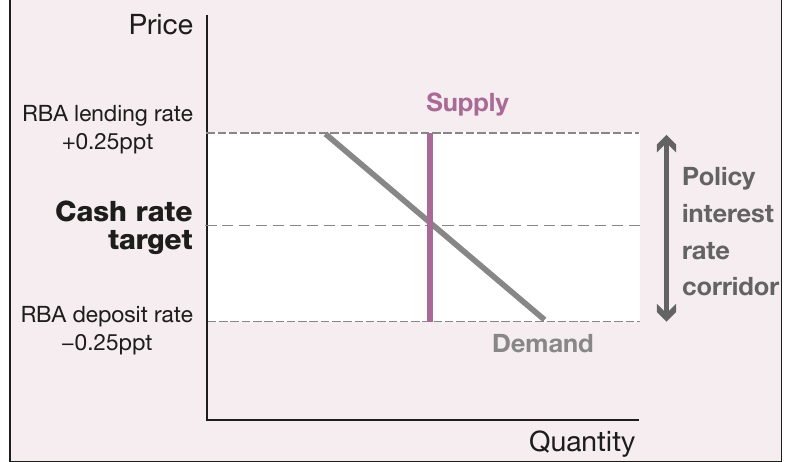

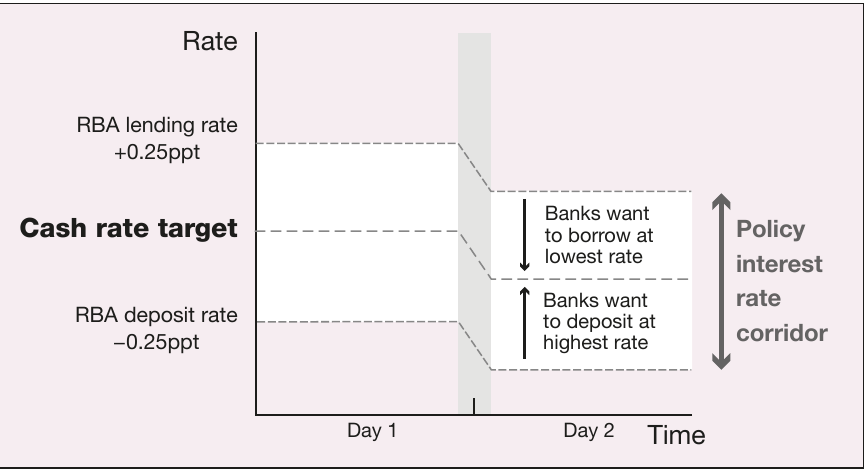

The policy interest rate corridor

The RBA does not directly set the actual cash rate at its announced target. Instead, the RBA uses a clever mechanism called the policy interest rate corridor to ensure the actual cash rate cannot stray far from the target.

The Policy Corridor Boundaries

The corridor works through two boundaries:

The floor (deposit rate): The RBA pays interest to banks on funds held in ES accounts. This interest rate is normally set at 0.25 percentage points below the cash rate target. For example, if the cash rate target is 1.0%, the RBA's deposit rate would be 0.75%.

This creates a floor for the cash rate because banks with excess ES funds have no incentive to lend in the overnight money market at a rate below the deposit rate. Why would they? They can simply leave their surplus funds in their ES account and earn the deposit rate from the RBA. This prevents the actual cash rate from falling more than 0.25 percentage points below the target.

The ceiling (lending rate): The RBA stands ready to lend ES funds directly to banks outside the overnight money market. The interest rate on these loans is always set at 0.25 percentage points above the cash rate target. Using the same example, if the cash rate target is 1.0%, the RBA's lending rate would be 1.25%.

This creates a ceiling for the cash rate because banks needing to borrow ES funds have no incentive to pay more than the RBA's lending rate in the overnight money market. If the cash rate were higher than the RBA's lending rate, banks would simply borrow directly from the RBA instead. This prevents the actual cash rate from rising more than 0.25 percentage points above the target.

Together, these two boundaries form a corridor that constrains the cash rate. The RBA's target sits exactly in the middle of this corridor. Banks have strong incentives to trade within this range, keeping the actual cash rate close to the target.

When the RBA announces a change to the cash rate target, the corridor shifts immediately. The floor and ceiling move up or down in line with the new target, and banks adjust their trading behavior accordingly.

A well-established market convention exists where participants in the overnight money market generally trade at exactly the target rate, rather than anywhere else in the corridor. This convention, combined with the RBA's management of ES fund supply (discussed below), means that changes to the cash rate happen as soon as the RBA announces a new target.

Domestic market operations

While the policy corridor ensures the cash rate cannot stray far from target, daily fluctuations in demand for ES funds could still cause the rate to bounce around within the corridor. To maintain greater stability, the RBA manages the supply of ES funds through domestic market operations (DMO).

Demand for ES funds varies from day to day, particularly when large transactions or payments occur in the economy (such as when the government pays social security benefits). The actual cash rate represents the price at which this fluctuating demand intersects with the available supply of ES funds. By actively managing the supply side, the RBA can ensure the cash rate stays very close to the target, not just within the corridor.

How DMO Works:

The RBA conducts DMO by purchasing and selling financial securities (primarily Commonwealth Government Securities) in exchange for ES balances. These transactions directly affect the supply of ES funds:

-

To increase ES fund supply: The RBA buys financial securities from banks. The RBA pays for these securities by depositing funds into the banks' ES accounts. This increases the supply of ES funds in the system.

-

To decrease ES fund supply: The RBA sells financial securities to banks. The banks pay for these securities, and the RBA withdraws the payment from their ES accounts. This decreases the supply of ES funds in the system.

Most DMO involves repurchase agreements (repos). In a repo transaction, the "seller" of a security effectively agrees to buy it back from the "buyer" at a later date. The RBA prefers repos because they are highly flexible instruments that allow very precise management of ES supply, much more so than outright purchases or sales of securities.

Transmission to other interest rates

The cash rate serves as the anchor for interest rates throughout the Australian economy. When the cash rate changes, it affects how much it costs financial institutions to obtain funding. Banks and other lenders must borrow in wholesale markets to fund their lending activities. When the cash rate increases, these funding costs rise. To maintain their profit margins, financial institutions typically pass these higher costs on to their customers by increasing the interest rates they charge on mortgages, business loans, and other lending products.

Similarly, when the RBA reduces the cash rate, it becomes cheaper for financial institutions to borrow money. Competition in the banking sector generally forces institutions to pass these cost savings on to customers through lower lending rates.

Factors Affecting Retail Interest Rates

The cash rate is not the only factor influencing retail interest rates. Other important factors include:

- Competition in the banking sector

- Banking regulations

- Conditions in global financial markets

- Conditions in domestic financial markets

- Banks' assessment of credit risk based on economic conditions

These factors mean the margin between the cash rate and retail interest rates can change over time. Banks don't always pass on the full amount of cash rate changes to their customers.

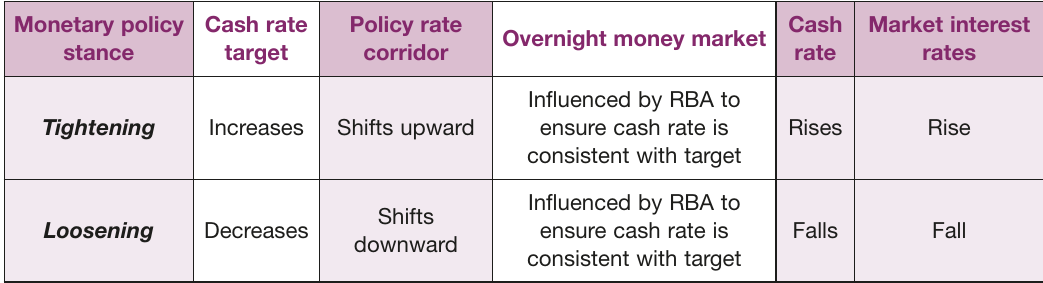

The RBA can adopt two basic monetary policy stances:

Tightening monetary policy: The RBA raises the cash rate target. This shifts the policy corridor upward, causing the cash rate to rise. Market interest rates throughout the economy then increase.

Loosening monetary policy: The RBA lowers the cash rate target. This shifts the policy corridor downward, causing the cash rate to fall. Market interest rates throughout the economy then decrease.

Financial markets closely scrutinize not just the RBA's cash rate announcements, but also other communications such as board minutes and speeches by senior RBA officials. Markets often interpret subtle changes in the RBA's language about economic conditions as signals of future interest rate movements. This can lead to interest rates in some financial markets changing even before the RBA officially adjusts the cash rate target – markets "price in" expected changes.

Unconventional monetary policy

In recent years, central banks worldwide have experimented with policy tools beyond traditional interest rate adjustments. These measures became necessary when interest rates approached zero, limiting the ability to provide further economic stimulus through conventional means. While other central banks adopted such measures following the 2007-2009 global financial crisis, the RBA implemented them in Australia during the COVID-19 recession.

Conventional vs Unconventional Monetary Policy

Conventional monetary policy refers to the traditional approach where central banks use their main policy interest rate (the cash rate in Australia) as their primary tool. Changes to this rate affect the entire interest rate structure across the economy.

Unconventional monetary policy involves using additional tools beyond the main policy rate. These measures have only been employed by advanced economy central banks over the past two decades, typically in response to extreme economic events.

Key unconventional measures used by the RBA:

1. Asset purchases: The RBA purchased government securities in the secondary market from financial institutions, paying for them by creating new ES balances in the institutions' accounts. This injected additional liquidity into the financial system and helped lower longer-term interest rates.

2. Forward guidance: The RBA used official communications to signal its future monetary policy intentions. By providing information about how long it expected to maintain certain policy settings, the RBA influenced current interest rates on longer-term financial assets.

3. Enhanced liquidity provision: The RBA increased the size of its domestic market operations beyond normal levels. It also created the Term Funding Facility, which provided low-cost loans to commercial banks to support their lending to households and businesses.

4. Corridor adjustment: The RBA temporarily changed the policy corridor by setting the floor at 0.1 percentage points (rather than 0.25 percentage points) below the cash rate target. This allowed the RBA to lower the cash rate to 0.1% without risking negative interest rates.

These unconventional measures were largely unwound during the second half of 2021 as Australia's economic recovery from the pandemic gained momentum. The RBA has consistently stated it is very unlikely to introduce negative interest rates, although some other countries (Japan, the European Union, and Sweden) have experimented with them.

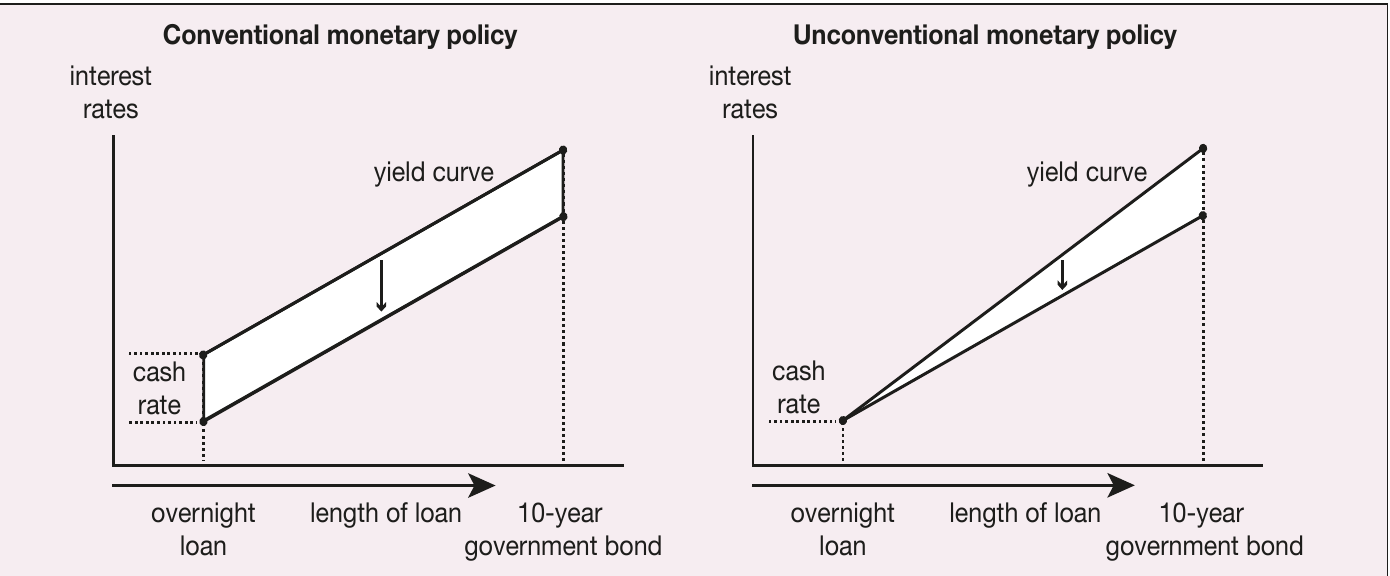

Understanding unconventional policy through the yield curve

The yield curve provides a useful framework for understanding how unconventional monetary policy differs from conventional policy. The yield curve shows the relationship between loan maturity and interest rates. In general, longer-term loans carry higher interest rates because lenders require greater returns to compensate for the increased risks of lending for extended periods.

Conventional monetary policy typically lowers the entire yield curve relatively evenly. When the RBA cuts the cash rate, interest rates decline across short-term and long-term loans.

Unconventional monetary policy works differently. These measures specifically target longer-term interest rates, flattening the yield curve. For example, when the RBA purchases long-term government bonds, it increases demand for these securities, which pushes up their prices and reduces their yields (interest rates). This targeted reduction in long-term rates provides additional economic stimulus beyond what conventional policy alone can achieve.

The transmission mechanism of monetary policy

The transmission mechanism describes the process through which changes in monetary policy flow through the economy to affect key economic objectives like inflation and economic growth. This mechanism operates through several channels:

The interest rate channel: Lower interest rates reduce the cost of borrowing for both consumers and businesses. Consumers often need to borrow for major purchases such as housing and consumer durables (cars, appliances, etc.). Businesses borrow to fund investment in capital equipment, plant upgrades, and business expansion. When interest rates fall, these borrowing costs decrease, encouraging both consumption and investment spending. This increased spending raises the overall level of economic activity in the economy.

Additionally, lower interest rates reduce the opportunity cost of business investment. Business owners could alternatively invest their funds in financial assets to earn interest returns. When these potential returns fall (due to lower interest rates), investing directly in business operations becomes relatively more attractive, further encouraging business investment.

The transmission mechanism works in reverse when the RBA tightens monetary policy by raising interest rates. Higher borrowing costs discourage consumption and investment spending, reducing overall economic activity.

Remember!

Key Points to Remember:

-

The cash rate is the interest rate in the overnight money market where banks lend to each other to settle daily payment obligations through their exchange settlement (ES) accounts

-

The RBA controls the cash rate through the policy interest rate corridor, which sets a floor (deposit rate at -0.25 percentage points) and ceiling (lending rate at +0.25 percentage points) around the target rate

-

Domestic market operations (DMO) involve the RBA buying or selling financial securities to manage the supply of ES funds and keep the cash rate aligned with the target

-

The cash rate influences other interest rates in the economy because it affects banks' funding costs, which they pass on to borrowers

-

Unconventional monetary policy tools (asset purchases, forward guidance, enhanced liquidity) specifically target longer-term interest rates by flattening the yield curve, providing additional stimulus when conventional policy is constrained