Break-even (OCR GCSE Business): Revision Notes

📚 Revision Notes

5.4 Break-even

Definitions

📎 Special order decision = A decision a business makes for an order that is outside of their usual routine

📎 Margin of safety = How much sales can fall before a business reaches its break-even point

📎 Contribution = How much each unit sold contributes towards covering fixed costs

- Useful as it helps businesses see which products are contributing the most/least

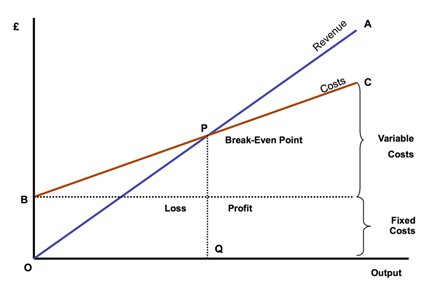

📎 Break-even point = When total revenue = total costs

📎 Break-even output = How many units you produce at your break-even point (measured in units)

Formulas

Revenue & Costs

Benefits

- Can change predictions to examine different scenarios (e.g., the impact of a rise in costs) allow the business to plan ahead and reduce expenditure/increase revenue, reduces risk, increases resilience

- Gives workers a target to aspire towards, more motivated, more commitment higher productivity

- Data generated can be used in a business plan, may help to obtain sources of finance in the future

- Based on estimates, don't take into account unexpected payments or external influences e.g., demand spikes or an economic downturn, decrease accuracy

Drawbacks

Many unrealistic assumptions!

- Doesn't account for the fact that variable costs do not always stay the same e.g., as output rises, may benefit from economies of scale, would reduce variable cost per unit

- Assumes that all units produced are sold, doesn't take into account a build-up of stock or damaged/wasted/refunded products

- Not suitable for a business with multiple products, not good for comparisons, waste of resources and time to create

- Its usefulness depends on the accuracy of the predicted data

Have a go at calculating the break-even point

A business makes and sells phone cases. It sells each case for £20. The variable cost is £8. The fixed cost is £30,000.

The calculation is shown below:

So, the business must sell 2,500 phone cases to break-even.