Analysing the financial performance of business (AQA GCSE Business): Revision Notes

Financial statements

What are financial statements?

Financial statements are essential documents that every business must produce by law. They provide a clear picture of a company's financial health and performance, helping both internal managers and external stakeholders make informed decisions about the business.

There are two main types of financial statements that businesses must prepare:

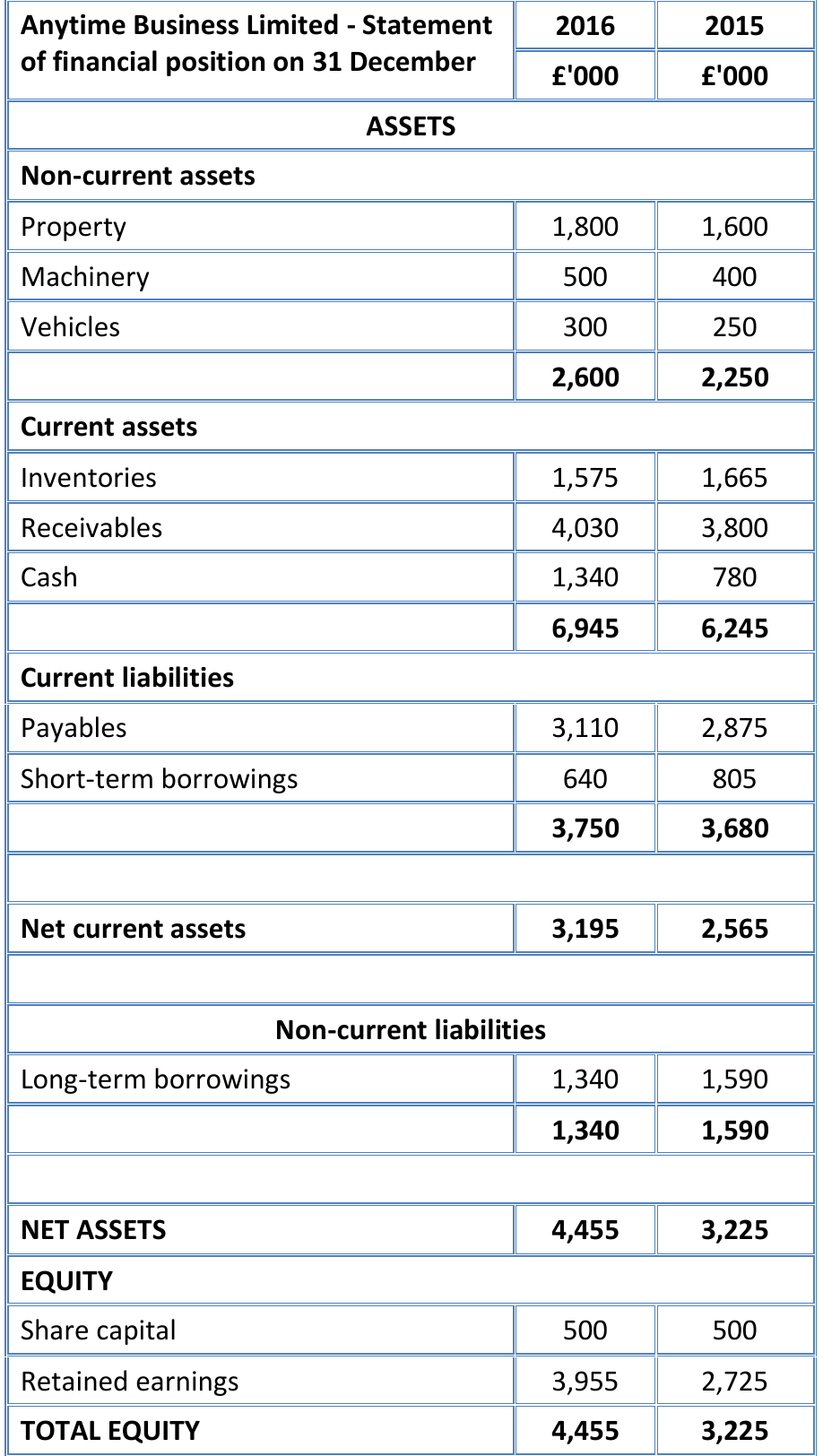

Key Definition: Statement of Financial Position

The statement of financial position acts like a photograph of the business's financial situation at one specific moment in time. It shows everything the business owns (its assets) and everything it owes (its liabilities) on a particular day, usually the final day of the financial year. This gives us the overall value or worth of the business.

Key Definition: Income Statement

The income statement works differently - it's like a video showing how well the business performed over a whole period, typically one year. It compares all the money coming into the business (income) with all the costs and expenses going out, helping us understand whether the business made a profit or loss.

Think of these two statements as complementary tools: the statement of financial position is a snapshot (like a photo), while the income statement is a performance record (like a video) showing what happened over time.

Who uses financial statements?

Financial statements aren't just for business owners - many different groups of people need this information to make important decisions. Each group has specific reasons for wanting to see these financial details:

Investors need to understand the risks and potential rewards of putting their money into the business. They want to know if the company can pay dividends and whether the management team is doing a good job running the business.

Lenders such as banks need confidence that any loans they provide will be repaid on time with interest. They use financial statements to assess whether the business is financially stable enough to meet its borrowing obligations.

Suppliers (payables) want to know if the business can pay for the goods and services they provide. They need assurance that they'll receive payment for their products.

Customers have a long-term interest in the business surviving and continuing to provide the products or services they depend on. They want to know the company will be around in the future.

Employees and trade unions need information about job security and the company's ability to continue paying wages and protecting pension funds. They're also interested in how much senior management is being paid.

Government agencies like HMRC (Her Majesty's Revenue and Customs) need profit information to calculate how much tax the business should pay.

Remember: Different users need different information from financial statements. Investors focus on profitability and growth, while lenders concentrate on the ability to repay debts, and employees are concerned with job security and wage payments.

Understanding the statement of financial position

The statement of financial position shows what a business owns and owes at a specific point in time. Here's how it's structured:

Current assets

Current assets are items that the business owns which can be converted into cash within the next twelve months. These are crucial for day-to-day operations because they help the business pay its bills, repay loans, and cover immediate expenses.

Inventories represent the stock that a business holds. This includes raw materials waiting to be used in production, finished goods ready for sale, and work-in-progress items that are partially completed. Inventories are considered the least liquid current asset because they take the longest to convert into cash. Sometimes stock might need to be sold cheaply or even thrown away if it becomes damaged or outdated.

Receivables are amounts owed to the business by customers who bought goods or services on credit. When a sale is made on credit, the business recognises the income immediately but doesn't receive the cash until later. These receivables will eventually become cash when customers pay their bills, although some may become bad debts if customers never pay.

Cash is the most liquid current asset - it's the actual money the business has in its bank accounts right now. This is immediately available to pay expenses and debts.

Liquidity Order - Remember ICE!

Current assets are always listed in order of liquidity (how quickly they can be converted to cash):

- Inventories (least liquid)

- Receivables

- Cash (most liquid - Easily available)

The closer an asset is to being cash, the more liquid it is!

Current liabilities

Current liabilities are debts that the business must pay within the next twelve months. These are typically paid using the money from current assets.

Payables are amounts the business owes to its suppliers for goods and services that have been received but not yet paid for. The timing of these payments depends on the credit terms agreed with each supplier.

Short-term borrowings include any money borrowed that must be repaid within one year. This category includes bank overdrafts and short-term loans.

Working Capital Management: The relationship between current assets and current liabilities is crucial for business survival. A business needs enough current assets to cover its current liabilities, or it may face cash flow problems.

Key calculations

Two important calculations help us understand a business's financial position:

Key Formula: Net Current Assets

This shows how much money is available for day-to-day operations after paying immediate debts. If this figure is negative, the business might struggle to pay its bills.

Key Formula: Net Assets

This represents the total value of the business, which equals the equity (ownership value) shown at the bottom of the statement of financial position.

Critical Concept: Negative Net Current Assets

If Net Current Assets is negative, this means current liabilities exceed current assets. This is a warning sign that the business may struggle to pay its immediate debts and could face serious cash flow problems.

Key Points to Remember:

- Financial statements provide a snapshot (statement of financial position) and a performance record (income statement) of business finances

- Many different groups use these statements for decision-making, from investors to employees to government agencies

- Current assets are listed in order of liquidity: inventories (least liquid), receivables, then cash (most liquid)

- Current liabilities must be paid within one year, while non-current liabilities are longer-term debts

- Net current assets show whether a business can meet its immediate obligations and continue operating day-to-day

- The statement of financial position must always balance: Assets = Liabilities + Equity