Simple Interest (HSC SSCE Mathematics Standard): Revision Notes

Simple Interest

What is simple interest?

Interest is the cost of borrowing money or the reward for saving money. When you take out a loan, you pay interest to the lender. When you save money in a bank account, the bank pays you interest.

There are different methods for calculating interest. One common method is simple interest (also called flat interest), which is used in flat-rate loans. Simple interest is a fixed percentage of the original amount borrowed or invested, and it remains constant throughout the loan or investment period.

Simple interest differs from compound interest because it's calculated only on the original amount (principal) and doesn't change over time. This makes calculations straightforward and predictable.

For example, if you borrow $10,000 from a bank at a simple interest rate of 6% per annum (per year), you would pay $600 in interest each year:

Or you can think of it as:

The key feature of flat-rate loans is that they are calculated on the initial amount borrowed, known as the principal. The total amount you owe is found by adding the interest to the principal.

Simple interest formulas

There are two important formulas for simple interest calculations:

Simple interest formula:

Amount owed formula:

Where:

- = Interest (simple or flat) to be paid for borrowing the money

- = Principal, the initial amount of money borrowed or invested

- = Rate of simple interest per period, expressed as a decimal (e.g., 6% = 0.06)

- = Number of time periods (years, months, etc.)

- = Amount owed or total to be paid

Converting percentages to decimals: Always remember to convert the interest rate percentage to a decimal before using it in calculations. To convert, divide by 100 (e.g., 9% = 9 ÷ 100 = 0.09).

Calculating simple interest

Let's work through an example to see how these formulas work in practice.

Worked Example: Calculating Simple Interest on a Loan

Abbey applied for a flat-rate loan of $40,000 at 9% per annum simple interest. She plans to repay the loan after two years and six months.

a) How much interest will be paid?

Write the simple interest formula:

Identify the values:

- (9% expressed as a decimal)

- (2 years and 6 months = 2.5 years)

Substitute into the formula:

Evaluate:

Therefore, the simple interest owed is $9,000.

b) What is the total owing at the end of two years and six months?

Write the amount owed formula:

Substitute and :

Therefore, the amount owed is $49,000.

Simple interest on bank accounts

Banks can also pay simple interest on savings accounts. Often, interest is calculated on the minimum monthly balance.

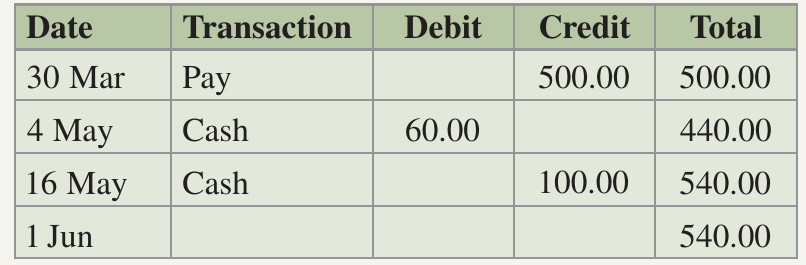

Worked Example: Interest on Savings Account

The table below shows the entries in Shane's bank account. If the bank pays interest at a rate of 3% per annum on the minimum monthly balance, find the interest payable for the month of May correct to the nearest cent.

Solution:

Determine the minimum monthly balance for May:

Looking at the table, the minimum balance during May was $440.00 (after the cash withdrawal on 4 May).

Write the simple interest formula:

Substitute the values:

- (one month is one-twelfth of a year)

Evaluate:

Therefore, the interest payable for May is $1.10.

Exam tip: When calculating interest for periods less than a year, express the time period as a fraction of a year. For example:

- 1 month = year

- 6 months = year

- 3 months = year

Finding the principal

Sometimes you know the interest amount and need to find the principal. This requires rearranging the formula.

Worked Example: Finding the Principal

Noah applied for a simple interest car loan with an interest rate of 9% p.a. He was told the total simple interest would be $6,300 for 3½ years. What was the principal?

Solution:

Write the simple interest formula:

Substitute the known values:

Make the subject by dividing both sides by :

Evaluate:

Therefore, the principal is $20,000.

Quick formula for finding principal: To find the principal directly, rearrange the formula to:

This can save time when you know the interest amount, rate, and time period.

Loan repayments

A loan repayment is the amount of money paid at regular intervals over the loan period. Common payment intervals include fortnightly or monthly payments.

Loan repayment formula:

This can also be written as:

Calculating loan repayments

Let's see how to calculate regular loan repayments with a practical example.

Worked Example: Calculating Fortnightly Loan Repayments

Jessica wishes to buy a lounge suite priced at $2,750. She chooses to buy it on terms by paying a 10% deposit and borrowing the balance. Interest is charged at 11.5% p.a. on the amount borrowed. Jessica makes fortnightly repayments over 3 years. Calculate her fortnightly repayments.

Solution:

Calculate the deposit:

Calculate the balance (amount to be borrowed):

Write the simple interest formula:

Substitute , , and :

Calculate the total to be paid:

Calculate the number of repayments:

There are 26 fortnights in a year, so over 3 years:

Calculate the fortnightly repayment:

Therefore, Jessica's fortnightly repayments are $42.68.

Exam tip: Remember these key time conversions:

- There are 26 fortnights in a year (52 weeks ÷ 2)

- There are 12 months in a year

- Always round money to two decimal places (nearest cent)

Simple interest graphs

When graphing simple interest, you create a visual representation of how interest grows over time. These graphs have distinct characteristics that make them easy to recognize.

Features of simple interest graphs

Simple interest increases by a constant amount each time period. This means that when you plot simple interest on a graph, you get a straight line. The graph shows a linear relationship between time and interest.

The key characteristic of simple interest graphs is that they are always straight lines. This is because the same amount of interest is added in each time period, creating a constant rate of increase.

How to construct a simple interest graph

Follow these steps:

Step 1: Construct a table of values for and using the simple interest formula.

Step 2: Draw a number plane with (time) on the horizontal axis and (interest) on the vertical axis. Plot the points from your table.

Step 3: Join the points to make a straight line.

Worked example: constructing a simple interest graph

Worked Example: Drawing a Simple Interest Graph

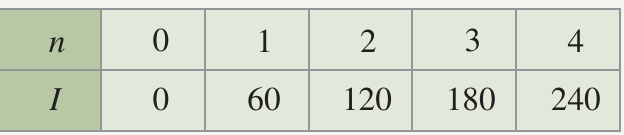

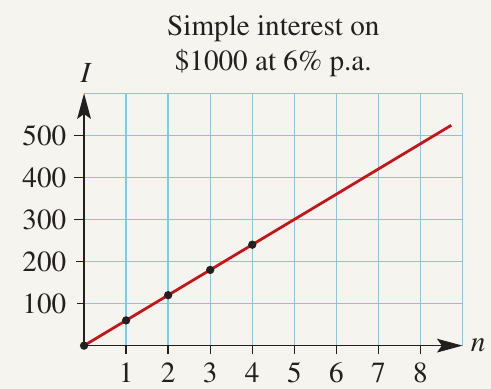

Draw a graph showing the amount of simple interest earned over a period of 4 years if $1,000 is invested at 6% p.a. Use the graph to estimate the interest earned after 8 years.

Solution:

Write the simple interest formula:

Substitute and :

Create a table of values by substituting different values of :

Draw the graph with on the horizontal axis and on the vertical axis. Plot the points , , , , and :

To estimate the interest after 8 years, extend the line to and read the corresponding value of from the graph.

From the graph, when , 480$`.

Therefore, the interest after 8 years is approximately $480.

Notice that the graph is a straight line passing through the origin. This is because simple interest increases by the same amount each year ($60 in this example). The slope of the line represents the interest earned per year.

Key Points to Remember:

-

Simple interest is calculated as a fixed percentage of the original amount (principal) borrowed or invested. It does not change over time.

-

The two key formulas are:

- (for calculating interest)

- (for finding the total amount owed)

-

When working with time periods, remember to convert months to years (divide by 12) and be aware that there are 26 fortnights in a year.

-

To find loan repayments, divide the total amount to be paid (principal plus interest) by the number of repayments.

-

Simple interest graphs are always straight lines because the interest increases by a constant amount each period. This is different from compound interest, which produces a curved graph.