Indonesia (HSC SSCE Economics): Revision Notes

Indonesia

Introduction to Indonesia's economy

Indonesia represents a significant case study in examining the impacts of globalisation on an emerging economy. Located in South-East Asia, Indonesia is the region's largest economy and the world's fourth most populous nation with 277 million people. Since opening its economy to global forces in the mid-1980s, Indonesia has experienced substantial economic transformation through increased trade, foreign investment, and participation of transnational corporations.

The country demonstrates both the opportunities and challenges of globalisation. While economic development has improved quality-of-life indicators, Indonesia has also faced major economic disruptions, including the devastating Asian financial crisis of 1997-98 and the COVID-19 pandemic.

Understanding Indonesia's economic journey is particularly valuable for Australia given the growing trade and financial linkages between the two nations.

Economic performance and development

Size and structure of the economy

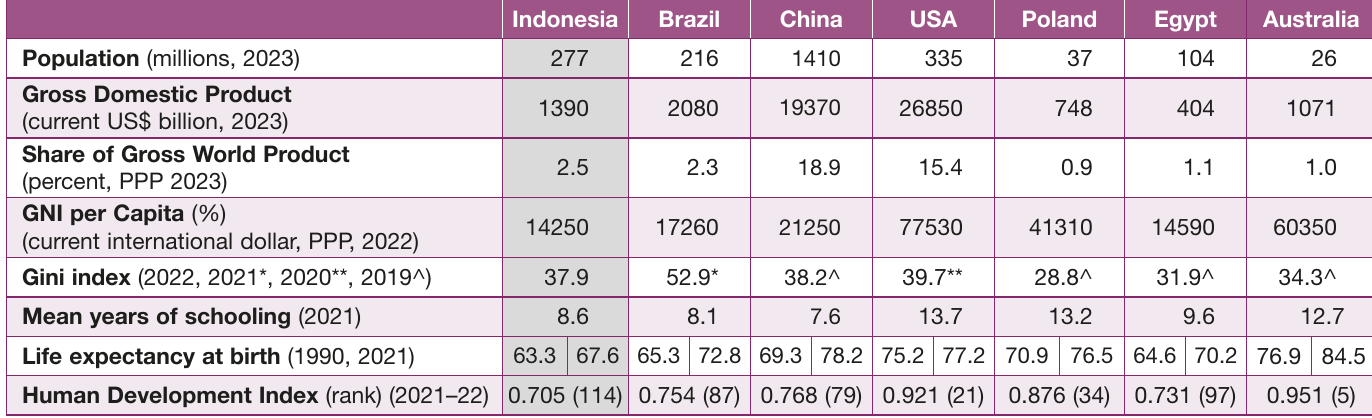

Indonesia's economy is valued at approximately US$1.4 trillion, making it the world's 16th-largest economy. While considerably smaller than major economies like China (15 times larger) or the United States (nearly 20 times larger), Indonesia exceeds neighbouring economies such as Thailand and Malaysia, whose economies are roughly half its size.

Living standards remain relatively low despite significant improvements over recent decades. In 2022, output per capita stood at US$4,788 (without purchasing power adjustments), representing more than a fivefold increase from the US$780 recorded in 2000. These living standards are comparable to the Philippines and Vietnam but approximately half those of Thailand and Malaysia. The World Bank downgraded Indonesia from upper-middle-income to lower-middle-income status in mid-2021 following the pandemic's impact.

Development indicators and quality of life

Indonesia's Human Development Index of 0.705 ranks it 114th globally, reflecting various challenges in economic development. This ranking primarily reflects low per capita income but also indicates relatively poor performance in adult literacy and life expectancy.

Health outcomes are particularly concerning, with 14% of the population lacking access to basic sanitation facilities and approximately one in ten Indonesians without access to basic drinking water services. Healthcare expenditure stands at around US$120 per person annually, significantly below comparable regional countries.

Despite these challenges, Indonesia has achieved substantial development progress:

- Life expectancy has improved by six years since 1990

- The under-five child mortality rate has decreased by nearly 75%, falling from 84 deaths per 1,000 births to 22 deaths over the same period

Income inequality in Indonesia, measured by a Gini index of 38, is similar to regional economies like Malaysia and Vietnam. The distribution of income is more equal than in many countries beyond the region, such as the United States and Brazil.

Indonesia as an emerging economy

Indonesia has transitioned from being classified as a developing economy to an emerging economy, reflecting its strong growth performance and prospects. This classification recognises Indonesia's success in transforming its industry structure to enhance economic performance and development.

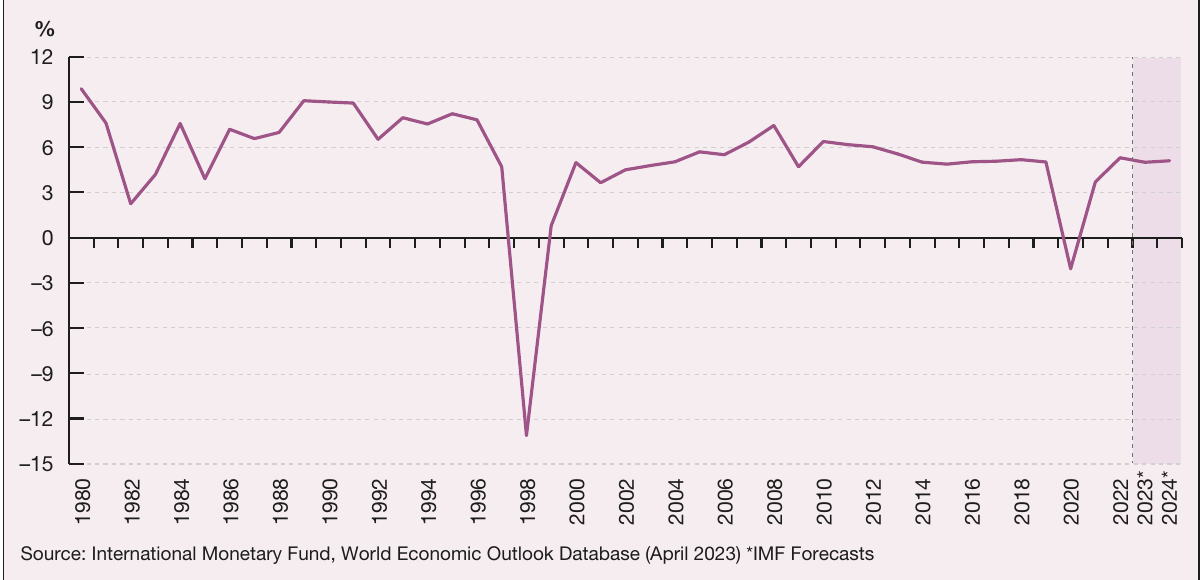

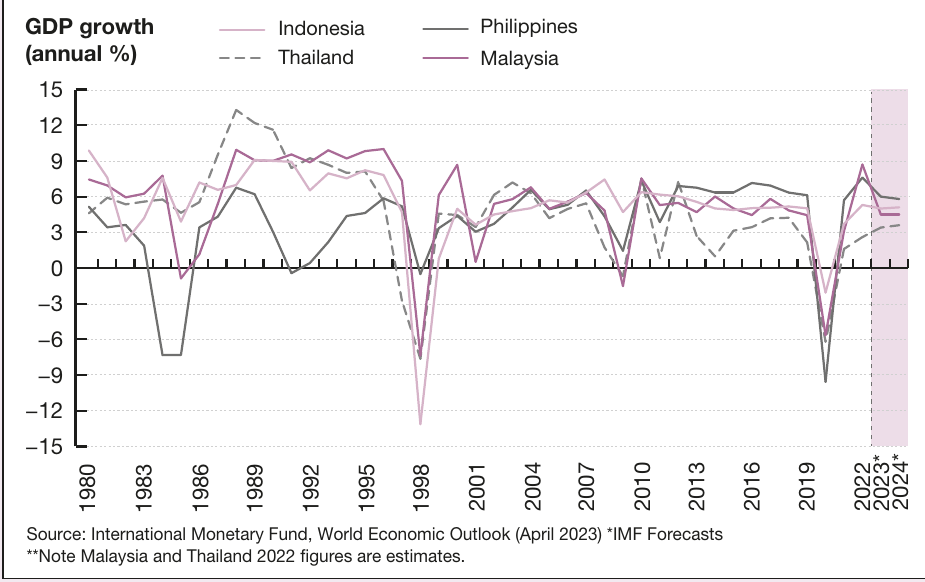

Between 1980 and 2023, Indonesia achieved an average annual growth rate exceeding 5%. Although not as rapid as some neighbouring East Asian economies, this growth rate significantly exceeds most economies worldwide, including advanced economies in Europe and North America, and emerging economies in Latin America, Central and Eastern Europe, and Africa.

Indonesia's growth trajectory has been influenced by both international and regional business cycles. During the 1970s, as a major oil exporter, Indonesia experienced accelerated growth while most economies struggled with rapid oil price increases. The 1980s brought the opposite effect, as oversupply pushed oil prices down, slowing Indonesian growth. The 1990s saw Indonesia participate in an East Asian growth boom that ended abruptly with the 1997 Asian financial crisis, resulting in a devastating 13% economic contraction in 1998.

In 2020, the COVID-19 pandemic caused the economy to contract by 2.1% - the first annual GDP decline since the Asian financial crisis. Unemployment rose by 1.8 percentage points to 7.1% in 2020. However, by the end of 2021, output had returned to pre-COVID-19 levels. Economic growth was forecast at 5% for 2023 and 2024, supported by export growth and investment. The labour market recovered rapidly, with unemployment falling to 5.9% in 2022 and expected to return to the pre-COVID-19 rate of 5.2% in 2024.

With its large population and continued economic growth, Indonesia is projected to join the world's largest emerging economies (the BRIC economies: Brazil, Russia, India, and China) in coming decades. Consulting firm PwC projects Indonesia will surpass Germany and Japan to become the world's fourth-largest economy by mid-century.

Structural transformation of the economy

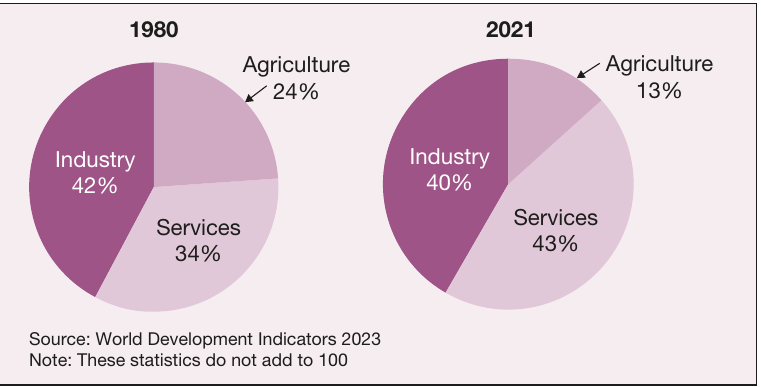

A characteristic feature of Indonesia's emergence as a developing economy is the transformation of its industry structure in recent decades. Like many East Asian economies, Indonesia has witnessed the declining economic importance of agriculture while manufacturing industries and services have become more significant.

The data reveals substantial structural change over four decades:

- Agriculture's share of GDP fell from 24% in 1980 to 13% in 2021

- Industry's contribution decreased slightly from 42% to 40%

- The services sector experienced the most significant growth, expanding from 34% to 43% of GDP

Primary industries

Despite structural shifts, Indonesia's primary industries remain important. Outside the formal economy, most of Indonesia's rural population survives on subsistence agriculture, with wages paid as crop shares. Rice is the main agricultural product, supplemented by rubber, coffee, cocoa, and spices.

Unlike other regional economies, Indonesia maintains a substantial oil and gas industry. Until 2016, Indonesia was Asia's only member of OPEC (Organisation of the Petroleum Exporting Countries). Palm oil, coal, petroleum oil, and gas comprised a quarter of total exports from 2000-2020. This dependence on resource-intensive exports exposes Indonesia to currency volatility.

Manufacturing sector

Indonesia's manufacturing sector includes a large textile and garment industry and other labour-intensive manufacturing. The sector has declined from 31% of GDP in 2002 to 19% in 2021. According to the World Bank, this typically occurs when countries achieve higher income levels, but in Indonesia's case it reflects lower competitiveness compared to similar economies.

Manufacturers face poor infrastructure, limited access to finance, complex regulations, and increased import barriers that raise capital goods costs.

Nevertheless, Indonesia possesses two key advantages for manufacturing growth: a large, low-cost labour force and a substantial domestic market.

Services sector

Indonesia's fastest-growing sector is services. In 2021, the services sector comprised 43% of GDP, employing 49% of the workforce. Main services include tourism and retail. Information and communications technology is expected to be a primary driver of future services sector growth.

The services sector enjoys increasing foreign direct investment flows, with services accounting for over one-third of Indonesia's investment inflow. Growth in information and communications services demonstrates the positive role of investment by foreign technology companies in enhancing the Indonesian workforce's skills. However, the services sector faces constraints from poor infrastructure and technology, inadequate workforce skills, and some of the world's highest trade barriers for services.

Progress on development goals

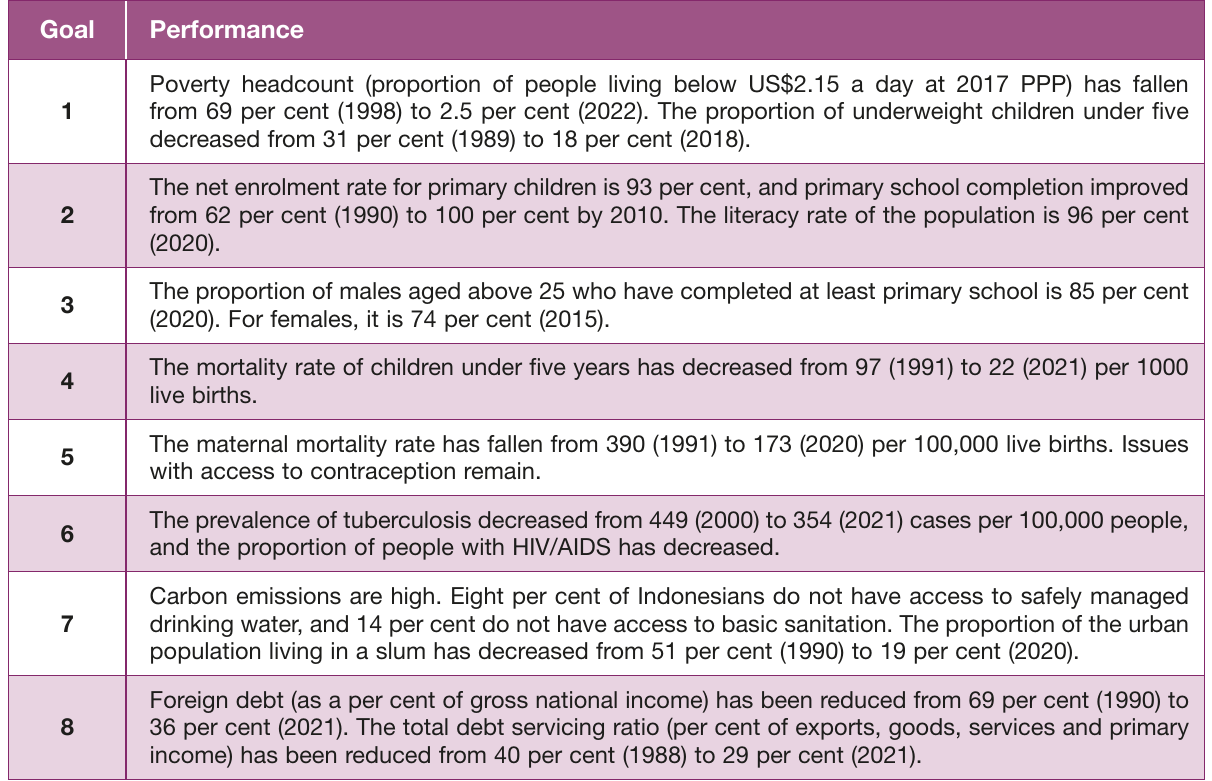

Indonesia did not meet all Millennium Development Goals by the 2015 target year but made significant progress in many areas. The Indonesian Government has committed to delivering progress on the Sustainable Development Goals, building on achievements with the MDGs in areas including poverty reduction, gender equality, and addressing climate change's long-term impacts.

Key Economic Development Points:

- Indonesia has transformed from a predominantly agricultural economy to a services-based economy (43% of GDP)

- GDP per capita has increased fivefold since 2000, though living standards remain relatively low at US$4,788

- Manufacturing sector faces competitiveness challenges but benefits from large domestic market and low-cost labour

- Services sector is the fastest-growing, driven by tourism and ICT

Environmental impacts of growth

Deforestation and environmental degradation

Degradation of the natural environment represents a significant cost of industrialisation and globalisation in the Indonesian economy. Indonesia possesses the world's third-largest rainforest yet also experiences one of the world's highest deforestation rates.

A 2019 Greenpeace study showed that more than 74 million hectares of rainforest - an area twice the size of Japan - was cleared over the past half-century. This results from commercial logging, land clearing for agriculture, mining developments, and population expansion.

The Indonesian Government has implemented a moratorium on new clearing for approximately 66 million hectares of primary forest and peatland. Retention of Indonesia's rainforests is crucial for various reasons, including their role in carbon absorption. Forest clearing saved under the moratorium contributed 86.9 million tonnes of emissions reductions between 2011-2018, despite retaining only an average of 0.65% more forest coverage than non-moratorium areas.

Other key environmental concerns include:

- 265 critically endangered animal and plant species as of 2019

- Major challenges in protecting the marine environment due to Indonesia's vast coastline, industrial pollution, and over-exploitation of fishing stocks

Carbon emissions and climate change

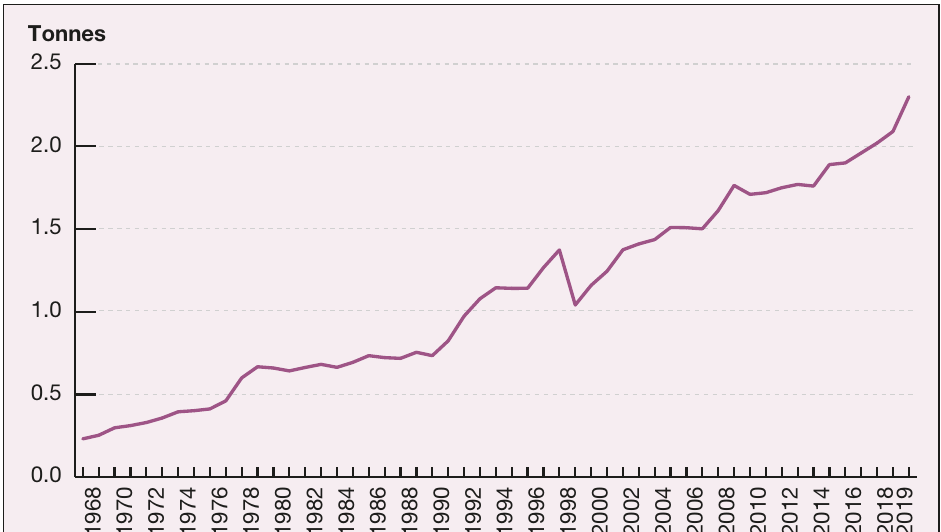

Indonesia's rapid economic and population growth places pressure on its ability to reduce emissions. Although per capita carbon dioxide emissions are relatively low at 2.3 tonnes per year, Indonesia ranks as the world's eighth-largest contributor to global carbon dioxide emissions (including deforestation-related emissions).

This is concerning because Indonesia is especially vulnerable to climate change's future impacts due to its high coastal population density. The World Risk Index ranks Indonesia's exposure to natural hazard-related risk as fifth-highest globally.

Climate risks have accelerated plans to relocate the capital from Jakarta on Java to the new forest city of Nusantra on Borneo, approximately 1,000 km away.

Indonesia has already witnessed a sharp increase in climate-related adverse weather events. The number of adverse events rose from 82 in 2000 to 3,058 in 2022. Recent examples include:

- 2019 land and forest fires: 600,000 hectares burned, 900,000 people contracted respiratory illnesses

- 2022 West Java earthquake: killed at least 335 people

Climate commitments and renewable energy

Reducing carbon dioxide emissions while maintaining economic growth will be a key environmental management challenge. Indonesia has committed through its Nationally Determined Contribution (NDC) to reduce emissions by 32% by 2030 and reach net zero emissions by 2060 or sooner. These commitments require significant policy and investment.

Indonesia is focusing on reducing electricity sector emissions by 49 million tonnes by 2028, with a shift towards renewable sources. In 2021, Indonesia's government utility company Perusahaan Listrik Negara (PLN) committed to building no new coal-fired plants after 2022 and phasing out all coal plants by 2056. The Indonesian Government has also committed to a 23% renewable energy target by 2030.

However, despite large sources and investment in geothermal and hydropower, Indonesia is unlikely to meet this target. Government efforts in renewable energy have focused on small-scale projects, such as installing solar panels in villages. Large public investment is needed, particularly in distribution infrastructure, to ensure renewable energy can be added to the system.

Resource management challenges

Indonesia confronts several other environmental issues, particularly relating to resource management. Indonesia has the second-highest plastic waste among the world's 146 coastal countries. The Government has a policy to slash marine litter by 70% by 2025 (achieving a 15% reduction by 2020).

Policy Success: Plastic Bag Reduction

In 2016, the Government introduced a charge on plastic bags. Within three months, this step reduced plastic bag use across Indonesia by 25%.

This demonstrates how targeted policy interventions can achieve rapid behavioral change in environmental management.

Environmental Challenges Summary:

- Indonesia faces severe deforestation (74 million hectares cleared in 50 years) and ranks as the world's 8th-largest carbon emitter

- Climate vulnerability is high due to coastal population density, with adverse weather events increasing from 82 (2000) to 3,058 (2022)

- Commitments include 32% emissions reduction by 2030 and net zero by 2060, requiring major investment

- Resource management challenges include plastic waste (2nd-highest globally) and marine protection

Indonesia's path to globalisation

Trade liberalisation since the 1980s

Since opening to global forces in the 1980s, globalisation has reshaped the Indonesian economy. Reforming the economy has been necessary for Indonesia to keep pace with other South-East Asian economies and avoid excessive reliance on commodity exports, whose value on global markets tends to be volatile. As the 1970s oil boom subsided, Indonesia needed more sustainable foundations for long-term economic growth, with exporting manufacturing goods central to this strategy.

Historical protection and the shift to openness

Prior to the mid-1980s, Indonesia was a highly protected economy. Indonesia's 1970s oil boom saw the imposition of strict trade barriers protecting government-sponsored and government-owned business enterprises. Protection methods included tariffs, licensing requirements, local content rules, and import monopolies.

One area that historically faced high non-tariff barriers was agriculture. In the mid-1980s, under control of Indonesia's sole approved rice importer, Bulog, the country achieved self-sufficiency in rice production and phased out all rice imports. The effective rate of protection for agriculture between 2011-2020 averaged 27% of total consumption, much higher than regional peers, contributing to higher domestic prices.

Many farmers are also disadvantaged by protectionism, as two-thirds buy more food than they sell (making them "net food buyers"). This means protective barriers that raise domestic food prices actually harm most farmers rather than helping them.

Indonesia's shift towards trade liberalisation began in the mid-1980s. The average level of tariffs was reduced by almost one-third. Between 1987 and 1995, the effective rate of tariff protection for manufacturing fell from 86% to 24%. For agriculture over the same period, it halved from 24% to 12%. The Government also relaxed the complicated network of import licensing restrictions through annual deregulation and liberalisation packages aimed at reducing barriers to foreign trade and investment.

After the Asian financial crisis in 1998, Indonesia continued pursuing trade liberalisation under IMF program auspices. Tariff and non-tariff barriers were reduced, together with easing restrictions on foreign investment. However, in the decade to 2020, the average tariff level increased marginally.

By 2020, the simple mean tariff rate applied to imported goods was 6%, down from 17% in the early 2000s, similar to the 5% average for the East Asia and Pacific region.

Regional and global trade agreements

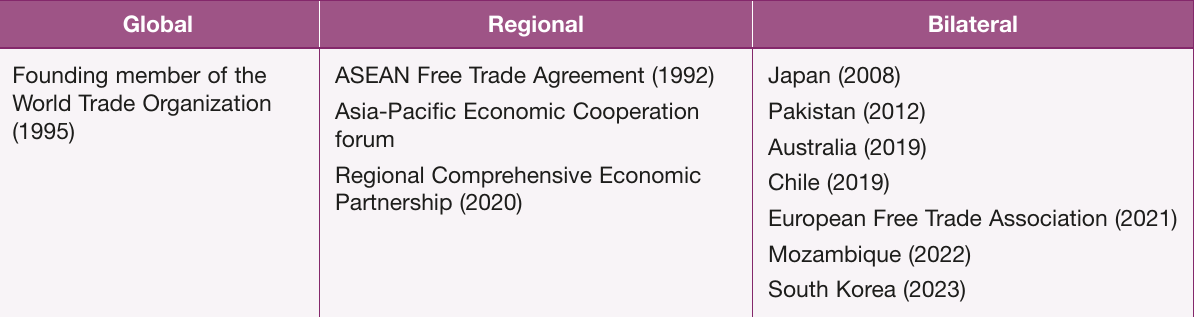

Indonesia has become increasingly integrated with the global economy through participation in global, regional, and bilateral trade agreements. Indonesia has also become more prominent on the global stage, particularly through its membership in the Group of 20 (G20) major economies.

World Trade Organization

Indonesia has been an active World Trade Organization (WTO) member since 1995. With almost one-third of the population employed in agriculture, Indonesia supported the failed Doha Round of trade negotiations, hoping for reductions in agricultural protection by advanced economies.

However, Indonesia also argued that "special and differential treatment" provisions must be at the heart of negotiated agreements. This refers to provisions in WTO agreements giving developing countries special rights, such as a slower tariff reduction schedule.

ASEAN and regional integration

The process of regional integration has seen the Association of South-East Asian Nations (ASEAN) emerge as the most important regional organisation. Formed in 1967 by Indonesia, Malaysia, the Philippines, Singapore, and Thailand, ASEAN has since expanded membership to include Brunei, Burma, Cambodia, Laos, and Vietnam.

The ASEAN Free Trade Area (AFTA) agreement, signed in 1992, aims to reduce tariff and non-tariff barriers within the region. It uses a Common Effective Preferential Tariff scheme, where tariffs are less than 5% for goods originating among member economies.

In 2007, ASEAN leaders adopted a blueprint for creating the ASEAN Economic Community (AEC), intended to create a single market of around 600 million people, allowing free flow of goods, services, capital, and labour. The AEC vision is to enhance South-East Asia's attractiveness as a foreign investment destination and improve regional integration. While the initial plan was to establish the AEC by 2015, this was revised under the AEC Blueprint 2025, giving members another decade to pursue reforms and initiatives needed to achieve the vision of a highly integrated, cohesive, and competitive economic region.

Indonesia is also party to several other trade agreements through the ASEAN Plus Three framework. ASEAN has concluded free trade agreements with China, South Korea, Japan, India, Australia, and New Zealand. Indonesia is also a member of the Asia-Pacific Economic Cooperation (APEC) forum, which has aimed to advance regional and global trade and investment liberalisation. Indonesia is also a member of the Regional Comprehensive Economic Partnership (RCEP), the world's largest trade bloc, which came into force in 2022.

Bilateral agreements

The Indonesia-Australia Comprehensive Economic Partnership Agreement was signed in March 2019, reflecting the growing significance of economic relations between the two countries. Under this agreement, almost all import tariffs in both countries were reduced or eliminated, effective from 2020. Australian primary industry exports such as frozen beef and sheep meat are now processed more quickly at the border, reducing trade barriers. Total trade between Australia and Indonesia was A$18 billion in 2021-22, making Indonesia Australia's 14th most significant trading partner.

Indonesia also has a comprehensive bilateral trade agreement with Japan that took effect in 2008. Japan accounts for 8% of Indonesia's exports and is its third-largest export destination after China (23%) and the United States (11%). Indonesia has agreements with South Korea, Chile, Mozambique, Pakistan, and the European Free Trade Association (comprising Norway, Switzerland, Iceland, and Liechtenstein). Indonesia has also signed, or is negotiating, agreements with the EU, India, Tunisia, and Türkiye, but these are not yet in force.

Changes in trade patterns

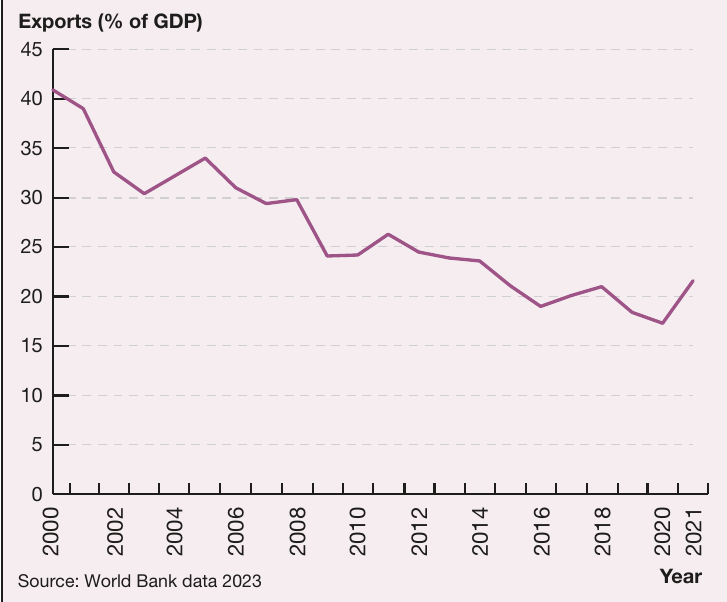

Trade liberalisation has improved Indonesia's access to overseas export markets and led to stronger economic growth. Exports of goods and services have grown at an average annual real rate of 4.9% globally in the period between 1980-2020. Meanwhile, Indonesia's trade expanded by 5.2%. While giving the country access to wider markets and improving export industry revenues and employment, this trade growth was low when compared with Malaysia, Thailand, and the Philippines, which grew 12-fold.

The contribution of trade to Indonesia's economy (as measured by percentage of GDP) has fallen over the past two decades. Trade in goods and services equalled around 33% of Indonesia's GDP in 2020, down from 72% in 2000. A major reason for the declining contribution of trade is that Indonesia still relies on a relatively narrow base of commodity exports.

The contribution of trade to the Indonesian economy is lower than the regional average for East Asian and Pacific economies (56%), highlighting the potential for Indonesia to expand further into international markets. While being the 16th-largest economy with the 4th-largest population, Indonesia is only the 25th largest in exports. This means that, through trade linkages at least, Indonesia is less exposed to the international business cycle than some other economies. With nearly three-quarters of its trade being with other Asian economies, Indonesia is most closely integrated at a regional level with economies such as Japan, China, Singapore, Malaysia, and South Korea.

Export composition and future directions

Since the mid-1990s, Indonesia's export base has shifted back towards food and fuels, with manufactured exports falling as a share of trade. High-technology exports contribute less than 3% of Indonesia's total export revenues. Unlike many other regional economies, Indonesia has not emerged as a major low-cost manufacturer for global markets, relying instead on commodity exports. This partly reflects the fact that some commodity prices have remained strong, but also highlights Indonesia's need to develop sustainable exporting industries in coming years.

Service exports, particularly tourism, represent an area of potential growth for Indonesia. The Indonesian Government has also promoted "resource down-streaming" or value-adding to existing commodity exports, pointing to the success of a government ban on the export of unrefined nickel ore in 2020 that substantially increased nickel-based steel exports by 2022. Nickel is also an important component in electric vehicle batteries, and Indonesia hopes to become one of the world's three largest manufacturing hubs for EV batteries by 2027.

Despite economic reforms of recent decades, Indonesia's main exports remain oil and gas, coal, palm oil, steel, and electrical machinery/equipment.

Financial liberalisation and foreign investment

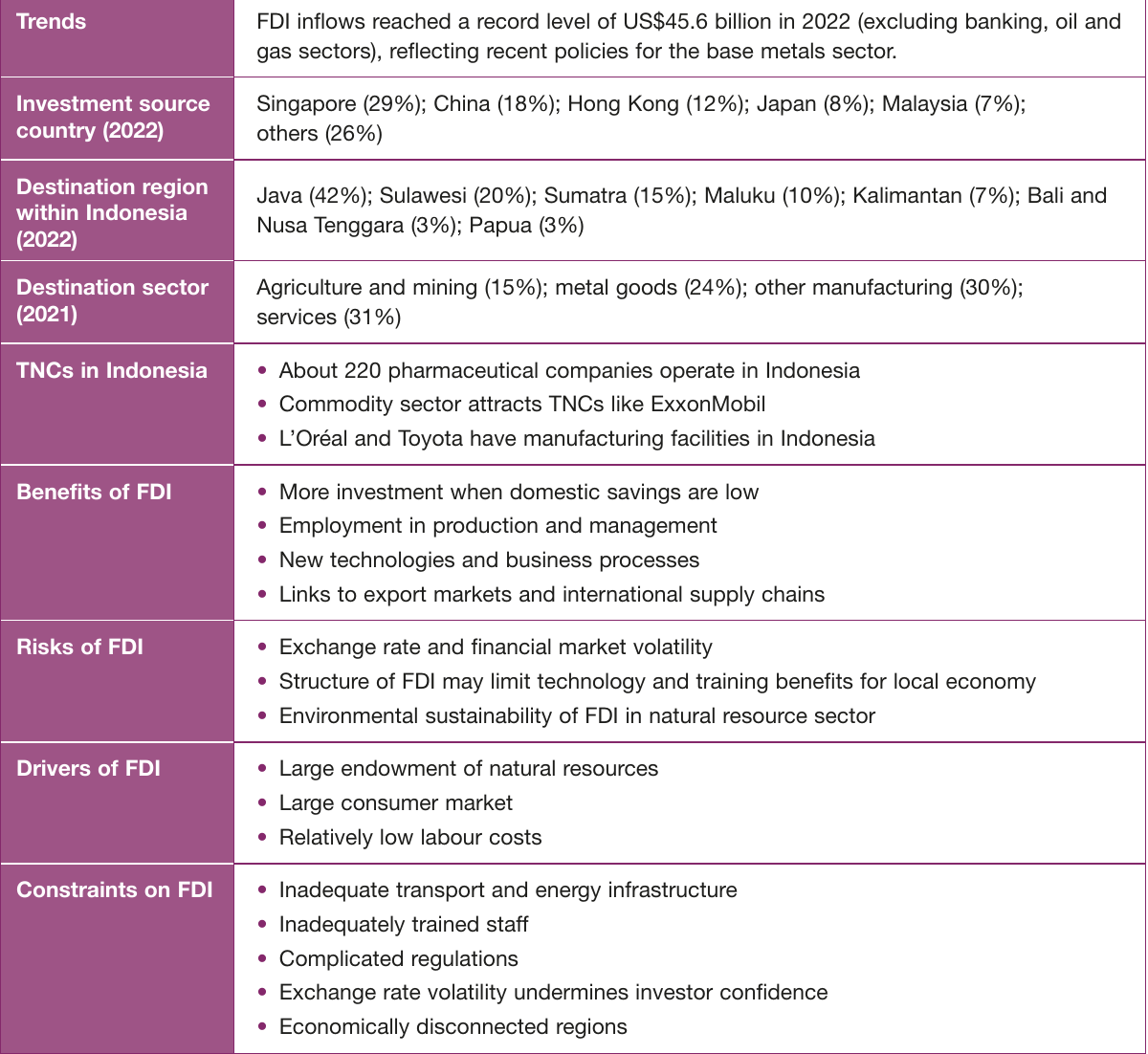

Indonesia has reduced barriers to financial and investment flows during the globalisation era to encourage economic growth and development. From the mid-1980s, Indonesia pursued tax reforms, deregulation of industry sectors, and removal of restrictions on foreign ownership. While previous decades saw FDI flow mainly to oil and mining sectors, the 1990s saw increased investment flow into manufacturing.

FDI trends and characteristics

While FDI reached a record level in 2022, overall FDI inflows to Indonesia remain lower than in comparable countries, owing to uncertainty about government policy settings and lower levels of international competitiveness.

FDI Success: Nickel Processing

Following the government decision to ban raw nickel ore exports, Chinese and US companies invested in local processing facilities to secure supplies of nickel, a critical input for electric vehicle production.

This demonstrates how strategic trade policy can encourage value-adding foreign investment.

Encouraging FDI, along with continuing to reduce trade barriers, is important to securing export-led development. The largest sources of foreign investment in 2022 were Singapore (29%), China (18%), Hong Kong (12%), Japan (8%), and Malaysia (7%).

Currency and financial markets

Financial markets have also been liberalised in recent decades to encourage economic growth, beginning with Indonesia's shift from a fixed exchange rate to a managed float in 1978. The currency, the Indonesian rupiah, was devalued during the 1980s as a deliberate strategy to improve export competitiveness. The managed float was abandoned during the Asian financial crisis in August 1997, and the rupiah was allowed to float freely after the central bank's attempts to stabilise the currency were unsuccessful. The rupiah suffered a massive depreciation, causing major turmoil in financial markets and the economy.

Currency volatility continues as a problem in Indonesia, with major shifts in the rupiah caused more by global factors than domestic factors. To reduce instability and encourage longer-term foreign investment, the Indonesian Central Bank has strengthened capital controls in financial markets, with investors in government bonds required to hold them for a minimum of six months, slowing the pace of any "capital flight".

IMF research has found currency volatility reduces private sector investment - for every 1% increase in volatility, there is a reduction in investment of almost 0.2%.

Foreign aid and development assistance

Economic development in Indonesia has been supported by foreign aid and assistance. The World Bank funds many active projects in Indonesia with a cumulative lending value of US$19.6 billion. These programmes have targeted community empowerment, government administration, energy, and infrastructure development. Australia was expected to provide Indonesia with $286 million in official development assistance in 2023-24, and also donated 8 million doses of COVID-19 vaccines during the pandemic.

Globalisation and Trade Summary:

- Trade liberalisation since mid-1980s reduced tariffs from 17% to 6% by 2020

- Indonesia participates in major trade agreements (WTO, ASEAN, RCEP, bilateral deals with Australia and Japan)

- Trade as percentage of GDP fell from 72% (2000) to 33% (2020) due to narrow commodity export base

- Major FDI sources: Singapore (29%), China (18%), Hong Kong (12%)

- High-technology exports remain very low at less than 3% of total exports

The Asian financial crisis

The Asian financial crisis of 1997 and 1998 was an early example of possible negative impacts of globalisation. As the economy most severely affected by the crisis, Indonesia's experience highlights how volatile global financial markets, combined with economic mismanagement, can have devastating consequences for economic growth and development.

Background and onset

The rapid growth of South-East Asian economies for much of the 1990s had led to a flood of short-term financial inflows that were increasingly flowing into stock markets, consumer finance, and real estate. Inadequate banking regulations saw finance flow to customers that did not meet normal creditworthiness standards.

In July 1997, sentiment changed as foreign investors reassessed the value of their assets and loans and suddenly withdrew their funds - known as "capital flight". Beginning with the Thai baht, the currencies of South-East Asian economies depreciated rapidly as financial outflows mounted. The financial "contagion" of the crisis also spread to other economies, including Indonesia, South Korea, and Malaysia.

IMF response and policy measures

To obtain an emergency US$18 billion financial assistance loan from the IMF, the Indonesian Government was required to undertake policy measures including:

- Spending cuts

- Budget surpluses

- Dramatically raising interest rates (to 80%)

- Closing some banks

- Cutting fuel subsidies

- Undertaking long-term structural reforms

Although designed to strengthen the Indonesian economy in the long term, these policies had the immediate effect of further undermining confidence and choking off economic activity. By mid-1998, as panic spread to Indonesia's businesses, households, and other deposit holders, the rupiah had lost 85% of its value against the US dollar (to be worth as little as Rp 16,000 to the US dollar) and the managed float was abandoned.

Devastating economic consequences

The Asian financial crisis had devastating economic consequences for Indonesia:

- The economy shrank by over 13%

- Unemployment increased substantially

- The number of people in poverty almost doubled from 11% to 19%

- As the exchange rate depreciated and import prices soared, inflation was recorded at over 75%

- Foreign debt increased to US$148 billion

- In May 1998, Indonesian President Suharto was forced to step down after over 30 years in office

- It took six years before living standards returned to pre-crisis levels

Causes and lessons

Aside from the mishandling of the crisis by the IMF and the Indonesian Government, economists often cite two causes of Indonesia's problems:

1. The combination of open financial markets with a fixed exchange rate:

The rupiah became overvalued, and because it was fixed, there was no mechanism for it to adjust to its market value

2. Excessive financial speculation and poor regulation of the financial sector during rapid globalisation

The Asian financial crisis in Indonesia highlights how, without an appropriate policy framework, global economic forces can destabilise an economy and cause extensive economic and social harm.

Reforms and lasting impact

The Asian financial crisis led to major economic reforms, including:

- Establishment of an independent central bank (Bank Indonesia)

- A new bankruptcy law

- Measures to promote competition and improve the social safety net

- The Indonesian Bank Restructuring Agency (IBRA) oversaw reforms to the financial sector

The Asian financial crisis also forced a change in the way the IMF responds to financial crises. In contrast to its policy prescriptions for Indonesia in the late 1990s, during the global financial crisis and the COVID-19 recession in the following two decades, the IMF recommended that economies actively stimulate growth through increased spending, lower interest rates, and boosting credit market liquidity.

As one of the first major crises of the modern era of globalisation, the Asian financial crisis helped shape future economic policy.

Asian Financial Crisis Key Points:

- Indonesia was the most severely affected economy, with a 13% economic contraction in 1998

- Currency lost 85% of its value, inflation reached 75%, poverty doubled from 11% to 19%

- IMF's contractionary policy prescriptions worsened the immediate crisis

- Crisis caused by combination of fixed exchange rate with open financial markets and poor regulation

- Led to lasting reforms: independent central bank, improved governance, and changed IMF crisis response approaches

Recent developments in economic policy

Indonesian economic policy has evolved gradually in recent years, with governments aiming to achieve macroeconomic stability, promote economic development, attract foreign capital, and increase social expenditure. At one point, Indonesia set a goal of being a top 10 and middle-income economy by 2025, but a combination of disappointing economic growth rates and the recession caused by the COVID-19 pandemic made that goal impossible.

Policy framework and development plan

The central element of Indonesia's current economic policy framework is the 20-year development plan known as RPJMN (Rencana Pembangunan Jangka Menengah Nasional). The plan, which began in 2005, is in its final phase. This last phase aims to focus on improving human capital and Indonesia's international competitiveness.

Monetary policy

The conduct of monetary policy is led by Indonesia's Central Bank, Bank Indonesia, which has been independent from the Government since 1999, and has had a medium-term inflation target of 4 to 6% since 2005. During the 2010s, the main central bank interest rate moved within a band between 4% and 8%. Monetary policy was loosened throughout 2016 and 2017, and after increasing rates in 2018, Bank Indonesia reduced interest rates to 3.5% in 2020. Rates rose sharply in late 2022, stabilising at 5.75% for the first half of 2023.

Fiscal policy

Fiscal policy has focused on maintaining the confidence of international investors and providing macroeconomic stability. During the 1990s, the Government achieved budget surpluses, using those surpluses to retire government debt. Spending was restrained while tax revenues increased (by around 15%). In the two decades to 2019, government debt fell from 87% to 30% of GDP. As a result of COVID-19 stimulus spending, government debt rose to 40% of GDP in 2020.

COVID-19 response

The Indonesian Government implemented a major fiscal policy response to COVID-19. The Government relaxed its self-imposed budget deficit ceiling of 3%. The Indonesian Government budgeted around US$50 billion - more than 4.5% of GDP - on its national economic recovery program (PEN).

COVID-19 National Economic Recovery Program (PEN)

The PEN was split into the following areas:

Healthcare spending (US$7 billion): Including purchase of medical equipment, funds for mass vaccination, and incentives for medical workers

Social protection (US$16 billion): Including food support programmes for up to 20 million families, extending the pre-employment card programme for around 5.6 million impacted workers, free electricity for around 30 million customers, supporting low-cost housing, and providing other support needs

Tax incentives and credit for business (US$8 billion): Including income tax exemptions, deferring import tax and debt payments, and reducing the corporate tax rate from 25% to 22%

Economic recovery programme (US$12 billion): Focused on providing credit restructuring and financing for small and medium businesses

This comprehensive response demonstrates Indonesia's capacity for large-scale fiscal intervention during crises.

Post-pandemic fiscal repair

As Indonesia emerged from the COVID-19 pandemic, its government began the task of fiscal repair, with fiscal policy becoming contractionary. Indonesia's budget deficit fell to an expected 2.8% of GDP in 2023, below the legally mandated ceiling of 3%. The fiscal repair task has been aided by windfall revenues from record commodity prices. However, overall spending still increased in 2022 due to subsidies for high fuel prices and the increasing interest burden from government debt.

Tax system challenges

A key constraint on the sustainability of Indonesia's fiscal policy is the narrowness of its tax base. Indonesia's ratio of tax revenues to GDP has been the lowest in the ASEAN-5 (Singapore, Malaysia, Philippines, Indonesia, and Thailand) and had been declining since 2013 up until the pandemic. This reflects factors relating to both the economy and the fact that Indonesia's tax revenues are heavily linked to the cyclical commodities sector.

There are many gaps in the tax collection system and a large number of exemptions in the tax system. Some improvements have been achieved under President Widodo reflecting tax reforms (particularly relating to tobacco) and increased compliance, as well as higher commodity prices. In 2022, the value-added tax rate (a tax on the delivery of goods and services) was increased, contributing to a 14% increase in tax revenues.

Measures to improve tax compliance include:

- A tax amnesty (which allows the declaration of previously untaxed assets)

- The simplification of compliance processes for taxpayers

- More effective use of banking data

However, over-reliance on commodity prices to drive revenue remains a critical problem. Indonesia collected more tax in 2022 than it had for some years, partly repairing the tax-to-GDP ratio.

Inequality and spending quality

One of the weaknesses of current policy settings is that the tax and transfer payment system makes no overall difference to the level of inequality. Fiscal policy's failure to promote inclusive growth reflects low-quality spending in infrastructure, education, and health, particularly evident in East Indonesia.

Regional Inequality: Internet Access

For example, 60 to 70% of people in East Indonesia lack adequate internet access. The Indonesian Government has identified the need to substantially increase spending across these areas.

This demonstrates the stark regional disparities in infrastructure and services.

Infrastructure investment

The Indonesian Government has also recognised the need to increase its investment in infrastructure. Between 2014 and 2018, infrastructure spending grew 22% a year on average. The Government has an ambitious plan to spend around US$430 billion on infrastructure in the five years to 2024.

In 2019, the government announced a US$32 billion project to move its capital city from Jakarta to Borneo, officially changing over in 2024. The government hopes 60,000 people will move between the two cities by 2025, and that this will encourage foreign investment into a less-developed region of the country.

However, Indonesia still has a large infrastructure deficit. Private investment will need to play a role too, but it has been hampered by regulatory issues, inadequate planning, and issues in securing finance. The Government has established a Public Private Partnership Unit within the Ministry of Finance to facilitate faster project approval and delivery, and has made steps to reduce regulatory burdens.

International assistance can also help address infrastructure needs, such as through a recent US$210 million project funded by the World Bank to improve protection of Indonesia's marine areas and coral fisheries.

Education spending

Indonesia's expenditure on education and health care is inadequate for population needs. Education spending is 3.5% of GDP, despite a commitment that 20% of government expenditure should be spent on education. Inadequate investment in education contributes to Indonesia's high rate of youth unemployment, which is usually around four times higher than for other age groups.

Educational outcomes are also relatively low, with around 55% of Indonesians completing education functionally illiterate.

The Government has expanded its Program Indonesia Pintar (PIP) policy, which provides a cash subsidy for school-age children in poor households, with a budget for 17.9 million students in 2023. Further, the "Merdeka Belajar" consists of 22 programmes in place since 2019 to improve Indonesia's human capital, including a revision of the national exam to better align with international standards.

Healthcare spending

Public spending on healthcare is below 1.5% of GDP, lower than in most South-East Asian economies, such as the Philippines or Cambodia. Improved health outcomes have been achieved since the introduction of a universal health insurance programme in 2014, the Jaminan Kesehatan Nasional (JKN).

The universal healthcare programme has nearly reached 90% coverage, assisted by a programme in 2022 that provided 97 million low-income households extra assistance in accessing the programme. The cost of JKN for individuals depends on their ability to contribute, with the poorest households having no requirement to contribute.

Around 240 million Indonesians participate in the scheme, although in 2021 only 60% were in the lowest income categories. The government has made steps to improve the scheme, including the introduction of the "Standard Inpatient Class" system in 2022. This reformed the existing tiered framework, which offered hospital wards of varying quality based on the premiums individuals paid.

However, while this addresses inequalities for in-patients, attention has been drawn to JKN's inability to address high out-of-pocket expenses, which make up a third of total health expenditures (above the WHO recommendation of 20%).

Structural reform: the Job Creation Act

The most audacious attempt at structural reform in Indonesia in recent years has been the Job Creation Act of 2020, also known as the "Omnibus Law" because of its wide-reaching impacts on many aspects of the economy. The legislation amended 77 other laws relating to environmental protection, spatial planning, special economic zones, small and medium enterprises, land rights, transport, energy, agriculture, fisheries, and taxation, with the aim of encouraging business investment and economic growth.

Labour market changes mostly reduced protections for employees. Foreign investment restrictions were reduced for hundreds of industries, including information and communications technology (ICT), energy, and tourism.

However, the Omnibus Law was highly contentious, prompting criticism from environmental and labour groups and even street protests. In 2021, the Constitutional Court declared the law unconstitutional. In 2023, an amended law removed three key restrictions on foreign investment and established the Indonesian Investment Authority with US$5 billion to create long-term investment opportunities in the country.

Challenges to reform

A consistent hurdle for reforming the Indonesian economy is resistance from established interest groups whose economic interests have been threatened by the removal of regulations that advantaged them. Historically, Indonesia has been associated with "crony capitalism", where economic policies were set up for the benefit of corrupt officials and relatives of senior officials and political leaders.

Indonesia was ranked 110th in the world in 2022 on the Corruption Perception Index. In 2023, a US$20 billion tax scandal forced President Widodo to pledge further efforts to fight corruption.

One part of his strategy over the past decade has been to shift towards a more decentralised state, with large areas of public expenditure and services being transferred from the central government to the nation's 440 local governments. However, significant reforms are still required for the legal system to improve corporate practices, with the World Bank ranking Indonesia 73 out of 190 countries for ease of doing business in 2019.

Future development targets

The potential dividend from economic reform and policy intervention is significant. According to the Ministry of National Development Planning (Bappenas), by 2030, policy interventions could:

- Lift fourth grade reading proficiency to 68%

- Reduce women in child marriages from 10% to 7%

- Increase annual real GDP per capita growth to 5.4%

- Lower the Gini index from 37 to 36

However, achieving these economic and social gains will require major investment, almost US$700 billion in annual spending on Sustainable Development Goals by 2030.

Economic Policy Key Points:

- Monetary policy targets 4-6% inflation through independent central bank

- Government debt fell from 87% to 30% of GDP (1999-2019) but rose to 40% with COVID-19 spending

- Tax-to-GDP ratio is lowest in ASEAN-5, constraining fiscal sustainability

- Major spending needs: infrastructure (US$430 billion planned), education (currently 3.5% of GDP), healthcare (below 1.5% of GDP)

- Corruption (ranked 110th globally) and crony capitalism remain significant reform challenges

Is Indonesia a globalisation success story?

Indonesia provides a complex picture of globalisation. Since the 1980s, Indonesia has liberalised trade, investment, and financial flows. Global and regional integration have delivered Indonesia substantial benefits and have allowed for progress towards reducing poverty. The severity of the Asian financial crisis in the late 1990s resulted in lasting reforms and improved governance.

While growth has been strong, Indonesia has fallen short of its ambitious growth target, and reforms have been hindered by difficulties in managing the economy, with its huge population, diverse range of cultures, and a population scattered across 6,000 inhabited islands.

Indonesia's experience highlights that globalisation is not an economic "silver bullet". To sustain growth over the long term, countries need to establish strong governance systems, build competitive industries, reform their economies, and undertake major investment in education, health, and infrastructure to achieve economic development.

Short-term challenges

Despite sustaining growth rates above 5% in recent decades, Indonesia is faced with numerous challenges. In the short term, it must sustain economic growth that has been fuelled by higher commodity prices and a recovery in tourism, which could be jeopardised by inflationary pressures, higher interest rates, or weaker international conditions. Securing foreign investment will be critical to strengthening the economy and sustaining strong growth through the 2020s. While the government cannot ensure currency stability, it can contribute to investor confidence.

Long-term challenges

In the long term, key economic challenges will include:

- Strengthening the financial sector

- Reorienting government spending towards more efficient spending on education and infrastructure

- Improving coordination between national and local governments

- Attracting more foreign investment that can diversify the Indonesian economic base

Development goals

Stronger economic growth is needed to reduce the incidence of poverty and improve quality of life. Indonesia hopes to mark its 100-year anniversary of independence in 2045 by achieving high-income status and reducing poverty to zero. This is an ambitious goal, and will require the Government to continue to provide a strong policy framework and support the development of human capital. With Joko Widodo completing his maximum two terms in office in 2024, the new president will play a central role in determining Indonesia's progress towards its economic ambitions.

Final Assessment:

- Globalisation has delivered substantial benefits but also exposed Indonesia to major economic disruptions (Asian financial crisis, COVID-19)

- Growth has been strong (5%+ average) but Indonesia remains 16th-largest economy while only 25th in exports

- Success requires: strong governance, competitive industries, major investment in education/health/infrastructure

- Short-term challenge: sustaining growth amid global economic uncertainty

- Long-term challenge: diversifying economic base, improving spending efficiency, strengthening financial sector

- Ambitious goal: high-income status and zero poverty by 2045 (100th anniversary of independence)

Remember!

Key Points to Remember:

-

Indonesia is the world's 16th-largest economy with 277 million people, but living standards remain relatively low at US$4,788 per capita (2022)

-

The Asian financial crisis of 1997-98 devastated Indonesia's economy with a 13% contraction, but led to lasting reforms including an independent central bank and improved governance

-

Indonesia has successfully transformed its economic structure, with services growing from 34% (1980) to 43% (2021) of GDP, while agriculture fell from 24% to 13%

-

Trade liberalisation since the mid-1980s has reduced average tariffs from 17% to 6%, and Indonesia participates in major trade agreements including ASEAN, RCEP, and bilateral deals with Australia and Japan

-

Environmental challenges are significant, with Indonesia ranking as the world's eighth-largest carbon emitter, experiencing one of the highest deforestation rates, and being highly vulnerable to climate change impacts

-

Despite progress on development goals including poverty reduction (from 69% in 1998 to 2.5% in 2022) and improved life expectancy (up six years since 1990), Indonesia still faces challenges with education quality, healthcare access, and infrastructure deficits

-

Future success depends on continued policy reform, increased investment in human capital and infrastructure, improved tax collection, reduced corruption, and attracting sustainable foreign direct investment to diversify the economic base