Economic Methodology and the Economic Problem (AQA A-Level Economics): Revision Notes

Economic Methodology

Introduction

Economics explores how people make choices when resources are limited. It examines the economic behaviour of both individuals and groups, as well as the economic relationships that exist between them. The subject centres on a fundamental question: in a world where most resources are scarce or limited, how can people make the best decisions about what to produce, how to produce it, and who should benefit from production? This challenge of allocating scarce resources among competing uses forms the economic problem, which is central to the discipline.

The economic problem arises because human wants are unlimited while the resources available to satisfy those wants are scarce. This fundamental scarcity forces individuals, businesses, and governments to make choices about how to allocate resources efficiently.

Economics as a social science

What is social science?

Economics belongs to the family of social sciences, which study human society and the relationships between individuals within that society. Social science encompasses several related disciplines, each with its own focus.

Psychology examines the behaviour and mental processes of individuals. Sociology investigates the social relationships between people within the broader context of society. Economics, as its name suggests, studies the economic behaviour of both individuals and groups, along with the economic relationships that connect them.

Other social sciences include political science, as well as important elements of history and geography. What unites these disciplines is their focus on understanding human behaviour and social interactions.

Economic behaviour and relationships

To understand what economists study, consider two key examples that illustrate different levels of economic analysis:

Individual behaviour: An important area of economics called demand theory looks at consumer behaviour—how people behave when shopping. For instance, why do consumers generally purchase more strawberries when the price falls? This represents the study of individual economic choices.

Economic relationships: Economists also examine how consumers interact with firms or producers. Firms supply and sell the goods that consumers buy, and the place where these transactions occur is called a market. You may have encountered the phrase "supply and demand" and thought economics was primarily about this. While this is largely true, especially in the early stages of economic study, the discipline extends far beyond simple market transactions.

Economics operates at different levels of analysis. Microeconomics focuses on individual consumers and firms, while macroeconomics examines the economy as a whole, including unemployment, inflation, and economic growth.

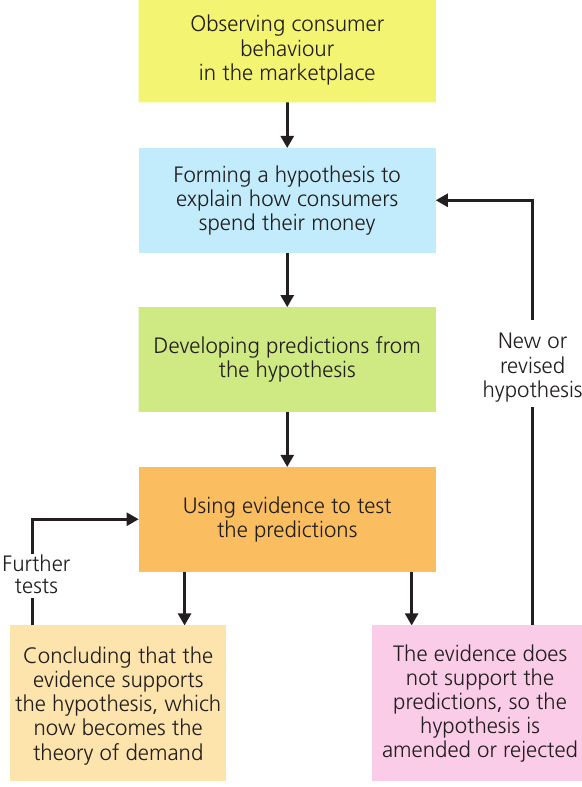

Economics and scientific methodology

The scientific method in economics

Economics employs scientific methodology to develop theories that explain real-world economic behaviour. The essentials of this approach can be understood through examining how demand theory develops.

Scientists begin by observing some aspect of the universe (in natural sciences) or some aspect of human behaviour (in social sciences). In demand theory, the starting point involves observing how individual consumers react to changes in the prices of goods and services they purchase.

From these observations, economists form a hypothesis—a tentative description or explanation of what has been observed. Hypothesis construction represents the second stage of the scientific method.

The third stage involves developing predictions from the hypothesis. These predictions describe human behaviour that should follow if the hypothesis is correct. For example, a hypothesis might predict that an individual will always respond to a lower price by demanding more of the good in question.

Testing and theory formation

The prediction is then tested against collected evidence about how individuals actually behave in the marketplace. This represents the fourth stage of the scientific method.

At this point, two outcomes are possible:

If the evidence supports the hypothesis, it survives the test and may become a theory. A theory differs from a hypothesis in that a hypothesis proposes an explanation for something, whilst a theory has been tested and survived that test.

However, surviving one test doesn't mean the theory is true in all circumstances. The hypothesis has simply survived the tests to which it has been exposed so far. It might not survive stronger tests that haven't yet been devised.

Key Distinction: A hypothesis is an untested explanation, while a theory has been tested and survived that test. However, even theories remain open to further testing and potential refutation—no theory is ever definitively "proven" in economics.

Falsification and refutation

Scientific method relies on the possibility of falsification or refutation of a hypothesis. When a hypothesis fails to survive testing, two things can happen:

The hypothesis may be rejected outright. For example, a hypothesis that consumers always respond to price cuts by demanding less would surely be rejected, as would the hypothesis that consumers always respond to a price cut by demanding more.

Alternatively, the hypothesis may be changed or diluted to make it less deterministic. This approach is common in economics. The hypothesis might be revised so that demand theory predicts that, in most but not all cases, consumers respond to price cuts by demanding more. When diluted in this way, the demand hypothesis survives the tests to which it is exposed and becomes the first "law" of demand.

Worked Example: Testing the Law of Demand

Step 1: Observe consumer behaviour Economists observe that when supermarkets reduce the price of strawberries from £3.00 to £2.00 per punnet, sales increase from 100 to 150 punnets per day.

Step 2: Form a hypothesis "Consumers will demand more strawberries when the price falls"

Step 3: Make predictions If this hypothesis is correct, whenever prices fall, quantity demanded should increase.

Step 4: Test with evidence Collect data from multiple supermarkets over several months. If 95% of price reductions lead to increased sales, the hypothesis survives the test and becomes part of demand theory.

Step 5: Refine the theory The refined theory states: "In most cases, consumers demand more of a good when its price falls, holding other factors constant."

Social sciences and natural sciences

Key differences

Economic theories often survive only by allowing a significant number of exceptions to their central predictions. According to critics, this turns theories into little more than generalisations with limited scientific application.

Some economists, like Ha-Joon Chang, argue that economics is not a science like biology. In his book Economics: The User's Guide, Chang contends that many economists believe, and tell others, that economics is a "value-free" science, like physics or chemistry.

However, Chang argues that economics is fundamentally political and moral in relation to choosing the best option. The particles and compounds studied by natural scientists don't hold political and moral views. In contrast, human beings who populate the economy do hold such views, and we cannot fully understand the economy without understanding politics and ethics.

Ha-Joon Chang's Critique:

Unlike the particles studied in physics or the cells studied in biology, human beings:

- Hold political and moral views

- Make decisions based on values and beliefs

- Cannot be studied in a truly "value-free" manner

- Respond to economic policies in unpredictable ways

This makes economics fundamentally different from natural sciences, despite economists' claims to scientific objectivity.

Positive and normative economics

Economists often respond to criticism that their subject is "soft" by arguing they are only concerned with positive economics, which they claim is based on quite strict use of scientific methodology.

Positive economics focuses on "what is" and "what will happen" if a course of action is taken or not taken. In contrast, normative economics is concerned with "what should or ought to be".

The difference between positive and normative statements

Understanding the distinction

A positive statement is a statement of fact that can be scientifically tested to see if it is correct or incorrect. If a positive statement doesn't pass the test, it is falsified.

A positive statement doesn't have to be true. For example, the statement that the Earth is flat is a positive statement. Although once believed to be true, the statement was falsified with the growth of scientific evidence.

The key point is that positive statements can in principle be tested and possibly falsified, whilst normative statements cannot.

A normative statement includes a value judgement and cannot be refuted purely by looking at the evidence. Normative statements are about value judgements and views. Because people have different views about what is right and wrong, normative statements cannot be scientifically tested.

Words such as ought, should, better and worse often provide clues that a statement is normative.

Quick Recognition Guide:

Positive statements:

- Can be tested with evidence

- Can be proven true or false

- Focus on "what is" or "what will be"

- Example: "Unemployment rose by 2% last year"

Normative statements:

- Contain value judgements

- Cannot be scientifically tested

- Often include words like "should", "ought", "better", "worse"

- Example: "The government should reduce unemployment"

Examples in economics

Consider the statement: "If the state pension were to be abolished, a million older people would die of hypothermia." This is a positive statement which could be tested, though few would want to conduct such a test.

By contrast, the statement "The state pension ought to be abolished because it is a waste of scarce resources" is normative, containing an implicit value judgement about the meaning of the word "waste".

Exam Tip:

Make sure you understand fully the difference between a positive and a normative statement. These concepts are often tested as multiple-choice questions in the exam, and you will need to be able to select which options are most clearly positive or normative statements.

Remember that normative statements often include clues that they are opinions, by using words or phrases such as "should", "ought to" or "must".

How value judgements influence economic decision making and policy

The role of value judgements

A value judgement is about whether something is desirable or not—whether we believe it is more desirable to study what is happening in the economy rather than what ought to happen. Economics necessarily requires that government ministers make value-based judgements when deciding on economic policies.

Despite this, economists often wrongly insist that the subject is value-judgement free.

Value judgements in practice

Most economics is concerned with what people ought to do. This is particularly true of government policy. Should the government try to reduce unemployment, control inflation and achieve a "fair" distribution of income and wealth? Most people probably think that all these objectives are desirable. However, they all fall within the remit of normative economics because they are about value judgements and views.

Value judgements are unavoidable in economic policy-making. When governments decide between competing objectives like controlling inflation versus reducing unemployment, they are making normative decisions based on their values about what matters most to society.

Make sure you understand fully how value judgements link to normative statements. Value judgements concern the desirability, or otherwise, of things. The fields of politics and economic policy making are based on value judgements. See if you can identify the normative statements made by politicians on news programmes.

Government decision-making

One particular chancellor of the exchequer (the UK government minister in overall charge of economic policy) once said:

"Rising unemployment and the recession have been the price that we have had to pay to get inflation down. That price is well worth paying."

Government ministers are often less frank than this, knowing that their political opponents and the media will immediately seize on the argument that those in power are uncaring and cynical people. However, the quote does serve to illustrate how decision-makers make value judgements when making economic policy decisions.

Government ministers occasionally make decisions on issues such as where a new airport should be located or whether high-speed trains are worthwhile. Before making decisions on issues like these, policy-makers know in advance that large groups of people will strongly oppose whatever decision is eventually made.

To try and avoid public hostility, government ministers usually create the illusion that the decision-making process is completely scientific and objective. To do this, they hire independent "experts" to provide advice. But the choice of expert in itself involves a value judgement.

The Illusion of Objectivity:

Government decision-making often appears scientific, but value judgements are embedded throughout the process:

- Choosing which experts to consult

- Deciding which costs and benefits to measure

- Determining how to value different outcomes

- Weighing the interests of different groups

Even "scientific" cost-benefit analyses require normative decisions about what to measure and how to measure it.

Do you choose someone you know in advance is sympathetic to the government's cause, or are you more willing to go for someone more impartial? Whichever way you go, the so-called scientific processes used by the "experts" to reach their conclusions may be full of value judgements.

A classic case involved weighing up the costs and benefits of the location of an additional London airport, which ultimately depended on putting money values on an hour of a business person's time, and an hour of a holidaymaker's time. It was quickly found that when different values were put on these, the airport location recommended by the experts would have "lost out" under different costing criteria.

The impact of moral and political judgements

Winners and losers

Whatever decision is eventually made in the course of framing government economic policy, there will always be winners who gain and losers who suffer as a result of the decision.

Governments often claim they have a moral right to make such decisions. They argue that their political manifesto published before the previous general election gives them the mandate, supported by the voters, to carry out their policies, regardless of the fact that among the electorate there will inevitably be some losers.

Policy Trade-offs:

Every economic policy decision creates winners and losers. For example:

- Raising the minimum wage helps low-paid workers but may cost some jobs

- Reducing inflation through higher interest rates helps savers but hurts borrowers

- Building new infrastructure improves transport but may harm local communities

Governments must make moral and political judgements about whose interests to prioritize.

Case example

One example is provided by former US president Donald Trump's decision in 2018 to implement a "zero tolerance" policy on illegal immigration into the USA. The policy involved splitting adult illegal migrants from their children and keeping them in wire cages along the US border with Mexico.

On humanitarian grounds the policy was so unpopular in the USA that it was quickly abandoned in a policy "U-turn", though the other parts of Trump's anti-immigrant policy remained in place.

Key Points to Remember:

-

Economics is a social science that studies choice and decision-making in a world with limited resources, focusing on economic behaviour and economic relationships

-

The scientific method in economics involves observation, forming hypotheses, developing predictions, and testing these predictions with evidence to develop theories

-

Positive statements can be tested scientifically to determine if they are correct or false, whilst normative statements involve value judgements that cannot be tested purely through evidence

-

Value judgements play a crucial role in economic policy-making, even when governments claim their decisions are purely scientific or objective

-

Government economic policy decisions inevitably create winners and losers, and these decisions are influenced by moral and political judgements as well as economic analysis

-

Words like "should", "ought", "better", and "worse" typically indicate normative statements