Nature and Purpose of Economic Activity (AQA A-Level Economics): Revision Notes

Nature and Purpose of Economic Activity

Introduction to economic activity

Economic activity exists primarily to produce goods and services that meet people's needs and wants. Understanding this fundamental purpose helps us analyse why economies function the way they do and how different economic systems attempt to satisfy their populations. When we study economics, we're examining how societies make decisions about production, distribution, and consumption of goods and services.

The three core aspects of economic activity are:

- Production: Creating goods and services

- Distribution: Allocating these goods and services among members of society

- Consumption: Using goods and services to satisfy needs and wants

Understanding how these three elements interact is fundamental to grasping how economies function.

Needs and wants

Understanding the difference

At the heart of economic activity lies a crucial distinction between needs and wants. These two concepts help us understand what drives production and consumption in any economy.

A need refers to something essential for human survival. Without meeting our needs, people cannot sustain life. Needs include fundamental requirements such as:

- Food to prevent starvation

- Clothing for protection

- Warmth to maintain body temperature

- Shelter to provide safety and protection from the elements

By contrast, a want describes something people would like to have but is not essential for survival. Wants make life more enjoyable or convenient but are not absolutely necessary. For example, whilst people need food to survive, they may want specific types of food like chocolate bars. Similarly, whilst shelter is a need, wanting a mobile phone is not essential for survival.

Exam Tip: The distinction between needs and wants isn't always clear-cut. Some goods can be both a need and a want depending on the context. For instance, food generally is a need, but luxury food items like expensive chocolates would be classified as wants. Focus on the survival element when making this distinction.

The concept of economic welfare

When economic activity successfully satisfies people's needs and wants, it improves economic welfare. This term describes the economic well-being of an individual, a group within society, or an entire economy. Economic welfare is a central concept throughout economics because it provides the benchmark by which economists judge whether policies are worth implementing.

The relationship between consumption and economic welfare is generally positive - consuming more goods and services usually improves economic welfare. However, this relationship has important nuances:

-

Short-term versus long-term welfare: Immediate happiness from consumption may come at the expense of long-term well-being. For example, consuming large quantities of food might provide short-term satisfaction but could lead to health problems that reduce long-term welfare.

-

Material versus non-material factors: Economic welfare extends beyond simply consuming goods and services. Human happiness and well-being also depend on quality-of-life factors such as relationships with family and friends, enjoying beautiful views, or having leisure time. These elements contribute significantly to welfare but don't necessarily involve market transactions.

Study Tip: Make sure you can explain the meaning of 'economic welfare' clearly. This concept appears throughout your studies and is fundamental to understanding how economists evaluate different policies and their impacts.

The key decisions of what and how to produce

Economic systems defined

Every society must answer fundamental questions about production: what should be produced, how should it be produced, and who should receive the goods and services produced? The way these decisions are made defines an economic system. An economic system represents the set of institutions within which a community organises economic activity and makes these crucial decisions.

Although scarcity is a universal problem affecting all human societies - from indigenous peoples in the Amazonian rainforest to wealthy nations like the United States - different economic systems have evolved to address this challenge in different ways. The primary distinction between economic systems lies in the mechanism used to allocate scarce resources to those who will eventually consume or use them.

Market economies

A market economy operates through the price mechanism within a system of markets. In this type of economy, goods and services are purchased through markets where prices adjust based on supply and demand. The price mechanism acts as a signalling system that communicates information between buyers and sellers, helping to allocate scarce resources without central coordination.

In a pure market economy, firms and other productive enterprises make decisions about what to produce based on prices and profit signals. Consumers express their preferences through their purchasing decisions, and these preferences guide production. The price mechanism coordinates the complex web of economic activities across the entire economy.

Command economies

A command economy (also called a planned economy) takes a fundamentally different approach. In this system, government officials or central planners allocate economic resources to firms and other productive enterprises. Rather than prices guiding production decisions, commands or directives from a central planning authority determine what to produce, how to produce it, and who receives the output.

A complete command economy, where all economic decisions are made by a central planning authority, represents a theoretical extreme. Such a system could only exist within a very rigid and controlled political framework because of the restrictions on individual decision-making it requires. Historical examples include the centrally planned economies of eastern Europe before the collapse of communist political systems around 1990.

These command economies faced significant challenges:

- Consumers often had to queue to obtain consumer goods

- Prices were fixed by planners rather than reflecting supply and demand

- Shortages resulted from mismatches between planned production and consumer demand

- The generally inferior quality of consumer goods, combined with shortages, contributed to the breakdown of command economies

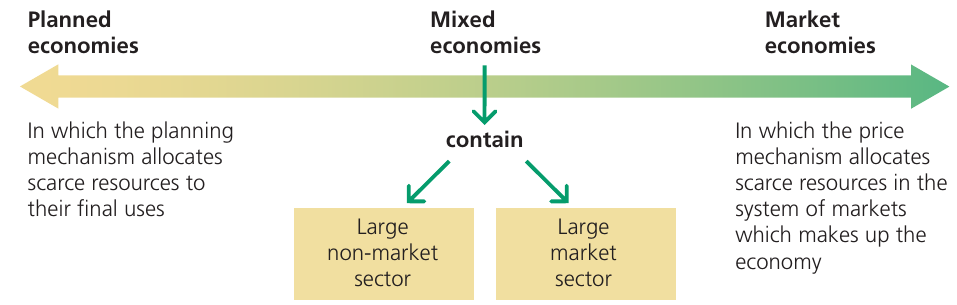

Mixed economies

In reality, most modern economies fall somewhere between these two extremes. A mixed economy contains both a large market sector where the price mechanism operates and a large non-market sector where the planning mechanism allocates resources. Many developed economies, particularly the UK, operate as mixed economies.

As the diagram illustrates, economic systems exist on a spectrum. At one end, planned economies rely primarily on the planning mechanism to allocate scarce resources to their final uses. At the other end, market economies use the price mechanism operating through market systems. Mixed economies occupy the middle ground, containing both mechanisms.

The balance between market and non-market sectors varies between countries and can change over time within the same country. Economic policies such as privatisation (selling state-owned assets to private owners), nationalisation (bringing private assets into public ownership), and deregulation (removing barriers to market entry) can shift an economy's position along this spectrum.

Real-world application: Allocating resources through different mechanisms

The price mechanism in practice

In a pure market economy, the price mechanism performs the central economic task of allocating scarce resources among competing uses through the markets that make up the economy. However, practical barriers often prevent this theoretical ideal from operating perfectly. Transport costs and lack of information can create barriers that separate or break up markets, preventing truly integrated market systems from developing.

Whilst some markets exist in particular geographical locations - such as a street market or the London Stock Exchange - many markets do not have a physical presence. Modern developments have transformed how markets operate:

- Goods can be transported more easily and at lower cost

- Information transmission via telephone and internet has improved dramatically

- Many markets, especially commodity and financial services markets, now function on a global or international basis

These technological advances have enabled markets to operate much more efficiently than in the past, though the ideal of a perfectly functioning market economy remains theoretical rather than practical.

The planning mechanism in practice

Similarly, a complete command economy where all decisions are made by a central planning authority issuing commands or directives to all households and producers represents a theoretical abstraction. No real-world economy can properly be described as a complete or pure planned economy.

Before the collapse of communist political systems around 1990, some countries in eastern Europe operated centrally planned economies. However, these were not pure command economies. Production was not restricted to consumption by planners - consumers often had to queue for consumer goods whose prices were fixed by planners, and shortages resulted. The generally inferior quality of consumer goods, together with the shortages, contributed to the breakdown of these command economies.

Some communist countries still exist, including the People's Republic of China, North Korea, Vietnam, and Cuba. However, with the exception until recently of North Korea, these countries have encouraged the growth of markets to varying extents. They maintain communist political systems but have moved away from being pure command economies. China, for instance, has become more capitalist than the UK and many mixed economies of western Europe. The term 'state capitalism' now describes much of China's economy.

Case study: The UK as a mixed economy

The UK provides an excellent example of how mixed economies evolve over time. The UK economy developed into a mixed economy after the Second World War ended in 1945, when important industries such as coal, rail, and steel were nationalised and taken into public ownership.

Case Study: The Evolution of the UK Mixed Economy

Phase 1: Post-War Expansion (1945-1970s)

Key developments included:

- The 1944 Education Act created state provision of education

- The creation of the National Health Service in 1948 established healthcare as a public service

For approximately 30 years after the Second World War (from the 1940s to the 1970s), the majority of UK citizens and major political parties agreed that the mixed economy was working well. A consensus existed around the belief that certain types of economic activity, particularly the production and distribution of consumer goods and services, were best suited to private enterprise and the market economy. However, people also accepted that utility industries such as gas and electricity should be nationalised, and that important services such as education and healthcare should be provided by government, outside the market, and financed through the tax system.

Phase 2: Economic Liberalisation (1980s onwards)

From about 1980 onwards, attitudes shifted. Many economists and politicians began arguing that the public and non-market sectors had become too large and were inefficient and wealth-consuming rather than wealth-creating. Critics argued that these sectors had become too dominant and that a concerted effort should be made to change the fundamental nature of the UK economy by increasing private ownership and market production.

Successive governments implemented policies that transformed the UK economy:

Privatisation: The sale of state-owned assets such as nationalised industries to private owners. This was often accompanied by marketisation (commercialisation), whereby prices began to be charged for goods and services that the state previously provided free of charge.

Deregulation: The removal of barriers to entry that prevented new firms from entering markets (explained further in Chapter 5), and the reduction of government bureaucracy and red tape from market operations.

These policies collectively became known as 'economic liberalisation'. The UK economy is now much closer to being a pure market and private enterprise economy than it was 45 years ago.

Exam Tip: When discussing mixed economies in essays, use the UK as a concrete example. Explain how the balance between market and non-market sectors can shift over time through government policies. This demonstrates your ability to apply theoretical concepts to real-world situations.

Remember: Key Points to Remember

-

Economic activity aims to satisfy needs and wants: Needs are essential for survival (food, shelter, clothing), whilst wants are desirable but not essential (mobile phones, luxury items).

-

Economic welfare measures well-being: This concept encompasses both material consumption and quality-of-life factors. It provides the benchmark for judging whether economic policies are worthwhile.

-

Economic systems differ in resource allocation: Market economies use the price mechanism, command economies use planning mechanisms, and mixed economies use both approaches.

-

Most modern economies are mixed: The balance between market and non-market sectors varies between countries and can change over time through policies like privatisation, nationalisation, and deregulation.

-

Real-world economies are complex: Neither pure market economies nor pure command economies exist in practice. All real economies contain elements of both market and planning mechanisms, though the balance differs significantly between countries.