Cash flow forecasting and problems (AQA GCSE Business): Revision Notes

Cash flow forecasting and problems

What is cash flow forecasting?

Cash flow forecasting is a vital financial planning tool that helps businesses predict their future cash movements. A cash flow forecast estimates how much money will flow into and out of a business over a specific period, typically shown month by month. This forward-looking approach allows businesses to spot potential cash shortages before they happen and take action to prevent serious financial difficulties.

A cash flow forecast is essentially a prediction tool that shows when money will enter and leave your business, helping you avoid the dangerous situation of running out of cash unexpectedly.

The forecast works by estimating cash inflows (money coming in) and cash outflows (money going out) for each period. By calculating the difference between these figures, businesses can determine their net cash flow and predict their bank balance at the end of each month.

Understanding how cash flow forecasts work

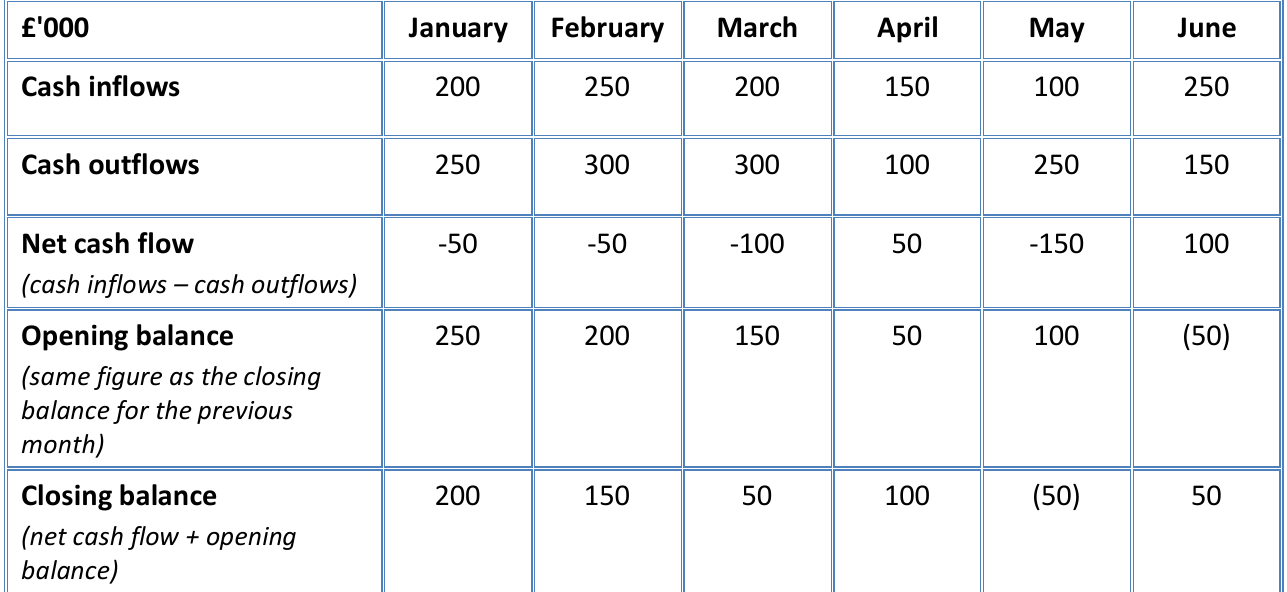

A typical cash flow forecast follows a standard structure that shows the financial position over several months. The forecast tracks several key components that work together to provide a complete picture of cash movement.

The forecast begins with cash inflows, which represent all the money expected to enter the business during each month. This might include sales revenue, loan receipts, or money from investors. Cash outflows show all the expected payments the business will make, such as supplier payments, wages, rent, and other operating expenses.

The forecast begins with cash inflows, which represent all the money expected to enter the business during each month. This might include sales revenue, loan receipts, or money from investors. Cash outflows show all the expected payments the business will make, such as supplier payments, wages, rent, and other operating expenses.

Key Cash Flow Calculations:

Net cash flow is calculated using the formula:

The closing balance is determined by:

Net cash flow is calculated by subtracting cash outflows from cash inflows. This figure can be positive (showing a cash surplus) or negative (indicating a cash deficit). The opening balance represents the amount of cash the business has at the start of each month, which becomes the closing balance from the previous month.

The closing balance is calculated by adding the net cash flow to the opening balance. This final figure shows whether the business will have a positive cash position or will be overdrawn.

When a business forecasts a negative closing balance, shown in brackets, it indicates potential cash flow problems that need urgent attention.

Why cash flow forecasting is essential

Cash flow forecasting serves as an early warning system for businesses, providing several critical benefits that help maintain financial stability and support business growth.

The primary advantage is identifying potential cash shortages well in advance. This predictive capability allows business owners to take preventive action rather than react to crisis situations. When managers can see months ahead where cash might run low, they can arrange additional funding or adjust their operations accordingly.

Think of cash flow forecasting like a weather forecast - it helps you prepare for storms before they hit, rather than getting caught in the rain without an umbrella.

Forecasting also ensures businesses can meet their payment obligations to suppliers and employees. Suppliers who don't receive payments on time may stop delivering goods or services, while late wage payments can damage employee morale and potentially lead to legal issues.

Another important benefit is monitoring customer payment patterns. By preparing forecasts, businesses can identify when customers are taking longer to pay their bills, allowing them to address credit control issues before they become serious problems.

The forecast also enables businesses to compare their actual performance against predictions. When significant differences emerge between forecasted and actual figures, management can investigate the causes and adjust their strategies accordingly.

External stakeholders, particularly banks and investors, often require regular cash flow forecasts to assess the business's financial health and repayment capability. This requirement becomes especially important when businesses have loans or are seeking additional funding.

Main causes of cash flow problems

Cash flow problems occur when businesses struggle to pay their debts as they fall due. These issues typically develop when cash outflows consistently exceed cash inflows, gradually depleting the business's cash reserves until serious difficulties arise.

| Factors | Why it causes a cash flow problem.. | |

|---|---|---|

| Low profits or (worse) losses | There is a direct link between low profits or losses and cash flow problems. Remember, most loss-making businesses eventually run out of cash | |

| Over-investmet in capacty | This happens when a business spends too much on machinery, equipment or premises. Factory equipment which is not being used does not generate revenue, so is often a waste of cash | |

| Too much stock | Holding too much inventory or stock ties up cash and there is an increased risk that these inventories become obsolete i.e. it cannot be sold and therefore cannot generate any cash inflows | |

| Allowing customers too much credit | Offering credit to customers, i.e. buy now and pay later, is a good way to build customer loyalty and long-term revenue, but late payment is a common problem and slow-paying customers put a strain on cash flow | |

| Overtrading | This occurs where a business expands too quickly, putting pressure on short- term finance. For example, a retail chain might try to open too many stores too quickly, before each starts to generate profits | |

| Seasonal demand | Predictable changes in seasonal demand create cash flow problems, but because they are expected, a business should be able to handle them |

Several factors commonly contribute to cash flow difficulties, each affecting the business's ability to maintain adequate cash balances.

1. Low profits or losses create a direct link to cash flow problems because businesses that consistently lose money will eventually exhaust their cash reserves. Even profitable businesses can face cash flow issues if their profits are insufficient to cover all their cash requirements.

Real-world Example: The Profit vs. Cash Flow Problem

A company might show £10,000 profit on paper but still face cash flow problems if:

- Customers owe £15,000 in unpaid invoices

- The business owes £8,000 to suppliers due immediately

- Despite being profitable, there's insufficient cash to pay immediate debts

2. Over-investment in capacity represents another significant cause of cash flow problems. When businesses spend heavily on machinery, equipment, or premises that don't immediately generate revenue, they tie up substantial amounts of cash without creating immediate returns. This situation often occurs when businesses expand too quickly without ensuring the new capacity will be profitable.

3. Holding excessive stock levels ties up cash that could be used elsewhere in the business. Stock represents money spent on inventory that hasn't yet generated sales revenue. Additionally, excess stock carries risks of obsolescence, where products become outdated or unsaleable, making the cash investment worthless.

Common Mistake to Avoid: Many businesses think that having lots of stock is always good for sales, but excessive stock ties up cash that could be used for other essential business activities like paying suppliers or wages.

4. Offering customers too much credit creates cash flow strain by delaying payment receipts. While credit terms can boost sales and customer loyalty, slow-paying customers put pressure on the business's cash position. The business has already incurred costs to produce and deliver goods but must wait to receive payment.

5. Overtrading occurs when businesses expand their operations too rapidly, putting excessive pressure on their short-term finance. For example, a retail chain might open multiple new stores simultaneously before each location becomes profitable, creating massive cash outflows without corresponding inflows.

6. Seasonal demand fluctuations create predictable but challenging cash flow patterns. Many businesses experience periods of low sales followed by busy seasons, requiring careful cash management to survive the quiet periods while preparing for peak demand.

Remember the "PILOTS" mnemonic for the six causes:

- Profits (low)

- Investment (over)

- Late payments

- Overtrading

- Too much stock

- Seasonal demand

Taking action to improve cash flow

The most effective approach to improving cash flow involves maintaining an accurate, up-to-date cash flow forecast and comparing it regularly with actual performance. This monitoring system helps identify cash flow issues early and enables prompt corrective action.

Several strategies can help businesses improve their cash flow position. Cost cutting represents the most direct and often most effective method of cash flow improvement. Every business can identify potential savings in non-essential expenses through careful analysis.

Historical Example: 2008-2009 Recession Response

During the 2008-2009 recession, many businesses demonstrated how effective cost cutting could be:

- Reducing non-essential travel and entertainment expenses

- Renegotiating supplier contracts for better terms

- Cutting back on temporary staff and overtime

- Reducing office space and other overheads

These actions immediately improved cash outflow positions and helped businesses survive the economic downturn.

Stock reduction involves decreasing the amount of cash tied up in inventory. Businesses can achieve this by:

- Ordering smaller quantities from suppliers more frequently

- Offering discounts to customers who purchase existing stock, preferably for immediate cash payment

Delaying payments to suppliers represents a commonly used but potentially risky strategy. By extending payment periods, businesses can reduce immediate cash outflows, providing time to generate sales revenue.

Warning about supplier payment delays: This approach risks damaging supplier relationships and may result in suppliers demanding immediate payment or refusing further credit. Use this strategy carefully and communicate openly with suppliers about temporary difficulties.

Reducing credit periods offered to customers can accelerate cash inflows by encouraging faster payment. However, customers may resist shorter payment terms, potentially requiring financial incentives such as early payment discounts to encourage compliance.

Cutting back on expansion plans can preserve cash by avoiding major capital expenditures. Many of the largest cash outflows occur during business expansion, such as opening new locations or adding production capacity. Delaying these investments can significantly improve short-term cash flow.

Additional financing options can provide temporary relief from cash flow problems:

- Arranging overdraft facilities for short-term shortfalls

- Securing loans from banks

- Raising additional capital from investors

- Restructuring operations or selling non-essential assets

- Issuing shares (though this may take time and may not suit all businesses)

Key Points to Remember:

- Cash flow forecasting predicts future cash movements to identify potential problems before they become serious

- Net cash flow = Cash inflows - Cash outflows, and Closing balance = Net cash flow + Opening balance

- The six main causes of cash flow problems are: low profits, over-investment, excess stock, customer credit issues, overtrading, and seasonal demand

- Cost cutting is often the most effective way to improve cash flow, followed by stock reduction and payment timing adjustments

- Regular monitoring and comparison of forecasts with actual performance enables early identification and correction of cash flow issues