Costs, Revenues, Profits, and Objectives (Edexcel A-Level Economics A): Revision Notes

Revenues, Profits, and Objectives

Understanding revenue

Revenue is the money that a firm receives from selling its goods or services. There are three main ways to measure revenue, each providing different insights into a firm's financial performance.

Types of revenue

Total revenue (TR) represents the complete amount of money a firm receives from all its sales. This is calculated by multiplying the price of the product by the number of units sold.

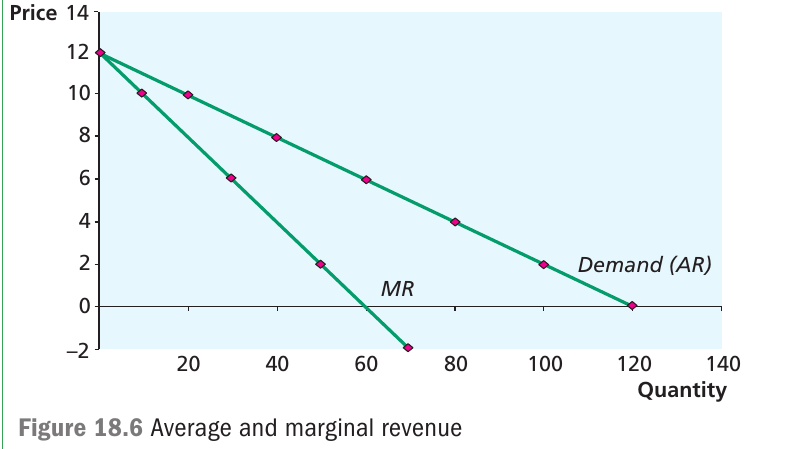

Average revenue (AR) shows the typical amount received per unit sold. When there are no indirect taxes, this equals the price that customers pay. The demand curve actually represents the average revenue because it shows the price at different quantities.

Marginal revenue (MR) measures the extra money a firm gains when it sells one more unit of output. This helps firms understand how their revenue changes as they adjust their production levels.

Understanding the distinction between these three revenue measures is essential for analyzing firm behavior. Each provides a different perspective on financial performance: TR shows overall earnings, AR indicates per-unit earnings, and MR reveals how revenue changes with each additional unit sold.

Revenue formulas

The mathematical relationships between these concepts are straightforward:

These formulas work similarly to the relationships between total, average, and marginal costs that you studied earlier.

Worked Example: Calculating Revenue Measures

Suppose a firm sells 50 units at £10 each:

Step 1: Calculate Total Revenue

Step 2: Calculate Average Revenue

Notice that average revenue equals the price when there are no indirect taxes.

Step 3: Calculate Marginal Revenue

If selling one more unit (51 units) at £9.90 gives TR = £504.90, then:

The relationship between sales and revenue

Understanding how quantity sold affects revenue is crucial for business decision-making. When a firm faces a downward-sloping demand curve, increasing sales requires lowering prices, which creates an interesting relationship between average and marginal revenue.

Key Principle: The marginal revenue curve always falls more steeply than the average revenue (demand) curve. Both curves share the same starting point on the vertical axis, but MR declines at twice the rate of AR. This relationship always holds true regardless of the shape of the demand curve.

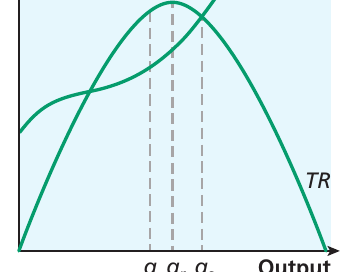

When the MR line crosses the horizontal axis (where ), this marks the point where total revenue reaches its maximum. Beyond this point, marginal revenue becomes negative, meaning that selling additional units actually reduces total revenue.

Why does MR fall faster than AR?

To sell more units, a firm with market power must lower its price. However, this lower price applies not just to the extra units sold but potentially to all units.

Worked Example: Understanding Why MR Falls Faster

Suppose you currently sell 20 units at £10 each:

- Current TR = £10 × 20 = £200

To sell 40 units, you drop the price to £8:

- New TR = £8 × 40 = £320

- Change in TR = £320 - £200 = £120

- Change in quantity = 40 - 20 = 20 units

Calculating the effect:

- Revenue from 20 extra units at £8 = £160

- BUT you lose £2 on each of the original 20 units = -£40

- Net change in revenue = £160 - £40 = £120

This £120 gain from selling 20 more units means MR = £120 ÷ 20 = £6 per unit, which is less than the new AR of £8. This explains why marginal revenue falls more rapidly than average revenue.

Business objectives

Firms organise production by bringing together factors of production to create output. But this raises an important question: what motivates them to produce particular quantities of output at specific prices? Economic analysis examines several possible objectives that firms might pursue.

Profit maximisation

Traditional economic theory assumes that firms aim to maximise profits. But what exactly counts as "profit" in this context?

Normal profit is the minimum profit level needed to keep a firm operating in its market. It represents the opportunity cost of the firm's resources – essentially, what the owners could earn by using their capital elsewhere. Economists consider normal profit as part of the firm's total costs because it's necessary to keep the business running.

Supernormal profit (also called abnormal profit or economic profit) is any profit earned above the normal profit level. These higher profits indicate that a firm is performing better than the minimum required to stay in business.

The distinction between normal and supernormal profit is crucial for understanding firm behavior in different market structures. Normal profit represents the minimum return needed to keep resources in their current use, while supernormal profit signals exceptional performance that may attract new competitors to the market.

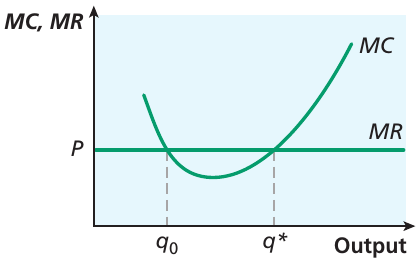

The MR = MC rule for profit maximisation

Firms maximise profit by producing at the output level where marginal revenue equals marginal cost (). This is one of the most important principles in economics.

The logic behind this rule is straightforward. If marginal revenue exceeds marginal cost, the firm gains more from selling an extra unit than it costs to produce it, so profit increases by expanding output. Conversely, if marginal cost exceeds marginal revenue, producing an additional unit costs more than it brings in, so the firm would increase profits by reducing output. Only when has the firm found the optimal output level that maximises profit.

Exam Tip: The rule applies in all market situations where firms seek to maximise profits. Make sure you understand it thoroughly – note that MC is the gradient of the total cost curve, and MR is the gradient of the total revenue curve. The profit-maximising output occurs where these gradients are equal.

Critical condition: Profits are maximised where AND where MC cuts MR from below. At a point where MC equals MR by cutting from above, the firm would actually be maximising losses rather than profits.

Profit maximisation with different demand curves

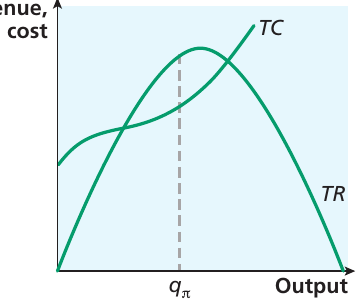

When a firm faces a downward-sloping demand curve (as most firms do), the analysis becomes slightly more complex.

Total revenue now follows a curved path rather than a straight line. It rises initially as quantity increases, reaches a peak, and then falls. Profit is maximised at the output level where the vertical distance between the total revenue and total cost curves is greatest.

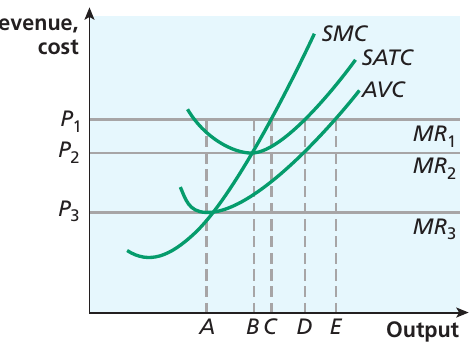

The shut-down point in the short run

Sometimes a firm may continue operating even when it's not covering all its costs. In the short run, a firm that isn't covering its opportunity costs might still remain in the market, provided it covers its variable costs.

The shut-down point is the price level below which a firm will stop production in the short run. This occurs where price falls below average variable cost. At this point, the firm's revenues no longer cover even its variable costs.

Why Continue Operating Below Normal Profit?

Consider the costs. A firm has already incurred fixed costs in the short run – these cannot be avoided. If the firm can at least cover its variable costs and contribute something towards fixed costs, it's better off continuing production than shutting down completely and losing all its fixed costs.

The mathematical condition is:

Only when price falls below AVC (at point in the diagram) should the firm cease production immediately.

In the long run, however, the firm must make at least normal profit to survive. If long-run average costs exceed average revenues, the firm will eventually exit the market.

Alternative business objectives

Not all firms aim purely to maximise profits. Research has shown that managers may pursue other objectives, leading to different output and pricing decisions.

Revenue maximisation

Economist William Baumol argued that managers might focus on maximising revenue rather than profit. This creates different outcomes compared to profit maximisation.

A revenue-maximising firm produces more output than a profit-maximising one. To sell this extra output, it charges a lower price. The revenue maximisation point occurs where , which is at the peak of the total revenue curve.

Why Might Managers Prefer Revenue Maximisation?

Baumol suggested that shareholders might not be entirely satisfied with this approach. However, if managers (the agents) have sufficient power over shareholders (the principals), they might successfully pursue revenue maximisation. The outcome might be a compromise, with output set somewhere between the profit-maximising and revenue-maximising levels.

Possible reasons include:

- Managers' salaries and status may be linked to company size (revenue)

- Market share concerns may drive focus on revenue

- Growth targets may prioritize sales over profits

Sales maximisation

In some situations, managers prioritise sales volume over revenue or profit. This could lead to even higher output levels than revenue maximisation.

A sales-maximising firm pushes output to the point where total revenue just covers total cost, including normal profit. At this point, average cost equals average revenue. The firm breaks even but has maximised the volume of sales.

The extent to which managers can pursue sales maximisation depends on their accountability to shareholders. Managers typically have better information about market conditions and internal operations than shareholders do, which may allow them some discretion to pursue their own objectives.

Practice Question: What is the difference between 'sales maximisation' and 'revenue maximisation'?

Answer:

- Revenue maximisation occurs where (at the peak of the TR curve), maximizing total monetary income

- Sales maximisation occurs where (including normal profit), maximizing the number of units sold while just breaking even

Sales maximisation produces higher output and lower prices than revenue maximisation.

Long-run profit maximisation

Sometimes firms take a strategic long-term view rather than maximising short-run profits. Several scenarios might justify this approach:

- Investment for future growth: A firm might undertake costly investment now to achieve higher profits in the long term

- Building customer loyalty: Firms may delay price increases following cost rises to maintain customer satisfaction

- Strategic positioning: Actions that reduce short-run profits might strengthen the firm's competitive position over time

These strategies suggest that what appears to be departing from profit maximisation in the short run might actually be profit maximisation when viewed from a longer-term perspective. This reconciles apparently contradictory behavior with traditional economic theory.

Behavioural theories of the firm

Businesses don't always pursue traditional objectives like profit or revenue maximisation. This might happen consciously through deliberate management decisions, or as a result of principal-agent problems where managers' motivations differ from owners' interests.

Satisficing behaviour

Satisficing describes behaviour where managers aim to produce satisfactory results rather than maximum profits. Herbert Simon introduced this concept, suggesting that managers might prefer a comfortable working environment over the stress of pushing for absolute maximum profits.

Firms might take rational approaches to decisions but lack complete market information or the analytical capacity to use available information fully. When information is costly to acquire or analyse, firms make the best decisions they can with what they have. This situation is known as bounded rationality – the firm's ability to make fully rational decisions is limited by information constraints.

Understanding Bounded Rationality

Bounded rationality recognizes that perfect information is costly or impossible to obtain. Firms must therefore:

- Work with incomplete information

- Use simplified decision-making rules

- Accept "good enough" rather than optimal solutions

- Balance the cost of gathering information against potential benefits

This is a realistic modification of traditional profit-maximisation theory that better explains actual firm behavior.

Corporate social responsibility

Many firms now emphasise their commitment to ethical business practices. Corporate social responsibility (CSR) involves actions demonstrating commitment to behaving in the public interest. This might include:

- Promoting community programmes and charitable activities

- Improving employee welfare and working conditions

- Engaging in environmental protection and sustainability initiatives

- Encouraging employee volunteering activities

Has CSR become essential for firms' survival? If customers perceive that failing to engage with CSR significantly impacts a firm's sales, then commitment to social responsibility becomes crucial for competing with rivals. In this case, CSR expenditure becomes part of a firm's strategy to protect its market position, and these costs become necessary operating expenses for maintaining the market share needed to maximise long-run profits.

CSR and Profit Maximisation

There's an interesting relationship between CSR and traditional profit maximisation:

- If CSR enhances brand reputation and customer loyalty, it may increase long-run profits

- CSR spending might be viewed as a marketing investment rather than pure cost

- In competitive markets, CSR may become necessary just to maintain market position

- This suggests CSR can be compatible with profit maximisation in the long run

Why assume profit maximisation?

Given the various objectives firms might pursue, should economists abandon the profit maximisation assumption?

From a modelling perspective, assuming profit maximisation offers significant advantages. It provides a simple, clear assumption that enables straightforward analysis of firm behaviour. This creates a useful benchmark for understanding how firms operate, even if it doesn't perfectly describe all real-world behaviour.

Some apparently non-profit-maximising strategies might actually represent long-run profit maximisation. For example, if all firms in a market engage in CSR to improve credibility with customers, then CSR expenditure becomes part of operating costs and a necessary element of maintaining the market share required to maximise long-term profits.

The Value of Profit Maximisation as an Assumption

Profit maximisation provides a starting point for analysing firm behaviour. Economists can then explore how firms might behave differently under alternative assumptions, using profit maximisation as the comparison benchmark. Even if not universally true, it remains a useful analytical tool for understanding business decisions.

Think of it as similar to assuming perfect competition – it may not exist in pure form, but it provides a valuable reference point for analysis.

Case study: Coke vs Pepsi in India

In the mid-2000s, Coca-Cola and PepsiCo competed intensely to increase sales in India. A pesticide contamination scare in previous years had caused sales to plummet, and both firms sought recovery.

The companies adopted several strategies:

- Reducing bottle sizes to appeal to lower-income consumers

- Cutting prices to increase affordability

- Expanding distribution in rural areas

- Encouraging more at-home consumption in urban areas

India offered substantial growth potential, showing one of the world's lowest average consumption levels of fizzy drinks, significantly below the Asian average. This partly reflected concerns about children consuming colas at school.

However, the firms charged some of the world's lowest prices for cola, battling to increase market share. This led to reduced profit margins and continued competition from local producers. The logistics of supplying such a large and diverse region added significantly to costs. To counter this, companies reduced bottle weight and used cheaper transport methods like bullock carts and cycle rickshaws in rural areas.

Market analysts suggested that soft-drink companies should be able to improve profits, but executives remained focused on boosting sales volumes. A Coca-Cola marketing executive in India stated that "any affordability strategy will put pressure on margins, but it is critical to build the market".

The CSR Dimension

The pesticide controversy proved long-lasting. The Kerala government filed a criminal complaint against PepsiCo over environmental impact, though this was rejected by the Supreme Court of India in 2010. Interestingly, the US Department of State named PepsiCo as one of 12 transnational companies displaying "the most impressive corporate social responsibility credentials in emerging markets".

This highlights how CSR can become crucial for maintaining market position, especially after reputational damage.

Analysis Questions:

-

Were Coca-Cola and PepsiCo trying to maximise short-run profits?

No – the companies were accepting lower profit margins by cutting prices and increasing costs through rural distribution expansion. -

What objectives were the firms trying to achieve through their strategies?

The firms appeared to be pursuing sales maximisation or market share growth, prioritizing volume over immediate profits to "build the market." -

How were firms seeking to influence their costs?

By reducing bottle weight and using cheaper transport methods (bullock carts, cycle rickshaws) to lower distribution costs in rural areas. -

What might PepsiCo's CSR record have on its market position?

Strong CSR credentials could help rebuild trust after the pesticide controversy and differentiate the brand from competitors. -

What might firms want to achieve in the long run?

The strategy suggests long-run profit maximisation through building market dominance, establishing brand loyalty, and creating infrastructure that would pay off once market penetration increased.

This case illustrates how firms may prioritise market share and sales volume over immediate profit maximisation, whilst also demonstrating the growing importance of corporate social responsibility in business strategy.

Key Points to Remember:

-

Average revenue equals price: Ignoring indirect taxes, the price customers pay for a good is the average revenue the firm receives. The demand curve represents average revenue.

-

Marginal revenue falls faster than average revenue: When a firm has a downward-sloping demand curve, the marginal revenue curve declines at twice the rate of the average revenue curve. MR becomes zero when total revenue reaches its maximum.

-

The rule is crucial: Firms maximise profit by producing where marginal revenue equals marginal cost, with MC cutting MR from below. This principle applies across all market structures.

-

The shut-down point protects against losses: In the short run, a firm will continue operating if it covers variable costs, even if not making normal profit. The shut-down point occurs where price falls below average variable cost.

-

Firms may pursue alternative objectives: Instead of profit maximisation, firms might aim for:

- Revenue maximisation (where )

- Sales maximisation (where including normal profit)

- Long-run profit maximisation requiring short-term sacrifices

-

Behavioural theories reflect reality: Satisficing behaviour, bounded rationality, and corporate social responsibility help explain why firms don't always maximise profits. These approaches may actually serve long-run profit maximisation by building sustainable competitive positions.