How the Macroeconomy Works (AQA A-Level Economics): Revision Notes

Determinants of Aggregate Demand

Introduction to aggregate demand components

Aggregate demand represents the total amount of planned spending on goods and services in an economy. It consists of four main components:

- Consumption (C) - spending by households on consumer goods and services

- Investment (I) - spending by firms on capital goods such as machinery and equipment

- Government spending (G) - spending by the government on public services and infrastructure

- Net exports (X-M) - the difference between exports and imports

This revision note focuses on the first two components: consumption and investment. These are the main drivers of aggregate demand in most economies, and understanding what causes them to change is essential for analysing macroeconomic performance.

Government spending and net exports are covered in other sections of the course. Government spending is examined when studying fiscal policy, whilst net exports are explored in relation to the balance of payments and international trade.

The determinants of consumption

Consumption refers to total spending by all households in an economy on consumer goods and services. When households decide how much to spend, they are simultaneously making decisions about how much to save. This means that the factors influencing consumption also determine the level of household saving.

In a simplified closed economy without government taxation or international trade, households face a simple choice with their income: they can either spend it on consumption or save it. This relationship can be expressed as:

Where is income, is consumption, and is saving.

Let's examine the key factors that influence consumption decisions.

Interest rates

The rate of interest represents two things: it is the reward savers receive for lending their money to others (such as banks), and it is the cost that borrowers must pay to access funds.

Interest rates affect consumption decisions because they determine the opportunity cost of spending. When interest rates rise, saving becomes more attractive because the reward for postponing consumption increases. This leads to higher saving and lower consumption. Conversely, when interest rates fall, the incentive to save diminishes, encouraging people to spend more.

What really matters for consumption decisions is not the nominal interest rate (the rate actually quoted by banks) but the real interest rate. The real interest rate adjusts for inflation and represents the true reward for saving.

The formula for calculating the real rate of interest is:

Worked Example: Calculating Real Interest Rates

If the nominal interest rate is currently 4.5% and the inflation rate is 6.2%, the real rate of interest would be:

In this example, the real interest rate is negative, meaning that the purchasing power of savings is actually falling despite earning interest. This situation encourages spending rather than saving.

Level of income

The relationship between income and consumption is perhaps the most fundamental determinant of spending patterns. This relationship was analysed by economist John Maynard Keynes during the 1930s Great Depression, leading to what is now called the Keynesian theory of consumption and saving.

Keynes identified what he called a "fundamental psychological law" that describes how people respond to changes in their income. He observed that as people's income increases, they do indeed consume more in absolute terms. However, consumption does not increase proportionally with income. Instead, consumption rises as a smaller fraction of total income as people become wealthier.

This insight has important implications. When income rises, people increase both their consumption and their saving, but the proportion of income saved tends to increase. This means that wealthier individuals typically save a larger proportion of their income than less wealthy individuals.

According to Keynesian analysis, this pattern of behaviour can lead to economic problems. If households collectively attempt to save more, this reduces aggregate demand in the economy. The resulting fall in spending means that other households earn less income (since one person's spending is another person's income). Through the multiplier effect, this can lead to a downward spiral of falling income and rising unemployment - a situation Keynes called the paradox of thrift. Attempting to save more individually can result in lower overall income and actually reduced total savings across the economy.

Expected future income

Whilst Keynes emphasised the importance of current income in determining consumption, later economists developed alternative theories that consider the role of expected future income. The most important of these is the life-cycle theory of consumption.

The life-cycle theory recognises that people's current income in any particular year may not accurately reflect their income over their entire lifetime. People plan their consumption and saving decisions based on their expected income over a much longer time period - potentially their entire working life and retirement.

Life-Cycle Patterns of Saving and Consumption

This theory helps explain several real-world patterns:

- Young people often save relatively little (or even borrow) because they expect their income to rise as their careers progress

- Middle-aged people typically save more heavily as they prepare for retirement

- Retired people draw down their savings to maintain consumption when their income from work ceases

The life-cycle theory emphasises that temporary fluctuations in yearly income generally have little effect on consumption patterns. People maintain relatively stable consumption levels by adjusting their saving in response to temporary income changes. Long-term changes in expected lifetime income, however, do significantly affect consumption decisions.

This approach is sometimes called the absolute income consumption theory because it focuses on the current level of income as the primary influence on consumption. However, pension contributions, life insurance purchases, and other forms of long-term saving clearly demonstrate that people do plan consumption based on expected future income over their entire life cycle.

Wealth

Beyond the flow of income, the stock of wealth that people own also significantly influences their consumption and saving decisions. In countries like the UK and USA, the two main forms of household wealth are property (houses) and financial assets (shares).

Rising house prices typically create a wealth effect that encourages increased consumption. When house prices rise, homeowners feel wealthier and may increase their spending whilst reducing their saving from current income. Additionally, rising property values generally increase the amount of borrowing that takes place in the economy. Homebuyers need larger mortgages to purchase houses, and this additional borrowing finances extra consumption - not just on houses themselves but also on furniture, home improvements, and other items.

Some homeowners engage in equity release - taking out larger mortgages on properties they already own to finance spending on other goods such as cars or holidays. In this context, 'equity' refers to wealth, and borrowing against home values reduces the amount of equity 'locked up' in people's houses.

Understanding Wealth Effects on Consumption

Rising asset prices create powerful psychological and economic effects:

- Rising house prices create optimism amongst property owners - a 'feel-good' factor that translates into increased consumer spending

- Conversely, falling house prices have the opposite effect, increasing uncertainty and encouraging precautionary saving through what might be called a 'feel-bad' factor

- Share prices can have similar effects, though this is less pronounced in the UK compared to the USA, where houses rather than shares are the main household wealth asset for most families

Historical examples illustrate these wealth effects. During summer 2007, a dramatic fall in share prices occurred in the USA and then spread to other countries including the UK. A year later, in 2008, falling house and share prices, combined with collapsing consumer and business confidence, triggered a recession in the USA that subsequently affected other countries including the UK. The share price collapse in early 2020 had different causes - it resulted from an anticipated economic slowdown due to the Covid-19 pandemic rather than a financial crisis. Share prices largely recovered their value over the following 18 months.

Consumer confidence

The state of consumer confidence closely links to people's expectations about their future income and wealth. When consumer optimism increases, households generally spend more and save less. Conversely, when optimism falls or pessimism grows, households reduce spending and increase saving.

Governments attempt to maintain and boost consumer confidence to prevent economic downturns. They do this by 'talking up' the economy and trying to enhance the credibility of government economic policies. When the government appears optimistic about future economic prospects and people believe this optimism is justified, consumer confidence tends to rise. However, if people believe the government is pursuing misguided policies, or if adverse economic shocks occur that the government cannot control, confidence can quickly evaporate.

Consumer confidence therefore represents a critical psychological factor in determining aggregate demand. Even when fundamental economic conditions remain stable, changes in confidence can drive significant variations in consumption patterns.

The availability of credit

Besides interest rates themselves, other aspects of monetary policy affect consumption, particularly the availability of credit. When credit is readily available, easily accessible, and relatively cheap (meaning interest rates are low and borrowing is straightforward for households and businesses), consumption tends to increase. People supplement their current income by borrowing through the credit created by the banking system. Conversely, tight monetary policy that restricts credit availability reduces consumption.

The financial crisis of 2007-2008 demonstrated this effect dramatically. The crisis originated in the USA sub-prime mortgage market, where banks had lent extensively to borrowers with poor credit histories who were at higher risk of defaulting on their debts. When these borrowers began failing to repay loans, banks were left holding large amounts of bad debt. This triggered a credit crunch - a severe shortage of funds in the credit market.

The Impact of Credit Crunches

During a credit crunch, interest rates rise and the supply of credit dries up as banks become reluctant to lend:

- Banks stop lending to each other out of fear that other banks might collapse, making them unable to recover their loans

- Banks become increasingly worried about their own solvency and therefore become more reluctant to lend money to customers

- This creates a severe contraction in economic activity as both consumption and investment fall

The consequences for the UK economy were severe. Northern Rock, a major British bank, had to be rescued by the UK government. Several years later, the government sold the bank to Virgin Money. The shortage of mortgages meant the property market stagnated, with houses changing hands less frequently and often selling for lower prices than would have occurred previously. This increased the amount of negative equity in the economy - situations where the value of a property falls below the outstanding mortgage debt.

Distribution of income

The pattern of income distribution within an economy also influences overall consumption and saving. Distribution of income refers to the spread of different incomes amongst individuals and different income groups across the economy.

Research consistently shows that wealthy people save a larger proportion of their income compared to those with lower incomes. This means that redistributing income from rich to poor households generally increases overall consumption and reduces total saving. Conversely, if income distribution becomes more unequal, with wealth concentrating amongst higher earners, aggregate saving tends to increase whilst consumption falls.

This relationship exists because poorer households typically spend almost all their income on necessities and have little left over for saving. Wealthier households, having already satisfied their basic needs, can afford to save substantial portions of their income.

Expectations of future inflation

Predicting how inflation expectations affect consumption is complex. However, fears of rising future prices generally create uncertainty that encourages precautionary saving and reduces consumption. People may postpone purchases if they expect prices to fall.

Conversely, expectations of rising prices can bring forward consumption decisions. If households expect inflation to increase, they may decide to purchase consumer durables such as cars or television sets immediately rather than waiting, thereby avoiding higher future prices. People may also borrow to finance house purchases if they expect property prices to appreciate faster than general inflation. In this situation, particularly when real interest rates are low or even negative, people often decide to buy property, land, and other physical assets such as art and antiques. These assets serve as a 'hedge' against inflation because they tend to maintain their value, unlike financial assets which may lose purchasing power during inflationary periods.

Understanding how consumer confidence and business confidence affect economic activity is essential for analysing aggregate demand. Consider carefully whether changes in confidence affect AD or AS (aggregate supply), and identify which specific component of aggregate demand or aggregate supply is influenced.

The determinants of savings

Saving represents a decision by people to postpone consumption. When households make decisions about spending on consumer goods, they simultaneously decide whether or not to save. Therefore, all the factors affecting consumption that we have examined also determine the level of saving. This relationship can be expressed through a simple equation:

This equation tells us that in a simplified economy (ignoring taxation and imports), people can only do two things with their income: spend it on consumption or save it. We can rearrange this equation to define saving:

This is the definition of saving: it is income that is not spent on consumption.

The personal savings ratio and household savings ratio

Economists and governments monitor saving behaviour through two key measures: the personal savings ratio and the household savings ratio.

The personal savings ratio measures the actual or realised saving of the personal sector as a proportion of total personal sector disposable income. It is calculated using this formula:

The household savings ratio works similarly but specifically measures households' realised saving as a proportion of their disposable income (including benefit payments) after deductions for tax have been made.

These ratios provide important information for policymakers about future aggregate demand. Since people's plans regarding future saving indicate their intended consumption, current savings behaviour helps predict future spending patterns. However, measuring people's plans accurately is difficult, so the personal savings ratio calculated for the most recent past period generally serves as an indicator of what people intend to do in future.

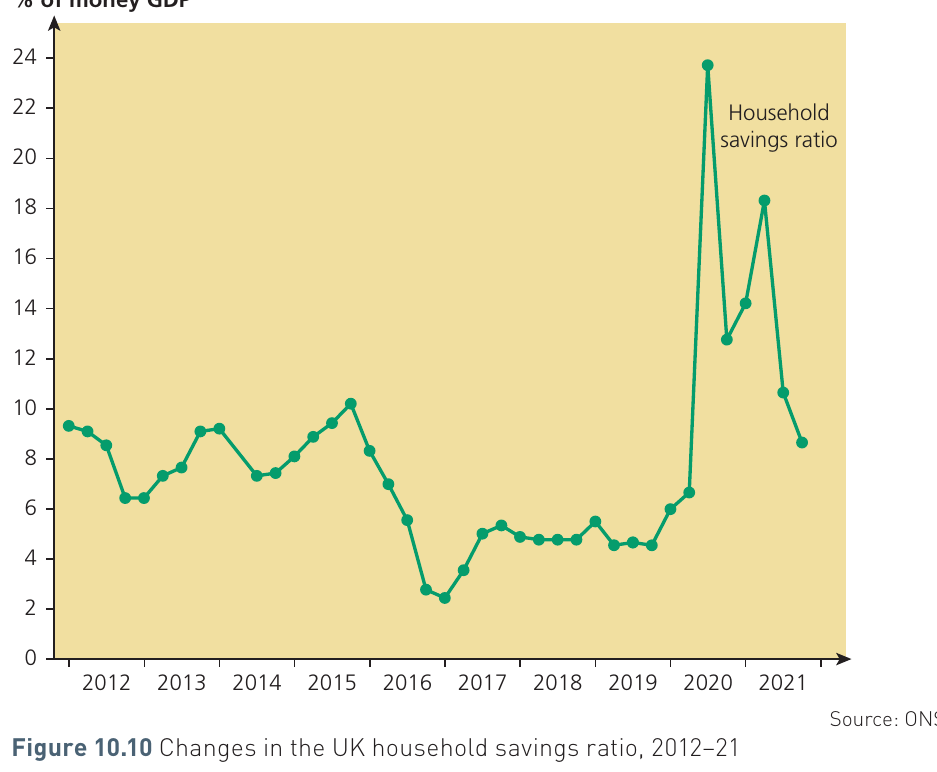

The UK savings ratio exhibited interesting patterns over recent decades. Between 2012 and 2016, it fluctuated between 7% and 10%. From 2016 onwards, it fell below 5% and remained around that level until 2020. The Covid-19 pandemic beginning in early 2020 was associated with a dramatic rise in the savings ratio. During the pandemic's main impact in 2020 and 2021, the savings ratio reached exceptionally high levels, peaking at over 20%.

Example: Pandemic Impact on Savings Behaviour

Several factors explain the surge in saving during the pandemic:

Increased Uncertainty: Increased uncertainty and insecurity about future jobs and income prospects undoubtedly encouraged precautionary saving.

Forced Reduction in Spending: A more obvious factor was the restrictions placed on people's shopping and lifestyle habits. Spending on holidays, restaurant meals, and pub visits was severely curtailed during the early part of the pandemic, meaning people saved much more of their surplus income than they normally would.

An important principle emerges from examining savings patterns: savings ratios generally rise during recessions unless offset by other factors such as increased borrowing to maintain spending levels and current living standards.

One key factor affecting household savings is uncertainty about the future. People who fear job losses or expect future income to fall are likely to save more for precautionary reasons. They want to build up a 'nest egg' - a sum of money held in reserve, often for a particular purpose - to protect themselves from potential future income losses.

This precautionary saving motive means that savings ratios tend to increase during economic downturns and periods of uncertainty, whilst falling during periods of economic growth and optimism when people feel more secure about their future income prospects.

The difference between saving and investment

Economists make a clear distinction between saving and investment, even though these terms are often used interchangeably in everyday conversation. Understanding this distinction is crucial for economic analysis.

Key Distinction: Saving vs Investment

Saving is simply income that is not spent on consumption. Households make saving decisions when they choose not to spend all their current income.

Investment, in economic terms, means spending by firms on capital goods such as machinery, office equipment, and factory buildings. This is called physical investment in new capital goods and should not be confused with financial investment, which refers to the demand for financial assets such as shares and bonds. Financial investment is actually a form of saving rather than investment in the economic sense.

As a simplification, economists often assume that households make saving decisions whilst firms make investment decisions. Firms invest when they purchase capital goods such as machinery. However, firms also save - for example, when they retain profits in bank accounts without immediately spending them.

It is important not to confuse investment with saving. In everyday language, people might say they are 'investing' their money when they put it in a savings account, but in economic analysis, investment and savings are quite different concepts. Investment refers to businesses spending on additions to their capital stock or inventory levels, whereas savings represents household disposable income that is not spent on consumption.

The determinants of investment

A country's total investment expenditure (gross investment) consists of two components:

- Replacement investment - spending to replace worn-out or obsolete capital, which maintains the size of the existing capital stock

- Net investment - spending that adds to the capital stock, thereby increasing the economy's productive potential

Along with technological progress, net investment serves as one of the main engines of economic growth. When firms invest in new capital goods, they create productive capacity that can generate returns extending many years into the future.

The future, however, is inherently uncertain, and the further ahead we look, the greater the uncertainty becomes. When firms decide whether to proceed with fixed investment projects - such as purchasing new machinery - they must form expectations about several key variables:

- Expected future sales revenue from the investment project

- Expected future production costs, including interest costs for borrowed funds used to finance the initial investment

- Future maintenance costs for the new capital equipment

Beyond interest rates, several other factors influence investment decisions by businesses.

The relative prices of capital and labour

When the price of capital goods rises (or when interest rates increase, making borrowing more expensive), firms tend to adopt more labour-intensive production methods over the long run, substituting workers for capital equipment. Conversely, when capital goods become relatively cheaper or interest rates fall, firms switch towards more capital-intensive production methods, replacing some workers with machinery. Therefore, decreases in the relative prices of capital goods encourage higher levels of investment.

The nature of technical progress

Technical progress can make machinery obsolete or outdated. When this occurs, the machine's business life becomes shorter than its technical life - meaning firms need to replace equipment before it physically wears out. A sudden burst of technical innovation may cause firms to replace capital goods early, well before the equipment reaches the end of its technical lifespan.

The adequacy of financial institutions in supplying investment funds

Many investments in fixed capital goods represent long-term commitments that yield expected income several years into the future. These investments may be difficult to finance because of inadequacies in the financial institutions that provide investment funding.

Banks have been criticised for favouring short-term investments whilst being reluctant to provide finance for long-term investment projects. Similarly, the stock market may favour short-termism over long-termism in company financing, although in recent years the growth of new lending methods to firms has provided an important source of medium- to longer-term finance.

Financial institutions function as intermediaries between savers (who provide funds) and investors (who use those funds). Their effectiveness in channelling savings into productive investment significantly affects the overall level of investment in an economy.

Government support

Governments provide funds to firms to finance investment projects, although simultaneously they tax firms through mechanisms such as corporation tax (a UK tax on company profits). When choosing whether to invest in particular projects or support certain investments, governments may be better at 'picking losers' than 'picking winners'.

Historically, UK governments have sometimes provided investment funds to rescue jobs in loss-making and uncompetitive industries that perhaps should have been allowed to decline. Government ministers and their civil servants may make poor investment decisions because, unlike entrepreneurs, they do not face the personal risk of bankruptcy resulting from bad decision-making.

Nevertheless, government support can play an important role in financing investment, particularly in strategic industries or during periods when private sector investment is insufficient to maintain full employment.

Capital is a stock concept (measured at a point in time), whilst investment represents a flow (measured over a period of time). The flow of investment expenditure over time adds to the total stock of capital at any given point in time.

The accelerator process

The accelerator process stems from a simple but important assumption that firms wish to maintain a relatively fixed ratio - known as the capital-output ratio - between the output they currently produce and their existing stock of fixed capital assets.

If output grows by a constant amount each year, firms invest exactly the same amount of new capital each year to enlarge their capital stock sufficiently to maintain the desired capital-output ratio. Year by year, the level of investment therefore remains constant. However, when the rate of growth of output accelerates (speeds up), investment increases as firms take action to enlarge their stock of capital to a level sufficient for maintaining the desired capital-output ratio. Conversely, when the rate of growth of output decelerates (slows down), investment declines.

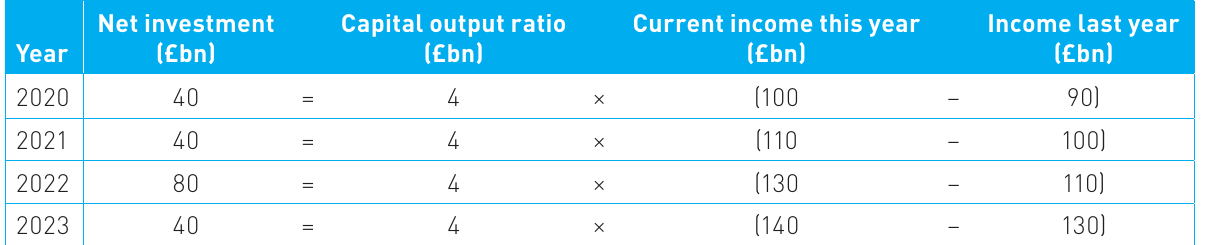

A numerical example of the accelerator

To illustrate the accelerator principle, consider an economy with a capital-output ratio of 4:1 (or simply 4). This means that 4 units of capital are required to produce 1 unit of output. Assume also that the level of current net investment in fixed capital depends on the change in income or output in the previous year. This relationship can be expressed as:

Where:

- = net investment

- = capital-output ratio

- = change in income or output

Or alternatively:

Where:

- = net investment this year

- = current national income

- = national income last year

- = capital-output ratio

The capital-output ratio, , is also known as the accelerator coefficient, or simply as the accelerator.

Worked Example: The Accelerator in Action

The table below illustrates a numerical example of how the accelerator operates:

Let's examine what happens in each year:

Between 2019 and 2020: National income grows by $10 billion (from $90bn to $100bn). Via the capital-output ratio of 4, this $10 billion income growth induces net investment of $40 billion in 2020. The capital stock increases by $40 billion to maintain the desired capital-output ratio at the higher level of income.

In 2021: Income continues to grow by $10 billion, so investment remains at $40 billion. The capital-output ratio stays constant.

In 2022: The situation changes. The growth rate of income speeds up (accelerates), doubling from $10 billion to $20 billion. Investment also doubles from $40 billion to $80 billion to maintain the capital-output ratio at 4. Thus, a $10 billion increase in income induces a $40 billion increase in investment.

In 2023: Although income continues growing, the growth rate falls back to $10 billion. Net investment consequently drops back to $40 billion - even though income is still rising.

This example demonstrates how the accelerator mechanism works. The key findings show that:

- When income grows by the same amount each year, net investment remains constant

- When income growth accelerates (speeds up), net investment increases

- When income growth decelerates (slows down), net investment declines

The accelerator principle therefore explains why investment in capital goods represents a more volatile or unstable component of aggregate demand compared to consumption. Relatively small changes in the rate of growth of income or output can cause quite large absolute rises and falls in investment levels.

Firms adjust their capital stock to maintain desired levels in relation to output. When these adjustments occur in response to changes in the rate of economic growth, the resulting investment fluctuations can significantly affect aggregate demand and contribute to economic instability.

Key Points to Remember:

-

Aggregate demand consists of four components: consumption (C), investment (I), government spending (G), and net exports (X-M). Understanding what determines C and I is essential for analysing macroeconomic performance.

-

The real interest rate matters more than the nominal rate: Calculate the real rate by subtracting inflation from the nominal rate. Negative real rates encourage spending; positive real rates encourage saving.

-

Keynesian theory emphasises current income: As income rises, people consume more in absolute terms but save a larger proportion of their income. This can lead to the paradox of thrift during economic downturns.

-

Wealth effects are powerful: Rising house and share prices create a 'feel-good' factor that boosts consumption. Falling asset prices have the opposite effect, increasing precautionary saving.

-

Don't confuse saving with investment: Saving is household income not spent on consumption (). Investment is business spending on capital goods. They are related but distinct concepts.

-

The accelerator makes investment volatile: Investment depends on the rate of change of income growth, not just the level of income. Small changes in growth rates can cause large swings in investment, making it an unstable component of aggregate demand.