Production (AQA A-Level Economics): Revision Notes

Production

Introduction to production theory

Production theory forms the foundation of microeconomic analysis of firms. It examines how businesses transform various inputs into outputs that can be sold to consumers. Understanding production is essential because it connects directly to how firms calculate their costs and ultimately determine their profit levels.

Production theory serves as the starting point for understanding firm behaviour. Without grasping how firms transform inputs into outputs, we cannot fully analyse their cost structures, revenue patterns, or competitive strategies.

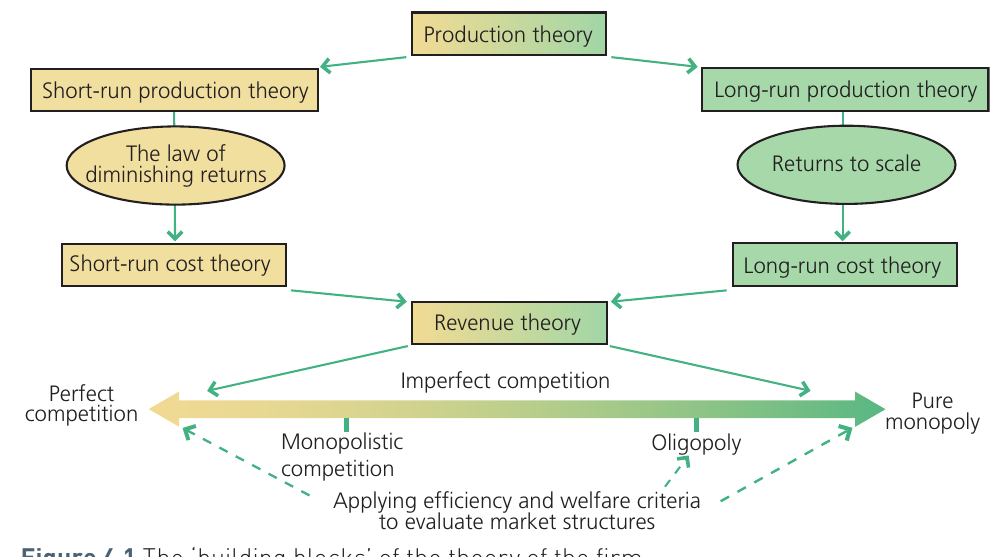

The theory of the firm builds systematically from production concepts. Production theory helps us understand the short-run and long-run behaviour of businesses, which then leads to analysis of cost structures, revenue patterns, and ultimately how firms compete in different market structures.

This framework shows how production theory serves as the starting point for analysing firm behaviour. In the short run, production theory leads to understanding the law of diminishing returns, which then explains short-run cost patterns. In the long run, production theory connects to the concept of returns to scale, which determines long-run cost structures. Both pathways ultimately help us understand how firms generate revenue and profit across different types of markets.

What is production?

Production refers to the process of converting inputs (also called factor services) into outputs of goods and services. It is not simply about manufacturing physical products; production also includes the creation of services such as healthcare, education, or financial advice.

The production process involves taking various resources and combining them in ways that create value. For example, a bakery takes flour, water, yeast, and labour to produce bread. A hospital combines medical equipment, skilled doctors and nurses, and facilities to produce healthcare services. In both cases, inputs are being transformed into outputs that people want to consume.

Common Confusion Alert:

It is crucial to distinguish between production and productivity:

- Production = the actual process or quantity of output created

- Productivity = efficiency measure (output per unit of input)

Students frequently confuse these terms, but they measure fundamentally different aspects of the production process.

Factors of production

Economists identify the inputs used in production as the factors of production. Traditionally, four main factors are recognised: land, labour, capital, and enterprise.

Land

Land encompasses all natural resources that firms use in production. This includes not just the physical ground that a business owns or rents, but also natural resources such as minerals, oil, forests, water, and even the air. Essentially, land represents the part of Earth's resources that a firm can access or use in its production activities.

Labour

Labour refers to all human effort employed in the production process. This includes everyone from shop floor workers to senior managers, provided they receive wages or salaries for their work. Labour is measured not just by the number of workers, but also by their skills, experience, and the hours they contribute to production.

The quality of labour can vary significantly. A highly skilled engineer contributes differently to production than an unskilled worker, even if both work the same number of hours. This is why labour productivity – the output per worker – becomes such an important measure of economic efficiency.

Capital

Capital in economics means the physical capital goods (also called capital equipment) that firms own or hire. This includes machinery, factories, computers, vehicles, and tools used in production. It also encompasses intellectual capital such as patents and software that the firm owns or licenses.

Do Not Confuse These Terms:

Capital in production theory refers to physical productive assets (machinery, equipment, buildings).

Financial capital refers to money.

When a firm invests in new machinery, economists call this capital widening – adding more capital. When a firm invests in newer, more advanced technology, this is termed capital deepening – improving the quality of capital.

Enterprise

The entrepreneurial function represents the fourth factor of production. Entrepreneurs are the individuals who make fundamental business decisions: what to produce, how to produce it, and for whom to produce it. They determine how much of the other factors of production (land, labour, capital) to employ.

Entrepreneurs play a unique role because they are both decision-makers and financial risk-takers. Unlike workers who receive guaranteed wages, entrepreneurs bear the risk that their business might fail. If the business succeeds, the entrepreneur's financial reward is profit – what remains after all costs of employing the other factors have been deducted from sales revenue. If the business fails, the entrepreneur may lose their investment.

Real-World Entrepreneurs:

Notable entrepreneurs include Rihanna, who has built successful business ventures in cosmetics and fashion, and Sir Richard Branson, who has created numerous companies under the Virgin brand. These individuals exemplify the entrepreneurial function of:

- Identifying opportunities

- Taking financial risks

- Coordinating resources to create value

- Making strategic business decisions

Understanding productivity

What is productivity?

Productivity measures the efficiency of production by calculating output per unit of input. It answers the question: "How much are we producing with the resources we use?" Higher productivity means generating more output from the same amount of inputs, or producing the same output with fewer inputs.

Productivity is one of the most important concepts in economics because it directly affects:

- Living standards

- International competitiveness

- Economic growth

When a country's productivity increases, it can produce more goods and services without using more resources, enabling higher incomes and better quality of life.

Labour productivity

Labour productivity specifically measures output per worker, typically calculated per period of time such as per hour or per week. It can be expressed as:

or

Labour productivity is particularly significant in manufacturing industries.

Worked Example: UK Automotive Productivity Gap

Consider the automotive sector productivity comparison from the 1990s and early 2000s:

Rover Car Group (UK):

- Labour productivity: approximately 33 cars per worker per year

Nissan Sunderland (UK):

- Labour productivity: 98 cars per worker per year

Analysis: Nissan achieved nearly 3 times higher labour productivity than Rover. This dramatic difference meant that Rover could not compete on cost, ultimately leading to the company's collapse in 2005.

The productivity gap resulted from differences in:

- Modern equipment investment

- Production methods

- Worker training

- Factory organization

The image above shows the production line at the BMW factory in Oxford, which produces Mini vehicles. BMW achieved high labour productivity by investing in modern equipment, efficient production methods, and well-trained workers. This high productivity allowed BMW to successfully manufacture Minis in the UK despite relatively high UK wage levels.

Other types of productivity

While labour productivity is most commonly discussed, economists also measure other forms of productivity:

Capital productivity measures output per unit of capital employed. This indicates how efficiently a firm uses its machinery and equipment.

Entrepreneurial productivity and land productivity can also be measured, though these are less commonly used in practice.

All these productivity measures share the same basic principle: they assess how efficiently different factors of production are being used to generate output.

The productivity gap

The productivity gap refers to the difference in productivity levels between countries. For the UK, this typically means comparing UK productivity with that of other developed economies such as Germany, France, and the United States.

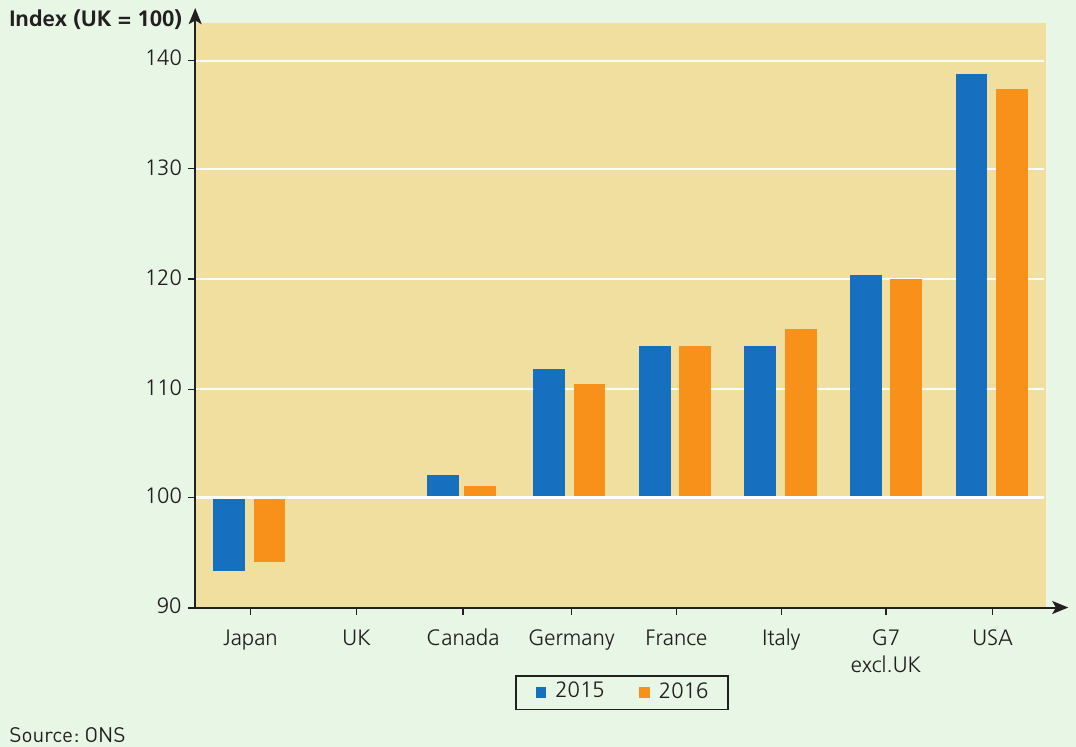

Interpreting the Productivity Gap:

This chart presents GDP per hour worked across G7 countries for 2015 and 2016, using index numbers where UK productivity equals 100. The data reveals that:

- USA productivity was approximately 38% higher than the UK's

- France, Italy, and Germany all exceeded UK productivity levels

- Germany achieved about 11% higher productivity than the UK

- Only Japan had lower productivity than the UK during this period

The productivity gap matters because it affects international competitiveness. If UK workers produce less per hour than workers in competing countries, UK firms may struggle to compete unless UK wages are correspondingly lower – which would mean lower living standards for UK workers.

The importance of productivity

Labour productivity has become a critical concern for the UK economy in recent years. Following the 2009 recession, UK productivity has failed to recover to its previous growth trajectory. This phenomenon, dubbed the "productivity puzzle", has significant implications for economic performance and living standards.

By 2014, UK labour productivity remained about one-fifth lower per hour worked than that of other leading nations. This stagnation occurred despite relatively strong employment growth, creating a puzzling situation where more people were working but producing less per person than before the recession.

The UK's productivity puzzle

Several factors may explain the UK's productivity puzzle:

Labour hoarding occurred when employers kept workers on their payroll during the recession, even though output fell sharply. Surveys in 2012 found that close to one-third of businesses employed more staff than needed to fulfil current orders. Employers preferred to retain workers rather than make them redundant, believing they would struggle to recruit skilled workers when demand recovered. This practice meant that output per worker inevitably fell.

Flexible labour markets in the UK allowed employers to offer part-time and temporary "zero-hours" contracts, where employers do not guarantee minimum working hours. By 2014, approximately 5.5 million people worked under such arrangements. This flexibility allowed firms to maintain employment at low cost, but it also reduced incentives to invest in productivity improvements.

Zombie firms emerged as another explanation. These under-performing companies generated just enough revenue to service their debts but lacked resources to invest in productivity improvements. Very low interest rates after the recession allowed zombie firms to survive when, under normal conditions, they would have failed. Banks and creditors, weakened by the 2008 financial crisis, were reluctant to force poorly performing companies into bankruptcy. The Bank of England estimated that zombie firms represented a significant drag on productivity, though this view remained controversial among economists.

Low investment in capital goods, infrastructure, and research and development may have constrained productivity growth. Investment levels in the UK economy in 2014 remained much lower than before 2008. Without new, more efficient equipment and improved infrastructure, productivity naturally stagnates.

Consequences of Continued Low Productivity:

The consequences of continued low productivity could be severe:

Negative scenario: Reducing labour costs per hour through wage cuts might become necessary to maintain competitiveness – leading to a "race to the bottom" in living standards.

Positive scenario: Boosting productivity through increased investment in equipment, infrastructure, and research would offer a more positive solution, though this requires sustained commitment and time to yield results.

What is a firm?

A firm is a productive business organisation that sells its output of goods or services commercially. Unlike non-business productive organisations such as charities, hospitals, or schools, firms operate primarily to generate revenue that covers their production costs and, ideally, produces profit.

Firms exist to transform inputs into outputs efficiently. They organise factors of production, make decisions about what and how to produce, and bear the financial risks associated with production. The revenue a firm earns from selling its output must cover the costs of employing land, labour, capital, and the entrepreneurial function.

Real-world application: Japanese manufacturing methods

Manufacturing methods have evolved significantly over recent decades, with important implications for labour productivity. Traditional car factories were chaotic, noisy places characterised by smooth-flowing production lines but with substantial waste and inefficiency.

The Toyota Production System (TPS), developed in the 1950s, revolutionised manufacturing. Central to TPS is "lean manufacturing" – an approach now adopted by virtually all mass car producers worldwide.

Case Study: Lean Manufacturing and Just-in-Time Production

Lean manufacturing aims to combine the best aspects of craft production and mass production while minimising waste. It uses less of every input:

- Less labour

- Less machinery

- Less factory space

- Less time in product design

Rather than tolerating defects up to a certain level, lean production seeks to eliminate all defects. Sometimes called "just-in-time" (JIT) production, this approach manufactures components exactly when needed rather than holding large buffer stocks.

Traditional vs. Lean Production:

Traditional factories: The entire assembly line would stop when a fault occurred, wasting considerable time.

Lean factories: Production happens "just in time" – if a defect is identified, the specific station stops immediately for correction, but the rest of the line continues. This allows mechanically perfect products to be manufactured continuously.

Impact: By eliminating waste, reducing defects, and optimising every stage of manufacturing, Japanese methods have significantly increased output per worker. The old approach of making large batches and storing materials between production stages required much higher labour input per unit produced.

Specialisation and division of labour

The benefits of specialisation and division of labour

Nearly 250 years ago, economist Adam Smith explained a fundamental principle of economics through his famous example of a pin factory. Smith observed that output could increase dramatically when workers specialised in different tasks rather than each worker attempting to complete all tasks individually.

Specialisation occurs when a worker focuses on performing one task or a narrow range of tasks. At a broader level, it also refers to different firms focusing on producing particular goods or services. Division of labour describes the arrangement where different workers perform different tasks in the course of producing a good or service.

Adam Smith's Three Reasons for Increased Output:

Adam Smith identified three main reasons why specialisation increases total output in a factory:

1. Time savings occur because workers do not need to switch between different tasks. Changing from one task to another wastes time as workers put down one set of tools, move to a different location, and pick up different equipment. When each worker focuses on one task, this time waste is eliminated.

2. Better capital equipment can be employed when workers specialise. If workers perform many different tasks, each needs access to various tools and machinery. When workers specialise, firms can invest in more sophisticated, task-specific equipment. This is called capital widening when more capital is employed, or capital deepening when firms invest in more advanced technology.

3. Skills develop through repetition when workers repeatedly perform the same task. They become faster, more accurate, and develop expertise. This learning-by-doing increases productivity over time.

These principles remain fundamental to modern production. From assembly lines to professional services, specialisation and division of labour underpin productivity improvements across the economy.

Remember!

Key Points to Remember:

-

Production transforms inputs into outputs – it is the fundamental process by which firms create goods and services using factors of production.

-

Four factors of production are land, labour, capital, and enterprise – each plays a distinct role, with entrepreneurs uniquely bearing risk and making key decisions.

-

Productivity measures efficiency, not quantity – specifically, it measures output per unit of input, with labour productivity (output per worker) being the most commonly used measure.

-

The UK faces a productivity gap compared to major competitors like the USA, Germany, and France, which has significant implications for competitiveness and living standards.

-

Specialisation and division of labour increase productivity through time savings, better use of capital equipment, and skill development – principles established by Adam Smith that remain relevant today.