Credit Cards (HSC SSCE Mathematics Standard): Revision Notes

Credit Cards

What are credit cards?

Credit cards allow you to purchase goods and services now and pay for them at a later date. This convenience comes with important financial considerations that you need to understand.

When you use a credit card, you're essentially borrowing money from the card issuer. The interest-free period is the time during which no interest is charged on your purchases. This period gives you an opportunity to pay off your purchases without incurring additional costs.

If you don't make payment when your statement is due, interest is charged from the original date of purchase. This is a critical distinction – the interest applies retroactively, not just from when you missed the payment.

How is credit card interest calculated?

Credit card interest uses compound interest that is calculated daily on your outstanding balance. This means:

- Interest is added to your balance every single day

- The next day's interest is calculated on the new, higher balance

- This creates a compounding effect that increases what you owe

The interest rates on credit cards are typically much higher than other types of loans and credit facilities, making them an expensive way to borrow money if you don't pay off your balance regularly.

Credit card interest formulas

To calculate credit card interest, you need to understand these key formulas:

Daily interest rate:

Future value formula:

Interest charged:

Key Variables:

- = Amount owing on the credit card (future value)

- = Principal (the purchases made plus any outstanding balance)

- = Rate of interest per compounding time period (as a decimal)

- = Number of compounding time periods

- = Interest (compound) charged on the outstanding balance

Worked example: Calculating the cost of using a credit card

Let's look at a practical example to see how these calculations work.

Worked Example: Calculating Credit Card Interest

Question: Samantha has a credit card with a compound interest rate of 18% p.a. and no interest-free period. She used her credit card to pay for clothing costing $280. She paid the credit card account 14 days later. What is the total amount she paid for the clothing, including interest?

Solution:

Step 1: Write the formula for compound interest.

Step 2: Substitute the values , and into the formula.

Step 3: Evaluate.

Step 4: Express the answer correct to two decimal places.

Step 5: Answer the question in words.

The clothing costs $281.94 including interest.

Note: Even though Samantha only waited 14 days to pay, she still incurred $1.94 in interest charges because there was no interest-free period on this card.

Understanding credit card statements

Credit card statements are issued monthly and provide a detailed record of your credit card activity. They serve as a ledger, which is a document that tracks your spending.

What information is on a credit card statement?

A typical credit card statement includes:

- Account number – your unique credit card identifier

- Opening balance – the amount you owed at the start of the statement period

- New charges – purchases made during the statement period

- Payments – money you paid towards your balance

- Refunds – any credits received

- Reward points – points earned and redeemed (if applicable)

- Payment due date – when payment must be received

- Minimum payment – the smallest amount you can pay to avoid late fees

- Closing balance – the total amount you owe at the end of the statement period

Consequences of missing the minimum payment

Critical Warning: Missing the Minimum Payment

If you fail to make the minimum payment by the due date, you may face:

- A late payment fee

- Interest charges on the unpaid amount

- Potential damage to your credit rating

These consequences can be expensive and create a cycle of increasing debt, so it's crucial to make at least the minimum payment on time.

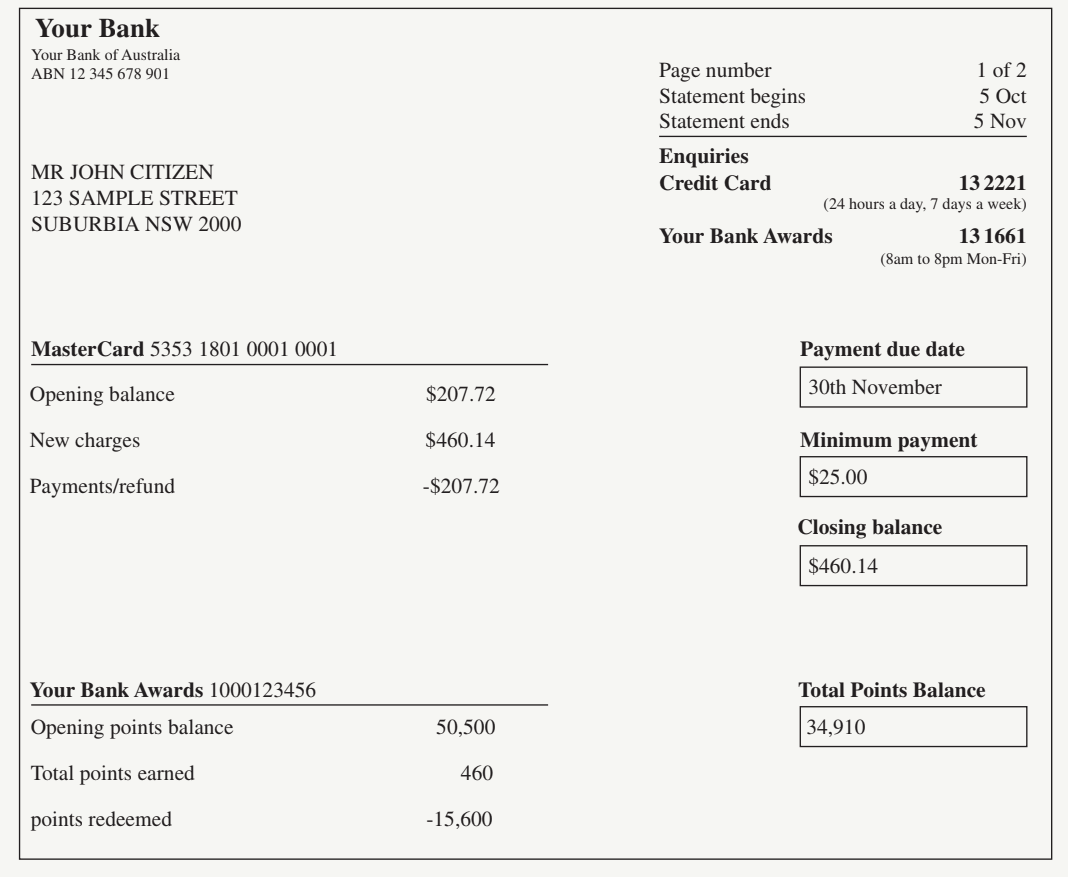

Worked example: Reading a credit card statement

Worked Example: Reading a Credit Card Statement

Question: Answer the following questions using the credit card statement:

a) What is the credit card account number?

b) What is the opening balance?

c) What is the payment due date?

d) What is the minimum payment?

e) What is the closing balance?

Solution:

a) Read the number after 'MasterCard': 5353 1801 0001 0001

b) Read 'Opening balance': $207.72

c) Read the box 'Payment due date': 30 November

d) Read the box 'Minimum payment': $25.00

e) Read the box 'Closing balance': $460.14

Exam Tip: When reading credit card statements, look for clearly labelled boxes and sections. The most important information is usually displayed prominently in designated areas.

Fees and charges for credit card usage

Banks and financial institutions charge various fees for maintaining and using a credit card account. Understanding these fees helps you make informed decisions about credit card usage.

Types of fees and charges

Annual card fee

- Charged yearly for maintaining your credit card account

- This fee applies whether you use the card or not

Interest charge

- Applied to retail purchases if you don't pay off your balance

- Also charged on amounts still owing from previous months

Late payment fee

- Charged when the minimum payment hasn't been received by the due date

- This is in addition to interest charges on the unpaid balance

Cash advances

- Fees for withdrawing cash directly from your credit card account

- Usually charged at a higher interest rate than purchases

Balance transfers

- Fees for moving your credit card balance to another account

- Often used when switching to a card with a lower interest rate

- May be held at a different financial institution

Worked example: Calculating fees and charges

Worked Example: Comparing Credit Card Balance Transfer

Question: Hilary has a debit of $6000 on a credit card with an interest rate of 14.75% p.a. that compounds daily. She decided to transfer the balance to a new card with a 0% balance transfer for 6 months. However, after 6 months the new card reverted to an interest rate of 19.75% p.a. that compounds daily. Is Hilary better off after 12 months?

Solution:

Old card calculation:

Step 1: Write the formula.

Step 2: Substitute , and into the formula.

Step 3: Evaluate correct to two decimal places.

New card calculation:

Step 4: Write the formula.

Step 5: Substitute , and (6 months only) into the formula.

Step 6: Evaluate correct to two decimal places.

Step 7: Calculate the saving by subtracting the future value of the new card from the old card.

Step 8: Write the answer in words.

Hilary is better off with the new card by $330.82.

Exam Tip: Balance transfer offers can save money in the short term, but always check what the interest rate reverts to after the promotional period ends. Calculate the total cost over the full period you expect to carry the balance.

Remember!

Key Points to Remember:

- Credit cards charge daily compound interest on outstanding balances, which can accumulate quickly if not paid off

- The interest-free period only applies if you pay your full balance by the due date

- Credit card interest rates are typically much higher than other types of loans

- Always make at least the minimum payment by the due date to avoid late fees and additional interest

- Balance transfers can save money, but watch out for what happens after promotional periods end

- Credit card statements serve as a ledger of your spending – review them carefully each month