Commercial Banks and Investment Banks (AQA A-Level Economics): Revision Notes

Commercial Banks and Investment Banks

Introduction to banking institutions

The banking sector consists of different types of banks, each serving distinct purposes in the financial system. The two main categories are commercial banks (also known as retail banks or high street banks) and investment banks. Although both aim to generate profits for their owners, they operate in very different ways and serve different customers.

The Bank of England, as the country's central bank, is an exception to the profit-making objective. Its primary aims are to oversee the financial system and implement monetary policy.

Commercial banks

What is a commercial bank?

A commercial bank is a financial institution that earns profits by providing banking services to its customers. These banks are also commonly referred to as retail banks or high street banks.

Commercial banks serve ordinary members of the general public and businesses. Their customers include individuals, families, and companies who need everyday banking services.

Examples of commercial banks

Major commercial banks operating in different countries include:

- United Kingdom: Barclays, HSBC

- Germany: Deutsche Bank

- France: Crédit Agricole

- Switzerland: Credit Suisse

- United States: Citibank

Historical development

To attract customers, commercial banks traditionally built extensive networks of branch banks located on high streets and in shopping centres. However, the development of electronic internet banking and increased customer access to accounts through computers and smartphones has changed this model significantly. Most large commercial banks have been closing many of their branch banks as customers increasingly manage their accounts online.

Key functions of commercial banks

Commercial banks are commercially run financial institutions that perform two primary functions:

- Accept deposits from the general public that can be transferred by cheque, debit card, or through online transfers

- Create deposits which are lent to customers who wish to borrow money from their bank

These two functions are interconnected. When a bank makes a loan (creates credit), it simultaneously creates a new deposit in the borrower's account.

Investment banks

What is an investment bank?

An investment bank operates very differently from a commercial bank. Investment banks do not generally accept deposits from ordinary members of the general public.

Until fairly recently, investment banks were commonly known as merchant banks. Before the internet era, investment banks were clustered in the square mile of the City of London. This geographical concentration existed because investment banks do not generally deal directly with ordinary members of the general public, so they do not require expensive branch networks.

Activities and functions of investment banks

Investment banks engage in several key activities:

Financial advisory work:

- Advising private companies on how to become public companies by floating on the stock market (making shares available to the public to buy or sell)

- Advising public companies on how to buy up other companies

- Underwriting share issues

Underwriting services:

Investment banks help companies, other financial institutions, and government agencies raise finance by selling shares or bonds to investors and securing against risks. They do this through underwriting share issues. In return for substantial fees, investment banks guarantee to buy up all unsold shares in the event of an unsuccessful launch of a new share issue.

Over past decades, investment banks have earned large amounts of money, paid ultimately by taxpayers, through underwriting the privatisation of previously state-owned businesses. Most recently, they helped underwrite the Royal Mail flotation in 2013, with the final 30% of share capital sold by the government in 2015.

Trading activities:

Investment banks also trade on their own behalf in shares, bonds, and other financial assets. This trade takes place with other investment banks and with other financial institutions such as insurance companies and pension funds.

Major global investment banks

Investment banks are essentially global banks. The largest trade in financial assets which are greater in size than the GDPs of most of the world's countries.

Many of the largest investment banks have been formed through the merger of a retail bank and a previously smaller independent investment bank. A notable example is S.G. Warburg & Co., a London-based investment bank. Warburg was listed on the London Stock Exchange and was once a constituent of the FTSE 100 index (one of the biggest 100 public limited companies listed on the London Stock Exchange). The bank was acquired by the Swiss Bank Corporation in 1995 and ultimately became part of another Swiss investment bank, UBS.

Only two of the 'big three' US investment banks, J.P. Morgan and Goldman Sachs, have remained fully independent of the retail banking sector.

Global presence and contribution to the UK economy

Although investment banks have headquarters in various countries including the USA, the UK, France, Germany, Switzerland, and Japan, they also have offices in all the world's major financial centres. This includes the City of London and 'City-East' (Canary Wharf to the east of the City proper).

All of the large global investment banks maintain a presence in London. These banks therefore contribute to UK economic activity and help support the efficient functioning of the financial system. However, investment banks also bring risks to the UK financial system.

Investment banks and systemic risk

Understanding systemic risk

Many banks carry out both retail and investment banking activities. This led to problems that appeared in the financial crisis that hit the financial system in 2007.

Systemic risk refers to the risk of a breakdown of the entire banking system rather than simply the failure of individual banks. This is a cascading failure caused by inter-linkages in the financial system, which may result in a severe downturn in the whole economy.

Systemic risk versus one-off risks

It is important to distinguish between systemic and one-off risks. In contrast to a one-off shock which affects only a single bank without rippling into the rest of the banking system, systemic risk affects the entire banking system and other financial institutions as well. The consequences of a systemic financial crisis can be devastating because of the role that banks and finance play in the wider economy.

Regulatory response: ring fencing

Largely in response to these difficulties, national banking authorities are introducing regulations designed to separate 'high-street' and investment banking activities.

Following the publication of the final version of the Vickers Report into the activities of the UK banking sector in 2011, the retail banking activities of banks operating in the UK must be ring fenced (separated) from their investment banking activities. This became law on 1 January 2019.

Ring fencing is an internal device implemented by the bank to separate different parts of a bank's activities. Without ring fencing, an investment bank's mergers and acquisitions (M&A) department may acquire 'inside knowledge' about a company it is advising. This 'inside knowledge' could be very useful to the bank's own trading in the company's shares. An effective ring fence, which is also known as a firewall, prevents this from happening.

How banks create credit and deposits

Understanding bank deposits

In contrast to cash, which is tangible and can be seen and touched, bank deposits are intangible. Customers only 'see' a bank deposit when reading the statement of a bank account, or when viewing the electronic display in a cash-dispensing machine.

Bank deposits are the main form of money, and most transactions are paid for by transferring bank deposits from one account to another. Cash (notes and coins) is a relatively small part of the total stock of money. According to the New Economics Foundation's 2014 publication "Where Does Money Come From?", only 2.6% of the broad money total was actually cash, whilst 97.4% took the form of bank and building society deposits, together with other liquid assets.

The concept of credit

Credit is created when a bank makes a loan. The loan results in the creation of an advance, which is an asset on the bank's balance sheet, and a deposit, which is a liability of the bank.

Illustrating credit creation: a simple example

To understand how bank deposits are created, consider the following scenario:

Suppose we write our signatures on a scrap of paper with the words: "We promise to pay the bearer $100." We then give this promissory note ('I owe you') and ask someone to go to a shop and buy $100 worth of goods. When the time comes to pay, the scrap of paper must be given to the shop assistant.

In real life, shops almost always refuse to accept such an 'I owe you.' But suppose the shop did accept our scrap of paper, believing it could then use the note to buy goods from its suppliers. Our 'I owe you' note would have become money.

Ordinary individuals cannot generally create money in this manner. However, banks can. If the promissory note were headed 'Lloyds Bank promises to pay the bearer $100', as long as people believe that Lloyds will honour its promise, the 'I owe you' can function as money.

Credit creation in a monopoly banking system

Setting up the model

The UK banking system, and indeed that of most other countries, is a 'multi-bank' system in which there are a large number of commercial banks competing for business in pursuit of profit. However, to illustrate the credit and bank deposit creating process, we first examine how credit would be created if there was just one commercial bank in the system. This is often called a 'monopoly' banking system.

Basic assumptions

We make three key assumptions:

- There is only one bank in the economy (it has the 'monopoly')

- The bank possesses only one asset, namely cash, which it uses to meet any cash withdrawals (and running down of deposits) by customers

- The bank decides that, to maintain confidence and always be able to meet its customers' desire to withdraw cash from their accounts, it must always possess cash equal to 10% of total customer deposits

The initial deposit

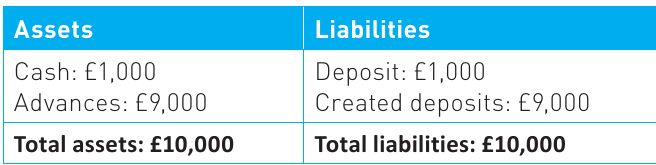

Suppose a member of the general public deposits $1,000 cash in the bank. From the bank's point of view, both its assets and its liabilities increase by $1,000. The cash is the bank's asset, but the $1,000 deposit credited in the customer's name is the bank's liability, since the bank is liable to honour any cash withdrawals made by the customer.

Creating new deposits through lending

At this stage, all the bank's deposit liabilities are backed with cash (the bank's cash ratio is 100%). If this remained the position, the 'bank' would not be a bank at all, but a safe-deposit institution.

However, other customers may need to borrow from the bank. Provided they are creditworthy (they can be relied on to pay back money), the 10% cash ratio the bank has chosen means that the bank can lend exactly $9,000 to these customers.

This may take the form of an interest-earning advance on the assets side of the bank's balance sheet, matched by a $9,000 created deposit on the liabilities side:

Both the customer who made the initial deposit of $1,000 and the customers who received the advances can make payments equal to $10,000 in total using their deposits. The initial $1,000 cash deposit has enabled total deposits to be increased to $10,000.

Cash ratios in reality

In the real-world banking system, the cash ratio is much lower than 10% — it is closer to 5%. However, for illustrative purposes, we use the assumption of a 10% cash ratio as it makes the calculations simpler.

Credit creation in a multi-bank banking system

The real-world system

The real-world banking system contains more than one bank. Some of the biggest in the UK are HSBC, Barclays, Lloyds, and NatWest. We call this a 'multi-bank' banking system.

When we drop the simplification of a monopoly bank and assume a multi-bank system similar to that in the UK, the general conclusions of our simple 'monopoly' model still hold. If the increase in cash deposits is spread over all the banks, deposits can expand to $10,000, provided every bank in the system is prepared to lend to the full extent that its chosen cash ratio allows.

Interbank payments

However, if only one bank is prepared to create deposits to the full, it will begin to face demands for cash that it cannot meet. This happens when the bank's customers make payments into the accounts of customers of other banks, losing some of its cash reserves to other banks.

If all banks are prepared to expand deposits to the full, payments to customers of other banks will tend to cancel out. The banking system as a whole can expand deposits to $10,000, though some banks may gain business at the expense of others.

Constraints on credit creation

The models illustrate how the supply of reserve assets, such as cash, available to the banks can limit their ability to create deposits. However, the banks' ability to create credit is also limited by their need to have sufficient capital.

Since the financial crisis, central banks have imposed larger minimum required capital ratios on the banks, and this has restricted their ability to lend.

Banks holding more capital are less likely to become insolvent if there is a fall in the value of their assets — for example, as a result of customers being unable to repay the money they have borrowed. This is the main reason why capital ratios are imposed.

The central bank acts as a 'lender of last resort' to the banking system. To maintain confidence in the banks and prevent a 'run' on an individual bank, the central bank is always prepared to supply cash at a price to a bank threatened by a sudden deposit withdrawal. However, this does not mean that the central bank will bail out a bank which has made bad investments and is making losses.

Worked example: calculating deposit expansion

Worked Example: Calculating Deposit Expansion

A customer makes a cash deposit of $100,000 in his bank. All the retail banks in the economy choose to keep 5% of their total assets in cash.

Calculate the maximum level of total bank deposits resulting from the deposit of $100,000 into the banking system.

Solution:

A 5% cash ratio means that cash equals 0.05 of total deposits.

Answer: $2 million

As all banks in the banking system have chosen to operate a 5% cash ratio, assuming that the banking system retains the extra cash, total bank deposits can increase to $2 million following a deposit of $100,000 into the system. Notice that $100,000 is 5% of $2 million.

The structure of a retail bank's balance sheet

Assets and liabilities

So far we have assumed that retail banks possess just two assets: cash and advances to customers. However, banks possess a range of other assets.

Understanding reserve assets

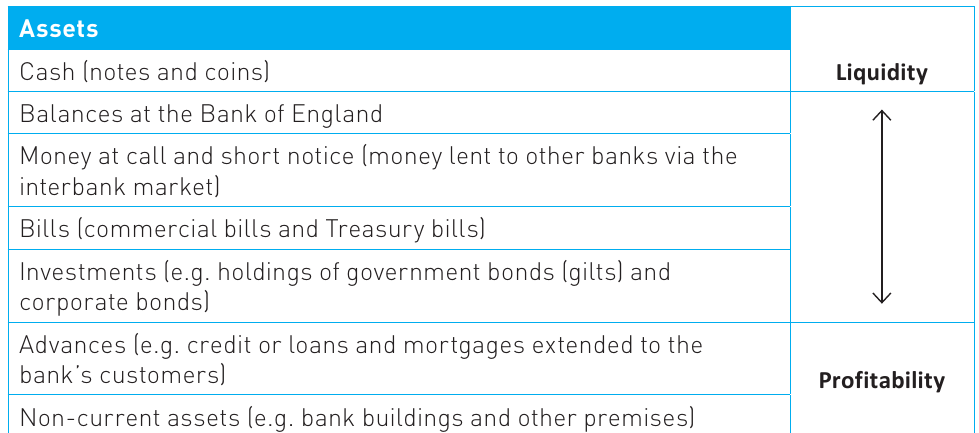

Banks possess reserve assets or liquid assets other than the cash we have already discussed. Nevertheless, cash is the most important reserve asset and source of liquidity in the banking system.

The purpose of reserve assets is to allow banks to maintain liquidity and confidence and to meet any likely demands by customers for cash. In the event of a withdrawal of cash by customers, a bank must be able to turn reserve assets into cash without suffering a capital loss.

The risk of illiquidity

To be as profitable as possible, a greedy or imprudent bank might be tempted to reduce cash and other liquid assets to a minimum. However, this would create the risk of illiquidity and a loss of confidence among customers in the bank's ability to meet its liabilities.

As was the case when the Northern Rock bank collapsed in 2007, a 'run' on the bank could then occur, leading to a crash. A 'run' on the bank occurs when people believe that a bank is going to run out of cash and a panic ensues, causing customers to attempt to withdraw all they can before it does run out of cash.

Categories of bank assets

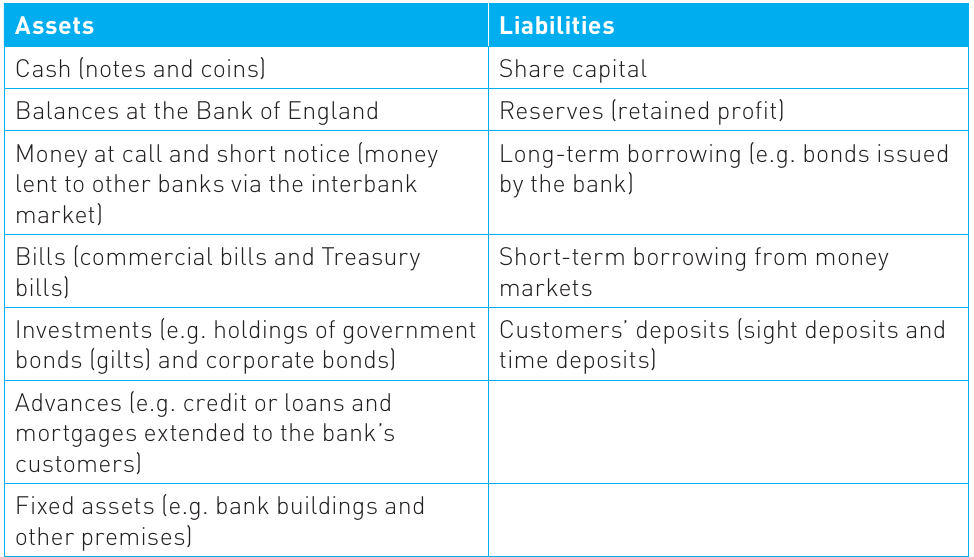

The main categories of assets on a bank's balance sheet include:

1. Cash (notes and coins)

The most liquid asset but earns no interest.

2. Balances at the Bank of England

Banks keep balances at the Bank of England. Just as members of the general public make payments to each other by shifting ownership of bank deposits from the payer to the payee, retail banks settle debts between themselves in the same way. To do this, all the banks keep balances at the Bank of England. As a bank can instantly withdraw cash by running down its balance at the Bank of England, the balance is as liquid as cash.

3. Money at call and short notice (interbank market)

If a retail bank is temporarily short of cash, which it needs to meet customers' demand for cash over the counter or via a cash machine, it can borrow cash from other banks.

The traditional name for this is 'money borrowed at call and short notice.' Money borrowed in this way which must be paid back tomorrow (overnight money) is an example of money at call. Money borrowed for a rather longer period, say a month, is money at short notice.

These days, the market on which money is lent and borrowed in this way is called the inter-bank money market. The money lent in this way is the third asset in the balance sheet. Since banks borrow from, as well as lend to, other banks, money at call and short notice figures on both sides of a bank's balance sheet — as a liability (money borrowed) as well as an asset (money lent). Since the money lent can quickly be turned into cash, money at call and short notice is a highly liquid asset for the bank making the loan to other banks.

4. Bills (commercial bills and Treasury bills)

Retail banks like to hold a portfolio of commercial bills and Treasury bills as a liquid asset. When first issued and sold to the retail banks (by investment banks on behalf of businesses in the case of commercial bills, and by the Debt Management Office (DMO) on behalf of the government in the case of Treasury bills), bills typically have a life of three months before they mature.

A bank purchasing a newly issued bill makes a profit because it buys the bill at a discount — the purchase price is lower than the bill's maturity value. The bank earns the bill's discount rate, which is, in effect, the interest rate on the bill. The money market on which commercial and Treasury bills are bought and sold is called the discount market.

At any point in time, retail banks possess a portfolio of bills, some of which mature today or tomorrow, some in a week's time, and some in three months' time. From the bank's point of view, its bill portfolio provides it with liquid assets which are nevertheless profitable.

5. Investments (government bonds and corporate bonds)

As shares never mature and might have to be sold second hand on a falling capital market, retail banks do not generally invest in company shares or equities. However, they do invest in corporate bonds issued by private-sector PLCs, and even more so in government bonds (gilt-edged securities or gilts).

When first issued and sold, most gilts have a life of anything up to 50 years before they mature. However, because gilts are issued by the government and their maturity value and yearly interest payment (the gilt's coupon) are guaranteed, banks usually regard gilts as absolutely safe and profitable investments.

For the banks which own them, gilts are profitable, but illiquid in the sense that the banks may suffer capital losses if they decide to sell the gilts on a falling second-hand market. From the banks' point of view, the risk of capital loss is greater for gilts than for bills.

6. Advances (credit, loans, and mortgages)

These are loans extended to the bank's customers. Advances are the most profitable but least liquid assets for banks.

7. Non-current assets (fixed assets)

These include bank buildings and other premises owned by the bank.

The liquidity-profitability trade-off

Understanding the trade-off

If a bank kept all its assets in the form of cash, it would not really be a bank at all, but a safe-deposit institution. The bank's profits, if it earned any, would come solely from the fees it charged customers for guarding their valuables. The bank's cash would be completely liquid, but not very profitable.

To make a profit, a bank has to make its cash go to work. Essentially, cash acts as 'high-powered' money which allows the banks to make advances to customers, creating deposits and increasing the total stock of money.

The rates of interest that retail banks charge their customers on the advances granted to them are a major source of the banks' profits. Banks might be tempted to create far too many potentially profitable advances — this would be unwise if they possess insufficient cash to meet customers' possible cash withdrawals. These banks would be operating on too low a ratio of cash and other liquid assets to the advances they have created. If a run on the banks occurred, the banks would crash.

Balancing liquidity and profitability

Profitability is the state or condition of yielding a financial profit or gain.

Prudent (cautious) retail banking requires banks to operate on ratios of cash and other liquid assets to advances that maintain customers' confidence in the bank, while generating acceptable profits for the bank.

In other words, prudent banking involves trading off liquidity against profitability.

Taking the UK retail banking system as a whole, over the years, cash ratios fell below 5%. Some argue that this was a major factor in the failure of the Northern Rock and Bradford and Bingley banks during the financial crisis of 2007–08, and in the government's need to rescue much larger banks such as Lloyds TSB. Since the financial crisis, cash ratios have been again towards 5%.

Potential conflicts: liquidity, profitability, and security

The security dimension

Besides trading off between profitability and liquidity, banks also have to make choices with regard to the security of their assets.

Security refers to secured loans, such as mortgage loans secured against the value of property, which are less risky for banks than unsecured loans.

Risk and return in lending

The profitability for banks of loans granted to customers depends to a significant extent on the degree of risk attached to the loans. Non-secured loans are risky because, if a customer defaults on the loan, the bank cannot recover any money. Banks therefore charge higher interest rates, and make more profit, on unsecured than on secured loans.

Mortgage loans granted to house purchasers are secured loans. If the borrower is unable to repay the loan or interest on the loan, the bank or building society which provided the mortgage can repossess the property which secures the loan. This reduces the risk involved in granting long-term mortgage loans.

Summary of the three-way trade-off

Banks must carefully balance three competing objectives:

- Liquidity: maintaining sufficient liquid assets to meet customer demands for cash

- Profitability: earning returns on assets to generate profits

- Security: managing risk by choosing appropriate types of loans and investments

This requires careful judgement and prudent management to ensure the bank remains stable whilst still generating profits for its owners.

Key Points to Remember:

-

Commercial banks (retail banks or high street banks) accept deposits from the general public and provide lending services, making profits by providing banking services to customers.

-

Investment banks do not generally accept deposits from the public but instead provide advisory services, underwrite share issues, and trade financial assets on their own behalf.

-

Banks create credit when they make loans, simultaneously creating both an advance (asset) and a deposit (liability) on their balance sheet, thus expanding the money supply.

-

The banking system's ability to create credit is constrained by cash ratios (liquidity requirements) and capital requirements imposed by regulators.

-

Banks must navigate the liquidity-profitability trade-off: cash is the most liquid asset but earns no profit, whilst advances are the most profitable but least liquid assets.

-

Systemic risk refers to the risk of a breakdown of the entire financial system rather than just individual bank failures, which led to regulations requiring ring fencing to separate retail and investment banking activities.

-

A bank's balance sheet contains various assets (cash, Bank of England balances, interbank loans, bills, investments, advances, and fixed assets) and liabilities (share capital, reserves, borrowing, and customer deposits), each serving different purposes in managing liquidity, profitability, and security.