Controlling Monopolies and Promoting Competition (Edexcel A-Level Economics A): Revision Notes

Controlling Monopolies and Promoting Competition

Controlling and regulating monopoly

The Competition and Markets Authority (CMA) investigates mergers that could increase market concentration. The CMA is particularly concerned about markets where concentration is already high. Natural monopolies present special challenges for policy-makers seeking to promote allocative efficiency.

Understanding natural monopolies

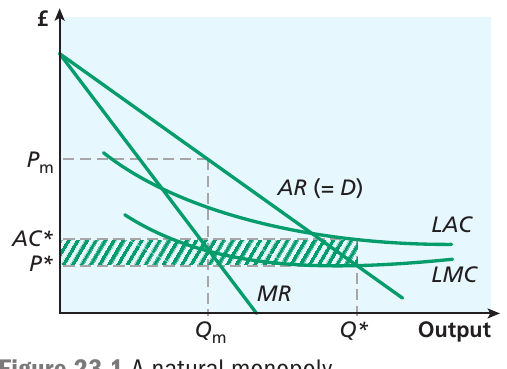

A natural monopoly occurs when one firm can supply an entire market more efficiently than multiple firms could. This happens because the industry has substantial economies of scale compared to market demand. In these industries, the minimum efficient scale of production is actually larger than the total market demand.

Understanding the Natural Monopoly Diagram

The diagram illustrates the key challenge facing natural monopolies:

- The long-run average cost (LAC) curve continues to fall across the entire range of market demand, showing ongoing economies of scale

- The demand curve (AR = D) and marginal revenue (MR) show market conditions

- If the monopoly maximises profits, it sets output at where marginal revenue equals marginal cost, charging price

- The competitive output level would occur where price equals marginal cost

Industries like railway systems, water supply, gas supply and electricity generation often operate as natural monopolies due to their large fixed costs relative to marginal costs.

The fundamental problem with natural monopolies

The Natural Monopoly Dilemma

Natural monopolies face a crucial policy dilemma. If such firms were required to set prices equal to marginal cost (at in the diagram), they would make losses. The average cost at this output level () exceeds the price, creating a loss shown by the shaded area on the diagram. This makes the firm financially unviable.

Because the largest firm can always dominate and undercut smaller competitors due to its natural cost leadership position, the market tends towards monopoly. If the monopoly chooses to maximise profits by setting marginal revenue equal to marginal cost, it will produce output and charge price , earning supernormal profits but creating allocative inefficiency.

Price regulation

Regulation emerged as one approach to controlling natural monopoly behaviour. Regulatory bodies focused initially on price controls, with the main method being to permit price increases each year at a rate set below changes in the retail price index. This became known as the RPI minus X rule.

The basic principle was to force companies to seek productivity gains to eliminate inefficiency that had accumulated over time. The X represents the productivity improvement that the regulator believed could be achieved, measured in terms of changes in average costs.

How the RPI - X Rule Works

If the regulator believed 5% productivity gains per year were achievable, and the RPI was increasing at 10% annually, then the maximum permitted price increase would be:

This forces the firm to become more efficient while allowing some price increases to account for general inflation.

However, this approach has inherent problems:

- Setting the X value: How does the regulator determine the appropriate productivity target? This is particularly problematic when companies have better information about their costs than regulators do, creating asymmetric information issues

- Quality trade-offs: Firms might achieve productivity gains by reducing product quality or by neglecting long-term investment and allowing maintenance standards to decline

- Diminishing returns: As time passes and the RPI minus X system proves effective, inefficiency gradually gets squeezed out. The X value must be reduced over time as it becomes increasingly difficult to achieve further productivity gains

In water supply, the regulator Ofwat adopted a variant of this rule. Water companies were required to set prices according to RPI plus k, where k represented Ofwat's estimate of capital investment needs.

Profit regulation

An alternative regulatory method involves placing a limit on the rate of return that firms can earn, thereby preventing them from making excessive supernormal profits.

During 2022, significant rises in oil and gas prices fuelled inflation and caused many households to struggle with energy bills. Simultaneously, some oil producers announced substantial profits. This raised the question of whether profit caps would be appropriate in such circumstances.

The Profit Regulation Debate

Several issues emerged in the debate:

- Business viability: Although some companies made large profits, others would have gone out of business if not allowed to raise prices. Capping profits could damage incentives for firms and shareholders to invest

- Efficiency concerns: Firms may not feel the need to operate as efficiently as possible if they can avoid declaring excessively high rates of return. They might fritter away profits in managerial perks

- Limited consumer impact: Limiting price rises to avoid large profits would only have limited impact on consumers if firms were going out of business or unable to find investment funds

Another approach considered was imposing a windfall tax on energy producers to recover some of the profits being earned. Although some large companies appeared to be making substantial profits in the UK, they also had to pay taxes on operations elsewhere. Nonetheless, the 2022 Autumn Statement announced an increase in the Energy Profits Levy from 25% to 35%.

Quality standards

By the mid-2010s, concerns had grown about the effectiveness of price regulation alone. There was a perception that companies were focusing too heavily on cost-saving rather than output delivery, and that they were pursuing static rather than dynamic efficiency. Environmental issues and output quality were receiving insufficient attention.

The regulators Ofwat (water) and Ofgem (gas and electricity) acted to phase out the RPI minus X controls, replacing them with the RIIO method. RIIO stands for Revenue using Incentives to deliver Innovation and Outputs.

RIIO is a price control mechanism that specifies the outputs companies must deliver and the revenue they can earn for delivering these outputs efficiently. The aim is to provide better incentives for companies to meet quality standards, rather than focusing solely on costs.

Performance targets

Under RIIO, companies that deliver their output targets within budget gain additional revenue generation. However, companies that fail to meet their performance targets face financial penalties. Companies must report to their regulator on an annual basis.

In water supply, the government strategy requires companies to provide social tariffs for customers who cannot afford to pay for water. This is monitored as part of the performance approach.

Some limitations of the regulatory approach

Key Limitations of Regulation

The effectiveness of regulatory attempts to control monopoly firms faces several limitations:

- High administrative costs: Monitoring performance carries significant administrative expenses

- Target identification difficulties: It can be challenging for regulators to identify appropriate targets for firms

- Asymmetric information: The monopoly firm typically has better information about its performance than the regulator does

- Regulatory capture risk: There have been examples where regulators have come to champion the firms they are supposed to be scrutinising, rather than controlling them effectively

Promoting competition and contestability

Beyond direct regulation, governments intervene in various ways to promote competition. This reflects the view that competition provides the best way of ensuring consumer protection and efficient resource allocation. It is also important that contestability can be introduced to discourage dominant firms from abusing their market power.

Encouragement of small businesses

Measures exist to encourage small businesses to grow and compete effectively. Following the wake of the 2008/09 financial crisis, the UK government was particularly keen to restore confidence in the economy.

The Department of Business Innovation and Skills (BIS) noted that small and medium-sized enterprises (SMEs) provided nearly 60% of jobs and 50% of GDP. A new set of measures to help small businesses was launched in 2010/11, including steps to improve access to finance and provide other forms of support. The underlying rationale was to help small businesses compete more effectively and provide targeted support to small firms with high growth potential.

However, promoting small businesses carries an opportunity cost for government, as it may divert funds from elsewhere. It may also work against market pressures under which large firms might operate more efficiently.

The financial crisis created particular problems. Banks became reluctant to lend, causing difficulties for small firms needing funding for investment. Banks faced a severe crisis themselves, with some requiring government assistance to bail them out of trouble. This was perhaps one of the largest-scale interventions in recent decades until the COVID-19 pandemic required even more substantial government intervention. While the prime aim was not to promote competition, encouraging banks to lend to small businesses was one of its side-effects.

Deregulation

Deregulation occurs when a government removes restrictions placed on producers in a market to encourage competition. This reflects the belief that competition benefits consumers by encouraging innovation and efficiency improvements, and by limiting the market power of firms.

The main argument for deregulation is that over-regulated firms may become complacent, which can result in X-inefficiency. Over-regulation may stifle innovation and risk-taking that could otherwise lead to new developments benefiting consumers.

The Dangers of Deregulation

However, deregulation carries dangers. Firms may take too much advantage of their newfound freedom from rules and restrictions. Widespread deregulation of financial markets in the early 2000s allowed banks in many countries to become too inventive in their search for new profit-making opportunities, laying the foundations for the financial crisis that affected the global economy in the late 2000s.

Deregulation can lead to more intensive competition. Until 2006, the Royal Mail held a monopoly in the postal service market in the UK, having maintained that position for 350 years. Action was taken to make the market more contestable. From 1 January 2016, any licensed operator could deliver mail to business and residential customers. This led to a surge of new businesses providing delivery services.

Direct provision or competitive tendering?

An approach that government could take to correct a market failure, or to improve resource allocation, is to undertake direct provision of a good. In the case of public goods, there must be some form of government involvement, as a free market will not ensure their provision.

Direct provision is closely akin to nationalisation, and many governments have been reluctant to follow this route. It has been recognised that the same arguments applying to the impact of competition on private sector efficiency are also relevant for public sector activity. Therefore, there is no guarantee that direct government provision will produce a more efficient allocation of resources. Furthermore, governments may not have the administrative or practical experience to engage directly in the production process.

However, direct provision is not the only way of ensuring a good is supplied. Several approaches have been developed whereby the public sector can ensure provision through some form of engagement with the private sector.

Contracting out

The simplest form of public-private cooperation is contracting out. Under this arrangement, the public sector issues a contract to a private firm for the supply of some good or service. One example is waste disposal, where a local authority may issue a contract for a firm to provide the necessary service.

Competition between firms can be encouraged by a competitive tendering process. In other words, the contract would be announced and firms invited to submit bids specifying the quality of service they are prepared to provide, and at what price. The local authority would then be positioned to choose the most competitive bid. The effectiveness of this approach would be reduced if firms engaged in collusive tendering.

Public-private partnerships

More complex models of cooperation between public and private sectors have been developed, involving various kinds of public-private partnership (PPP). A PPP is an arrangement by which a government service or private business venture is funded and operated through a partnership of government and the private sector.

The most common partnership model is the Private Finance Initiative (PFI), later reformed as PF2.

The Private Finance Initiative

The PFI was launched in 1992 as a way of trying to increase private sector involvement in the provision of public services. This established a partnership between the public and private sectors. The public sector specifies, perhaps in broad terms, the services it requires, and then invites tenders from the private sector to design, build, finance and operate the scheme.

In some cases, the project may be entirely free-standing. For example, the government may initiate a project such as a new bridge, which is then taken up by a private firm that recovers its costs entirely through user charges such as tolls. In other cases, the project may be a joint venture between the public and private sectors. The public sector could become involved with such a venture to secure wider social benefits, perhaps through reductions in traffic congestion that would not be reflected in market prices, and that would not be fully taken into account by the private sector. In other cases, it may be that the private sector undertakes a project and then sells the services to the public sector, often over a period of 25 or 30 years.

The aim of the PFI was to improve the financing of public sector projects. This is partly achieved by introducing a competitive element into the tendering process. In addition, it enables the risk of a project to be shared between the public and private sectors. This was intended to enable efficiency gains to be made.

The Evolution and Criticism of PFI

The PFI was much debated and criticised because of poor-quality outputs and high costs to the taxpayer. A reformed process (PF2) was launched in December 2012, but enthusiasm for this approach has waned. The collapse of Carillon, which held numerous PFI contracts, in early 2018 fuelled the criticisms.

One effect of the PFI is to reduce the pressures on public finances by enabling greater private sector involvement in funding. However, it might be argued that this may actually raise the cost of borrowing, if the public sector would have been able to borrow on more favourable terms than commercial firms.

The introduction of a competitive element in the tendering process may be beneficial, but on the other hand it could be argued that the private sector may have less incentive than the public sector to give due attention to health and safety issues. There may be a concern that private firms will be tempted to sacrifice safety or service standards in the quest for profit. Achieving the appropriate balance between efficiency and quality of service is an inevitable problem to be faced whatever way transport is financed and provided. However, it becomes a more critical issue to the extent that use of the PFI switches the focus more towards efficiency and lower costs.

In the Budget of 2018, the government announced that it would no longer use PFI. However, many projects funded under the scheme continue to operate until they run down. In particular, there are a number of continuing projects in the NHS.

Privatisation

During Margaret Thatcher's Conservative government in the 1980s, there was widespread privatisation (the transfer of nationalised industries into private ownership). One central argument was that this would force managers to be accountable to their shareholders, which would encourage an increase in efficiency.

However, this did not remove the original problem: that these industries were natural monopolies. Therefore, wherever possible, privatisation was accompanied by measures to encourage competition and contestability, which were seen as even better ways to ensure efficiency improvements. This proved more feasible in some industries than others because of the nature of economies of scale. There is little to be gained by requiring several firms in a market where economies of scale can be reaped only by one large firm. However, changing technology in some industries did allow some competition to be encouraged, especially in telecommunications.

Extension: anti-competitive behaviour

The CMA does not only investigate mergers and acquisitions, but also examines cartels (price-fixing) and other forms of anti-competitive behaviour by firms.

Price-fixing by firms in a cartel is illegal in most countries globally. In the UK it is potentially a criminal offence.

CMA Action on Bid-Rigging (2018)

Two of the main suppliers of bagged household fuels to large supermarkets and petrol stations were found guilty of bid-rigging. The firms had colluded to rig competitive tenders to supply Tesco and Sainsbury's, agreeing to submit bids designed to allow one or the other firm to win, so that each could retain its existing customer. They were fined over $3.4 million.

Pharmaceutical Price Abuse: The Pfizer Case

The pharmaceutical company Pfizer produced an anti-epilepsy drug that was supplied to the NHS. The CMA discovered that expenditure by the NHS on the drug had increased from about $2 million in 2012 to about $50 million in 2013, following a price increase. The price charged to the NHS was higher than the price at which Pfizer was selling the drug in any other EU country. The CMA imposed a fine of $84.2 million on the company.

A similar case emerged in December 2016, when a CMA press release announced its provisional finding that Actavis appeared to have contravened competition law in its pricing of hydrocortisone tablets to the NHS. For example, the price of 10mg packs of the drug was seen to have increased from $0.70 in April 2008 to $88 per pack by March 2016.

Intervention to protect suppliers and employees

Restrictions on monopsony power

The main focus of the CMA's work is on mergers and markets where there could potentially be problems with firms gaining a dominant position. In the past, the Competition Commission had also identified issues with competition involving a monopsony, rather than a monopoly position. A high-profile example involved UK supermarkets.

Large supermarkets form a major part of the food industry in the UK, providing consumers with low prices and a wide variety of products. However, issues were raised about the way some supermarkets were treating their suppliers and farmers. When small farmers are supplying supermarkets that have substantial buying power, there is a possibility of exploitation of market power.

The Groceries Code Adjudicator

In December 2012, the competition minister announced that the Groceries Code Adjudicator was to be given greater powers to enforce the Groceries Code, providing additional protection for farmers and other suppliers, including the ability to fine supermarkets that transgress the code. In February 2015, it was announced that the Adjudicator was launching an investigation into Tesco following allegations that it had delayed payments to some suppliers and treated payments for shelf promotions unfairly.

The proposed merger of Sainsbury with Asda in 2018 raised concerns that the combined group would have enhanced monopsony power over its suppliers. This echoed concerns that had been rising over a number of years, notably the controversy over the pricing of milk in supermarkets. Farmers argued that the price they were receiving for milk at the farm gate was not covering their costs, and that the supermarkets were using the product as a loss leader at the farmers' expense. The CMA blocked this merger from taking place in 2019.

A monopsony producer is able to use its market power to control its supply chain and to keep its costs to a minimum. This may benefit consumers, who face lower prices for the final goods. However, the impact of a monopsony is to put pressure on suppliers, which may force some small enterprises out of business. It may also lead to less diversity in the range of goods on offer. Monopsony in a labour market may lead to lower levels of employment, with workers receiving lower wages. Control of monopsony may be needed to protect both suppliers and employees.

Nationalisation

In the past, one response to a natural monopoly would have been to nationalise the industry (take it into state ownership), since no private sector firm would be prepared to operate at a loss, and the government would not allow firms running such natural monopolies to act as profit-maximising monopolists making supernormal profits. Nationalisation would protect consumers from exploitation and also protect employees.

To prevent the losses from becoming too substantial, many utilities such as gas and electricity supply adopted a pricing system known as a two-part tariff system. Under this system, all consumers paid a monthly charge for being connected to the supply, and on top of that a variable amount based on usage. In terms of the natural monopoly diagram, the connection charge would cover the difference between and , spread across all consumers, and the variable charge would reflect marginal cost.

However, as time went by, this system came to be heavily criticised. In particular, it was argued that the managers of the nationalised industries were insufficiently accountable. The situation could be regarded as an extreme form of the principal-agent problem, in which the consumers (the principals) had very little control over the actions of the managers (their agents), a situation leading to considerable X-inefficiency and waste.

Nationalisation has been much less used in the twenty-first century, but there have been some high-profile examples. These have occurred when the government has decided to intervene to bail out failing firms. The bailout of a number of banks during the financial crisis in the late 2000s is one prominent example, although the banks concerned have now been returned to the private sector. Another example occurred in 2018, when the Virgin Trains East Coast franchise failed. The company was taken into public hands, and replaced by LNER, with a parent company owned by the secretary of state for transport.

The impact of government intervention

Successive UK governments have taken serious action to promote competition, using a variety of tools and approaches. The objective of such intervention is to have an impact on a range of important indicators:

- Prices: If firms compete with each other on price, then consumers should gain as they will face lower prices than if firms are free to exploit their market power. However, low prices may not always be what consumers want to see

- Profits: If firms face intense competition, they may find their profits are eroded, and some firms may not be able to sustain their market position

- Efficiency: Firms facing intense competition may become efficient in the short run, in the sense that they are likely to eliminate X-inefficiency to reduce average costs. However, if profits are low, they may not be able to achieve dynamic efficiency by innovating and developing new products

- Quality: Firms facing severe competition may not be able to maintain quality standards in their production, or they may not be in a position to look for product improvements

- Choice: Competition may force firms to focus on a narrower range of products in order to keep their costs down

Competition should ensure that consumers face reasonable prices, with good-quality products and variety of choice. Indeed, the whole basis of the market system is that the consumer is king, and firms only make profit when they are producing the products that consumers wish to buy.

Evaluating effectiveness

How effective has intervention been in practice? This is difficult to evaluate, as it is not possible to observe how things would look in the absence of intervention. There have been instances where the CMA or its predecessors have stepped in to prohibit a merger or acquisition, or have set conditions that safeguard consumer interests. The number of merger cases brought to the CMA's attention seems high, but many are ruled as not being contentious or not meeting the threshold rules for investigation. It might be argued that the very existence of the CMA with its powers to intervene may act as a deterrent to anti-competitive actions.

Questions to Consider

- Is monopoly always bad? Microsoft reached a position supplying 95% of the global market for operating systems for PCs. Was this because of abusing a dominant market position, or because it was very good at what it did?

- Are firms like Amazon and Google reaching market dominance because they are building market power, or because they are providing a service that consumers want?

- Is competition always good? When a local shop goes out of business because it cannot compete with the prices and variety of choice offered by supermarkets, do consumers end up with less choice, or with more choice?

There are no simple answers to these questions, but they provide endless possibilities for debate and for watching how markets evolve into the future.

Limits to government intervention

Government intervention through direct controls must be carefully designed to avoid introducing market distortions. This is reflected in the changing approaches over time that attempt to rectify flaws that have become apparent.

Regulatory capture

In some cases, regulatory capture is a problem. This occurs when the regulator becomes so closely involved with the firm it is supposed to be regulating that it begins to champion its cause rather than imposing tough rules where they are needed. In this situation, regulation is not likely to have the desired impact.

Asymmetric information

Asymmetric information can also come into play when the companies have better information about the way they are operating than their regulators. This makes it difficult for regulators to set appropriate targets or identify when firms are not operating efficiently. Firms may use their superior information to their advantage, making regulation less effective.

Key Points to Remember

- Natural monopolies require special regulatory approaches because forcing them to price at marginal cost would cause losses due to their cost structure

- Price regulation (RPI - X) aims to encourage productivity improvements but faces challenges with asymmetric information and quality trade-offs

- RIIO represents a shift towards outcome-focused regulation emphasising quality and innovation, not just cost control

- Deregulation can promote competition and innovation but carries risks if firms exploit too much freedom

- Public-private partnerships like PFI share project risks between sectors but have faced criticism over costs and quality concerns

- Privatisation aims to improve efficiency through shareholder accountability but must be accompanied by competition measures

- Monopsony power requires regulation to protect suppliers and employees from exploitation by large buyers

- Nationalisation has been used sparingly in recent decades, mainly to bail out failing firms or maintain critical services

- Government intervention impacts multiple outcomes including prices, profits, efficiency, quality and choice

- Regulatory capture and asymmetric information represent key limitations that can undermine the effectiveness of intervention