Market Equilibrium (HSC SSCE Economics): Revision Notes

The Role of the Market and Government Intervention

Introduction

Markets play a crucial role in determining how resources are allocated within an economy. Through the price mechanism, markets coordinate the decisions of millions of consumers and producers without central planning. However, markets do not always produce ideal outcomes, which is why governments sometimes intervene to correct market failures.

Understanding the balance between free markets and government intervention is fundamental to modern economics. While markets are generally efficient at allocating resources, there are specific situations where government action can improve outcomes for society as a whole.

The price mechanism in product markets

The price mechanism serves as the primary tool for solving the economic problem in a market economy. It provides information that answers fundamental questions about production, distribution, and exchange of goods and services.

Product markets are where demand for and supply of finished goods and services interact. In these markets, the demand curve represents consumer wants, while the supply curve represents what firms can produce with their limited resources. When these two forces interact, they establish a price and quantity that best satisfies consumer wants given the resource constraints firms face.

The market equilibrium represents the point where consumer demand and producer supply are perfectly balanced. At this point, every consumer willing to pay the market price can purchase the good, and every producer willing to sell at the market price can sell their output.

How producers respond to price signals

Producers only manufacture goods and services where genuine consumer demand exists—meaning consumers are both willing and able to purchase at a certain price. When the price of product X rises, producers face a higher opportunity cost in producing alternative goods. This price increase signals producers to reallocate resources away from other products and increase production of product X.

This process happens automatically through price changes. Information about consumer tastes and preferences flows between buyers and sellers without any central coordination. No government agency needs to collect data or issue instructions—the price mechanism does this work efficiently.

The Beauty of Market Coordination

The price mechanism achieves something remarkable: it coordinates the economic decisions of millions of people without anyone being in charge. Price signals transmit information about scarcity and consumer preferences instantly throughout the economy, allowing resources to flow to their most valued uses.

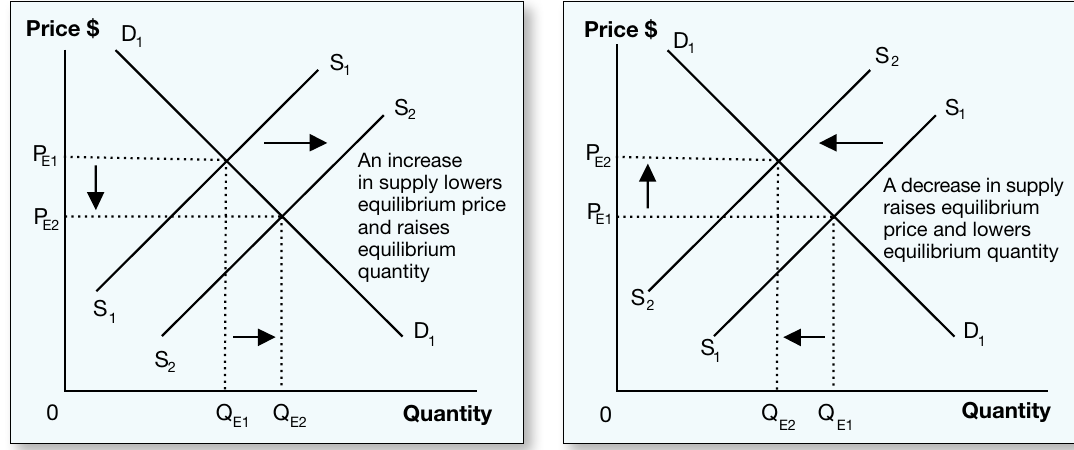

Supply shifts and equilibrium changes

Understanding the Diagrams

The diagrams above illustrate how supply changes affect market equilibrium:

- When supply increases (shifts right), the equilibrium price falls and equilibrium quantity rises

- When supply decreases (shifts left), the equilibrium price rises and equilibrium quantity falls

These movements show how markets automatically adjust to changes in production conditions, always seeking a new equilibrium point.

The price mechanism in factor markets

Factor markets trade the inputs needed for production: land, labour, capital, and enterprise. The price mechanism also operates in these markets, determining both:

- The price paid for factors of production

- The share of total output received by individuals

Individuals who possess scarce resources or skills in high demand will earn higher incomes and receive a larger proportion of total output.

Worked Example: Factor Market Pricing

Consider the market for software engineers:

Step 1: Identify the scarcity Software engineers with specialized skills in artificial intelligence are relatively rare compared to general programmers.

Step 2: Assess the demand Tech companies have high demand for AI expertise to develop new products.

Step 3: Determine the outcome An AI specialist may command a salary of $150,000 per year, while an unskilled worker might earn $30,000 per year. The AI specialist's skills are both scarce and highly valued by employers, resulting in a much higher income and larger share of total output.

Allocative efficiency and market competition

Markets are said to achieve allocative efficiency—the economy's ability to allocate resources to satisfy consumer wants effectively. The demand curve indicates the value consumers place on a product, while the supply curve shows producers' costs. The market mechanism ensures equilibrium occurs where these curves intersect.

This means production continues until the value to consumers of the last unit produced equals the cost to producers of supplying it. No resources are wasted producing goods that consumers value less than their production cost, and no valuable production opportunities are missed.

The Efficiency Condition

Allocative efficiency is achieved when:

At the market equilibrium in perfectly competitive markets, this condition is satisfied because:

- The demand curve represents MSB (what consumers are willing to pay)

- The supply curve represents MSC (what it costs society to produce)

Why markets are efficient

The market mechanism achieves efficiency because:

- Any consumer willing to pay the market price will have their demand satisfied

- Any producer offering goods at the market price will sell everything they produce

Competition between producers reinforces this efficiency. Firms must respond to consumer demand and minimise production costs to remain competitive and profitable. This competitive pressure ensures the most cost-efficient production methods are used, eliminating waste and reducing prices for consumers.

Competition acts as a natural discipline on producers. Inefficient firms that fail to minimize costs or respond to consumer preferences will lose market share to more efficient competitors, ultimately being forced out of the market.

Market failure

Despite their strengths, markets left entirely to themselves can produce unsatisfactory outcomes. This occurs because the price mechanism considers only private costs and benefits (those affecting producers and consumers directly) but ignores social costs and benefits (those affecting society as a whole).

Market failure occurs when the price mechanism fails to account for these indirect social costs, such as environmental damage, or indirect social benefits, such as an educated population.

Understanding the Private vs. Social Distinction

- Private costs/benefits: Direct effects on the producer or consumer making the decision

- Social costs/benefits: Total effects on society, including both private effects AND external effects on third parties

When these differ, the market equilibrium will not be socially optimal.

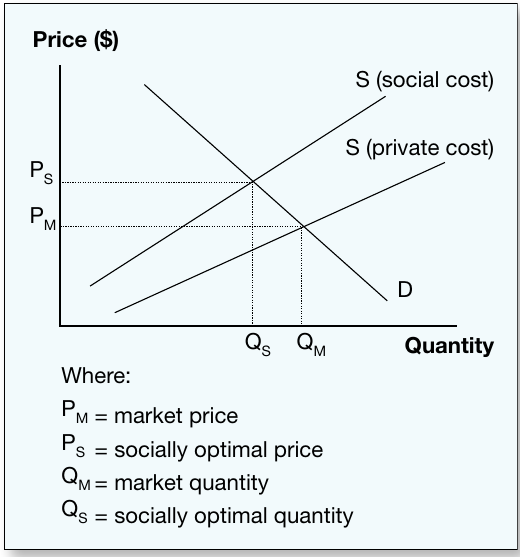

Interpreting the Negative Externality Diagram

The diagram above illustrates market failure caused by negative externalities:

- The S private cost curve shows only the direct costs producers face

- The S social cost curve includes both private costs and external costs to society, such as pollution

The free market produces at quantity and price , but the socially optimal outcome would be quantity and price . The market overproduces because producers don't bear all the costs of their production—society pays through environmental degradation and health problems.

The shaded area represents the welfare loss to society from overproduction.

Government intervention through price controls

When market prices are deemed too high or too low, governments may intervene by imposing price controls. The main motivation for price intervention is to redistribute income—either from sellers to buyers, or from buyers to sellers.

Price controls are among the oldest forms of government intervention in markets, dating back to ancient civilizations. However, they remain controversial because while they achieve their redistributive goals, they also create market inefficiencies.

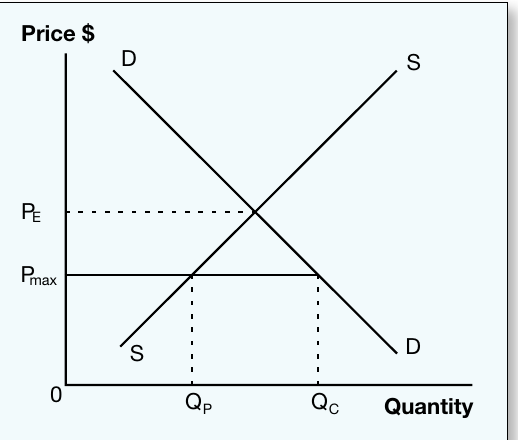

Price ceilings

A price ceiling sets the maximum price that can be charged for a commodity. Governments use price ceilings when they believe the market price is excessively high, particularly for essential goods.

Consider the market for bread shown above. The free market would establish equilibrium at price . If the government considers this too high, it may impose a price ceiling at below the equilibrium.

At this maximum price, producers will only supply quantity , but consumers demand quantity . This creates disequilibrium, with excess demand (a shortage) equal to the distance between and .

Key Problem with Price Ceilings

While price ceilings help consumers afford goods, they create shortages because producers find it unprofitable to supply sufficient quantities at the low price.

Additional problems include:

- Development of black markets where goods are sold illegally above the ceiling price

- Queuing and rationing systems may be needed to allocate scarce supply

- Quality deterioration as producers cut costs to maintain profitability

- Deadweight loss from mutually beneficial trades that don't occur

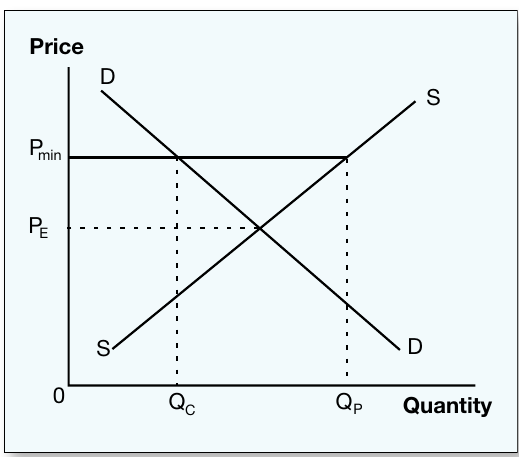

Price floors

A price floor sets the minimum price that can be charged for a commodity. Governments use price floors when they believe the market price is too low, often to protect producer incomes.

The diagram shows a market where the government sets a price floor at above the equilibrium price . At this minimum price, producers want to supply quantity , but consumers only demand quantity . This creates disequilibrium, with excess supply (a surplus) equal to the distance between and .

Key Problem with Price Floors

While price floors increase producer incomes, they cause overproduction as producers supply more than consumers want to buy at the higher price.

Additional problems include:

- Government may need to purchase surplus to maintain the floor price

- Resources wasted producing unwanted output

- Consumers pay higher prices and reduce consumption

- Deadweight loss from reduced market activity

In both cases, government price intervention leads to market disequilibrium. Due to these problems, governments in recent decades have moved towards more sophisticated intervention methods.

Government intervention through quantity controls

Markets may produce too much or too little of certain goods because individual firms and consumers don't consider social costs and benefits in their decisions. These social impacts, called externalities, are not captured by the price mechanism.

Addressing negative externalities

Negative externalities are social costs not considered by producers, such as pollution and environmental damage. While firms account for obvious costs like labour and raw materials, they often ignore the harm their production causes to society.

Governments can address this through:

Taxes: Imposing taxes on businesses increases their production costs, forcing them to reduce output. This makes firms pay for the social costs they create—a process called internalising the externality. The tax increases equilibrium price and reduces equilibrium quantity towards the socially optimal level.

Regulations: Laws can directly restrict production levels, such as pollution emission permits that limit how much pollution firms can generate.

Worked Example: Carbon Tax on Steel Production

The Problem: A steel factory produces 1,000 tonnes per month. Its private cost is $500 per tonne, but pollution creates an additional social cost of $100 per tonne.

Step 1: Calculate total social cost

- Private cost: $500 per tonne

- External cost: $100 per tonne

- Social cost: $600 per tonne

Step 2: Government imposes tax The government imposes a $100 per tonne carbon tax on steel production.

Step 3: Outcome

- The tax increases the firm's costs from $500 to $600 per tonne

- The firm now faces the true social cost of production

- Production decreases to the socially optimal level (e.g., 800 tonnes per month)

- The externality has been internalised—the firm now pays for the pollution it creates

Addressing positive externalities

Positive externalities are social benefits not considered by consumers, such as the broader community benefits from education or public transport use. While individuals consider their private benefits, they ignore the advantages their consumption creates for others.

Merit goods are products that involve positive externalities and are therefore underconsumed if left to the free market. Examples include museums, public parks, art galleries, and public transport.

When you visit a museum or use public transport, you create benefits beyond your own enjoyment:

- Museums preserve culture and history for future generations

- Public transport reduces traffic congestion and pollution for everyone

- Education creates a more productive workforce that benefits all employers

- Vaccination protects not just you but also those around you through herd immunity

Governments encourage consumption of merit goods through:

Subsidies: Payments to consumers or producers lower the price and increase consumption. The subsidy reduces equilibrium price and increases equilibrium quantity towards the socially optimal level.

Worked Example: Public Transport Subsidy

The Problem: Bus tickets cost $5 based on private benefits alone, but each bus journey creates $2 of additional social benefits (reduced congestion, lower pollution).

Step 1: Identify the market failure

- Market quantity: 10,000 journeys per day

- Socially optimal quantity: 15,000 journeys per day

- The market underproduces by 5,000 journeys

Step 2: Government provides subsidy The government provides a $2 subsidy per bus ticket.

Step 3: Outcome

- Ticket price decreases from $5 to $3 for consumers

- Consumption increases to 15,000 journeys per day

- Society now captures the full social benefits from public transport use

Public goods provision

Some goods and services won't be provided by private firms at all. Public goods are products where producers cannot exclude non-payers from benefiting. Examples include national defence, police services, public roads, and waterway cleanup.

Everyone benefits from national defence whether they pay or not, so people have no incentive to contribute voluntarily. Private firms cannot profitably provide such goods because they cannot charge for their use.

Characteristics of Public Goods

Public goods have two key features:

- Non-excludability: Once provided, it's impossible or prohibitively expensive to exclude non-payers from benefiting

- Non-rivalry: One person's consumption doesn't reduce the amount available for others

Because of these characteristics, public goods suffer from the free-rider problem—people can benefit without paying, so everyone has an incentive to wait for others to pay. This leads to under-provision or no provision at all by private markets.

Therefore, governments directly provide public goods and finance them through taxation. This ensures these essential services exist, even though markets would not supply them.

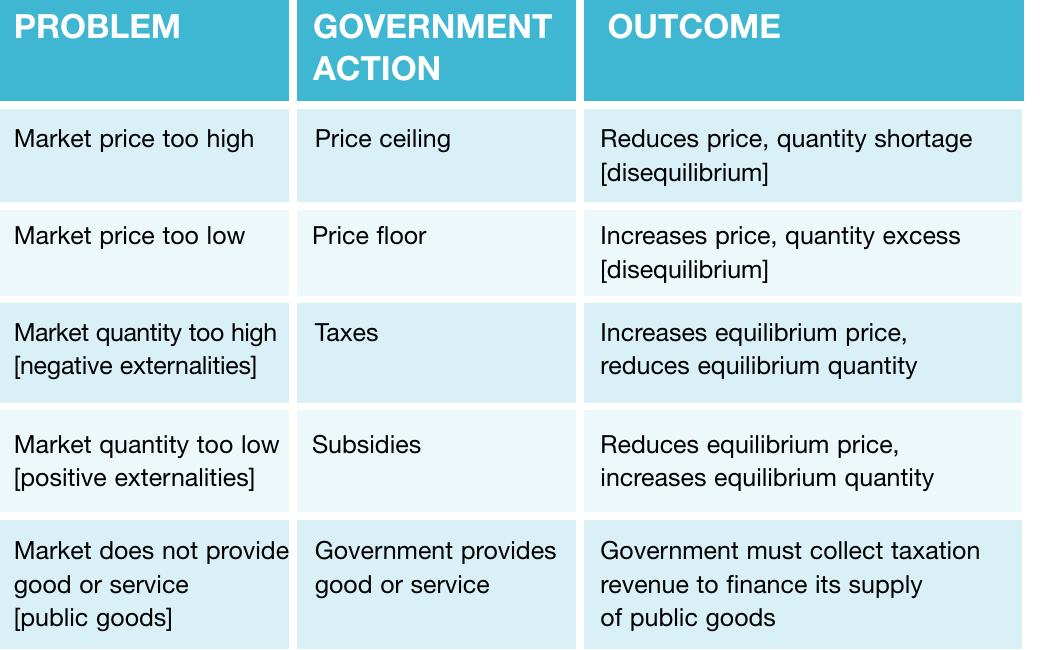

Summary of government interventions

Key Points: Government Intervention Types

The table above summarizes the main types of government intervention in markets, showing the problem each addresses, the government action taken, and the outcome of that intervention.

Price Controls:

- Price ceilings reduce prices but create shortages and disequilibrium

- Price floors increase prices but cause excess supply and disequilibrium

Quantity Controls:

- Taxes address negative externalities by increasing price and reducing quantity

- Subsidies address positive externalities by decreasing price and increasing quantity

Direct Provision:

- Government provision supplies public goods that markets won't provide, funded through taxation

Exam guidance

Essential Exam Strategies

When analysing government intervention:

For price controls: Always explain the disequilibrium created and identify whether there will be excess demand (shortage) or excess supply (surplus). Use diagrams to show the gap between quantity demanded and quantity supplied at the controlled price.

For externalities: Distinguish clearly between private and social costs/benefits. Explain why the market equilibrium differs from the socially optimal outcome and how the government policy moves the market towards the optimal position.

For evaluation questions: Consider both benefits and drawbacks of intervention:

- Price controls help some groups but harm others and create inefficiencies

- Taxes and subsidies move markets towards optimal outcomes but require government revenue or spending

- Government provision of public goods requires funding through taxation, which itself creates economic effects

Remember: Key Concepts

-

The price mechanism coordinates decisions between consumers and producers through price signals, solving the economic problem without central planning

-

Allocative efficiency occurs when production continues until the value to consumers equals the cost to producers

-

Market failure happens when the price mechanism ignores social costs and benefits, considering only private costs and benefits

-

Price ceilings create shortages (excess demand) while price floors create surpluses (excess supply)—both cause disequilibrium

-

Negative externalities require government intervention through taxes or regulations to reduce overproduction

-

Positive externalities require subsidies to increase consumption of merit goods towards socially optimal levels

-

Public goods must be provided by government because private firms cannot exclude non-payers from benefiting, leading to the free-rider problem