Australia's Current Account Deficit (HSC SSCE Economics): Revision Notes

Australia's Current Account Deficit

Understanding external stability and the current account

External stability refers to a key goal of government economic policy. It aims to ensure that Australia's economic relationship with the rest of the world remains sustainable over time. When external stability is achieved, imbalances in international trade and finance do not undermine domestic economic goals like growth, low unemployment, and price stability.

External stability is an aim of government policy that seeks to promote sustainability on the external accounts so that Australia can service its foreign liabilities in the medium to long run and avoid currency volatility.

The current account deficit (CAD) serves as a crucial measure of external stability. Australia must manage its external position carefully because unsustainable imbalances can trigger serious consequences:

- Currency depreciation

- Withdrawal of foreign investment

- Reduced access to overseas financial markets

- Higher interest rates

- Slower economic growth

Historical trends in Australia's current account deficit

Australia has experienced persistent current account deficits throughout much of its modern economic history. The best way to measure the CAD is as a percentage of GDP, which allows for accurate comparisons over time and between countries.

Key historical trends

The CAD has varied significantly across different decades:

- 1970s: averaged 1.1% of GDP

- 1980s: rose sharply to 4.1% of GDP

- 1990s: remained at 4.1% of GDP

- 2000s: increased to 4.9% of GDP

- 2010s: improved to 2.5% of GDP

For most of the period from the 1980s onwards, the CAD fluctuated between 3% and 6% of GDP. The large increase during the 1980s caused significant concern among policymakers and economists, prompting major structural reforms to restore competitiveness.

Recent improvements

A notable shift occurred in the late 2010s. Starting in 2019-20, Australia recorded a series of current account surpluses for the first time in nearly half a century. However, forecasts suggest a return to deficit, with the CAD projected to reach 3.5% of GDP by 2024-25.

Why does Australia have a persistent current account deficit?

Economists have developed three main explanations for Australia's ongoing CAD. Each provides different insights into the causes and implications of external imbalances:

- The CAD as a trade deficit - focusing on international competitiveness

- The CAD as a savings-investment gap - examining domestic capital needs

- The "consenting adults" thesis - analyzing private sector decision-making

The CAD as a trade deficit

This explanation focuses on Australia's trade performance, particularly the balance on goods and services. When the CAD first emerged as a major concern in the 1980s, economists primarily viewed it as the result of trade problems.

Lack of international competitiveness

Australia faces significant competitiveness challenges in higher value-added areas of global trade, particularly in elaborately transformed manufactures (ETMs). Many traditional manufacturing industries have struggled to compete with overseas producers who benefit from large-scale, low-cost production.

Examples of industries that have largely moved offshore include:

- Footwear and clothing

- Textiles and electronics

- Whitegoods and motor vehicles

- Tyres and machinery

- Oil refining and food processing

As manufacturing has declined as a share of total output, Australia has become more reliant on imports. This structural shift reflects both cost factors and non-cost factors affecting competitiveness.

Factors Affecting International Competitiveness

Cost factors include:

- Transport costs to overseas markets

- Lack of economies of scale in domestic production

- High labour costs

- Exchange rate levels

Non-cost factors include:

- Quality of production

- Reliability of supply

- Marketing effectiveness

- Customer service standards

In the 2023 IMD World Competitiveness Yearbook, Australia ranked 19th globally. The assessment highlighted the need to improve productivity growth, manage the clean energy transition more efficiently, and broaden the export base.

Dutch disease and commodity dependence

Dutch disease describes how strong demand for one type of export can drive up the exchange rate, making other exports less competitive. In Australia's case, high commodity prices have boosted the dollar's value, hurting non-commodity sectors.

Since the 2000s, sustained high commodity prices have contributed to this phenomenon. A stronger Australian dollar makes manufactured goods and services less price-competitive in international markets, further accelerating the decline in these sectors.

Think of "Dutch disease" as a commodity boom that makes other exports "sick" - when mining thrives, the strong currency hurts manufacturing and services competitiveness.

Terms of trade impacts

Australia's terms of trade have a major influence on the current account balance. The terms of trade measures the ratio of export prices to import prices, reflecting how much a country can import for each unit of exports.

Since 2003, Australia experienced the largest commodity price boom in its history. The terms of trade roughly doubled between 2003 and their peak in 2022. This dramatic improvement was driven by:

- Strong demand from China

- Supply constraints in global commodity markets

- Rising prices for iron ore (Australia's largest export)

The surge in commodity export revenues helped transform the trade balance. It improved from an average deficit of 1.5% of GDP in the 2000s to an average surplus of 0.2% in the 2010s. Between 2019-20 and 2021-22, the trade surplus averaged 4.7% of GDP.

Risks of a narrow export base

Critical Vulnerability in Australia's Export Structure

The improvement in Australia's current account position comes with significant risks due to the narrow export base:

- Two-thirds of export revenue comes from minerals and energy

- More than two-fifths of export dollars come from Chinese markets

This concentration creates vulnerability. A sharp fall in commodity prices or major disruption to trade with China could quickly trigger a large increase in the CAD. The narrowness of the export base represents a structural weakness in Australia's external position.

The CAD as a savings-investment gap

The second major explanation views the CAD as the result of an imbalance between domestic investment and domestic savings. This perspective offers a different understanding of why Australia runs current account deficits.

Understanding the savings-investment relationship

When domestic spending exceeds domestic output, Australia must finance the difference through financial inflows from overseas. In other words, foreign savings supplement domestic savings to fund domestic investment. The economy borrows from overseas or sells domestic assets to overseas residents.

Government budget deficits also affect this relationship. When the government runs a deficit, it reduces national savings and widens the savings-investment gap.

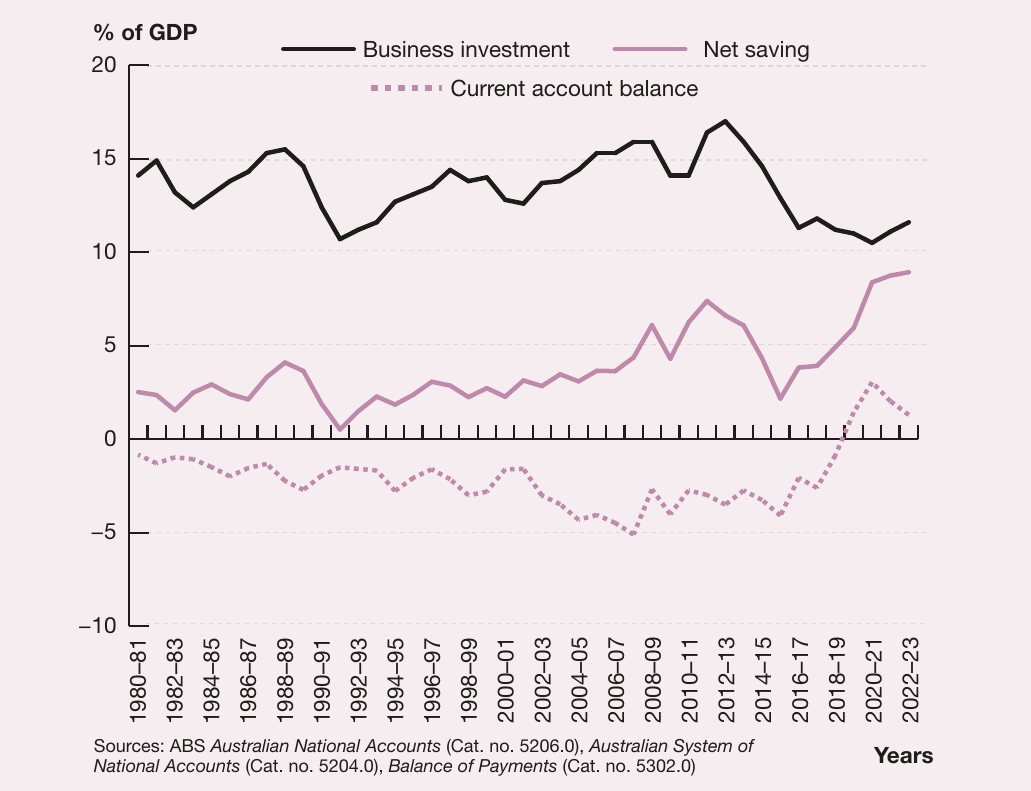

The diagram above shows the relationship between business investment, net saving, and the current account balance over time. Recent record-low global interest rates and reduced investment levels have helped narrow the savings-investment gap and improve the current account balance.

Australia's natural need for foreign capital

From this perspective, Australia's persistent CAD represents a natural consequence of the country's economic characteristics:

- Small population relative to land mass

- Extensive natural resources requiring development

- Large infrastructure needs

Historically, Australia has relied on overseas capital to bridge the gap between domestic savings and the investment needed for economic development. Foreign investment and borrowings have enabled Australia to grow more rapidly than would have been possible using only domestic savings.

When foreign capital supports growth

The key question is whether foreign capital increases Australia's productive capacity or simply funds purchases of existing assets like housing. If foreign investment and loans enhance productive capacity, they improve Australia's ability to service its foreign liabilities. Under these conditions, current account deficits become sustainable in the long term.

However, if foreign capital primarily funds consumption or purchases of existing assets, it does not enhance the economy's capacity to repay foreign obligations. This distinction is crucial for assessing the sustainability of the CAD.

The "consenting adults" thesis (Pitchford thesis)

The third explanation, developed by Professor John Pitchford in the 1990s, takes a more relaxed view of Australia's external imbalances. This argument became known as the Pitchford thesis or the "consenting adults" thesis.

The Pitchford Thesis

The Pitchford thesis states that as long as a current account deficit is the result of savings and investment decisions by the private sector that are not the result of distortions to normal market mechanisms, then there is no cause for concern about an economy's external stability.

Core arguments

Pitchford observed that Australia's CAD and foreign liabilities were almost entirely generated by the private sector. Even with recent large government budget deficits, the private sector still accounts for around 80% of Australia's net foreign debt.

This private-sector nature of foreign liabilities makes Australia different from many other countries that experienced financial crises due to large foreign debt burdens. In those cases, foreign debt typically resulted from government borrowing rather than private-sector decisions.

The thesis rests on several key assumptions:

- Private individuals and firms properly calculate risks and costs of overseas borrowing

- Borrowers and lenders act as "consenting adults" responsible for their own decisions

- Government policy does not distort private-sector decision making

- Private-sector debt remains separate from public-sector obligations

Under these conditions, the government need not be overly concerned about foreign liabilities accumulated by the private sector. Market mechanisms should ensure that borrowing and lending decisions remain sustainable.

Criticisms and limitations

Post-GFC Challenges to the Pitchford Thesis

The global financial crisis of 2008 prompted significant debate about the validity of the Pitchford thesis. Critics questioned whether its underlying assumptions always hold true.

Risk calculation concerns: The collapse of the subprime mortgage market in the United States demonstrated that large financial institutions may not accurately calculate risks associated with complex financial products. Private-sector actors do not always make perfectly informed decisions, even when they are "consenting adults."

Public-private separation: The Pitchford thesis assumes that private-sector debt remains entirely separate from public-sector debt. However, the global financial crisis showed that governments often must assume the liabilities of private-sector banks to prevent broader financial collapse. The line between private and public debt can blur during crises.

Recent support for the thesis: Despite these criticisms, the Pitchford thesis has received some vindication in recent years. Australia's improved current account position and downward trend in net foreign liabilities support the view that, particularly in an environment of strong commodity prices, Australia's external imbalances remain sustainable.

Key Points to Remember:

- External stability ensures that imbalances with the global economy do not undermine domestic economic goals

- Australia's CAD historically ranged between 3-6% of GDP from the 1980s until recent improvements

- The CAD can be explained as: (1) a trade deficit, (2) a savings-investment gap, or (3) acceptable private-sector decisions

- Australia lacks competitiveness in manufacturing and services but relies heavily on commodity exports

- Dutch disease occurs when commodity booms strengthen the currency, hurting other export sectors

- Two-thirds of export revenue comes from minerals and energy, with over 40% going to China

- The savings-investment gap explains why Australia needs foreign capital to fund development

- The Pitchford thesis argues that private-sector foreign debt should not concern government, though the GFC raised questions about this view