Economic Resources (AQA A-Level Economics): Revision Notes

Economic resources

Understanding economic resources

For most people, increasing the consumption of material goods represents an important way to improve personal welfare and quality of life. However, before we can consume goods, they must first be produced. This fundamental requirement highlights the importance of economic resources in the economy.

Economic resources are the inputs needed to produce goods and services. These resources are scarce in relation to the demand for them, which creates the need for careful rationing and economising in how they are used. Scarcity means that societies must make choices about how to allocate these limited resources among competing uses.

Understanding Scarcity

The concept of scarcity is fundamental to economics. It doesn't mean that resources are in short supply in an absolute sense, but rather that they are limited relative to human wants and needs. This creates the economic problem of choice – how to allocate limited resources among unlimited wants.

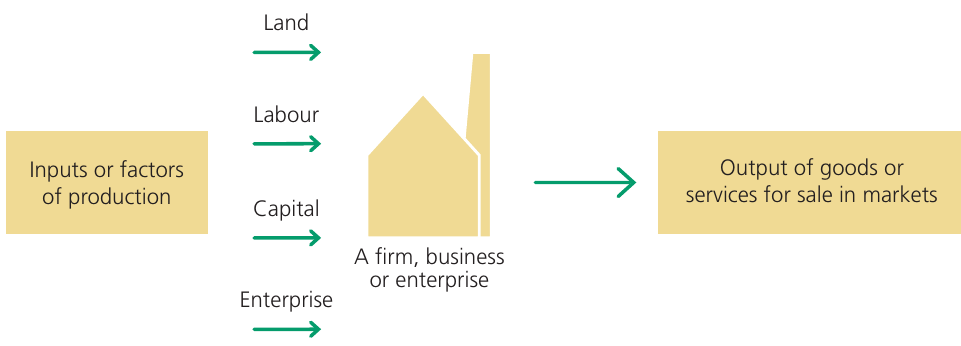

What is production?

Production is a process, or series of processes, that transforms inputs into outputs. This conversion is the foundation of all economic activity.

The outputs from production become the consumer goods and services that make up our standard of living. However, inputs are also used to create capital goods – items that are themselves used in the production of other goods and services. Capital goods are sometimes called producer goods because they help to produce other items rather than being consumed directly by households.

Consumer goods, by contrast, are items consumed by individuals or households to satisfy their needs or wants. These are the final products that people use in their daily lives.

Capital Goods vs Consumer Goods

The distinction between capital goods and consumer goods is important:

- Capital goods (e.g., factory machinery, delivery trucks) are used to produce other goods and services

- Consumer goods (e.g., food, clothing, smartphones) are purchased for direct consumption by households

Some items can be either, depending on their use. For example, a car is a consumer good when purchased by a household, but a capital good when purchased by a business for deliveries.

The diagram above illustrates the basic nature of production, showing how the four factors of production flow into a firm or business, which then produces outputs for sale in markets.

The factors of production

The Four Factors of Production

Economists identify the inputs used in the production process as the factors of production. There are typically four factors recognised:

- Land – all natural resources

- Labour – human effort, physical and mental

- Capital – manufactured goods used in production

- Enterprise – entrepreneurial coordination and decision-making

Each of these factors plays a distinct role in the production process, and all are necessary for production to occur.

Land

Land encompasses all natural resources used in production. This includes:

- The physical land itself

- Natural resources extracted from the earth

- Environmental resources

Labour

Labour refers to the human effort, both physical and mental, used in the production process. This includes workers at all skill levels contributing to the creation of goods and services.

Capital

Capital means the manufactured goods used to produce other goods and services. This includes:

- Machinery and equipment

- Factory buildings

- Tools and technology

- Infrastructure such as roads and railways

What Capital Means in Economics

It's important to note that capital in economics refers to physical capital goods, not money or financial capital. When economists talk about capital as a factor of production, they mean tangible items like machinery and buildings, not financial assets or cash.

Enterprise

Enterprise, often called the entrepreneurial input, is the factor that coordinates and organises the other three factors. The entrepreneur is the person who makes key business decisions.

Exam tip: Remember that factors of production are inputs used to produce output of goods and services. Enterprise is the factor which coordinates factor inputs of capital, land and labour in pursuit of profit.

The role of entrepreneurs

Entrepreneurs differ fundamentally from the other factors of production. They are the people who address the central economic questions:

- What to produce?

- How to produce it?

- For whom to produce it?

An entrepreneur decides how much of each factor of production to employ, including labour. The costs of employing land, labour and capital, together with the cost of the entrepreneur's own services, become the firm's costs of production.

Essentially, the entrepreneur is a financial risk-taker and decision-maker. Their reward for successful decision-making is profit. Entrepreneurial profit is what remains after deducting the costs of employing all factors of production from the sales revenue gained from selling the goods and services produced.

Worked Example: Calculating Entrepreneurial Profit

Consider a small bakery business:

- Sales revenue from selling bread and cakes: $10,000 per month

- Costs of production:

- Land (rent): $2,000

- Labour (wages): $4,000

- Capital (equipment depreciation, utilities): $1,500

- Raw materials: $1,000

- Total costs: $8,500

Entrepreneurial profit = Sales revenue - Total costs

Entrepreneurial profit = $10,000 - $8,500 = $1,500

This $1,500 is the reward for the entrepreneur's decision-making, risk-taking, and coordination of the other factors of production.

The environment as a scarce resource

Environmental resources form part of the land factor of production and comprise all the natural resources that are used or can be used in the economic system. These include:

- Physical resources – such as soil, water, forests, fisheries and minerals

- Gases – such as hydrogen and oxygen

- Abstract resources – such as solar energy, wind energy, the beauty of the landscape, clean air and water

Renewable and non-renewable resources

Environmental resources can be categorised into renewable and non-renewable resources, with the latter further divided into recyclable and non-recyclable.

Renewable resources are reproducible and perpetually maintainable. Examples include forests, animals and water. However, the availability of these resources depends critically on careful management by humans. Without proper stewardship, even renewable resources can be depleted.

The Importance of Resource Management

Even though renewable resources can regenerate naturally, they still require careful management. Overfishing can deplete fish stocks, deforestation can destroy forests faster than they can regrow, and water sources can become polluted beyond their natural capacity to self-clean. Sustainability requires balancing resource use with regeneration rates.

Non-renewable resources, such as oil, gas and minerals, cannot be regenerated, or their regeneration takes so long that the stock of resources cannot meaningfully be increased. These are finite resources in the sense that once used, their stock diminishes.

Recyclable non-renewable resources, such as minerals, paper and glass, can be reused in the economic system. In theory, all such resources could be recycled, but in practice it is not always possible or economically viable to recycle more than a small fraction.

Non-recyclable resources, such as coal, gas and oil, are finite in the sense that once used, their stock is no longer available for future use. These are sometimes called finite resources.

The 'free gifts of nature' debate

Some environmental resources, such as the air we breathe and the water we drink, are often described as the 'free gifts of nature'. However, this view can be challenged.

Challenging the 'Free Gifts' Assumption

In most countries and regions where large numbers of people live, clean air and drinkable water have become scarce commodities rather than free gifts. The need to address pollution created by humankind means that clean air and water are actually scarce resources. Resources that could be used for other purposes must instead be dedicated to producing clean air and water.

This represents a real opportunity cost to society – the alternative uses of resources that are forgone when we must dedicate them to environmental protection and restoration.

Production and consumption activities taking place in the economy frequently affect and often damage the natural environment. This creates opportunity costs, as resources must be diverted to environmental protection and restoration.

Key Points to Remember:

- Production converts inputs into outputs – understanding this basic process is fundamental to economics

- The four factors of production are land, labour, capital and enterprise – each plays a distinct role in the production process

- Entrepreneurs coordinate the other factors and bear financial risk in pursuit of profit

- Environmental resources can be renewable or non-renewable – renewable resources can be maintained with careful management, while non-renewable resources are finite

- Clean air and water are scarce resources, not free gifts – they require resources to produce and protect in modern economies