Monopolistic Competition (AQA A-Level Economics): Revision Notes

Monopolistic Competition

What is monopolistic competition?

Monopolistic competition is a market structure that shares characteristics with both perfect competition and monopoly. This makes it one of the most common market structures in the real world, as many industries operate under these conditions.

Similarities with perfect competition

Monopolistic competition shares several important features with perfectly competitive markets:

- Many firms operate in the market – there are numerous businesses competing with each other, meaning no single firm dominates the industry

- Low barriers to entry and exit – in the long run, new firms can enter the market relatively easily if they see opportunities for profit, and existing firms can leave if they're making losses

- Normal profits in the long run – because new firms can enter when existing firms make abnormal (supernormal) profits, competition drives prices down until only normal profits remain

Similarities with monopoly

However, monopolistic competition also resembles monopoly in key ways:

- Downward-sloping demand curve – each firm faces its own demand curve that slopes downward. This occurs because each business produces a slightly different product through product differentiation

- Product differentiation – firms make their products distinct through features such as style, design, packaging, branding, and advertising. These goods are partial substitutes but not perfect substitutes for each other

- Some monopoly power – because of product differentiation, each firm has a degree of market power over its own product. If a firm raises its price, it won't lose all its customers (unlike in perfect competition) because of brand loyalty

- Marginal revenue below average revenue – each firm's marginal revenue (MR) curve lies below its average revenue (AR) curve, which is the demand curve for that firm's output

Common Misconception:

Students sometimes mistakenly believe that monopolistic competition is more similar to pure monopoly than to perfect competition. In reality, monopolistically competitive markets, characterised by many small to medium-sized firms competing by differentiating their products and services, are much closer to perfect competition in structure.

Short-run profit maximisation

In the short run, firms in monopolistic competition can make abnormal profits, just like monopolies. The profit-maximising behaviour follows the same rule that applies across all market structures: firms produce where marginal revenue equals marginal cost ().

The key features of short-run profit maximisation are:

- The demand (average revenue) curve represents demand for one firm's product, not the entire market's demand. Because other firms produce similar (though not identical) products, this demand curve is relatively elastic compared to a pure monopoly

- The profit-maximising output level () occurs where

- At this output level, the firm charges the price shown on its AR curve

- If price exceeds average total cost (), the firm makes abnormal profit, shown as a rectangular area between the price level and the ATC curve

Worked Example: Calculating Profit in Monopolistic Competition

Consider a barber's shop operating in monopolistic competition. The shop faces the following revenue and cost conditions:

| Number of haircuts per day | Price (£) | Total revenue (£) | Marginal revenue (£) | Total costs (£) | Marginal costs (£) |

|---|---|---|---|---|---|

| 0 | 22 | 0 | – | 10 | – |

| 1 | 20 | 20 | 20 | 14 | 4 |

| 2 | 18 | 36 | 16 | 20 | 6 |

| 3 | 16 | 48 | 12 | 32 | 12 |

| 4 | 14 | 56 | 8 | 48 | 16 |

| 5 | 12 | 60 | 4 | 66 | 18 |

Finding the profit-maximising output:

Profit maximisation occurs at 3 haircuts per day, where . At this output level:

- Price per haircut = £16

- Marginal revenue = £12

- Marginal cost = £12

- Total profit = Total revenue - Total costs = £48 - £32 = £16

Notice that the third haircut has zero effect on total profit (since ), but the firm still provides it because the first two haircuts generate profit that isn't eliminated by the third.

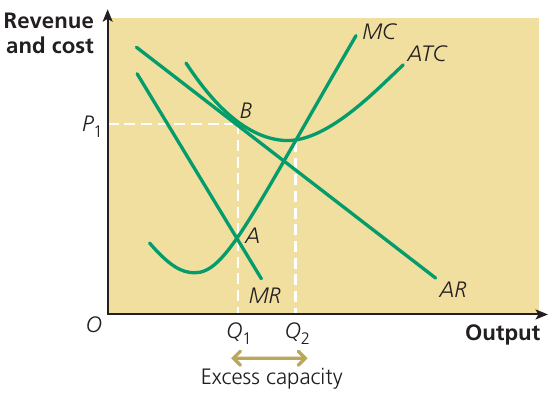

Long-run profit maximisation and excess capacity

The long-run equilibrium in monopolistic competition differs significantly from the short run due to the absence of barriers to entry. This is one of the most important aspects of this market structure.

The process of long-run adjustment

When existing firms make abnormal profits in the short run, these profits attract new entrants to the market. As new firms enter:

- The demand curve (AR) facing each established firm shifts leftward (or inward)

- This happens because customers switch to the new substitute products offered by new firms

- The leftward shift continues until the AR curve just touches (forms a tangent with) each firm's average total cost (ATC) curve

- At this point, abnormal profit disappears, and firms make only normal profit

Excess capacity and inefficiency

Long-run equilibrium occurs at point B, where the AR curve is tangent to the ATC curve. At this point, only normal profit is earned, meaning total revenue equals total costs ().

The profit-maximising output () occurs where , but this is not the productively efficient level of output. The productively efficient output () would occur at the lowest point of the ATC curve.

Excess Capacity and Productive Inefficiency

Excess capacity is measured as the difference between (the profit-maximising level of output) and (the productively efficient level). This represents productive inefficiency because:

- Firms operate below their most efficient scale of production

- Average costs are higher than they need to be

- Resources are not being used as efficiently as possible

Study tip: Remember that in all market structures – perfect competition, monopoly, and all types of imperfect competition – the profit-maximising level of output occurs where MR = MC. This is a fundamental principle in economics.

Evaluating monopolistic competition

Inefficiency compared to perfect competition

Monopolistic competition demonstrates both allocative and productive inefficiency when compared to perfect competition:

Allocative inefficiency:

- In monopolistic competition, price (P) is greater than marginal cost (MC)

- This means firms produce above the lowest point on their ATC curve

- Resources are not allocated to their most valued uses from society's perspective

Productive inefficiency:

- Firms produce at a level of output below the minimum point on their ATC curve

- This excess capacity means higher average costs than necessary

- In perfect competition, firms would be forced to produce at their most efficient scale (lowest point on ATC) to survive

The role of product differentiation

However, the inefficiency argument isn't straightforward. Product differentiation in monopolistic competition creates benefits that may offset these inefficiencies:

- Greater consumer choice – the range of differentiated products increases consumer options

- Meeting diverse preferences – different consumers value different product features, and product differentiation allows firms to cater to these varied tastes

Alternative Perspective: Consumer Welfare Benefits

The economist Kelvin Lancaster argued that the variety created by product differentiation can actually improve economic welfare. The gains to consumers from having more choice might exactly equal (or even exceed) the losses from producing fewer existing products at higher cost.

According to this view, monopolistic competition doesn't necessarily result in economic waste. Consumers may prefer the wider choice available in monopolistic competition to any improvement in productive efficiency that alternative market structures might provide.

Cotton price increase example

When analysing how firms respond to cost changes, consider this scenario: if cotton prices (a major input cost for clothing retailers) increase by 80%, we need to think about what happens to sales and profits.

Worked Example: Cost Shock Analysis

| Sales of clothing | Profits |

|---|---|

| A Constant | Fall |

| B Rise | Rise |

| C Fall | Constant |

| D Constant | Constant |

| E Fall | Fall |

Why option B is correct:

When input costs rise significantly, clothing retailers face higher production costs. To maintain profit margins, they raise prices. However, in monopolistic competition:

- The price increase leads to some customers switching to substitute products

- But brand loyalty and product differentiation mean the firm doesn't lose all customers

- Sales volume typically rises when firms adjust to new equilibrium prices

- Profits can be maintained or even increase if firms successfully pass costs to consumers

The other options are less likely because constant sales with rising costs would squeeze profits (eliminating A and D), and falling sales would typically accompany falling profits in this scenario (making E less optimal than B).

Advertising: barrier or promoter of competition?

Advertising plays a complex role in monopolistic competition. It can either promote competition or act as a barrier to entry, depending on the type and purpose of advertising.

Informative advertising

Informative Advertising and Competition

Informative advertising increases competition by providing useful information to consumers and producers about:

- Which goods and services are available to purchase

- The different products that various firms are producing

- Product features, specifications, and prices

This type of advertising helps markets function more efficiently by reducing information asymmetry and helping consumers make better-informed decisions.

Persuasive advertising

Persuasive advertising, by contrast, often reduces competition. This type of advertising:

- Makes the demand curve for a product less price elastic

- Creates "captive customers" who become unwilling to buy cheaper substitute goods

- Attempts to convince people that a product is a "must-have" item

- Focuses on emotional appeals rather than product information

- Emphasises how ownership or use of the product will improve self-worth or social image

- Provides little actual information about the product itself (such as price)

Large brands like Coca-Cola use persuasive advertising extensively. People who regularly drink Coca-Cola may become unwilling to switch to cheaper substitute drinks, even when the taste difference is minimal. This brand loyalty reduces price competition.

Saturation advertising as a barrier to entry

Saturation Advertising as a Barrier to Entry

Saturation advertising occurs when monopolies and large firms use extensive advertising to prevent small firms from entering the market. This works as a barrier to entry because:

- Small firms cannot afford the minimum level of advertising needed to persuade retailers to stock their products

- The mass advertising, brand imaging, and marketing strategies of large established firms effectively crowd out newcomers from the marketplace

- Supermarkets are often unwilling to stock goods produced by new entrants if these products aren't sufficiently advertised

This creates a situation where the advertising expenditure required for market entry becomes prohibitively expensive for small firms, protecting large incumbents from competition.

Price competition

Price competition occurs when firms reduce prices to sell more of their goods or services. Increased sales can happen in two interconnected ways:

- Market expansion – consumers switch from other markets where prices are higher and buy this particular good instead

- Market share capture – within the same market, consumers switch from buying similar goods from rival firms to buying from the firm that has reduced its price

Arguments about price competition

Some economists argue, though without strong evidence, that competitive firms dislike using price competition because it can lead to price wars. In such scenarios, all firms cut prices, ultimately only benefiting consumers while firms see reduced profit margins.

However, there are several ways firms engage in price competition, particularly in markets with just a few dominant firms:

- Special offer pricing – firms introduce temporary special offer prices on selected goods

- Discount pricing – certain goods are sold at discounted prices for limited periods

- Multi-buy offers – examples include "buy one, get one free" or "three for two" deals

- Predatory pricing – firms deliberately price below cost to drive competitors out of the market

These strategies are especially common in monopolistic competition and oligopolies, where firms have some market power but still face significant competition.

Synoptic Link:

The coverage of price competition in this chapter connects with earlier analysis of the role of prices in markets from your microeconomics studies. Price acts as both a signal and an incentive in market economies.

Non-price competition

In the absence of price competition, or alongside it, firms in imperfectly competitive markets (including monopolistic competition and oligopoly) often engage in various forms of non-price competition. These methods allow firms to gain market share or protect existing sales without cutting prices.

Forms of non-price competition

Marketing competition:

- Obtaining exclusive outlets (such as tied public houses where only one brewery's products are sold)

- Securing exclusive agreements with petrol stations for oil company products

- Creating distribution networks that competitors cannot easily access

Product-based competition:

- Persuasive advertising campaigns

- Product differentiation through unique features

- Brand imaging and brand building

- Distinctive packaging design

- Fashion and style elements

- Design innovation

Service-based competition:

- Quality competition (offering superior products or services)

- Point-of-sale service (helpful, knowledgeable staff)

- After-sales service (warranties, repairs, customer support)

- Customer experience improvements

These non-price methods are particularly important in monopolistic competition because:

- They reinforce product differentiation

- They build brand loyalty

- They can be more sustainable than price cuts

- They make demand curves less elastic

Key Points to Remember:

-

Monopolistic competition combines elements of both perfect competition and monopoly – it features many firms and low entry barriers like perfect competition, but also product differentiation and downward-sloping demand curves like monopoly

-

Product differentiation is the defining feature – firms compete by making their products slightly different through branding, design, packaging, and advertising, giving each firm some degree of market power

-

Profit maximisation occurs where MR = MC in both short and long run – but in the long run, the absence of entry barriers means new firms enter when abnormal profits exist, eventually eliminating these profits

-

Excess capacity demonstrates productive inefficiency – firms in monopolistic competition produce below their most efficient scale, operating at higher average costs than necessary

-

The welfare effects are ambiguous – while monopolistic competition is less efficient than perfect competition in terms of productive and allocative efficiency, the increased consumer choice from product variety may offset these losses