The Budget Deficit and the National Debt (AQA A-Level Economics): Revision Notes

The Budget Deficit and the National Debt

Understanding the budget deficit

A budget deficit occurs when government spending exceeds the revenue it receives from taxes and other sources. This concept was introduced earlier when we defined it as G > T (government spending greater than tax revenue). In this section, we explore how budget deficits connect to the national debt and examine the broader implications of government borrowing for the economy.

Understanding the distinction between deficits and debt is crucial for analysing fiscal policy. The deficit measures an annual shortfall, whilst the debt represents the cumulative total of all past borrowing that remains outstanding.

The relationship between deficits and debt is similar to the relationship between water flowing into a bathtub (the deficit) and the total amount of water in the tub (the debt). Even if you reduce the flow of water, the tub continues to fill as long as water is still flowing in.

What is the national debt?

Defining the national debt

The national debt refers to the total stock of accumulated central government borrowing that has not yet been repaid. Despite its name, this is somewhat misleading - it is not the debt of the entire nation, nor does it include all public-sector borrowing. Rather, it specifically represents the debt owed by central government.

The national debt builds up over time as the government borrows to finance budget deficits. Each year that spending exceeds revenue, the government must borrow the difference, and this borrowing adds to the existing stock of debt. The debt represents all the government bonds (gilts) and other borrowing instruments that have been issued but not yet redeemed.

Historical perspectives on national debt

Attitudes towards national debt have shifted considerably over time. During the Keynesian era from the 1950s to the 1970s, when deficit financing was common in the UK, the national debt was not seen as a significant burden on the population. During this period, the national debt as a proportion of nominal GDP was actually falling, despite continuous government borrowing. This occurred because the economy was growing rapidly and experiencing inflation, which reduced the real value of the debt.

Even during periods of continuous borrowing, the debt burden can decrease relative to the size of the economy if GDP grows faster than the debt itself. This demonstrates why economists focus on the debt to GDP ratio rather than absolute debt figures.

In contrast, more recent decades have seen national debt reduction become an important element of supply-side fiscal policy. Free-market economists favour low levels of government spending and taxation, and typically support running balanced budgets. This represents a fundamental shift in how policy-makers view public finances.

The relationship between budget balance and national debt

Flow versus stock concepts

A critical distinction in understanding public finances is the difference between flows and stocks. The budget deficit (or surplus) is a flow concept - it measures the rate of borrowing over a period of time, typically one year. In contrast, the national debt is a stock concept - it represents the accumulated total of borrowing at a particular point in time.

In recent decades, UK governments have typically run budget deficits. When this occurs, the flow of public-sector borrowing that finances the deficit adds to the stock of accumulated debt. Even when the deficit is falling, provided it remains positive, new borrowing continues to add to the national debt. Only a budget surplus allows the government to pay down the existing debt.

Understanding Flow vs Stock is Essential

Even when the deficit is falling (the flow is decreasing), the national debt continues to grow (the stock increases) as long as the deficit remains positive. This is why between 2015 and 2020, the UK deficit fell significantly whilst the national debt continued to increase - the government was still borrowing each year, just at a slower rate.

Understanding this flow-stock relationship helps explain why the deficit and debt can move in different directions. For example, between 2015 and 2020, the UK deficit fell significantly (the flow decreased), but the national debt continued to grow (the stock increased) because the government was still borrowing each year.

Nominal and real values

It is useful to distinguish between the nominal (or money) values and real values of both the budget deficit and national debt. More importantly, we need to consider these figures as a percentage of nominal GDP - this gives us the debt to GDP ratio.

The debt to GDP ratio serves as an indicator of the burden that national debt places on the economy. Understanding this ratio helps clarify important distinctions. For instance, whilst the nominal national debt may be rising in absolute terms, the national debt as a percentage of nominal GDP may actually be falling. This happens when nominal GDP rises faster than the nominal debt, either because of genuine economic growth (which is beneficial) or inflation (which may be problematic), or a combination of both.

During the recession before 2010, both the budget deficit and national debt were growing rapidly. More recently, the deficit fell substantially, but the national debt continued to increase. Between 2015 and 2020, the UK's national debt was approximately 80% of GDP. However, the large deficits incurred in 2020 and 2021 to fund the Covid-19 pandemic support pushed the national debt higher, reaching around 100% of GDP by mid-2022.

The debt to GDP ratio is a more meaningful measure than absolute debt figures because it shows the debt relative to the economy's capacity to service it. A country with a £1 trillion debt and a £2 trillion GDP (50% ratio) is in a better position than a country with a £500 billion debt and a £500 billion GDP (100% ratio).

To understand why the debt continued growing even as the deficit fell, we must remember that a deficit represents a flow. Even when the deficit is falling, if it remains positive, the flow of new borrowing still adds to the stock of national debt.

Types of budget deficits

To fully understand the links between government budgetary position and the wider economy, we must distinguish between the cyclical and structural components of the budget deficit and borrowing requirement.

Cyclical budget deficits

The cyclical budget deficit is the portion of the total deficit that changes with the level of aggregate demand at different phases of the economic cycle. During a boom, when the economy is operating above its potential output, tax receipts are relatively high and spending on unemployment benefit is low. The cyclical deficit falls during the boom and may even turn into a surplus. The reverse occurs during the downswing of the economic cycle - tax revenues decline but public spending on unemployment and poverty-related welfare benefits increases. This causes government borrowing to rise and the cyclical deficit to expand.

How Cyclical Deficits Work

During a boom:

- Tax revenues are high (more people earning, more spending)

- Welfare spending is low (fewer unemployed)

- Cyclical deficit falls or becomes a surplus

During a recession:

- Tax revenues are low (less income, less spending)

- Welfare spending is high (more unemployed, more benefits)

- Cyclical deficit rises

Structural budget deficits

The structural budget deficit is the component that is not related to the state of the economy. This part of the deficit does not disappear when the economy recovers from a recession. Therefore, it provides a better guide to the underlying level of the deficit than the headline or cyclical figure. Because the structural deficit cannot be directly measured, it must be estimated by economists.

The structural component of the budget deficit and borrowing requirement relates partly to changes in the structure of the economy. For example, it reflects government policy decisions such as those related to defence expenditure. In recent years, several factors have contributed to the growth of the structural budget deficit in the UK:

- Deindustrialisation and globalisation eroding the tax base

- Movement of industries to eastern Europe and Asia

- An ageing population

- Growth in single-parent families dependent on welfare benefits

Why Structural Deficits Matter More

A growing structural deficit carries a concerning message: a government that seriously wishes to improve public-sector finances will need to introduce significant tax increases, public spending cuts, or possibly both. Unlike cyclical deficits which disappear during economic recoveries, structural deficits persist regardless of economic conditions, requiring deliberate policy action to address.

A growing structural deficit carries a concerning message: a government that seriously wishes to improve public-sector finances will need to introduce significant tax increases, public spending cuts, or possibly both. This is what occurred during the rapid deterioration in the UK's public finances from 2008 onwards, when the government implemented a period of austerity.

The impact of budget deficits on macroeconomic performance

The Keynesian perspective

From the 1950s to 1979, Keynesian-inspired governments in the UK and other western countries used discretionary macroeconomic policy to manage the level of aggregate demand in the economy.

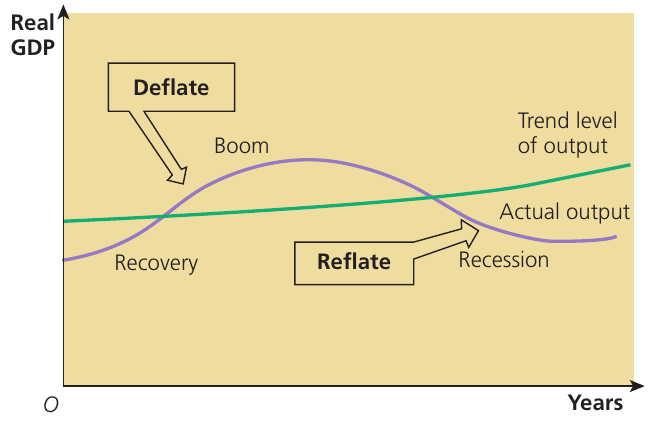

These governments employed contractionary fiscal and/or monetary policy to deflate aggregate demand during the boom phase of the economic cycle. This was followed by expansionary fiscal and/or monetary policy to reflate (increase) aggregate demand to counter the downswing of the cycle. If successful, this approach would make the economic cycle smoother and less volatile than it would have been without discretionary demand management. Through better utilisation of labour and other resources throughout the cycle, the long-run trend rate of growth might also improve. This approach is known as counter-cyclical demand management policy.

Counter-Cyclical Policy in Action

The Keynesian approach involves:

- During booms: Deflate (reduce) aggregate demand through tax increases or spending cuts

- During recessions: Reflate (increase) aggregate demand through tax cuts or spending increases

The goal is to smooth out the peaks and troughs of the economic cycle, reducing economic volatility and improving overall resource utilization.

Automatic stabilisers

As you work through fiscal policy content, you might conclude that governments face a choice between Keynesian-style discretionary demand management and the "balancing the budget" approach favoured by free-market supply-side economists. However, there is an alternative approach that lies between these extremes, in which governments base fiscal policy on the operation of automatic stabilisers.

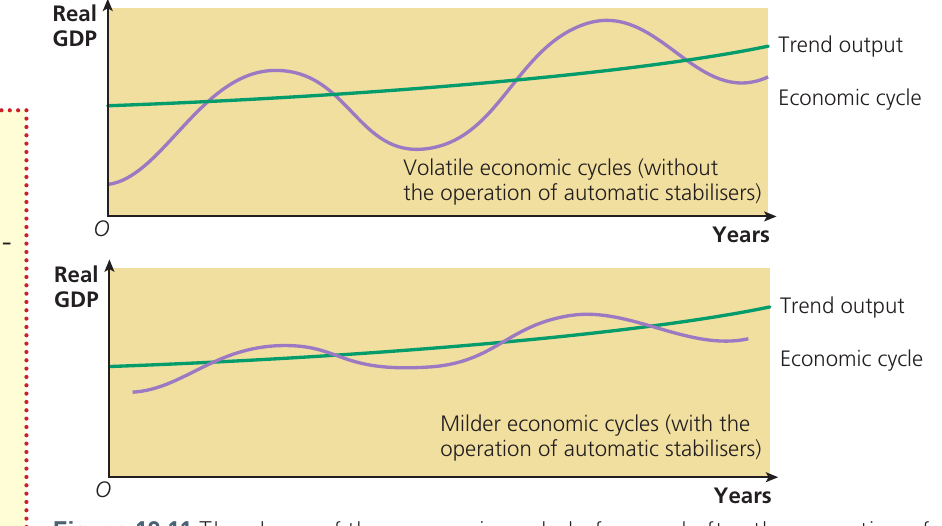

Automatic stabilisers are fiscal policy instruments, such as progressive taxes and income-related welfare benefits, that automatically stimulate aggregate demand when the economy is in a downswing and depress aggregate demand during an upswing. By doing this, they reduce the volatility of economic fluctuations - the "ups" and "downs" of the cycle - thereby smoothing the economic cycle.

Suppose, for example, that a collapse in confidence or export orders causes aggregate demand to fall. National income then also begins to fall, declining in response to the initial fall in demand. However, as national income falls and unemployment rises, demand-led public spending on unemployment pay and welfare benefits also increases. If the income tax system is progressive, the government's tax revenues fall faster than national income. Through these mechanisms, increased public spending on transfers and declining tax revenues inject demand back into the economy. This stabilises and dampens the deflationary impact of the initial fall in aggregate demand, reducing the overall size of the contractionary multiplier effect.

Automatic stabilisers also work in the opposite direction. As incomes and employment rise during an economic upswing, the take-up of means-tested welfare benefits and unemployment-related benefits automatically falls. Meanwhile, tax revenues rise faster than income due to progressive taxation. By taking demand out of the economy and reducing the size of the expansionary multiplier, automatic stabilisers help prevent overheating during the boom phase of the economic cycle.

How Automatic Stabilisers Function Without Policy Changes

The key advantage of automatic stabilisers is that they work without requiring any government decision-making:

Progressive taxation: When incomes fall during a recession, people move into lower tax brackets automatically, leaving them with more disposable income than if tax rates were flat.

Welfare benefits: As unemployment rises, benefit payments automatically increase, maintaining some level of consumer spending without requiring new legislation.

These mechanisms respond immediately to economic changes, unlike discretionary policies which may take months to implement.

Evidence from developed economies

There is now widespread agreement that automatic stabilisers such as progressive taxation and income-related transfers have contributed to milder economic cycles experienced by the UK prior to 2008. Before 1939, economic cycles - or trade cycles as they were known then - displayed much more volatile fluctuations between boom and slump than in the years between the Second World War and 1973. Keynesians have argued that the relatively mild economic cycles prior to 1973 provide evidence of the success of Keynesian demand management policies in stabilising cyclical fluctuations.

However, the economic cycle was also relatively mild in countries such as West Germany, which did not use fiscal policy to manage aggregate demand in a discretionary manner. This suggests that automatic stabilisers of progressive taxation and the safety net provided by welfare benefits for the poor - both introduced widely in western industrialised economies after 1945 - were more significant than discretionary fiscal policy in reducing economic cycle fluctuations.

Most economists now agree that deficits should grow during the downswing of the economic cycle, provided these are matched by surpluses in the subsequent upswing. This allows automatic stabilisers to function effectively whilst maintaining fiscal sustainability over the complete cycle.

The free-market critique

Challenges to Keynesian demand management

Pro-free-market or anti-Keynesian economists oppose the use of Keynesian counter-cyclical demand management policies. They raise several important objections to discretionary fiscal intervention.

Firstly, they argue that governments may misjudge the appropriate timing - deflating when they should be reflating, and vice versa. This problem is particularly likely if governments reflate (expand) aggregate demand to win votes in a general election, even when economic conditions suggest they should resist this temptation.

Secondly, time lags between changes in the state of the economy and when policies become effective create difficulties for policy-makers attempting to fine-tune the economy. For example, if a downturn occurs and the government responds with tax cuts and increased government spending, the economy may have already recovered on its own by the time these policies take effect.

The Timing Problem

Free-market economists argue that by the time a government:

- Recognizes an economic problem

- Decides on appropriate policy action

- Implements the policy through legislation

- Waits for the policy to take effect in the economy

...the economic situation may have completely changed. This can lead to policies that are counter-productive, potentially making economic cycles more volatile rather than smoothing them.

Thirdly, free-market economists believe that our knowledge of the economy is imperfect and that market forces will naturally drive the economy towards its normal capacity level of output in the medium term, without government intervention. They argue that government intervention is more likely to contribute to greater cyclical instability rather than reduce it. In other words, intervention may increase the variability in economic growth over the economic cycle rather than reducing it.

Additionally, when discretionary fiscal policy is used to try to "smooth" the economic cycle, free-market economists contend that the long-run trend rate of growth is likely to fall. This reduction in potential growth undermines the economy's productive capacity over time.

Financial crowding out

Perhaps most importantly, free-market economists believe that the Keynesian use of demand management policies provides merely an excuse for the growth of "big government". This leads to crowding out, in which wealth-consuming government spending replaces the profit motive and wealth-creating private-sector activity.

As explained earlier, resource crowding out occurs when resources employed by the government cannot simultaneously be used in the private sector. However, in the context of potentially harmful effects of large budget deficits, financial crowding out becomes particularly relevant.

Financial crowding out results from the method of financing an increase in public spending. Public spending can be financed through taxation or borrowing. Taxation obviously reduces the spending power of private individuals and firms paying the taxes. However, suppose the government increases public spending by £40 billion and finances the resulting budget deficit by selling new bonds on the capital market - in the form of new gilt-edged securities.

To persuade insurance companies, pension funds, and other financial institutions in the capital market to purchase these extra gilts, the guaranteed annual interest rate offered on new gilt issues must increase. The resulting general rise in interest rates makes it more expensive for firms to borrow and raise capital for investment. Private-sector investment therefore falls, and financial crowding out has occurred. Higher interest rates are also likely to reduce household consumption, further diminishing aggregate demand.

The Financial Crowding Out Mechanism

- Government increases spending and borrows to finance it

- Government sells bonds (gilts) to raise funds

- To attract buyers, government must offer higher interest rates

- Higher interest rates in general economy discourage private investment

- Business investment falls, reducing long-term economic growth

- Consumer spending may also fall due to higher borrowing costs

The net effect may be that increased government spending is offset by decreased private-sector spending, undermining the intended expansionary effect of fiscal policy.

Evaluating budget deficits

Benefits and costs

When analysing the benefits and costs of budget deficits, economists like Megan McArdle, a free-market economist, distinguish between the effects of cyclical and structural deficits. According to this view, Keynesian economists focus on cyclical deficits, which are not considered a major problem. In contrast, pro-free-market economists express more concern about structural deficits, which can become highly problematic.

When correcting cyclical fluctuation in the economy, government intervention may prove effective, whether through discretionary demand management or through the automatic fiscal stabilisers described earlier. McArdle argues that this intervention can be thought of as "Great Depression insurance" - providing protection against severe economic downturns. Furthermore, the resulting debt is likely to be eroded by inflation, meaning it will cost less in real terms than in nominal terms. Cyclical deficits should also disappear as the economy recovers. During a boom, a cyclical surplus should emerge, allowing some of the accumulated debt to be repaid.

The structural deficit presents greater challenges. This is the mismatch between government spending and tax revenues that persists regardless of the phase of the economic cycle. The structural deficit becomes manageable as long as the resulting growth of the national debt roughly matches, or grows more slowly than, the rate of GDP growth. In this situation, even persistent structural deficits can be tolerated because the debt to GDP ratio will not increase.

When Structural Deficits Become Problematic

Structural deficits become serious when they exceed the rate of economic growth. When this happens:

- Interest payments grow as a proportion of the overall budget

- The size of required tax rises or spending cuts increases over time

- Higher taxes may reduce incentives for work and enterprise

- Spending cuts often harm the most vulnerable members of society

This creates a vicious cycle where the deficit problem becomes progressively harder to solve.

However, when the structural deficit begins to exceed the rate at which the economy is growing, serious problems emerge. Interest payments start to grow as a proportion of the overall budget. As they increase, the size of tax rises or spending cuts needed to close the budget deficit also grows. Higher taxes may reduce incentives for work and enterprise, whilst cuts in spending often harm the most vulnerable members of society.

Regarding budget surpluses, these can provide benefits by reducing inflationary pressures through taking demand out of the economy. They also enable the national debt to fall, as explained previously. However, persistent budget surpluses may induce harmful deflation caused by excessive depression of aggregate demand. They can also indicate that taxes are higher than necessary, potentially damaging the supply-side performance of the economy by reducing incentives and growth potential.

The significance of national debt size

Reproductive versus deadweight debt

Some economists and politicians argue that a large national debt burdens the economy because future generations of taxpayers will pay interest on extravagant borrowing by current governments. To properly assess this argument, it is useful to distinguish between the reproductive national debt and the deadweight national debt.

Suppose the government sells gilts to finance the construction of a motorway or other capital investment or infrastructure project. Although the government borrows for many years, the resulting liability is matched by a wealth-producing asset - the motorway itself. This type of "reproductive" borrowing does not burden future generations, since interest payments on the debt are essentially "paid for" by the motorway's contribution to future national output. Some capital assets, such as schools and hospitals, do not last forever, whereas the debt incurred when they were built often persists long after the assets have depreciated.

In contrast, long-term borrowing to finance current spending - such as on wars, salaries of public-sector employees, or cash welfare benefits - can be regarded as imposing a burden on future generations. Their taxes will be required to pay interest on the "deadweight" spending indulged in by the government today. Since deadweight debt does not cover any real asset, interest payments ultimately burden both current and future generations of taxpayers.

Reproductive vs Deadweight Debt: A Practical Distinction

Reproductive debt finances:

- Infrastructure projects (roads, railways, bridges)

- Schools and hospitals

- Public investments that generate future economic benefits

- Assets that contribute to future national output

Deadweight debt finances:

- Wars and military spending

- Current public-sector salaries

- Welfare benefits and transfers

- Day-to-day government operations

The key difference is whether the borrowing creates an asset that helps pay for itself over time or whether it simply funds consumption that provides no future return.

Historically, the UK national debt grew fastest during the two world wars of the twentieth century. On one hand, spending on arms led to massive growth in deadweight debt. On the other hand, because the wars were won, this growth in national debt arguably saved the country from national enslavement. Despite the huge interest payments the UK had to pay for many decades, this represented a price worth paying for national survival.

Debt as a percentage of GDP

The significance of the national debt depends partly on its size as a percentage of GDP, and on whether the national debt can be "rolled over" - that is, continually renewed as portions of it mature.

When the rate of inflation exceeds the rate at which the budget deficit and borrowing requirement add to the nominal national debt, the real value of the debt as a proportion of money or nominal GDP falls. If the inflation rate is greater than the nominal interest rate which the government pays to debt-holders, the government gains and debt-holders lose. This represents an example of inflation redistributing wealth from lenders (holders of the national debt) to borrowers (the government), thereby reducing the real burden of the debt to the government.

However, if holders of the national debt recognise this situation, they will demand much higher nominal interest payments as a condition for continuing to lend to the government. This can lead to difficulties in rolling over the debt.

Rolling over the national debt

Each year, part of the national debt matures and, unless there is a budget surplus, the government must sell new debt to raise the funds needed to repay the maturing debt. This process is called renewing or "rolling over" the national debt. If the government is forced to pay higher nominal interest rates to provide lenders with a real return on their savings, this can lead to financial crowding out, as discussed earlier.

The cost of servicing the national debt - represented by the interest payments to debt-holders - would not pose a problem if, firstly, the national debt were small, and secondly, if all the debt were held internally by people living in the country. When debt is held internally, servicing costs amount essentially to a transfer from taxpayers (whose taxes are higher than they would be in the absence of debt interest payments) to debt-holders who have lent to the government.

Why External Debt Matters

When significant portions of the debt are held externally by people living in other countries, the servicing burden of the national debt becomes more significant for the country. Interest payments must be made to foreign debt-holders, representing a real resource transfer out of the domestic economy.

With internally held debt, interest payments represent a redistribution within the country (from taxpayers to bondholders). With externally held debt, these payments represent a genuine loss of resources to other countries.

However, when significant portions of the debt are held externally by people living in other countries, the servicing burden of the national debt becomes more significant for the country. Interest payments must be made to foreign debt-holders, representing a real resource transfer out of the domestic economy.

The Office for Budget Responsibility

The Office for Budget Responsibility (OBR) was created in 2010 to provide independent analysis of the UK's public-sector finances. The OBR produces medium-term forecasts of the UK economy twice yearly in its Economic and Fiscal Outlook. By contrast, the Treasury compiles a monthly list of external economic forecasts, comparing them to those of the OBR.

Rather than the chancellor making judgements based solely on Treasury forecasts, the OBR rules on whether the government's policies have a better than 50% chance of meeting the Treasury's fiscal targets. This arrangement was designed to make the government more accountable for its implementation of fiscal policy.

The OBR's creation reflected concerns that democratic governments left to their own devices are prone to "deficit bias" in their management of public finances. There are several possible reasons for such bias:

- Ministers may prioritise their own electoral prospects over sound fiscal management

- Governments may lack the forward-looking perspective needed for sustainable fiscal policy

- Finance ministries may have less influence than large spending departments they are meant to control

The Case for Independent Fiscal Oversight

The core analytical argument for fiscal watchdogs like the OBR is that outside scrutiny by unofficial bodies could help take politics out of tax and spending policy decisions. However, governments can easily dismiss criticism from outside bodies by claiming that such organisations lack access to privileged information on the behaviour of tax revenues and public spending.

By having a statutory entitlement to all relevant government information, the OBR can fulfil its core duty: to examine and report on the sustainability of public finances. This independent oversight helps ensure greater transparency and accountability in fiscal policy-making.

By having a statutory entitlement to all relevant government information, the OBR can fulfil its core duty: to examine and report on the sustainability of public finances. This independent oversight helps ensure greater transparency and accountability in fiscal policy-making.

Key Points to Remember

-

The national debt is a stock concept: It represents all accumulated central government borrowing that has not been repaid, not the debt of the whole nation.

-

Budget deficits are flows that add to the debt stock: Even when deficits fall, if they remain positive, they continue adding to national debt. Only surpluses reduce the debt.

-

Cyclical and structural deficits require different responses: Cyclical deficits change with the economic cycle and are generally less concerning. Structural deficits persist regardless of economic conditions and pose greater long-term challenges.

-

Automatic stabilisers smooth economic cycles: Progressive taxes and income-related benefits automatically dampen economic fluctuations without requiring discretionary policy changes.

-

The debt to GDP ratio is more important than absolute debt levels: A rising nominal debt can coincide with a falling debt to GDP ratio if the economy grows faster than the debt, indicating a decreasing burden.

-

Reproductive debt creates assets; deadweight debt does not: Borrowing for infrastructure and investment can pay for itself through future output, whilst borrowing for current spending burdens future generations.

-

Financial crowding out occurs when government borrowing raises interest rates: This reduces private investment and consumption, potentially offsetting the expansionary effects of fiscal policy.

-

The OBR provides independent oversight: By having access to all government financial information and assessing policy credibility, the OBR helps reduce deficit bias and improve fiscal accountability.