Inflation and Deflation: Further Exploration (AQA A-Level Economics): Revision Notes

Inflation and Deflation: Further Exploration

Introduction

Understanding inflation and deflation requires looking beyond simple price movements. This note explores how expectations shape inflation, examines the real-world consequences of both rising and falling prices, and considers how global factors transmit inflationary pressures across borders. These concepts are essential for grasping why controlling inflation remains one of the most important challenges facing policymakers.

The role of expectations in the inflationary process

How expectations influence current inflation

Economists now recognize that when people anticipate future price increases, their expectations can influence today's inflation rate. This insight has become a fundamental part of modern economic theory. Milton Friedman, a leading economist, was among the first to highlight how expectations drive the inflationary process alongside the quantity theory of money.

The logic is straightforward: when individuals predict high inflation ahead, they adjust their behavior today in ways that actually push prices upward. Workers and trade unions negotiate for higher wages to protect their future purchasing power. Employers, anticipating these wage demands and higher costs, raise their prices now. This creates a self-fulfilling cycle where expectations about tomorrow's inflation generate the inflation we experience today.

The reverse also holds true. When people expect inflation to fall, their behavior changes in ways that help achieve lower inflation. Workers moderate wage demands, and firms feel less pressure to increase prices. This is why governments work hard to convince the public that inflation will remain low and that policymakers have the tools and determination to control it.

Theories of expectations formation

Two main theories explain how people form their inflation expectations. Although the detailed mechanics are complex, understanding the basic principles is valuable.

Adaptive expectations are where people form their beliefs of future events based on past events. In the context of inflation, if prices have been rising rapidly, people using adaptive expectations will assume that high inflation will continue. These expectations adjust slowly as new information emerges. When inflation has been persistently high, people expect it to remain high, which perpetuates the inflationary cycle.

Rational expectations are where people form their expectations using all available information that exists to support decision making. Rather than simply extrapolating from past trends, individuals consider current economic conditions, government policies, and any other relevant data. This means people can quickly adjust their expectations when circumstances change. For example, if the government announces credible anti-inflation policies, people immediately update their expectations rather than waiting to see results.

Modern economic theory, particularly monetarist theory, has incorporated rational expectations into its framework. This integration represents an evolution from Milton Friedman's original work on the quantity theory of money in the 1950s, through his development of expectations theory, to the current synthesis that recognizes how forward-looking behavior shapes economic outcomes.

Government credibility and monetary policy

The concept of credibility plays a vital role in managing inflation expectations. When people believe that the government and central bank have both the knowledge and the determination to control inflation, they are more likely to expect low inflation in the future. This belief itself helps keep inflation low.

The UK government's 1997 decision to grant operational independence to the Bank of England was partly motivated by the need to establish credibility. By removing day-to-day monetary policy decisions from political interference, the government aimed to convince financial markets and the public that inflation control would remain a priority regardless of short-term political pressures. The goal was to anchor inflation expectations around the 2% target.

However, credibility can be fragile. When the Bank of England fails to hit its inflation target, public confidence erodes. If people start to doubt the central bank's ability to control inflation, their expectations for future inflation rise. This makes the task of actually reducing inflation more difficult, as higher expectations become embedded in wage negotiations and pricing decisions.

Workers demand larger pay increases to compensate for expected inflation, which then pushes up costs for firms and contributes to actual inflation.

Inflation psychology

Beyond formal economic theories, psychology plays a significant role in inflation dynamics. Over decades, certain groups in British society developed a vested interest in allowing inflation to continue. Homeowners with large mortgages benefited as inflation reduced the real value of their debt. Property owners saw the nominal value of their houses increase faster than general inflation, improving their wealth position. Even some governments found inflation politically convenient as it eroded the real value of accumulated public debt.

This created an inflation psychology where inflation became normalized and expected. Different groups competed to stay ahead of price increases rather than working to prevent them. Those with strong bargaining positions could protect themselves by securing wage increases, while vulnerable groups on fixed incomes suffered losses.

Between 1997 and 2007, UK governments successfully challenged this psychology. By maintaining credible policies and keeping inflation close to the 2% target, they convinced people that low inflation would persist. This benign effect on expectations and behavior made inflation control significantly easier. People stopped automatically building high inflation into their economic decisions.

Yet even during this period, some economists warned against complacency. They argued that circumstances could change rapidly and that inflationary pressures might return. The experience of 2022, when multiple economic shocks overlapped, demonstrated these concerns. Inflation rose sharply, and expectations for future inflation increased, suggesting a potential return to more problematic inflation psychology.

Consequences of inflation for the economy and individuals

Understanding the impact

The effects of inflation on economic performance and individual welfare depend critically on whether inflation is anticipated or unanticipated. If everyone could predict inflation perfectly, many problems would disappear. Households and firms would simply build expected price increases into their economic calculations. However, complete anticipation is unrealistic, and wrong predictions create serious difficulties.

The two faces of inflation

When inflation remains low and relatively stable from year to year, predicting next year's inflation rate becomes straightforward. In this environment, creeping inflation can actually help the economy function more smoothly, a phenomenon economists describe as "greasing the wheels" of economic activity. Low, predictable inflation maintains business confidence, supports healthy profits, and creates conditions for economic expansion. Some economists argue that this type of inflation may be a necessary side-effect of policies designed to reduce unemployment.

However, the picture changes when inflation becomes problematic. Rather than greasing the wheels, higher or more variable inflation "throws sand in the wheels" of the economy. It reduces efficiency, distorts decision-making, and makes the economy less competitive. When the costs of inflation outweigh any benefits, inflation becomes a drag on economic performance.

Disadvantages of inflation

Distributional effects create winners and losers from inflation. Those with fixed incomes suffer as their purchasing power erodes. Pensioners on fixed pensions and workers without strong bargaining power fall behind as prices rise. Meanwhile, groups with negotiating strength can demand wage increases that keep pace with or exceed inflation, protecting their real income. During rapid inflation, real interest rates may turn negative, meaning lenders effectively pay borrowers for the privilege of lending. This represents a hidden transfer of wealth from savers to borrowers.

Distortion of normal economic behavior occurs when households and firms change their behavior in response to inflation. Consumers may bring forward purchases to avoid higher prices later, leading to hoarding of goods. Firms might divert investment away from productive long-term projects into commodity speculation, buying goods simply to sell them later at higher prices.

This type of activity creates no real value but ties up resources. Additionally, inflationary noise confuses economic signals. When individual prices change, people struggle to distinguish whether it reflects genuine changes in relative scarcity or simply reflects general inflation. This confusion leads to poor economic decisions.

Breakdown in the functions of money becomes severe during extreme inflation. Money serves as a medium of exchange, a store of value, and a unit of account. High inflation undermines these functions. In hyperinflation, where the rate of inflation accelerates to a minimum of several hundred percent a year, money loses usefulness entirely. People resort to barter, and economic transactions become far more costly and difficult. Even in less extreme cases, inflation reduces money's effectiveness as a store of value.

Reduced international competitiveness occurs when domestic inflation exceeds that of trading partners. If the UK experiences higher inflation than competitor countries, British exports become more expensive in foreign markets. With a fixed exchange rate, this pricing disadvantage reduces demand for exports while making imports cheaper, potentially increasing unemployment. A floating exchange rate can restore competitiveness as the currency depreciates, but the resulting higher import prices may fuel further inflation.

Shoe leather and menu costs represent transaction costs imposed by inflation. The term "shoe leather costs" (also called "search costs") refers to the time and effort consumers spend shopping around to find the best prices, metaphorically wearing out their shoes in the process. In the past, consumers needed to physically visit multiple shops to compare prices. Menu costs are incurred by firms having to adjust price lists more often. Restaurants must print new menus, shops must relabel products, and vending machines require adjustment.

Technology has reduced some of these costs. Online shopping makes price comparison easier, minimizing shoe leather costs. Digital price displays and computerized systems allow firms to adjust prices more readily, reducing menu costs. However, other inflation costs have grown.

Weakening trade union power means real incomes often fall during inflationary periods. Fiscal drag has become more significant, where increases in nominal income "drag" people into paying higher amounts of income tax even if their real income is unchanged. When governments fail to adjust tax bands in line with inflation, as happened in the UK during 2021-22, more income becomes subject to taxation, effectively raising the tax burden.

Consequences of deflation

Understanding deflation vs disinflation

Make sure you don't confuse deflation and disinflation. The former refers to falling prices whereas the latter refers to falling inflation (i.e. rising prices but at a lower rate).

- Deflation means a continuing or persistent fall in the average price level. Prices are actually declining.

- Disinflation refers to a slowing down in the rate of inflation. Prices are still rising, just at a decreasing rate.

The deflation debate: not all deflation is equal

Common sense might suggest that if inflation is problematic, its opposite must be beneficial. However, extended deflation brings its own serious challenges. When people expect prices to fall, they postpone major purchases like cars or houses, waiting for better deals. This behavior erodes business confidence, potentially triggering recession or deepening an existing downturn.

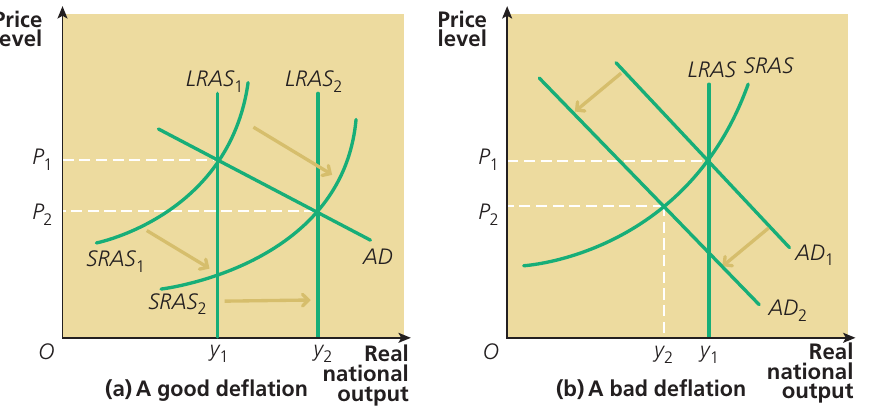

The key insight is that not all deflation has the same cause or consequence. Economists distinguish between good deflation (or benign deflation) and bad deflation (or malign deflation).

The diagram illustrates these two contrasting scenarios. Good deflation results from improvements on the economy's supply side, which reduce business costs of production. Both the short-run aggregate supply (SRAS) and long-run aggregate supply (LRAS) curves shift rightward. Assuming aggregate demand remains stable, the price level falls from P₁ to P₂, but real national output increases from Y₁ to Y₂. This represents a healthy expansion driven by productivity improvements or technological advances. Lower prices accompany rising output and employment.

Bad deflation, by contrast, stems from a collapse of aggregate demand. The AD curve shifts leftward, perhaps due to negative multiplier effects or a credit crunch during recession. With SRAS and LRAS unchanged, the price level falls from P₁ to P₂, but real national output contracts from Y₂ to Y₁. This scenario involves falling prices alongside declining output and rising unemployment.

The danger of deflationary spirals

Bad deflation creates particularly serious problems because falling prices disrupt the price mechanism and generate instability. During deflation, people become confused about relative values. They see prices falling and defer purchases, expecting even lower prices later. This reduction in spending erodes business confidence, leading firms to cut investment and employment.

A dangerous feedback loop can develop. Lower spending reduces output, which increases unemployment, which further reduces spending. This deflationary spiral can be difficult to escape. The real value of debt rises during deflation, which reduces people's net wealth and typically leads to decreased spending, perpetuating the downward cycle.

The housing market presents a particularly concerning example. If house prices crack and homeowners with large mortgages suddenly find themselves in negative equity (owing more than their homes are worth), many may need to sell. A wave of forced sales intensifies the deflationary pressure on house prices, creating a self-reinforcing spiral.

Understanding these dynamics is crucial. During the 2008-09 recession, UK policymakers faced deflation concerns. Their response included stimulus measures like the car scrappage scheme, which aimed to encourage spending and prevent a deflationary spiral from taking hold.

During deflationary periods, nominal interest rates may appear low while real interest rates (adjusted for falling prices) are actually high. If the Bank of England's base rate is 2% but prices are falling at 3%, the real cost of borrowing is 5%. This high real interest rate burdens borrowers and may discourage the borrowing and spending needed for economic recovery.

World commodity prices and domestic inflation

The changing nature of cost-push inflation

More than forty years ago, rising wage costs were widely seen as the primary driver of cost-push inflation in the UK. Recently, the picture has become more nuanced. Wage-cost inflation still occurs, but it tends to be concentrated among specific highly-paid groups like bankers, top business executives, and premier league footballers, whose salary increases far exceed productivity gains. Some public-sector unions, such as those representing London Underground train drivers, have contributed to cost pressures. However, for most ordinary workers, wages between 2008 and 2017 grew more slowly than inflation, with some experiencing no real wage growth at all. Pay freezes among public-sector workers since 2010 further dampened wage-cost inflation.

Cost-push inflation now stems mainly from rising prices of imported commodities. Food, energy, and raw materials have all experienced significant price increases, directly feeding into domestic inflation. To a lesser extent, manufactured goods imported from China and other countries have also contributed, though China's impact has historically been more disinflationary as cheap imports kept UK prices down.

This import-cost inflation operates through shifts in the short-run aggregate supply curve. When the cost of imported inputs rises, the SRAS curve shifts leftward, pushing up the general price level.

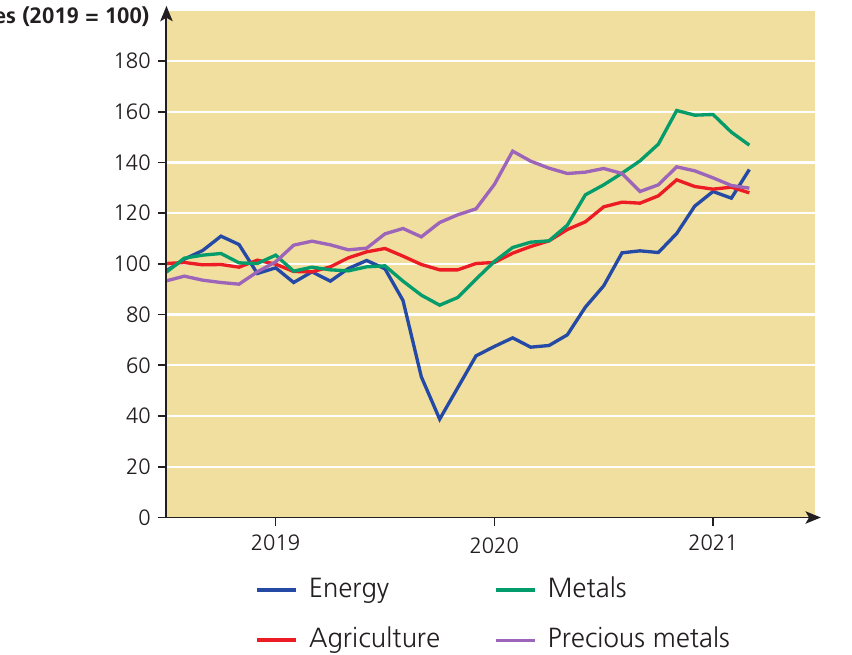

Understanding the Commodity Price Chart:

The chart displays how world commodity prices changed between January 2019 and September 2021, using index numbers with 2019 as the base year (= 100). Four categories are tracked: energy, metals, agriculture, and precious metals.

The most dramatic movement appears in energy prices (blue line), which collapsed to approximately 40 in early 2020 as the COVID-19 pandemic devastated global demand. Energy prices then recovered strongly through 2020 and 2021. Metals prices (green line) showed robust growth, peaking near 160. Agricultural commodity prices (red line) demonstrated steady gradual increases, reaching around 135. Precious metals (purple line) maintained a consistent upward trend to approximately 140.

The data were presented as index numbers rather than absolute prices, allowing easy comparison of percentage changes across different commodity types. For example, all commodities started at 100 in 2019, so a reading of 160 indicates a 60% price increase.

Recent patterns and future expectations

Periods like 2014-15 and 2020 saw UK inflation reduced by falling prices of food, oil, and other commodities. However, the situation reversed during 2021 and 2022, when rising commodity prices rapidly fed through into higher consumer prices. Some observers believe that although gas prices may eventually stabilize, they are unlikely to return to the low levels seen over the previous decade. This suggests upward pressure on inflation may persist for some time.

How changes in other countries affect UK inflation

The UK in the global economy

The UK now represents just a small part of an interconnected global economic system. This means the UK has very limited power to influence worldwide economic conditions. Instead, global forces shape domestic inflation outcomes.

When the world economy is booming, rising demand for commodities pushes up their prices. The UK tends to import inflation from the rest of the world. Higher prices for imported food, energy, and raw materials directly increase domestic inflation through import-cost inflation. Conversely, when the global economy experiences recession and other countries face economic difficulties, pressure on UK inflation eases. Falling worldwide demand for UK exports can even shift the aggregate demand curve leftward, potentially leading to falling domestic prices or deflation.

It is important to note that positive inflation (prices rising) is more likely than negative inflation (deflation). Additionally, when the pound's exchange rate falls against other currencies, this contributes to imported cost-push inflation by making all imports more expensive.

The particular influence of major economies

Two countries exert especially significant influence on UK price levels: the USA and China.

The saying "when America sneezes, the rest of the world catches a cold" captures the USA's importance to the UK economy. As a major source of export demand, inward investment, and business and consumer confidence, American economic conditions powerfully affect UK economic performance. An American economic downturn exerts downward pressure on UK inflation. Conversely, a booming American economy, as experienced in 2018, tends to push UK inflation upward.

China's impact on UK inflation follows a somewhat different pattern. For many decades, British consumers benefited from falling prices of manufactured goods imported from China. This reduced the UK's inflation rate. More recently, however, production costs in China have risen, partly reflecting higher wages paid to Chinese workers. As a result, manufactured goods imported from China and other emerging-market economies are now increasing retail prices in the UK. So far, this effect has been relatively mild, but it represents a shift from China's historical role as a source of disinflation.

External shocks and commodity prices

Events in other countries can create sudden shocks that affect UK inflation. A sudden increase in oil prices caused by instability in the Middle East will raise UK inflation. Conversely, the rapid growth of oil production through fracking in the USA has dampened world oil prices, reducing inflationary pressure in the UK.

These international linkages mean that UK policymakers must stay informed about developments in the European Union, the USA, and other major trading partners. Recent events provide valuable context for understanding how global forces shape domestic economic outcomes. Being aware of international developments adds depth and application to economic analysis.

Remember!

Key Points to Remember:

-

Expectations drive inflation: When people expect high inflation tomorrow, their behavior today creates that inflation. This makes managing expectations crucial for inflation control.

-

Credibility matters: Central bank independence and credible policies help anchor inflation expectations. When credibility erodes, controlling inflation becomes much harder.

-

Not all inflation is bad: Low, stable, predictable inflation may help economies function smoothly ("greasing the wheels"), but higher or variable inflation throws "sand in the wheels" and creates serious costs.

-

Deflation is not simply good news: While good deflation from supply-side improvements benefits the economy, bad deflation from collapsing demand can trigger dangerous deflationary spirals. Always distinguish between deflation (falling prices) and disinflation (inflation slowing down).

-

The UK imports inflation: As a small open economy, the UK is highly vulnerable to global economic forces. World commodity prices, especially for energy, and conditions in major economies like the USA and China significantly influence domestic inflation.