Competitive environment (AQA GCSE Business): Revision Notes

Competitive environment

Understanding the business landscape

Every business operates within a competitive environment, though the intensity of this competition varies significantly. While some entrepreneurs might hope to avoid competition entirely, the reality is that most businesses face some form of rivalry for customers. This competition can take different forms and has important implications for how businesses operate and succeed.

The competitive environment shapes how businesses make decisions about pricing, product development, marketing, and overall strategy. When competition is fierce, businesses must work harder to attract and retain customers. When competition is limited, businesses may have more flexibility in their approach, but this can also lead to complacency.

The Reality of Competition

Most entrepreneurs discover that completely avoiding competition is nearly impossible. Even businesses with unique products or services eventually face competitors as markets evolve and new entrants emerge. Understanding and preparing for competition from the start is crucial for long-term success.

What is a market?

Understanding competition requires first grasping what we mean by a market. A market represents the space where similar goods and services are bought and sold, giving consumers choices about how to spend their money. Markets aren't always physical locations - much of today's business happens online, where competitors' products and services can be easily compared and purchased.

Modern Market Dynamics

Modern markets are increasingly complex, with businesses competing not just locally but globally. The rise of e-commerce has made it possible for small businesses to compete with large corporations, while also exposing them to competition from around the world.

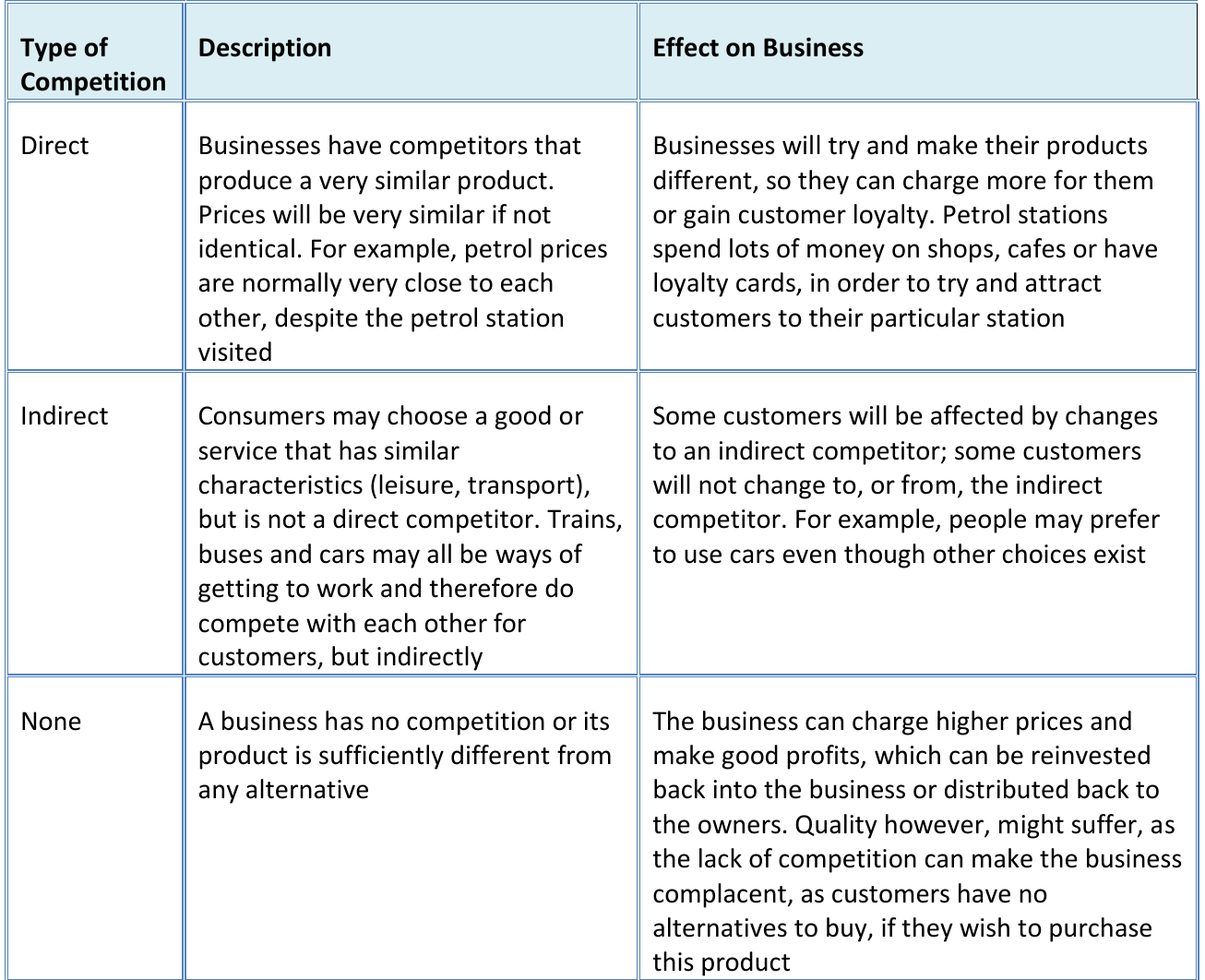

Types of competition

Competition comes in several forms, each with different implications for how businesses operate and succeed.

Direct competition occurs when businesses offer very similar products or services to the same customer base. These competitors often have nearly identical offerings, making price and service quality the main differentiating factors.

Direct Competition Example: Petrol Stations

Petrol stations typically compete directly because they offer essentially the same product. In response, businesses facing direct competition often try to differentiate themselves through customer service, loyalty programmes, or additional services like car washes or convenience stores.

Indirect competition happens when businesses offer different products or services that can satisfy the same customer need.

Indirect Competition Example: Transport Options

Transport provides a good example - trains, buses, and cars all help people get from one place to another, but they're not direct competitors. Some customers might be influenced by changes in one option (like higher petrol prices making cars more expensive), while others remain loyal to their preferred method regardless of alternatives.

No competition exists when a business offers a unique product or service with no viable alternatives. This situation, sometimes called a monopoly, allows businesses to charge higher prices and potentially earn greater profits. However, the lack of competitive pressure can sometimes lead to reduced innovation and quality, as there's less incentive to improve when customers have no alternatives.

Business risks in competitive environments

Running a business involves taking risks, and understanding these risks is crucial for success. Risk can be defined as the chance of loss or damage, the probability that something will go wrong, or when a hoped-for outcome doesn't materialise.

The Primary Business Risk

The primary risk facing any business is failure, which can result in the entrepreneur losing their investment. For sole traders and partnerships, there's the additional risk of personal liability for business debts.

Beyond financial losses, business failure can make it difficult to secure future employment or start another business. Perhaps most challenging is the personal impact of failure. Many entrepreneurs struggle with the psychological effects of business failure, even though failure is a normal part of the business world and nothing to be ashamed of.

Why Entrepreneurs Persist

These various risks often explain why entrepreneurs continue trying to make struggling businesses work - they're "risking it all" and putting tremendous effort into avoiding failure. The fear of losing everything motivates intense dedication to business survival.

Learning from business failure

One of the most valuable ways to understand business risks is to examine why businesses fail. By learning from these common mistakes, entrepreneurs can better prepare their businesses for success and survival.

| Factor | Details |

|---|---|

| Poor management | Plain and simple. Planning is inadequate leading to poor decision-making, costs are not kept under control, business owners or management do not understand their market and customers well enough and/or a poor quality product is provided. |

| Poor market research | In starting a business or keeping an existing business successful, there is a need to undertake market research. This will need to be reliable enough to predict future sales. If it is not done as it is too expensive, or if it is done that is out of date or not fully relevant. |

| Sales lower than expected | It is very easy to over-estimate the sales that will be achieved by a start-up. The business plan can be over-optimistic about the price that customers will accept and the volumes they will buy. |

| Start-up costs too high | Another common weakness of start-up business planning. Sometimes costs are simply missed out altogether or alternatively the amounts are under-estimated. This is a big concern at the start-up stage, where finance is limited. A delayed product launch or store opening may be the cause of start-up costs being higher than expected. |

| Unexpected shocks | These can come in various forms, for example flash floods that hit different places in the UK from time to time, a new competitor entering the market, a global recession, a change in government and the UK leaving the EU (BREXIT). |

| Too reliant on a small number of customers | A start-up that is too reliant on one or a few customers is at greater risk of failure than one which has a broader, more diverse customer base. If the customer relationship breaks down and/or the customer stops buying products from the business, then it puts the business at risk. |

| Poor quality | This is linked to poor management. Persistent poor quality products or services will ultimately kill a business, as rival businesses will produce superior products that customers will undoubtedly prefer. |

Poor management represents one of the most significant threats to business success. This includes inadequate planning, lack of cost control, insufficient understanding of the market, and failure to adapt to changing circumstances. Good management requires both business skills and the ability to make sound decisions under pressure.

Market Research Failures

Market research failures can doom a business from the start. Without reliable information about customer needs, market size, and competitor activity, businesses may develop products nobody wants or enter markets that can't support them. Proper market research requires time and resources, but skipping this step often leads to much larger problems later.

Overestimating sales is a common trap for new businesses. Entrepreneurs often have unrealistic expectations about how quickly customers will adopt their products or services. This overoptimism can lead to cash flow problems and inadequate preparation for slower-than-expected growth.

Underestimating costs can quickly drain a business's resources. Start-up costs are often higher than expected, and ongoing operational expenses may exceed initial projections. This is particularly problematic for new businesses with limited access to additional funding.

Uncontrollable External Factors

External shocks represent risks that businesses cannot completely control. These might include natural disasters, economic recessions, new competitors entering the market, or major political changes like Brexit. While businesses cannot prevent these events, they can prepare for them through contingency planning and maintaining financial reserves.

Over-reliance on limited customers creates vulnerability when key relationships change. Businesses that depend too heavily on one or a few major customers risk serious problems if these relationships end. Diversifying the customer base helps spread this risk.

Quality Problems

Quality problems can quickly destroy a business's reputation and customer base. In competitive markets, customers have alternatives, and persistent quality issues will drive them to competitors. Maintaining consistent quality requires ongoing attention and investment.

Rewards of enterprise

Despite the risks, entrepreneurship offers significant rewards that motivate people to start and run businesses. These rewards come in both financial and non-financial forms.

Non-financial rewards often provide the initial motivation for entrepreneurs. These include personal satisfaction from building something from scratch, having control over business decisions, and the excitement of achieving milestones like making the first sale or expanding to new locations. Many entrepreneurs also value the opportunity to help others and address social needs through their businesses.

Financial Rewards Take Time

Financial rewards, while often taking time to materialise, can justify the risks and effort involved in running a business. Successful entrepreneurs may build businesses worth millions of pounds, providing both personal wealth and the resources to start new ventures. The potential for significant financial gain motivates many people to accept the risks of entrepreneurship.

The combination of personal fulfilment and financial opportunity makes entrepreneurship attractive despite the risks. Many successful entrepreneurs use their experience and profits from one business to start others, creating a cycle of innovation and economic growth.

Key Points to Remember:

- Competition comes in three main forms: direct (similar products), indirect (alternative solutions), and none (monopoly situations)

- Business risks include financial loss, personal liability, and the challenge of future employment after failure

- Common reasons for business failure include poor management, inadequate market research, overestimated sales, and underestimated costs

- External shocks, over-reliance on few customers, and quality problems can also cause business failure

- Entrepreneurship offers both financial and non-financial rewards, including personal satisfaction, control, and the potential for significant profits