Brazil (HSC SSCE Economics): Revision Notes

Brazil

Introduction

Brazil serves as an important case study for understanding how different economies respond to globalisation. In the 2000s, Brazil was celebrated as one of the fastest-growing emerging economies and a success story of global integration. However, since 2015, it has become one of the worst-performing economies in the G20, demonstrating the volatility and challenges that can face developing economies.

Brazil is the world's ninth-largest economy and ranks as the third-largest of the BRIC economies (behind China and India, but ahead of Russia). It is the sixth-most populous country globally with 216 million people, and the fifth-largest by land area.

The country has a highly diverse population, shaped by Portuguese colonisation since the 1500s and over 2000 Indigenous groups.

Like other Latin American economies, Brazil has embraced globalisation more cautiously than East Asian emerging economies. A global commodity boom combined with the discovery of large resource deposits contributed to years of strong growth and rising incomes. However, this collapsed suddenly in 2014 with a deep recession triggered by slumping commodity prices and a corruption crisis. Years of weak growth were followed by catastrophic mismanagement of the COVID-19 pandemic, which left Brazil among the world's worst-affected countries.

Development indicators

Brazil's economic and social indicators reveal both progress and persistent challenges:

| Indicator | Brazil | Comparator economies |

|---|---|---|

| Population (2023) | 216 million | Indonesia: 277m, China: 1410m |

| GDP (2023) | $2080 billion | 9th largest globally |

| GNI per capita (PPP, 2022) | $17,260 | Upper-middle-income category |

| Gini index (2022) | 52.9 | One of world's highest (more unequal) |

| Mean years schooling (2021) | 8.1 years | Below OECD average |

| Life expectancy (2021) | 72.8 years | Fell from 76 in 2019 due to COVID-19 |

| HDI rank (2021-22) | 0.754 (87th) | Improved from 0.68 in 2000 |

These indicators show that while Brazil has a substantial economy, it faces significant challenges in development, inequality and education compared to other major economies. The Gini index of 52.9 is one of the world's highest, indicating severe income inequality.

Economic performance

Social and economic progress

Brazil has achieved notable improvements in human development over recent decades, though starting from a relatively low base. The country's Human Development Index improved from 0.68 in 2000 to 0.754 in 2021-22, ranking 87th globally. This places Brazil slightly ahead of the Latin American regional average.

Key improvements include:

Health outcomes:

- Life expectancy increased from 63 years in 1980 to 76 years in 2019, before falling to 72 years in 2021-22 following the severe COVID-19 pandemic

- Infant mortality declined dramatically from 53 per 1000 live births in 1990 to 13 in 2021

Education:

- Adult literacy reached 94% in 2021, up from 82% in 1990

- However, average years of formal schooling remain relatively low at 8.1 years

Poverty reduction:

Brazil's most significant achievement has been progress in reducing poverty and inequality. Historically characterised by very high inequality, Brazil has made measurable improvements:

- The percentage of Brazilians living on less than $2.15 per day fell from 23.2% in 2002 to 5% in 2019 – the best improvement in Latin America

- The Gini index (measuring income inequality) fell from around 60 in 2000 to 49 in 2020, before rising sharply to 53 during the COVID-19 recession

The Bolsa Família program:

Case Study: The Bolsa Família Program

Introduced in 2004 by President Lula's administration, this flagship policy exemplifies effective poverty reduction strategy. Low-income households receive small cash transfers conditional on keeping children in school and attending preventive health care visits.

These conditional cash transfer policies are regarded as one of the most effective strategies to combat poverty. Research suggests approximately half the reduction in inequality resulted from economic growth, while the other half came from government redistribution policies.

An IMF paper in 2020 found the program helped more people gain stable employment. However, progress reversed during the COVID-19 recession, which saw unemployment exceed 14%.

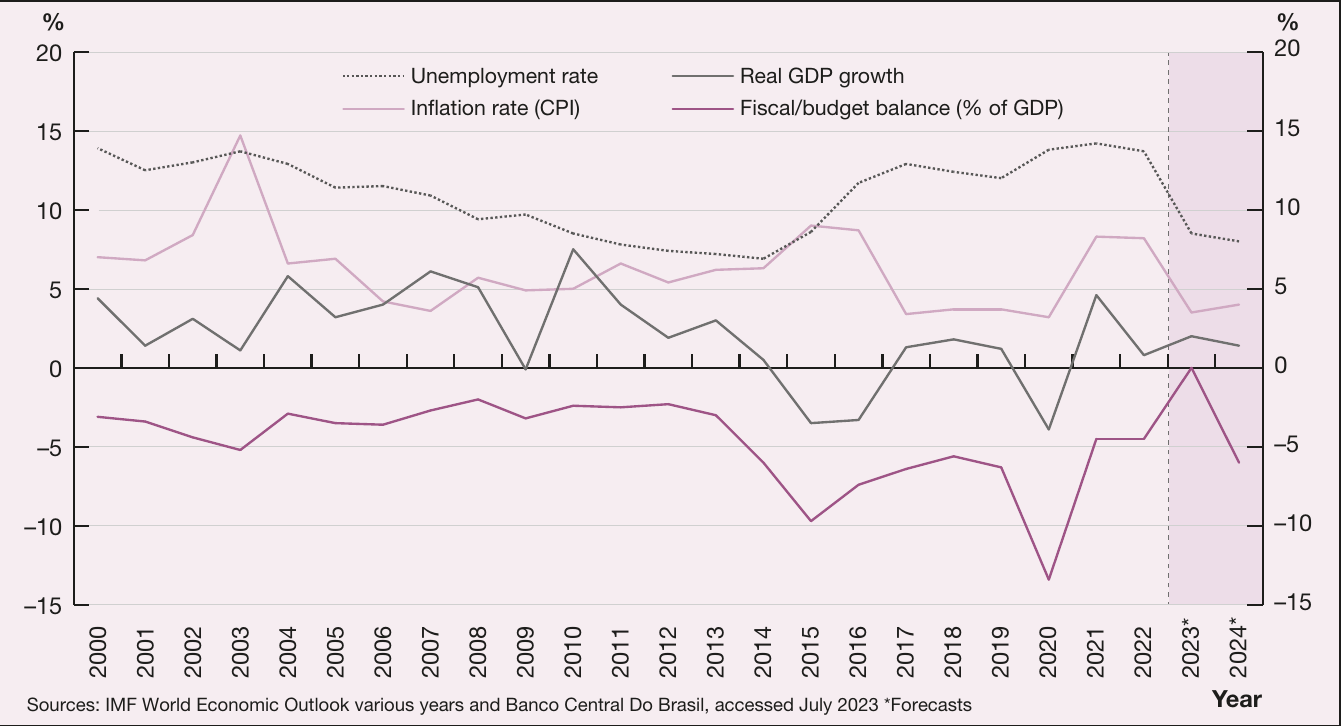

Economic recessions

Brazil's economic performance reveals stark contrasts between decades. In the 2000s, the economy grew by an average of 3.7% annually with rising living standards. However, the 2010s were dismal, averaging growth only fractionally above zero.

The 2015-2016 recession:

This recession was so severe it approached a depression (defined as a deep and sustained recession). Per capita incomes in 2020 had still not recovered to 2014 pre-recession levels, pushing 55 million Brazilians into poverty – approximately one in four people.

Stagflation:

The 2010s witnessed the unusual phenomenon of inflation and unemployment surging simultaneously – the textbook definition of stagflation, rarely seen since the 1970s:

- Unemployment reached 13.7% in 2017, leaving close to 14 million Brazilians without work

- Inflation rose to 9%

- Similar conditions recurred during COVID-19 when unemployment surged to 14.7% in 2021 while inflation jumped over 10%

Policy responses:

In response to rising inflation in 2016, Brazil's main interest rate was raised to 14.25%, giving Brazil the highest interest rates of any comparable economy in the mid-2010s. Sharp falls in tax revenues created a vicious cycle, forcing further spending cuts by state and local governments. Many of Brazil's famous annual Carnival celebrations were even cancelled in 2016 due to budget constraints.

COVID-19 recession:

While economies globally fell into recession in 2020 due to the pandemic, Brazil's recession was worsened by mismanagement of the national response. The health system was overwhelmed by multiple waves of infections. The economy contracted 4.1% in 2020, raising unemployment to record highs and pushing 18 million into poverty.

Recovery challenges:

Brazil recovered slowly from the COVID-19 recession. A 14% official interest rate raised the cost of household borrowing, and the war in Ukraine disrupted trade relationships. However, inflation rapidly fell to just 3% in 2023, and forecasts for economic growth rebounded to 4% backed by strong commodity exports.

Financial stability:

One positive feature has been the stable operation of financial markets despite two severe recessions in less than a decade. The floating exchange rate (which fell 50% in the four years to 2016 and another third during COVID-19) helped improve export competitiveness. Stronger banking regulations maintained confidence in the financial sector.

Seven reasons for recession (2014-2016)

Understanding why Brazil moved from being celebrated as a "Latin American tiger economy" to the G20's worst performer requires examining multiple interconnected factors:

1. Commodity price collapse:

Brazil is a major commodity exporter. The sharp fall in prices for oil, iron ore and agricultural output resulted in lower export revenues and falling national income. Eight of Brazil's top ten exports in 2015 were commodities. Brazil's downturn was significantly worse than other commodity-exporting economies.

2. Economic diversification failure:

Brazil was unprepared for falling commodity prices. Other sectors could not fill the gap left by the collapse in export revenue, revealing structural weaknesses in the economy.

3. Corruption scandal:

From 2014, a major corruption scandal engulfed Brazil's business and political elites, halting economic reforms. The investigation revealed massive bribery and corruption involving Petrobras (Brazil's large state-controlled oil company) and leading political figures. The scandal engulfed so many major businesses and politicians that Congress could not advance reform proposals.

4. Loss of investor confidence:

Investors lost confidence in Brazil's ability to address budget problems. Public spending had grown at an annual average of 6% for two decades, well above economic growth. With interest payments of almost 8% of GDP, Brazil was running a massive budget deficit of 11% of GDP by 2016.

5. Credit rating downgrade:

Loss of confidence led to the downgrading of Brazil's sovereign debt by ratings agencies to below "investment grade", making it more difficult and expensive for the government to obtain loans. Public debt rose from 52% to 68% of GDP between 2013 and 2016.

6. Policy failures:

Many government policies failed to overcome economic problems, including:

- Price controls that failed to control inflation

- Aggressive lending by state banks that failed to stimulate investment

- Infrastructure project plans that failed to attract private investors

7. Structural problems:

Brazil made little progress addressing deep-seated structural problems affecting labour productivity, transport infrastructure, education levels and its reputation as a difficult place to do business. This left Brazil exposed when favourable conditions of high commodity prices disappeared.

Exam tip: Analysing Brazil's Recession

When analysing Brazil's recession, demonstrate understanding of the interconnected nature of economic problems. Don't just list factors – explain how they reinforced each other:

For example: corruption scandal → loss of confidence → credit downgrade → higher borrowing costs → worse budget deficit

This shows sophisticated understanding of how economic problems create feedback loops that amplify economic downturns.

Environmental challenges

Brazil faces significant environmental challenges that have both economic and global implications.

Deforestation:

Brazil's economic development has come at the cost of large-scale forest clearing. Eighty per cent of Amazon deforestation has been for cattle farming, with other uses including soybean farming and mining – some of Brazil's biggest industries. Forest coverage declined from 72% to 60% between 1990 and 2020.

Management of the Amazon has been a polarising political issue. Former President Bolsonaro (2019-2022) made land clearing a priority, even promising to build a motorway through the Amazon to make logging easier. The fires used for land-clearing contributed to the fastest rate of deforestation since 2006. For the first time on record, in 2021 the Amazon emitted more carbon dioxide than it absorbed.

Global significance:

Brazil's management of the Amazon is a major international concern because it is the world's largest tropical rainforest, sometimes called the "lungs of the planet". It produces an estimated 20% of the world's oxygen supply and absorbs vast amounts of carbon dioxide. Destruction releases large quantities of carbon dioxide into the atmosphere.

President Lula, returning to power in 2023, took action to reduce land clearing, achieving a 34% reduction during his first six months in office.

Environmental pollution:

Like many developing economies, Brazil suffers from high levels of water and environmental pollution:

- Only 37% of wastewater is treated

- Almost half of garbage and solid waste is not collected

- Around one-third of housing is not connected to sewerage

- Poor sanitation leads to worse public health outcomes

Biofuels success:

In contrast to its deforestation record, Brazil has been a world leader in developing sustainable biofuels (ethanol and biodiesel). These assist in transitioning from fossil fuels and emit less carbon. Brazil is the world's second-largest ethanol producer (after the United States). Ethanol, mostly made from sugar cane, accounts for around 45% of fuel usage in Brazil.

Influence of globalisation

Trade

Despite maintaining some protectionist policies, Brazil has benefited from rapid growth in international trade brought by globalisation. Brazil supplies large quantities of commodities which sustained historically high prices over the last two decades.

Commodity dependence:

More than one-third of Brazil's export revenues come from just three commodities:

- Iron ore

- Soybeans

- Oil

Oil exports grew rapidly following discovery of large reserves in "pre-salt" fields three kilometres below the ocean surface in the 2000s. Brazil is also the world's largest exporter of beef and chicken. JBS, its largest agribusiness company, sells five billion chickens annually and is now the largest meat producer in Australia.

Export revenue cycles:

Brazil's export revenues reflect cycles of global commodity prices:

- Total export value soared from $55 billion in 2000 to over $250 billion at the height of the global resources boom in 2011

- After a decade of weaker growth throughout the 2010s, the surge in commodity prices in the early 2020s saw export revenues rise by more than 50% over pre-pandemic levels to a record $335 billion in 2022

Vulnerability to external shocks:

Globalisation has increased Brazil's exposure to both ups and downs of commodity prices and the international business cycle. Lower global commodity prices led to weaker exports and in 2014, a record trade deficit and high current account deficit. While the trade deficit improved in subsequent years, this was achieved only through sharp depreciation in the real and a severe recession that reduced import demand.

Confidence disruptions:

Brazil experienced several major disruptions to international confidence:

- Political corruption scandals

- The "Weak Flesh" scandal in 2017, where revelations that producers used red dye to mask putrefying meat damaged confidence in meat exports

- The collapse of the Brumadinho dam in 2017, revealing poor safety practices and causing major disruptions to Brazil's largest mining company, Vale

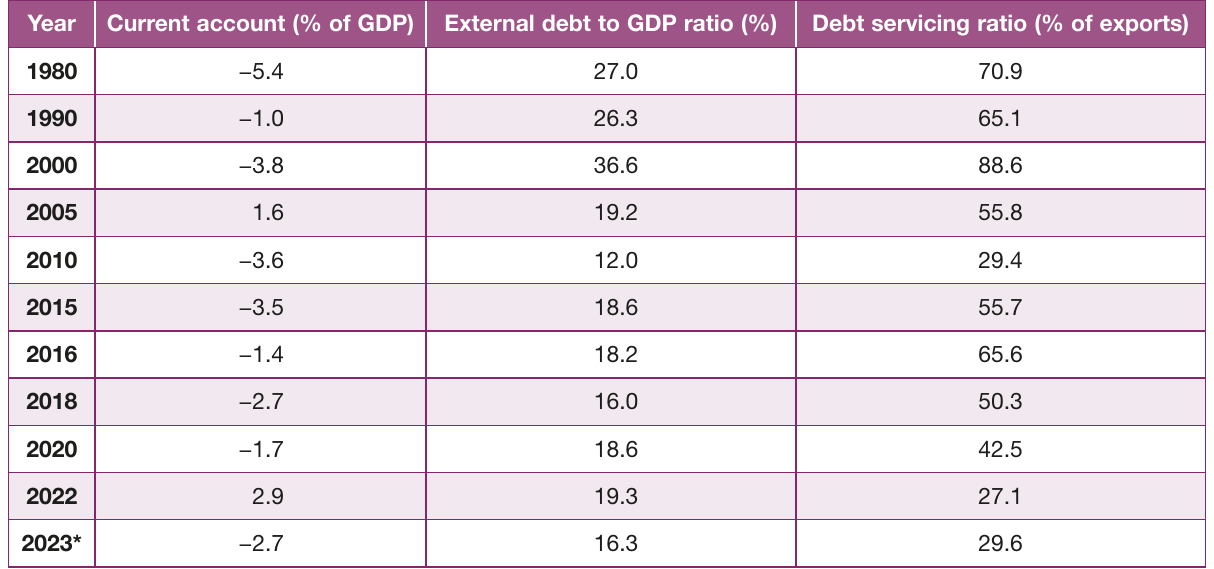

External accounts

One benefit of weak economic growth in the past decade has been improvement in Brazil's external accounts. While historically Brazil struggled with external imbalances, the IMF has said a current account deficit averaging between 1.2% and 2.0% of GDP is compatible with long-term economic stability. In the five years to 2023, Brazil averaged 2.5% of GDP – slightly above that range but better than many other indicators.

Foreign debt challenges:

Historically, the most significant problem underlying Brazil's external vulnerability has been its high level of foreign debt, once among the highest in the developing world. Specific characteristics made Brazil's debt concerning:

Debt servicing burden:

- Prior to the global resources boom, the cost of servicing Brazil's foreign debt reached 89% of export value by 2000

- After falling to 29% in 2010 and rising to 66% during the 2016 recession, the debt servicing ratio returned to 29% in 2023

Public sector debt:

- The IMF calculates Brazil's total public sector debt at up to 91% of GDP, with persistent concerns about spending sustainability

- Servicing foreign debt cost approximately 9% of GDP in 2023, reflecting vulnerability to increases in international interest rates, particularly in the US (the source of most Brazilian foreign borrowing)

Progress in debt management:

Brazil has made significant progress managing external debt:

- Better current account outcomes and contractionary fiscal policy helped stabilise foreign debt levels

- Brazil entered the 2020s with its lowest external debt levels since the mid-2000s

- External debt to GDP ratio fell from 36.6% in 2000 to 16.3% in 2023

Currency composition shift:

An important factor in debt improvement was a dramatic shift from borrowings in foreign currency to borrowings in Brazilian real. Foreign currency debt fell from 70% in the early 2010s to 3% in 2020, according to the Bank of International Settlements. This reduces vulnerability to exchange rate fluctuations.

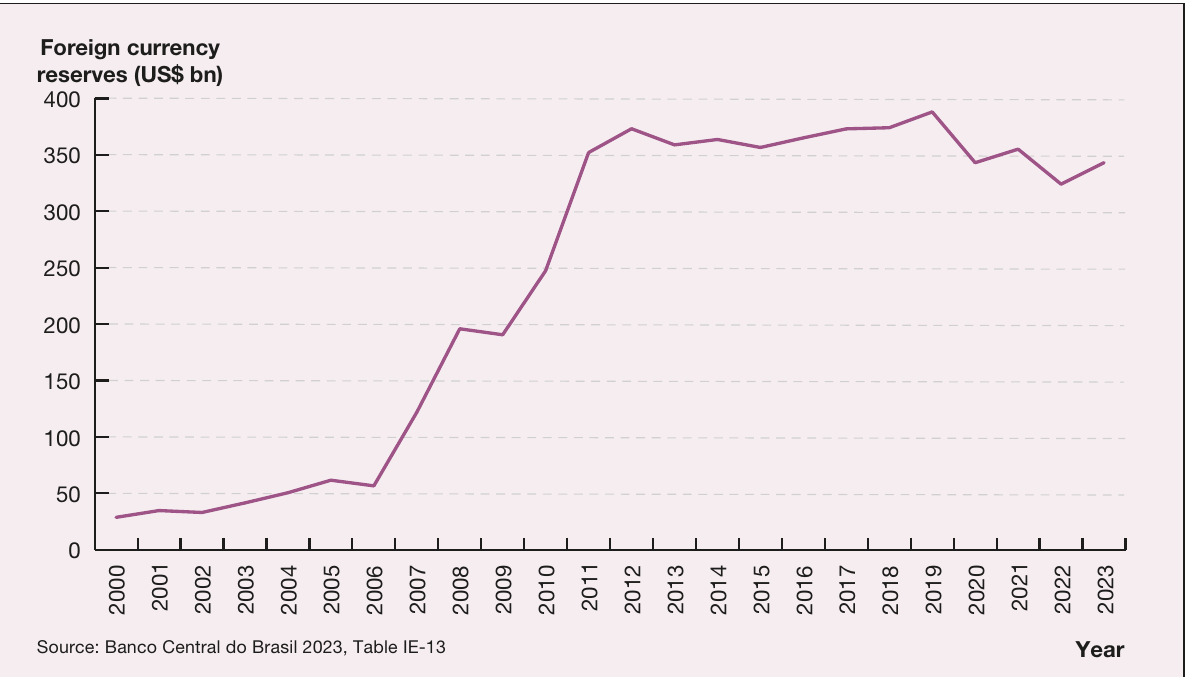

Foreign currency reserves:

Brazil substantially increased its foreign currency reserves to $325 billion in 2023. In the event of sudden exchange rate depreciation, these reserves can be used to buy Brazilian currency and stabilise its value. This proved useful during sharp depreciation in the first half of 2020 when Brazil intervened in the foreign exchange market to the tune of $40 billion.

Exam tip: Linking External Stability to Policy

When discussing Brazil's external stability, link improvements in debt management to specific policy choices:

- Floating exchange rate allows automatic adjustment to external shocks

- Building foreign currency reserves provides a buffer against speculation

- Shifting to domestic currency borrowing reduces exchange rate risk

This shows understanding of how governments can reduce external vulnerability through deliberate policy choices rather than merely describing outcomes.

Financial markets

Many Brazilians view globalisation through the lens of financial shocks that have regularly featured in recent economic history. Some crises had dramatic effects, such as the early 1990s exchange rate collapse that saw inflation reach over 4000%.

The 2002 crisis:

The last time a major regional financial crisis spilled over to Brazil was 2002, when:

- Brazil's GDP shrank by 40% in US dollar terms

- Interest rates soared to 23%

- Both unemployment and inflation rose sharply

IMF intervention:

The IMF provided an emergency loan of $30 billion to Brazil, requiring the government to adopt a range of economic reforms in return. These reforms helped make Brazil more resilient during subsequent crises in 2008, 2014 and 2020. The intervention successfully restored investor confidence, and by 2005 Brazil had repaid its entire IMF borrowing eight months ahead of schedule.

Brazil's response to globalisation

Different approach from Asian tiger economies

Like most Latin American nations, Brazil has been more cautious in embracing globalisation than many East Asian economies. Throughout the 20th century, successive governments sought to create a large industrial base and minimise dependency on imported manufactured goods, hoping to develop greater self-sufficiency. This import substitution strategy focused on producing for the domestic market rather than developing export markets.

Brazil relied largely on foreign borrowing to fund industrialisation, which proved less successful than the more export-oriented East Asian model. Higher growth rates in more open East Asian economies in the 1980s and 1990s led observers to question the more protectionist Latin American approach.

Gradual opening:

Brazil, like many neighbours, gradually opened its economy in the 1990s, attracting foreign investment and pursuing export opportunities. Brazil benefited from China's rapid growth and hunger for resources, as well as growth in Latin American economies.

Resource control:

Brazil's model of globalisation is less reliant on export demand. Brazil values control over its natural resources, particularly oil and gas. Until recently, there was a requirement that Brazil's state-owned business Petrobras must own at least 30% of new projects. Brazil remains cautious about adverse impacts of globalisation, such as unrestrained financial flows, and previously restricted short-term financial speculation by foreign investors.

Increased openness to foreign investment

Since the 1990s, Brazil has attracted foreign investment rather than merely borrowing funds to provide capital for economic development. To increase attractiveness to foreign investors, Brazil undertook extensive reforms:

- Deregulation

- Privatisation of state-owned monopolies like Vale (mining) and Embraer (aircraft manufacturing)

- Priority given to low inflation as a major macroeconomic policy goal

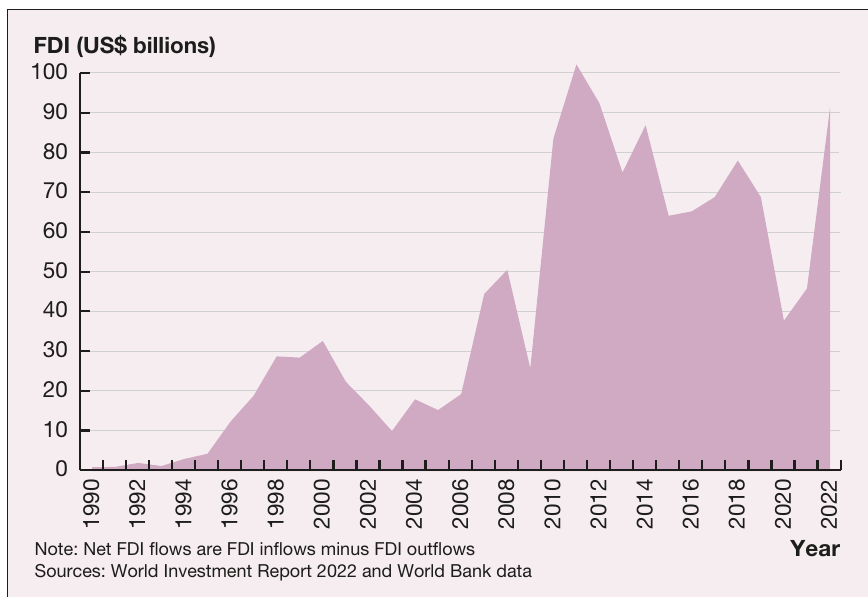

FDI inflows:

These measures dramatically increased foreign investment. Transnational corporations (TNCs) play important roles in industries such as telecommunications, pharmaceuticals and manufacturing. Brazil receives the largest share of foreign direct investment (FDI) in Latin America, with focus on resources, finance and construction sectors. While international confidence and FDI fell under the Bolsonaro Administration, they recovered strongly in 2022.

Brazilian TNCs abroad:

Another important aspect of Brazil's globalisation response is increasing investment by Brazilian companies in other countries. Brazil's stock of foreign direct investment assets more than doubled from $173 billion in 2010 to $392 billion in 2020. Brazilian TNCs are making large offshore acquisitions in steel production, cattle, banking and construction sectors.

Brazilian FDI outflows have substantial focus on developing and emerging countries, reflecting a historic shift because FDI typically flowed from developed to developing economies.

Trade liberalisation progress

Despite embracing financial and investment flows, Brazil has been relatively slow in liberalising trade flows. Until the 1990s, Brazil implemented tariffs and subsidies to develop domestic industries that could substitute locally made goods for imports. While this kept import levels down, it also made Brazilian industry less internationally competitive and less successful in developing export markets.

Current trade barriers:

According to the OECD 2020 Economic Survey, Brazil's trade integration remains limited:

- Exports and imports below 30% of GDP – significantly less integrated than other emerging markets of similar size

- Average tariff levels weighted by imports almost twice as high as neighbouring Colombia and more than 8 times higher than Mexico or Chile

- Most frequently applied tariff rate is 14%

- Around 450 tariff lines at the maximum of 35%, including textiles, apparel, leather and motor vehicles

- Brazil has the highest number of tariff lines above 10%

Gradual reform:

Although Brazil remains more closed than many comparable economies, it has become more outward-oriented since the 1990s, substantially reducing industry protection:

- Average tariff levels fell from 32.2% in 1990 to 8% in 2020

- Most import quotas were abolished

- Foreign trade increased from just 15% of GDP in 1990 to 39% by 2022

This is nevertheless low by international standards, making Brazil one of the least open economies in the G20 and OECD.

Recent trade policy:

While Brazil is under pressure to further reduce protection, progress has been inconsistent:

- President Lula has expressed support for trade liberalisation

- President Bolsonaro suspended planned removal of trade barriers unless other countries (many already with fewer protections) did likewise

- In December 2020, Brazil imposed a 20% tariff on all US ethanol imports

- To combat high inflation in 2022-23, Brazil made 10% tariff cuts to 87% of goods subject to tariffs, including 6000 Australian products

Industry structure changes:

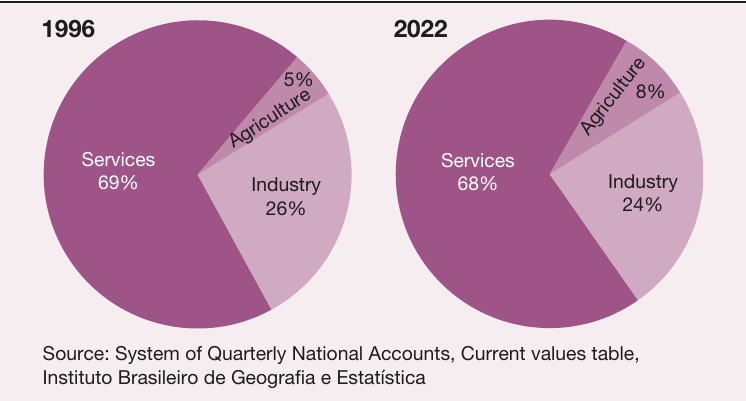

Brazil's gradual integration into the global economy has contributed to modest changes in industry structure:

- Manufacturing sector has become smaller as a share of the economy

- Concerns about deindustrialisation in some sectors (Ford, Mercedes-Benz, Sony and Canon closed Brazilian manufacturing operations)

- Manufactures' share of merchandise exports fell from 58% to 33% between 2000 and 2020

- Other industry categories (mining, construction) grew, offsetting manufacturing decline

- Services sector comprises the largest share of the economy but is domestically oriented, generating very little export income

Exam tip: Evaluating Trade Policy

When evaluating Brazil's trade policy, consider both costs and benefits of protection:

Costs of high tariffs:

- Limit integration into global economy

- Reduce competitiveness of domestic industries

- Lead to higher prices for consumers

Benefits of protection:

- Protect domestic industries and employment

- Allow infant industries time to develop

- Maintain control over strategic sectors

Brazil's gradual approach reflects political economy considerations – rapid liberalisation could cause significant job losses and political backlash.

Role in the global economy

President Lula is currently seeking to renew Brazil's global leadership role, which diminished during the decade before he returned to office. Poor economic performance since 2014, combined with corruption crises and political instability, reduced its capacity for global and even Latin American leadership. This contrasts sharply with the 2000s, when Brazil and India led a bloc of developing economies pushing for a new World Trade Organization agreement (the Doha Round, which ultimately failed, but Brazil helped advance reforms of intellectual property rules to make medicines cheaper in poorer countries).

Regional economic integration:

One consistent aspect of Brazil's global role has been support for greater regional economic integration through preferential trade agreements. Within South America, Brazil was a driving force for formation of Mercado Común del Sur (Mercosur), a customs union between Brazil and four other Latin American nations (Argentina, Paraguay, Uruguay and Venezuela), which came into effect in 1995. Trade within the Mercosur bloc is mostly tariff-free.

Trade agreements:

The Mercosur bloc concluded a trade agreement with the European Union in 2019 after nine years of negotiations, gradually removing tariffs on 92% of goods traded between the two blocs (many previously attracting tariffs up to 35%). Brazil also wants to negotiate a trade agreement with the US, but this would require changing Mercosur rules, which prevent member countries from signing bilateral trade agreements.

Currency reserves strategy

Financial instability is one of the most undesirable impacts of globalisation for developing economies. Brazil has experienced numerous exchange rate crises caused by sudden shifts of sentiment on financial markets, pointing to high foreign debt and exposure to changing foreign investor sentiment.

Floating exchange rate:

Brazil responded to its history of financial instability by floating its exchange rate in 1988. Floating exchange rates are generally less vulnerable to excessive speculation on foreign exchange markets than fixed rates. While Brazil has continued to experience currency volatility during economic and political crises, these movements have assisted the economy in adjusting to changed conditions.

Building reserves:

Since the global financial crisis of 2008, Brazil has used foreign reserves to cushion itself from financial speculation and risk of financial volatility. Brazil has built the tenth-largest reserves of foreign currency in the world:

- Just $54 billion in 2005

- $343 billion in 2023

The OECD has criticised the size of international reserves held by Brazil, noting the high cost in interest payments by the central bank. However, for Brazil the reserves provide a safeguard against instability in global financial markets.

Political crises: from impeachment to COVID-19

In modern economies, governments play an important role in responding to changing economic conditions and establishing policy priorities. It is rare for political crises to have such economic impact as Brazil has seen in the past decade.

Brazil's recent political crises have seen corruption charges against the last three presidents:

- Lula da Silva served time in prison (later charges nullified)

- Dilma Rousseff lost office before her term ended

- Jair Bolsonaro faces several trials for conduct as president

2014 Petrobras scandal:

Brazil's political crises began in 2014 with one of the biggest corruption scandals in modern history, involving billions of dollars in contracts from state-owned energy company Petrobras. The scandal saw:

- 352 of 594 members of Congress facing criminal accusations

- 27 of Brazil's largest construction companies implicated

- President Rousseff blamed despite no evidence of direct involvement

The scandal and extensive criminal investigation brought the economy to a halt at the same time falling commodity prices were undermining export revenues.

2016 impeachment:

President Rousseff lost popular support amid public anger over corruption, weak economy, poor government services and rising prices. In 2016, Brazil's congress voted her out of office. The official reason was using accounting tricks to make the fiscal deficit appear smaller than it really was, allowing increased public spending before the 2014 election.

Continued instability:

Instead of restoring stability, Rousseff's removal worsened Brazil's political crisis. Within months, new president Michel Temer was caught up in corruption allegations as part of the "Weak Flesh" scandal, where meat packers bribed politicians and officials to ignore food safety law breaches. This resulted in bans on Brazilian meat exports to the US and European Union.

2018 election:

Popular former president Lula had been expected to win the 2018 election but was prevented from standing due to a corruption charge (later nullified by the Supreme Court). With Lula out of the race, populist anti-establishment candidate Jair Bolsonaro won, nicknamed "Trump of the Tropics".

Bolsonaro era (2019-2022):

Brazilian society became increasingly polarised. Political crises continued under President Bolsonaro with:

- Series of scandals involving family members

- Successive resignations by senior officials and cabinet ministers

- Downplaying of COVID-19 pandemic (described as "just a little flu")

- Brazil suffering world's fifth-highest deaths per capita (over 700,000 lives lost)

- Threats to disregard October 2022 election results

- Finance minister shutting the IMF's representative office

2022 return of Lula:

Former president Lula won the 2022 election run-off, returning to power after years of political turmoil.

Recent policy developments

Macroeconomic policy

Key themes concerning economic management emerging from Brazil's recent history:

- Investor concerns about corruption and political incompetence

- Poor management of fiscal policy due to structural problems in public finances

- Better management of monetary policy to reduce inflation

- Despite political instability, progress on managing financial instability and trade liberalisation

Fiscal policy challenges:

After rebounding from the COVID-19 recession, the primary macroeconomic challenge is moving beyond the sluggish growth of the 2010s through implementing overdue structural reforms.

The key issue with Brazil's budget is that less than 15% of expenditure can be changed or removed from one year to the next (discretionary funding), while the remaining 85% is fixed expenditure. This severely limits fiscal policy flexibility.

Structural fiscal measures:

Two key measures address Brazil's fiscal problems:

- Fiscal Responsibility Law: Requires reductions in public debt and a medium-term target for "primary fiscal surplus" (fiscal surplus before payments on government debt)

- Constitutional spending cap (2016): Imposes a spending cap that effectively freezes the national budget in real terms for 20 years. This was introduced after Brazil's credit rating was downgraded to BBB− in 2014, sliding further to BB− in 2023

To stabilise public debt at current levels, an overall public-sector surplus of 1.1% is required.

COVID-19 fiscal response:

Like other countries, COVID-19 led to emergency fiscal measures that, while appropriate according to the IMF, resulted in a sharp 15% of GDP increase in public debt. The government invoked the "escape clause" of the constitutional expenditure ceiling, effectively suspending the Fiscal Responsibility Law.

Fiscal measures included:

- Temporary income support to vulnerable households

- Bringing forward pension payments

- Expanding Bolsa Família to another million households

- Cash transfers to unemployed workers

- Employment support (compensation to workers and incentives for firms to keep employees)

- Lower import levies on essential medical supplies

However, President Bolsonaro continued spending above the cap after the pandemic, worsening high inflation in 2022. The government then provided cost-of-living relief that also exceeded the cap.

2023 fiscal framework:

The new fiscal framework announced by President Lula in 2023 aims to balance fiscal objectives and social responsibility:

- Limits government spending

- Goal of achieving primary budget surplus of 1% by 2026

- Relies on revenue increases to achieve targets (given Lula's commitment to social spending)

Pension reform:

One significant structural reform achieved in recent years was pension system reform, approved by parliament just before the COVID-19 pandemic. Brazil's pension system was one of the world's most generous, accounting for 56% of the national budget and available from age 54 (compared to OECD average retirement age of 66).

The reforms:

- Increased retirement age to 65 for males and 62 for females

- Require individuals to work for 40 years

- Reduced entitlements for those under 70 to encourage longer workforce participation

- Forecast to save $230 billion over 10 years, though this will only stabilise spending at current levels

Monetary policy:

During periods of high inflation, monetary policy plays a central role. This became necessary again in the 2020s as Brazil faced another bout of high inflation, chiefly due to global price increases.

After inflation exceeded 12% in 2022:

- Interest rates rose to 13.75% by August 2022

- Sharp increase from the low of 2% in early 2021

- This proved successful: inflation forecast at 5.6% in 2023, down from 9.3% the previous year

These outcomes represent significant progress given Brazil's history of high inflation (reaching a record 4500% in 1994). Brazil's reliance on high interest rates risks causing economic downturn, but sharp rate increases only mildly affected growth in 2023.

Exam tip: Analysing Macroeconomic Policy Trade-offs

When analysing Brazil's macroeconomic policy mix, evaluate the trade-offs between different objectives:

Tight monetary policy:

- ✓ Controls inflation effectively

- ✗ May slow economic growth

- ✗ Increases cost of borrowing

Expansionary fiscal policy:

- ✓ Supports vulnerable populations

- ✓ Stimulates economic activity

- ✗ Increases public debt

- ✗ May worsen inflation

Show understanding of these policy dilemmas rather than suggesting simple solutions. Real-world policy requires balancing competing objectives.

Microeconomic policy

Comprehensive reviews by the IMF and OECD have set out a detailed agenda for microeconomic reform in Brazil. They highlight policy challenges Brazil needs to address for long-term sustainable growth:

Trade openness:

- Brazil remains "one of the most closed major economies in the world" (IMF)

- Although the world's ninth-largest economy, it represented just 1% of global trade value in 2022

- Trade as a proportion of GDP (39%) is lower than all but seven other countries globally

- Brazil has been the world's third-most active user of anti-dumping actions in the WTO

Labour productivity:

- Brazil needs to increase labour productivity, which is low by international standards

- Around one-third the level of main regional competitor Argentina

- Productivity growth will be the main engine of long-term growth

- Strengthening it requires more competition in many sectors to allow labour and capital to move to activities with strong potential

Education improvements:

Brazil has a young population but poor education outcomes:

- Quality of education (measured by PISA tests) below OECD average

- Expected to deteriorate due to high drop-out rates during COVID-19

- Vocational education especially weak (fewer students enrolled than all but three OECD economies)

- Share of young adults completing tertiary education is 23 percentage points below OECD average (2021)

Infrastructure development:

More rapid progress needed on infrastructure:

- Transport infrastructure important in a country as large and populous as Brazil

- Road, rail and port quality ranks poorly in international studies

- A major 2019 IMF report noted Brazil invested an average of just 2% of GDP in public infrastructure over the past two decades – around one-third the average level of other emerging economies

Government reform:

- Political crises revealed corruption throughout government, stifling economic growth

- In 2022, Brazil ranked 94th among 180 countries on Transparency International's annual corruption index

Tax system overhaul:

The IMF recommends:

- Replace complex indirect taxes with a single broad-based value-added tax

- Remove complexities making tax compliance expensive

- World Bank's 2020 "Ease of Doing Business" report ranked Brazil 124th out of 190 countries

- Takes almost 2000 hours on average for a business to prepare tax returns – more than any other country (compared to around 200 hours for most economies)

Regulatory simplification:

OECD's Product Market Regulation Indicators report finds Brazil highly restrictive. Excessive regulations have encouraged a culture of "jeitinho" (finding a way around laws or rules, sometimes illegally).

Brazil's complex system of environmental licences often criticised by foreign investors and evaded by local developers. In other areas, failure to enforce regulations (e.g., 2018 EU ban on imports from seven Brazilian meat processing factories due to food safety concerns).

Successful social policies:

Despite challenges, Brazil has created successful and innovative social policies:

Case Study: Bolsa Família (now Auxilio Brasil)

Introduced in 2004 to assist poor households. Success led to expanded education, elderly care, health and micro-lending package called Brasil Sem Miséria (Brazil Without Misery). This program incorporated the Fome Zero (Zero Hunger) program, providing monthly support to around 14 million of Brazil's poorest families.

By merging income distribution payments, the government targeted inequality more effectively. Its cost (just 0.6% of GDP) is very small compared to 14% of GDP spent on pension benefits that mostly go to Brazil's less needy middle class.

Conclusion

Brazil is rebuilding from a once-in-100-years pandemic that eroded the health system and left an already weak economy with political instability in deep recession, followed by high inflation and high interest rates. Nevertheless, President Lula has ambitions for Brazil to be the leading advocate for developing countries in the global economy, with an agenda to reform trade, finance, climate and globalisation itself.

President Lula must first reckon with significant challenges at home after a decade characterised by long recession, corruption scandals and catastrophic mismanagement of the COVID-19 pandemic. Brazil is also far more politically divided than when Lula was first in office in the 2000s.

Institutional strength:

For a country that only became a democracy in 1988, Brazil's institutions have endured a difficult period and proved to be strong, stable and mostly independent (with some exceptions). These are important elements of a positive environment for long-term investment and growth.

Future potential:

Brazil has potential to play an important role in the future global economy because of:

- Size of population and economy

- Proven potential in diverse export markets (minerals, fuels, food, manufactures)

If strong commodity prices are sustained, Brazil's recovery prospects will strengthen. However, it will take time to rebuild confidence in Brazil's economic future.

Requirements for success:

To maintain investor confidence and strengthen Brazil's place in the global economy, Brazil needs to improve:

- Educational performance

- Regulatory framework

- Fiscal management

Events of recent years underscore the importance of:

- Political stability

- Anti-corruption measures

- Rule of law

These provide foundations for confidence and growth.

Remember!

Key concepts:

- BRIC economies: Brazil, Russia, India, China – major emerging economies

- Gini index: Measure of income inequality (0 = perfect equality, 100 = perfect inequality). Brazil's 52.9 is one of the world's highest

- Stagflation: Simultaneous high inflation and unemployment – rare phenomenon Brazil experienced in 2010s

- Conditional cash transfers: Social welfare payments requiring recipients to meet conditions (e.g., Bolsa Família requires school attendance and health check-ups)

- Import substitution: Strategy of replacing imports with domestic production rather than developing exports

- Debt servicing ratio: Cost of servicing foreign debt as percentage of export earnings

- Mercosur: South American customs union led by Brazil

- Sovereign debt: Government borrowing, rated by agencies for investment quality

Development achievements:

- HDI improved from 0.68 (2000) to 0.754 (2021-22), ranking 87th globally

- Life expectancy rose from 63 years (1980) to 76 years (2019), but fell to 72 due to COVID-19

- Extreme poverty fell from 23.2% (2002) to 5% (2019) – best improvement in Latin America

- Gini index fell from 60 (2000) to 49 (2020), before rising to 53 during COVID-19

Economic challenges:

- Average growth in 2000s: 3.7% annually; 2010s: fractionally above zero

- 2015-2016 recession so severe it approached depression

- Stagflation in 2010s: unemployment reached 13.7%, inflation 9%

- COVID-19 recession: economy contracted 4.1% (2020), unemployment exceeded 14%

- Still one of world's most unequal societies despite progress

Seven factors explaining 2014-2016 recession:

- Commodity price collapse (8 of top 10 exports were commodities)

- Lack of economic diversification

- Massive corruption scandal (Petrobras)

- Loss of investor confidence (budget deficit 11% of GDP by 2016)

- Credit rating downgrade to below investment grade

- Policy failures (price controls, state lending, infrastructure projects)

- Unresolved structural problems (productivity, infrastructure, education)

Globalisation impacts:

- Export revenues: $55bn (2000) → $250bn (2011) → $335bn (2022)

- Foreign trade increased from 15% of GDP (1990) to 39% (2022) – still low by international standards

- External debt to GDP ratio: 36.6% (2000) → 16.3% (2023)

- Debt servicing ratio: 89% (2000) → 29% (2023)

- Foreign currency reserves: $54bn (2005) → $343bn (2023)

Policy responses:

- Average tariffs reduced from 32.2% (1990) to 8% (2020)

- Floating exchange rate since 1988

- Bolsa Família program (2004): conditional cash transfers to poor households – costs only 0.6% of GDP

- Pension reform: retirement age increased to 65 (male) and 62 (female), forecast to save $230bn over 10 years

- 2023: Interest rates 13.75% to combat inflation (down to 3% from 12%)

Exam preparation:

- For "explain" questions: Link factors together (e.g., commodity dependence → price falls → recession → corruption exposed → confidence loss → deeper recession)

- For "analyse" questions: Examine causes and consequences with data support (e.g., how did corruption scandal affect economic performance?)

- For "evaluate/assess" questions: Weigh successes (poverty reduction, debt management) against failures (recession, inequality, environmental damage). Consider short-term vs long-term impacts

- Always support arguments with specific Brazilian data and examples

- Compare Brazil with other emerging economies where relevant (especially other BRIC nations)

- Consider political economy factors (why reforms are difficult, how inequality affects policy choices)