Reducing-Balance Loans (HSC SSCE Mathematics Standard): Revision Notes

Reducing-Balance Loans

What is a reducing-balance loan?

A reducing-balance loan is a type of loan where interest is calculated based on the current balance you owe, not on the original amount you borrowed. This differs from a flat-rate loan, where the interest rate stays fixed on the original borrowed amount throughout the life of the loan.

The key advantage of a reducing-balance loan is that as you make payments, your outstanding balance decreases. When the balance decreases, the amount of interest charged also decreases. This means you pay less interest over time compared to a flat-rate loan, potentially saving thousands of dollars.

Financial institutions use tables to help calculate reducing-balance loan repayments because the calculations involved are quite complex. These tables simplify the process of determining your monthly payment amount.

Key formulas for loan repayments

When working with reducing-balance loans, you need to understand two important formulas:

Total amount to be paid:

Relationship between total payment, principal and interest:

From these formulas, you can rearrange to find the interest:

Key Terms to Remember:

- Principal is the original amount borrowed

- Interest is the cost of borrowing the money

- Loan payment is the regular payment amount (usually monthly)

- Number of repayments is how many payments you make over the loan term

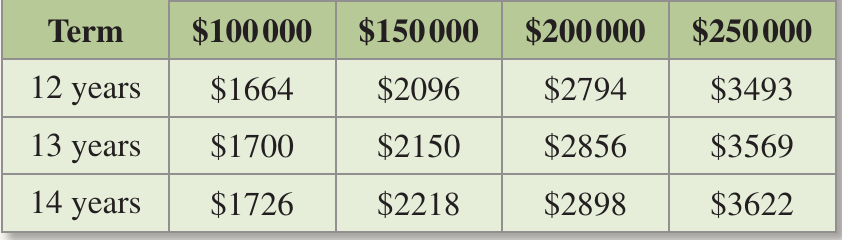

Worked example 1: Calculating interest using a loan table

Let's look at how to use a reducing-balance loan table to calculate the total interest paid.

Worked Example: Calculating Total Interest on a Reducing-Balance Loan

Question: Calculate the amount of interest to be paid on a loan of $200,000 over 13 years using the table below.

Solution:

Step 1: Identify the loan amount and time period

- Loan amount = $200,000

- Time period = 13 years

Step 2: Find the monthly payment from the table

- Look at the row for 13 years

- Look at the column for $200,000

- The monthly payment = $2,856

Step 3: Calculate the total amount to be paid

- Number of repayments = 13 years × 12 months = 156 months

- Using the formula:

Step 4: Calculate the interest paid

- Using the formula:

Answer: The interest paid is $245,536.

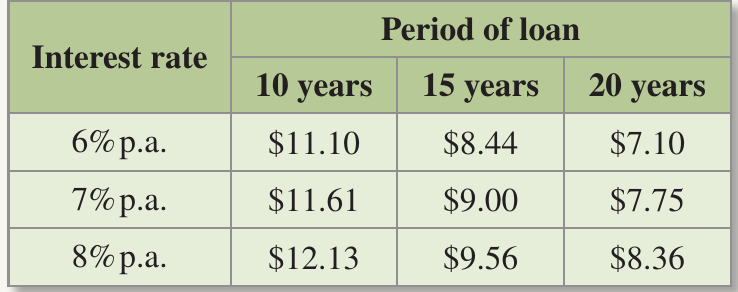

Worked example 2: Comparing different loan terms

Some loan tables show the monthly payment for each $1,000 borrowed. This type of table is useful for any loan amount.

Worked Example: Comparing Loan Terms Using a Per-$1,000 Table

Question: Molly is planning to borrow $280,000 to buy a house at 8% per annum. Use the table below to answer the following:

a) What is Molly's monthly payment if the loan is over 20 years?

b) How much would Molly pay in total to repay this loan?

c) How much would Molly save if she repaid the loan over 15 years instead?

Solution:

Part a) Finding the monthly payment:

Step 1: Find the value from the table

- Interest rate = 8% p.a.

- Loan period = 20 years

- From the table: $8.36 per $1,000 borrowed

Step 2: Calculate the actual monthly payment

- Molly is borrowing $280,000 = 280 thousands

- Monthly payment = $8.36 × 280 = $2,340.80

Answer: Molly's monthly payment is $2,340.80

Part b) Finding the total amount paid:

Step 1: Calculate total to be paid

Answer: The total amount paid for the loan is $561,792

Part c) Calculating savings with a shorter loan term:

Step 1: Calculate the monthly payment for 15 years

- From the table: $9.56 per $1,000 at 8% p.a. for 15 years

- Monthly payment = $9.56 × 280 = $2,676.80

Step 2: Calculate total to be paid over 15 years

Step 3: Calculate the savings

Answer: Molly would save $79,968 by repaying the loan over 15 years instead of 20 years.

Exam tip: Notice that although the monthly payment is higher for the 15-year loan ($2,676.80 vs $2,340.80), the total amount paid is much less because of the shorter loan period and reduced interest charges.

Fees and charges for loans

When you borrow money from a bank or financial institution, you'll pay more than just the interest. There are various fees and charges to consider:

- Loan application fee – covers the costs of setting up the loan initially

- Loan establishment fee – the initial cost of processing your loan application

- Account service fee – an ongoing monthly fee for maintaining your loan account

- Valuation fee – the cost of assessing the market value of a property (for home loans)

- Legal fee – covers the legal processing required for a property purchase

Many of these fees are negotiable, so it's worth comparing both the fees and interest rates between different financial institutions before choosing a loan. Don't assume the advertised fees are fixed – you can often negotiate better terms!

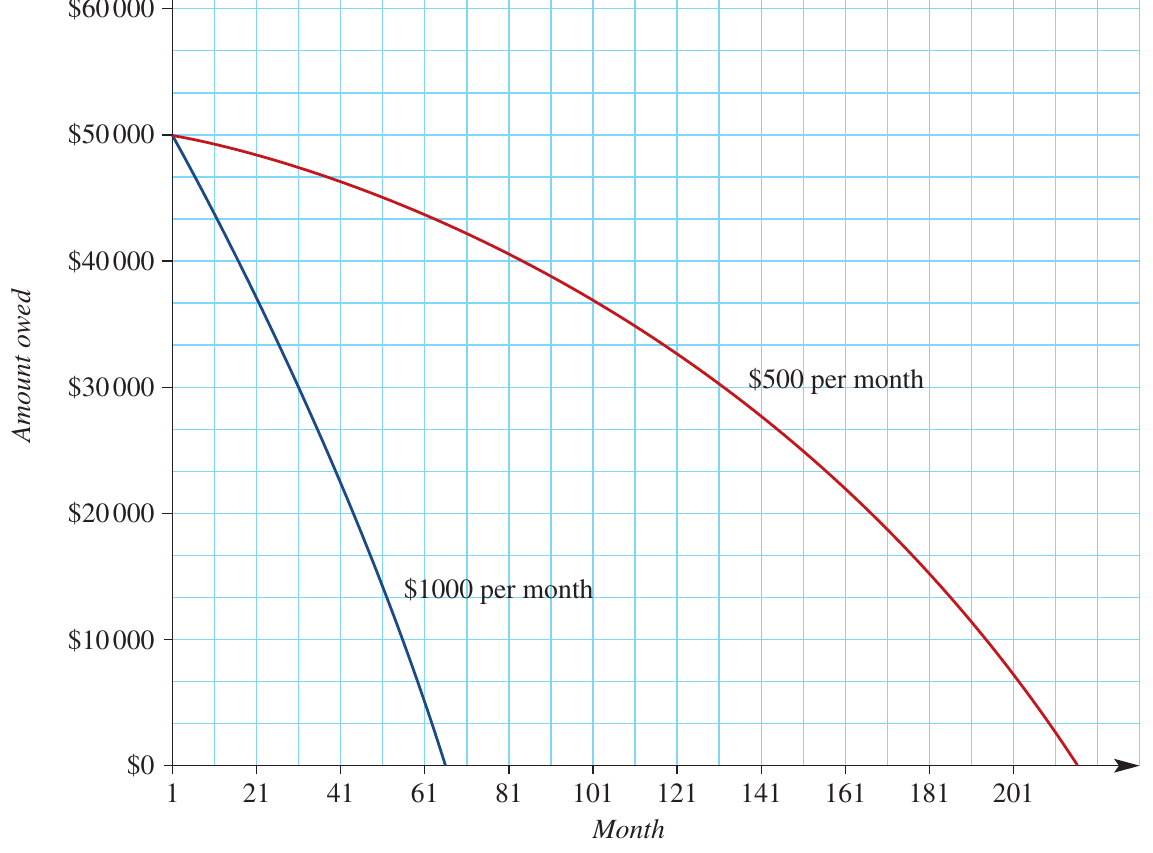

Visualising loan repayments

The graph below shows how different monthly payment amounts affect how quickly you pay off a reducing-balance loan.

This graph compares two repayment scenarios for a $50,000 loan at 10% per annum:

Scenario 1: $500 per month (red line)

- Time to repay: 215 months (about 18 years)

- Total interest charged: $57,500

Scenario 2: $1,000 per month (blue line)

- Time to repay: 65 months (about 5.5 years)

- Total interest charged: $15,000

Key observations:

- Both lines curve downward gradually rather than being straight lines

- This curve occurs because as the balance decreases, less interest is charged each month

- Doubling the monthly payment more than triples the rate of repayment

- Higher monthly payments result in dramatically less interest paid overall

- The $1,000 per month option saves $42,500 in interest

Critical Insight:

The graph shows that increasing your monthly payment is one of the most effective ways to reduce the total cost of a loan. Even modest increases in monthly payments can result in substantial savings over the life of the loan.

Remember!

Key Points to Remember:

-

Reducing-balance loans calculate interest on the remaining balance, which decreases with each payment – this saves money compared to flat-rate loans

-

Use the formula: Total to be paid = Loan payment × Number of repayments to find the total cost

-

Calculate interest using: Interest = Total to be paid - Principal

-

When using per-$1,000 tables, multiply the table value by the number of thousands borrowed

-

Shorter loan terms mean higher monthly payments but much less total interest paid

-

Don't forget to account for fees and charges in addition to interest when calculating the true cost of a loan

-

Higher monthly payments dramatically reduce both the time to repay and the total interest charged