The Balance of Payments: Further Exploration (AQA A-Level Economics): Revision Notes

The Balance of Payments: Further Exploration

Applying AD/AS analysis to the current account of the balance of payments

The current account of the balance of payments records a country's trade in goods and services, along with income flows and transfers. Understanding how changes in the current account affect the wider economy requires us to use aggregate demand and aggregate supply (AD/AS) analysis.

Recall that aggregate demand is calculated using the equation: AD = C + I + G + (X - M), where C is consumption, I is investment, G is government spending, and X is exports and M is imports. The term (X - M) represents net exports, which is a key component of the current account. When net exports are positive (X > M), there is a current account surplus. When net exports are negative (X < M), there is a current account deficit.

Exports represent an injection of spending into the circular flow of income. When overseas consumers purchase British goods and services, money flows into the UK economy. In contrast, imports represent a leakage or withdrawal of spending from the circular flow. When UK consumers purchase foreign goods and services, money flows out of the UK economy.

Let's consider what happens when overseas demand for UK exports increases while UK demand for imports stays the same. This creates a net injection of spending into the circular flow of income, and the current account moves into surplus (or an existing surplus increases).

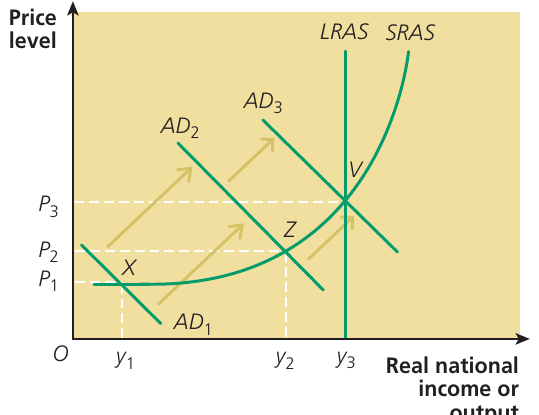

The diagram above shows how this increase in exports affects the economy through the AD/AS model. The rise in export demand shifts the aggregate demand curve to the right, from AD₁ to AD₂. What happens next depends critically on the shape and position of the short-run aggregate supply (SRAS) curve.

Initially, suppose the economy is at point X, experiencing a deep recession with deficient aggregate demand. At this point, there are substantial unemployed resources in the economy. The increase in export demand shifts AD to the right, causing real output to rise from to . The price level rises slightly from to , but the main effect is to reduce demand-deficient unemployment and increase real national income. In this situation, the increase in exports helps to reflate the economy and move it closer to full employment.

However, as the SRAS curve becomes steeper moving up the curve, further increases in aggregate demand have a different effect. When the AD curve shifts from AD₂ to AD₃, the economy moves to point Z. At this point, the main effect falls increasingly on the price level rather than on output and jobs. The price level rises from to , while output increases only modestly from to .

As the economy approaches full employment, export demand becomes inflationary rather than reflationary. This is because when the economy is operating on its vertical long-run aggregate supply (LRAS) curve, there is no spare capacity to produce additional output. Any further increase in export demand at point V simply pushes up prices without generating sustained increases in real output. This demonstrates that export-led growth is only beneficial when there are unemployed resources that can be brought into production.

Nevertheless, sustained growth in export demand can eliminate demand deficiency and help the economy reach its long-run aggregate supply curve at point V. Moreover, if overseas demand for exports stimulates supply-side improvements in the domestic economy, the LRAS curve itself may shift to the right. This would enable the economy to produce and supply more goods to meet the increased export demand without generating inflation. This outcome represents export-led growth in its truest sense.

Export-led growth refers to economic growth resulting from increased international competitiveness of exporting industries. In the short run, it means growth from rising exports (one of the components of aggregate demand). In the long run, it means growth from the expansion and increased competitiveness of export industries, associated with productivity improvements and increased productive capacity.

Historical Examples of Export-Led Growth

The German and Japanese economies enjoyed export-led growth from the 1960s to the 1980s. More recently, China has experienced similar benefits, though the worldwide growth of demand for Chinese exports has begun to cause inflationary pressures in the Chinese economy.

Deficits and surpluses on the current account

The current account measures trade flows and reflects a country's international competitiveness. Understanding whether deficits and surpluses pose problems is essential for evaluating a country's economic health.

A country runs a current account deficit when its currency outflows exceed its currency inflows. Generally, this means the country is importing more goods and services than it is exporting. Conversely, a current account surplus occurs when currency inflows exceed outflows, typically indicating that the country exports more than it imports.

| Country | Current Account Balance 2020 (£m) |

|---|---|

| China | +273,980 |

| Germany | +269,077 |

| United Kingdom | -55,888 |

| United States | -616,087 |

The table above shows the current account positions of selected major economies in 2020. China and Germany both ran large surpluses, meaning they exported significantly more than they imported. In contrast, the UK and USA ran substantial deficits, importing far more than they exported. The USA's deficit was particularly large, exceeding $600 billion.

Do current account deficits pose problems?

A short-run deficit or surplus on the current account does not necessarily pose a problem. However, a persistent or long-run imbalance indicates fundamental disequilibrium in the economy. The severity of any problem depends on the size and cause of the deficit.

The larger the deficit, the greater the problem is likely to be. Additionally, the problem is more serious if the deficit results from the uncompetitiveness of the country's industries. When industries cannot compete effectively in international markets, this suggests structural weaknesses that can worsen over time.

In the short run, a deficit allows a country's residents to enjoy living standards boosted by imports, consuming more than they could from domestic output alone. However, this comes at a cost. In the long run, the decline of industries unable to compete internationally leads to lower living standards. Workers lose jobs in uncompetitive sectors, and the economy becomes increasingly dependent on foreign goods and services.

For a poor or developing country, a current account deficit can be justified if it results from importing capital goods on a large scale to modernise infrastructure and promote economic development. In this case, the deficit represents investment in future productive capacity rather than simply excessive consumption.

Do current account surpluses pose problems?

While many people agree that persistent current account deficits can cause serious problems, fewer recognise that surpluses can also be problematic. A surplus is often viewed as a sign of national economic success. The popular view is that the bigger the surplus, the better the country's economic performance must be.

Insofar as a surplus measures the competitiveness of a country's exporting industries, this view has merit. However, there are several reasons why a large payments surplus is undesirable, though a small surplus may be justifiable.

One country's surplus is another country's deficit

The balance of payments must balance for the world as a whole. Since we do not trade with other planets, it is impossible for all countries to run surpluses simultaneously. When countries with persistently large surpluses refuse to take action to reduce them, deficit countries cannot reduce their deficits. These deficit countries may then be forced to impose import controls, from which all countries, including surplus nations, eventually suffer.

In an extreme scenario, such protectionist measures could trigger a collapse of world trade and a global recession. This is not merely theoretical. At various times since the 1970s, current account surpluses of oil-producing countries have contributed to global economic problems. More recently, Japan's surpluses and especially China's large payments surpluses have created similar tensions. These have been the counterpart to the massive US trade deficit. On several occasions, the US government has faced pressure from manufacturing and labour groups to introduce import controls and other forms of protectionism. When enacted, such protectionist measures undoubtedly harm world trade and reduce global economic welfare.

It's worth noting that non-oil-exporting developing countries almost without exception suffer chronic deficits, though these differ significantly from the US trade deficit. The imbalance of trade between more developed and less developed economies cannot be reduced without industrialised countries of the Global North taking action to reduce surpluses gained at the expense of developing economies in the Global South.

A balance of payments surplus can be inflationary

A balance of payments surplus represents an injection of aggregate demand into the circular flow of income. This increases the equilibrium level of nominal or money national income. If the economy has substantial unemployed resources, this injection has the beneficial effect of reflating real output and jobs. However, if the economy is already close to full capacity, the result is demand-pull inflation.

When a country's economy is initially near full employment, any further increase in aggregate demand from a growing surplus pushes up the price level without generating sustained increases in real output. The economy simply experiences inflation rather than real economic growth.

Three factors that influence a country's current account balance

Several factors can influence a country's current account balance. Three of the most important are productivity, inflation rates, and the exchange rate. Primary income flows (profits, dividends, and interest payments) also play a role, though we'll focus primarily on the main three factors.

Productivity

Improving labour productivity - that is, output per worker - is critical to the success of supply-side policies intended to improve both the price competitiveness and quality competitiveness of a country's exports in international markets. Higher productivity means that firms can produce goods at lower unit costs, enabling them to charge more competitive prices while maintaining profit margins.

Productivity improvements also enable firms to invest more in research and development, design, and marketing. These investments enhance the quality competitiveness of products, making them more attractive to international buyers. Countries with sustained productivity growth tend to see improvements in their current account positions over time, as their exports become more competitive globally.

Inflation

The key point about inflation is not a country's absolute rate of inflation, but its inflation rate relative to those of its trading competitors. If a country's inflation rate is higher than the inflation rates of competitor nations, its exports will lose price competitiveness in international markets. This deteriorates the country's current account balance.

Understanding Relative Inflation

If the UK experiences 5% inflation while its main trading partners experience only 2% inflation, UK goods become relatively more expensive. Foreign buyers will tend to purchase fewer UK exports, while UK consumers will find imported goods relatively cheaper and purchase more of them. Both effects worsen the current account balance.

However, the price elasticities of demand for exports and imports complicate this analysis. If demand is relatively price inelastic, changes in relative prices may have limited effects on trade volumes. We'll explore this issue in more detail when discussing devaluation.

Exchange rate

Changes in the exchange rate of a country's currency have a similar effect to changes in its relative rate of inflation. In short, a rising exchange rate increases the foreign currency prices of the country's exports and reduces their competitiveness. Meanwhile, imports become more price competitive, as their domestic prices fall.

The price elasticities of demand for exports and imports are relevant here too. These determine the extent to which changes in relative prices affect trade volumes and the current account balance.

Note also that if a rise in the domestic inflation rate relative to other countries is matched by a fall in the exchange rate of equal magnitude, the two effects cancel each other out. The country's international price competitiveness remains unchanged.

Policies to cure or reduce a balance of payments deficit

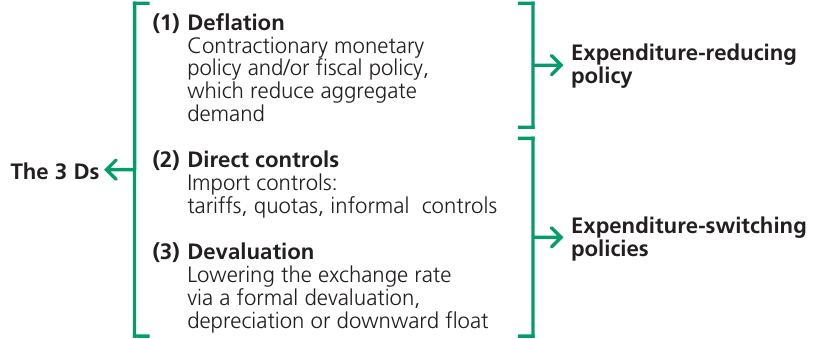

Traditionally, governments (and their central banks) could use three different policies to try to cure a persistent deficit caused by an over-valued exchange rate. These are known as the "3 Ds" of deflation, direct controls, and devaluation or currency depreciation.

The diagram above illustrates these three policy options:

- Deflation: Contractionary monetary and/or fiscal policy that reduces aggregate demand (expenditure-reducing policy)

- Direct controls: Import controls including tariffs, quotas, and informal controls

- Devaluation: Lowering the exchange rate via formal devaluation, depreciation, or downward float

Deflation is classified as an expenditure-reducing policy, while direct controls and devaluation are expenditure-switching policies. Let's examine each in detail.

Deflation as an expenditure-reducing policy

Expenditure-reducing policy is a government policy that aims to eliminate a current account deficit by reducing the demand for imports. It does this by reducing the level of aggregate demand in the economy. Conversely, to reduce a current account surplus, aggregate demand would need to increase, causing spending on imports to rise.

Deflationary policy involves using contractionary monetary and/or fiscal policy to reduce the demand for imports. For example, if the marginal propensity to import in the economy is 0.4, reducing aggregate demand by £10 billion should cause spending on imports to fall by £4 billion. This is an example of expenditure-reducing policy in action.

Although deflation is primarily an expenditure-reducing policy, it also has an expenditure-switching element. By reducing the rate of domestic price inflation relative to inflation rates in other countries, deflation improves the price competitiveness of exports and reduces the attractiveness of imports. Domestic consumers switch some of their spending from imports to domestically produced goods.

However, in modern economies this expenditure-switching effect is usually quite small. The main effect of deflationary policy, at least in the short run, is to reduce aggregate demand and depress economic activity in the domestic economy.

Incomes and employment tend to fall rather than just the price level. Falling demand for domestic output may force firms to seek export orders to use spare production capacity. However, because exports are generally less profitable than domestic sales, a sound and expanding home market is usually necessary for a successful export drive.

When deflating aggregate demand to achieve the external objectives of supporting the exchange rate and reducing a current account deficit, a government sacrifices the domestic economic objectives of full employment and economic growth. For this reason, governments often prefer to use expenditure-switching policies of import controls and devaluation rather than expenditure-reducing deflationary policies.

However, when an economy is overheating, expenditure-reducing measures are more appropriate than expenditure-switching policies. Reducing aggregate demand helps to control domestic inflationary pressures as well as to correct a balance of payments deficit.

Direct controls as expenditure-switching policies

Direct controls involve imposing quotas or even outright bans (embargoes) on imports. These measures directly cut or prevent expenditure on imports. As a result, consumers switch their spending from foreign goods to home-produced goods. Together with import duties or tariffs, which make imports less price competitive, direct controls represent examples of expenditure-switching policies.

Expenditure-switching policy is a government policy that aims to reduce a current account deficit by switching domestic demand away from imports to domestically produced goods. Conversely, to reduce a current account surplus, the policy would aim to switch domestic demand away from domestically produced goods towards imports.

Direct controls do not, however, cure the underlying cause of a current account deficit - namely, the uncompetitiveness of a country's goods and services. Moreover, because a country essentially gains an advantage at the expense of other countries, import controls tend to provoke retaliation.

Free-market economists believe that protectionism reduces specialisation and causes world trade, world output, and economic welfare to fall. Because of these concerns, international organisations such as the European Union and the World Trade Organization (WTO) have reduced the freedom of individual countries to impose import controls unilaterally to improve their current accounts.

The EU uses its common external tariff to provide protection for all its member states collectively. As a member of the WTO, the UK government is unlikely to be able to use import controls to reduce a current account deficit.

However, the rules-based system of international trade has come under strain in recent years. The election of Donald Trump as US president resulted in new trade wars with China and threats to withdraw from the WTO. In 2022, Russia's invasion of Ukraine led to economic sanctions on trade with Russia imposed by the international community, though not all countries participated. The UK's withdrawal from the EU has also created difficulties in establishing trading rules between Northern Ireland and the EU.

Devaluation or currency depreciation as an expenditure-switching policy

The exchange rate is the value of one currency in terms of another currency. The word "devaluation" can be used in several ways. In a narrow sense, a country devalues by reducing the value of a fixed exchange rate. (Fixed exchange rates are explained in the next chapter.) However, the term is sometimes used more loosely to describe any fall in the value of the currency - that is, a decrease in the exchange rate.

When the exchange rate is floating, a fall in its value is usually referred to as a depreciation of the exchange rate (though devaluation can be used here as well). It's important to distinguish between external and internal depreciation of the currency. Devaluation or a downward float causes an external depreciation; more units of the currency are needed to buy a unit of another currency. This should not be confused with internal depreciation of the currency, which occurs when there is inflation within the economy. Internal depreciation reduces the internal purchasing power of the currency as the price level rises.

In a fixed exchange rate system, an increase in the external value of a currency is known as a revaluation. In a floating rate system, it is called an appreciation of the exchange rate.

If we assume the unavailability of import controls, a country wishing to reduce a current account deficit must generally choose between deflation and devaluation (or currency depreciation). As with tariffs and export subsidies, a fall in the external value of the currency has a mainly expenditure-switching effect.

By increasing the price of imports relative to the price of exports, a successful devaluation switches domestic demand away from imports and towards home-produced goods. Similarly, overseas demand for the country's exports increases in response to the fall in export prices. A successful devaluation therefore improves the current account through both reduced imports and increased exports.

Price elasticity of demand and devaluation

The effectiveness of a fall in the exchange rate in reducing a balance of payments deficit depends significantly on the price elasticities of demand for exports and imports.

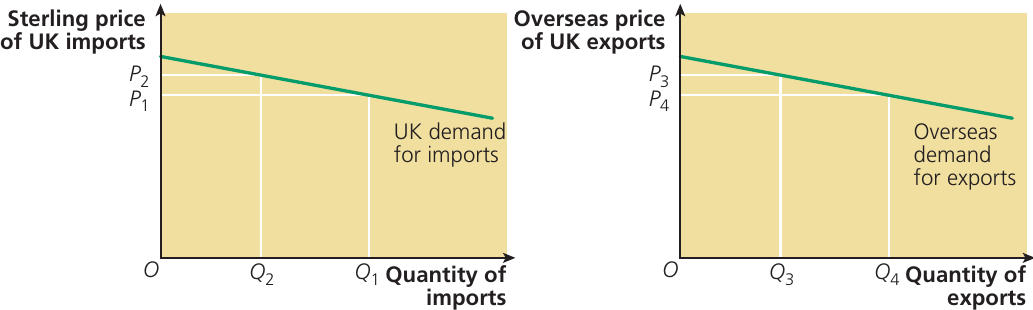

As the diagrams below show for the UK, when the demand for exports and the demand for imports are both highly price elastic, a fall in the exchange rate is likely to reduce a current account deficit.

Following a devaluation, the domestic price of imports into the UK rises from to , while the overseas price of UK exports falls from to . As a result, UK residents spend less on imported goods following an increase in their relative prices. At the same time, residents of overseas countries spend more on UK exports, whose relative prices have fallen.

On the import side, spending falls from the rectangular area bounded by and to the area bounded by and . Higher import prices mean that consumers switch to the now cheaper domestically produced substitutes. The quantity of imports demanded falls significantly because demand is elastic.

In a similar way, expenditure on the country's exports increases from the rectangular area bounded by and to the area bounded by and . Foreign consumers increase their purchases substantially in response to lower export prices. Overall, the current account improves, assuming the demand for imports and the demand for exports are both price elastic.

The Marshall-Lerner condition

It is more difficult to predict what may happen to the current account when, for example, the demand for exports is price inelastic but the demand for imports is price elastic. The Marshall-Lerner condition provides a simple rule to assess whether a change in the exchange rate can improve the current account.

The condition states that when the sum of the export and import price elasticities is greater than unity (ignoring the minus sign), a fall in the exchange rate can reduce a deficit and a rise in the exchange rate can reduce a surplus. When the export and import price elasticities of demand are both highly inelastic, summing to less than unity, a fall in the exchange rate can have the perverse effect of worsening a deficit, while a revaluation might increase a surplus.

The Marshall-Lerner condition is a necessary but not sufficient condition for a fall in the exchange rate to reduce a payments deficit. Even when the condition is met, a devaluation may not work if other factors undermine its effectiveness.

For a devaluation or currency depreciation to be successful, firms in the domestic economy must have spare capacity to meet the surge in demand brought about by the fall in the exchange rate. If the economy is working at, or close to, full capacity, expenditure-reducing deflation and expenditure-switching devaluation should best be regarded as complementary policies rather than substitute policies for reducing a current account deficit.

Deflation alone may be unnecessarily costly in terms of lost jobs and domestic employment and output. However, it may be necessary to provide the spare capacity and conditions in which a falling exchange rate can successfully cure a payments deficit. Deflation may also be needed to offset the potential inflationary consequences of a fall in the exchange rate, which can erode the improvement in competitiveness resulting from the initial fall in the external value of the currency.

Extension: How changes in exchange rates affect the prices of imports

To understand why a fall in the exchange rate is likely to reduce a current account deficit when both import and export demand are highly price elastic, consider the effect of exchange rate changes upon UK prices of imports.

Worked Example: Exchange Rate Changes and Import Prices

Suppose a UK firm, Quidsin supermarkets, buys 500 tonnes of Californian apples each month. The dollar price of the apples is $100 per tonne. The total amount that Quidsin has to pay for the apples is therefore $50,000.

Scenario 1 (January): If the exchange rate is £1 = $1.50, then Quidsin will have to give up around £33,333 to acquire $50,000 (50,000 ÷ 1.50).

Scenario 2 (One year later): When the exchange rate changes to £1 = $2.00, Quidsin now has to give up only £25,000 to get the $50,000 that the supermarket chain needs to pay its suppliers. The strengthening of the pound's exchange rate has benefited Quidsin. The supermarket chain now has to give up fewer pounds to get the same amount of dollars. Quidsin's costs have fallen by around £8,333 a month.

Scenario 3 (Two years later): Suppose the situation changes again, with the exchange rate falling back to £1 = $1.50. This means that, once again, Quidsin has to give up £33,333 to acquire $50,000 (50,000 ÷ 1.50). Compared to a year earlier, Quidsin's costs have now risen by approximately £8,333.

Conclusion: The example shows that for a UK business which imports goods or services, a fall in the pound's exchange rate increases costs. The position for a UK business which exports goods or services would be the exact opposite. A depreciation of the pound makes UK exports cheaper for foreign buyers, potentially increasing export volumes.

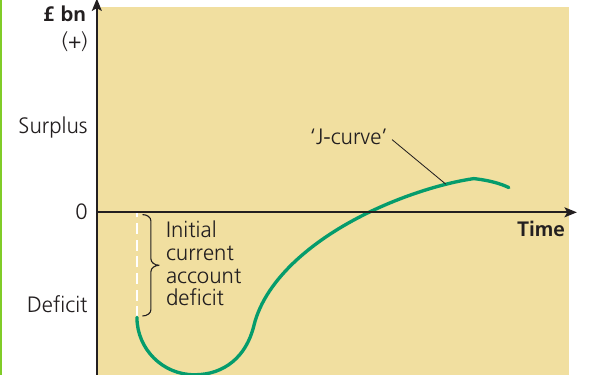

The J-curve effect

Even if domestic demand for imports and overseas demand for exports are both price elastic and spare capacity exists in the economy, in the short run the balance of payments may deteriorate following a devaluation. It takes time for demand to respond to price changes, and firms within the country may still be unable immediately to increase supply following a fall in the exchange rate.

In the short run, the Marshall-Lerner condition may not hold because elasticities of demand are lower in the short run than in the long run. In these circumstances, the balance of payments may worsen before it improves. This is known as the J-curve effect.

The diagram above illustrates the J-curve effect. Initially, the economy starts with a current account deficit. Following a devaluation, the deficit initially worsens, falling deeper into negative territory. This occurs because in the immediate aftermath of the devaluation, import and export volumes don't change much - contracts have already been signed and goods are already in transit. However, because imports are now more expensive in domestic currency terms, the value of imports rises, worsening the deficit.

Over time, as demand responds to the new prices, export volumes increase and import volumes decrease. The current account gradually improves, eventually moving into surplus. The path traced out resembles the letter J, hence the name.

The initial worsening of the balance of payments following a fall in the exchange rate may reduce confidence in the idea that changing the exchange rate is the most appropriate method for reducing a deficit in the current account of the balance of payments. Falling confidence may, in turn, cause capital outflows that destabilise both the balance of payments and the exchange rate. The J-curve effect thus reduces the attractiveness of exchange rate adjustment as an instrument to correct payments disequilibrium.

Nevertheless, if conditions are right, devaluation can reduce a current account deficit. Despite occurring on 'Black Wednesday', the pound's devaluation in September 1992 was extremely successful, at least for a number of years. There were two main reasons for this success.

First, expenditure reduction in the severe recession of the early 1990s created the spare capacity that enabled successful expenditure switching following the pound's devaluation. Secondly, the adoption and achievement of a low inflation target helped to prevent the benefits of the fall in the exchange rate being eroded by accelerating inflation. Low inflation expectations also helped export price competitiveness.

Additionally, factories built in the UK by Japanese companies such as Honda and Toyota had just come on stream, producing goods of a quality that people wanted in the UK and overseas. Some economists believe that the supply-side reforms introduced in the 1980s and 1990s also contributed to improved competitiveness.

In contrast, the pound's devaluation of 2008 did not improve the UK's current account position significantly. Despite the pound losing over 25% of its value against its major trading partners, the current account deficit did not shrink. Instead, by 2010 the UK's deficit on the current account was larger than it had been in 2007. This was partly because in the years following the depreciation, the UK's major trade partners were in a deep recession, making it difficult for exporters to sell in these markets.

Hence, a devaluation of a country's currency is in itself insufficient to eliminate a current account deficit because other macroeconomic factors are important. The exchange rate must fall sufficiently, the Marshall-Lerner condition must be met, and the global economic context must be favourable for the devaluation to succeed.

Supply-side policies and the current account

Deflation, devaluation, and direct controls (the "3 Ds") may be effective short-term policies for reducing current account deficits. However, it is now increasingly recognised that long-term improvement in trade flows requires appropriate and successful supply-side policies and supply-side improvements undertaken by firms within the economy.

The ability of the UK economy to deliver sustained growth of exports and meet the challenge of imported goods and services depends on making UK exports quality competitive as well as price competitive. Low exchange rates, low interest rates at which UK firms can borrow, and low domestic inflation all contribute to increased export price competitiveness. However, price competitiveness on its own is not enough. UK goods and services must also be quality competitive, which involves good design and well-made products.

Improved quality competitiveness may only be achievable in the long run if helped by appropriate government supply-side policies together with supply-side improvements undertaken by the private sector. Supply-side policies that promote greater investment in research and development and improved marketing strategies can have powerful long-term effects in improving quality competitiveness.

Supply-side improvements, followed by an outward shift of the LRAS curve, provide the economy with increased capacity - enabling a reallocation of resources towards exporting. Successful supply-side policies can also improve exports and lead to import substitution by increasing labour productivity, which in turn is likely to improve the price competitiveness of UK exports.

Export-led growth and the UK economy

Export-led growth is a term first introduced about 45 years ago, in the context of speeding up the rate of economic growth in developing countries. The term is still widely used with regard to growth strategies in the developing world. However, in recent years in the UK, together with the concept of investment-led growth, export-led growth has been more narrowly focused on how best to increase the competitiveness of UK exports and achieve sustained economic growth, without the UK economy slipping into recession.

Perhaps not surprisingly, debate in the UK about how to achieve export-led growth became prominent when the economy appeared to be stuck in recession in 2008 and 2009, and there seemed to be little hope of speedy economic recovery.

To remind you, short-term economic growth occurs whenever one or more of the components of aggregate demand increases. The components of aggregate demand are consumption (C), investment (I), government spending (G), and net export demand (X - M). In recent decades, short-term economic growth has been largely consumption-led, though in 2008 and 2009, via its fiscal stimulus, the Labour government tried to achieve government spending-led growth to "spend the UK economy out of recession" as part of the response to the collapse in large parts of the financial sector in the UK.

Consumption-led growth

Consumption-led growth leads to two big problems. First, since much consumer spending is on goods and services produced in other countries, consumption-led growth "sucks" imports into the economy. This may soon lead to a worsening deficit in the current account of the balance of payments. A growing payments deficit may then force the government and the Bank of England to deflate aggregate demand, which at best slows the rate of economic growth and at worst triggers recession.

Secondly, and perhaps more significant, recent economic history has shown that consumption-led growth is unsustainable. A rapid growth of consumption, fuelled by increased household debt and consumer borrowing, leads to speculative bubbles, particularly in the housing market. When these bubbles eventually "prick", aggregate demand collapses, bringing to an end the "boom" phase of the economic cycle. The rate of economic growth declines and perhaps becomes negative.

In this scenario, export-led growth and investment-led growth are seen as "magic bullets" (factors that create positive effects). If they can be achieved, they will increase productivity, competitiveness, and supply-side reform within the economy, enabling sustained economic growth to take place. In such a situation, short-term economic growth, brought about by the increase in aggregate demand, will seamlessly move into sustainable long-term growth.

This is because export-led growth and investment-led growth are associated with increased productivity and with the modernisation and enlargement of the economy's productive capacity. These supply-side improvements enable the LRAS curve to shift rightward, increasing the economy's potential output.

Achieving export-led growth and investment-led growth is, however, much easier said than done. At the time of writing this material, the UK's continuing recovery from recession appears once again to be consumption-led, with little or no evidence of export-led or investment-led growth. Whether this heralds the eventual onset of another recession remains to be seen. It must be remembered that adverse economic "shocks" in the wider world economy can also lead to a collapse in aggregate demand in the UK economy, even when domestic conditions seem favourable.

Government policies to correct or reduce a balance of payments surplus on current account

The policies available to a government for reducing a balance of payments surplus are the opposite of the "3 Ds" of deflation, direct controls, and devaluation that are appropriate for correcting a payments deficit. The policies for reducing a surplus are the "3 Rs" of reflation, removal of import controls, and revaluation.

-

Reflation: Reflating demand via expansionary monetary policy or fiscal policy increases a country's demand for imports. This helps to reduce a current account surplus by increasing spending on foreign goods and services.

-

Removing import controls: Trade can be liberalised by removing import controls. This makes it easier for foreign goods to enter the domestic market, increasing imports and reducing the surplus.

-

Revaluation: There have been calls on countries with large payments surpluses, such as Japan and China, to revalue in order to reduce global payments imbalances. However, because there is much less pressure on a surplus country to revalue than on a deficit country to devalue, such calls have not usually been successful.

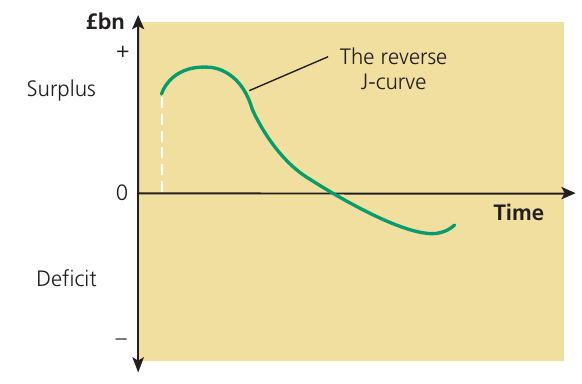

It is also worth noting that for a revaluation to reduce a current account surplus, the Marshall-Lerner condition must be met. In addition, a reverse J-curve may operate.

The reverse J-curve, illustrated in the diagram above, shows that following a revaluation, the payments surplus may initially get bigger before it eventually starts to get smaller. This occurs because in the short run, export and import volumes don't adjust immediately to the new exchange rate. The surplus initially increases as export prices rise and import prices fall in domestic currency terms, but existing trade volumes continue. Over time, as volumes adjust, the surplus gradually diminishes.

The significance of balance of payments deficits and surpluses for individuals

Earlier in this section, we addressed the issue of whether balance of payments deficits and surpluses on current account pose problems for the country experiencing the deficit or surplus.

We explained that while a short-run deficit or surplus on current account does not pose a problem, a persistent or long-run imbalance indicates fundamental disequilibrium. In the case of a deficit, the nature of any resulting problem depends on the size and cause of the deficit. The larger the deficit, the greater the problem is likely to be. The problem is also likely to be serious if the deficit is caused by the uncompetitiveness of the country's industries.

Although in the short run a deficit allows a country's residents to enjoy living standards boosted by imports (higher than would be possible from consuming the country's output alone), in the long run, the decline of industries in the face of international competition lowers living standards. Workers lose jobs, and the country becomes increasingly dependent on imports.

While many people agree that a persistent current account deficit can pose serious problems, we also noted that few realise that a balance of payments surplus on current account can lead to problems. As a surplus is often seen as a sign of national economic success, a popular view is that the bigger the surplus, the better must be the country's performance.

This is obviously true insofar as the surplus measures the competitiveness of the country's exporting industries. However, although a small surplus may be a justifiable objective of government policy, a large payments surplus should be regarded as undesirable for two reasons:

One country's surplus is another country's deficit

Since we do not trade with other planets, the balance of payments must balance for the world as a whole. It is therefore impossible for all countries to run surpluses simultaneously. Unless countries with persistently large surpluses agree to take action to reduce their surpluses, deficit countries cannot reduce their deficits. Deficit countries may then be forced to impose import controls from which all countries, including surplus countries, eventually suffer. In an extreme scenario, this could trigger a world recession and collapse of global trade.

A balance of payments surplus is an injection of aggregate demand

This injection into the circular flow of income can be inflationary. If there are substantial unemployed resources in the economy, this can have the beneficial effect of reflating real output and jobs. However, if the economy is initially close to full capacity, demand-pull inflation results. The economy experiences rising prices without sustained increases in real output.

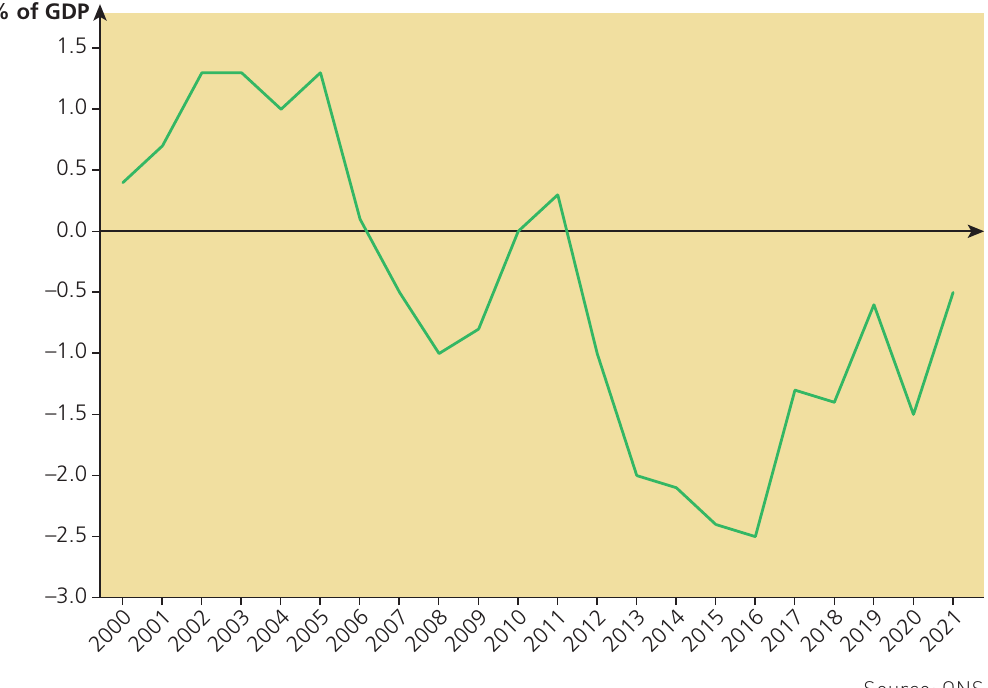

In recent years, the UK's current account deficit has increased in size. This has not necessarily been regarded as a problem because it has been financed by inward capital flows. However, the deficit has been increasing as a percentage of national income, and some economists believe that unless the deficit is reduced, it could lead to capital outflows as foreign investors question the ability of the UK to finance its growing overseas debts.

As the chart below shows, it is not a deterioration in the balance of trade in goods and services that has been the main problem in recent years. A significant cause of the growing current account deficit is a deterioration in the primary income balance.

Primary income is the balance between the income (profits, dividends, and interest payments) received on the UK's foreign investments, and the income paid to overseas investors on their UK investments. The chart shows that since 2011 there has been a significant deterioration of the UK's primary income position, which has widened the deficit on the current account.

According to Parliament's research service:

The deterioration in the primary account was driven by UK residents receiving lower income on their overseas foreign direct investments (FDI). This in turn was a result of both lower returns on those investments (thanks in part to economic weakness in the eurozone), and a reduction in the total stock of UK overseas FDI. In contrast, foreign residents have continued to expand their holdings of UK assets (something that may be linked to the relative strength of the UK's recovery and its status as a "safe haven"), and have shifted the composition of their assets from low-yielding debt to riskier, higher-yielding equity, thereby increasing the rate of return on their holdings.

The deterioration in the primary income balance reflects changes in the returns UK investors receive from overseas investments compared to what foreign investors earn from UK investments. When the UK pays out more in investment income than it receives, this worsens the current account deficit, even if the trade balance remains stable.

Implications for the global economy of other economies taking action to reduce their current account imbalances

As we have seen, countries are more likely to take action to try to reduce a current account deficit than to reduce a current account surplus. Indeed, surplus countries very often like to keep things exactly as they are, particularly if they benefit from artificial price competitiveness caused by an under-valued exchange rate.

Perhaps not surprisingly, corrective action by an economy to reduce the size of a current account deficit may have very little effect on other economies. This is true if the deficit is small and, secondly, if the economy forms only a tiny part of the world economy. The same is not true, however, if the economy taking the corrective action is large.

The USA

The USA is the country that runs the largest current account deficit, importing far more than it exports. Many of these imports are cheap Chinese manufactured goods and components that US firms such as Apple design before they are assembled into finished consumer goods (often in China). China benefits from this arrangement because the USA provides a ready market for its exports. Many US importing firms and consumers also benefit because they gain access to cheap components and consumer goods.

However, other US manufacturing firms and the workers they employ do not benefit. Unless these firms move out of the USA and relocate in countries with cheap labour, they may be forced to go under. Either way, American workers lose their jobs.

To correct the deficit and save American jobs, the US government may resort to protectionism. In the past, the USA used its power to engage in various forms of covert or hidden protectionism, such as giving preferential defence contracts to aircraft manufacturers and subsidies to farmers. Such policies undoubtedly harm countries that sell goods to the USA.

If a smaller and less powerful country were to take protectionist action, it might suffer retaliation from other economies. However, the size and power of the USA generally make retaliation impractical. In recent years, the USA has aggressively demanded better trading terms by breaking WTO rules and introducing tariffs on imported goods from China and the EU. It has upset traditional allies Mexico and Canada and demanded the renegotiation of NAFTA to better suit US interests.

The USA has never really deflated its economy in order to correct its payment deficit. However, when the US economy does suffer from a downturn - for example, during the recessions in 2008 and 2009 - other countries have faced a sudden loss of export markets. There is a saying: "When America sneezes, the rest of the world catches a cold." The size of the US economy means that countries that export to the USA are highly dependent on it continuing to grow. A recession in the USA tends to mean that other countries import recession from it, which is clearly not what those countries want.

Competitive devaluation

As we have seen, another action a country can take to reduce a current account deficit is to devalue or encourage a depreciation of its exchange rate. If this policy is viewed by other countries as an attempt to gain at their expense, it might lead to retaliatory devaluations and to an exchange rate war from which nobody benefits.

Encouraging the dollar to fall has not always been an effective way of reducing the USA's balance of payments deficit. This is because other currencies, such as China's renminbi (RMB) or yuan, have at times been effectively "pegged" to the dollar. This means that if the dollar's exchange rate falls, so does the RMB's exchange rate.

Note that the official name for China's currency is the renminbi, but when talking about quantities of the currency it is referred to in terms of yuan. This is similar to "sterling" being the official name for the British currency but "pounds" being used to measure the quantity of the British currency.

China stunned financial markets in August 2015 by devaluing the RMB on two consecutive days in order to counter a slowdown in China's growth rate. This action occurred despite the fact that China had previously been reluctant to raise the RMB's exchange rate and lose its price competitive advantage. This was repeated in 2019, leading to accusations by President Trump of the Chinese government being a "currency manipulator".

In the case of the USA and China, the imbalance in the two countries' current accounts is largely resolved by large capital flows from China into the USA. For example, China has purchased large quantities of US government bonds. Today, China holds US Treasury bonds worth more than $1 trillion. These capital flows finance the US trade deficit. Indeed, the world as a whole is generally willing to "invest" in the USA, irrespective of the state of the US current account, because the US dollar is a reserve currency and is viewed as a "safe haven" for international investors.

Smaller countries

For a smaller country such as the UK, a downward float of the pound's exchange rate might be a viable method of reducing a current account deficit. A fall in the pound's exchange rate would probably have relatively little effect on other economies.

However, the effectiveness of a depreciation would depend on how big it was, on whether it provoked retaliation, and on the price elasticities of demand for the UK's exports and imports. A fall in the exchange rate might also provoke a "hot money" flow out of the pound, leading to a further fall in the value of the currency. This could destabilise the UK economy, triggering capital flight and financial instability.

Remember!

Key Points to Remember:

-

The current account affects aggregate demand: Changes in net exports (X - M) shift the AD curve, affecting national income, employment, and inflation. Export increases can help reflate a depressed economy but become inflationary at full capacity.

-

Deficits and surpluses have different implications: Persistent deficits suggest uncompetitiveness and can lower future living standards. However, surpluses also pose problems because one country's surplus must be another's deficit, and surpluses can cause domestic inflation.

-

The "3 Ds" for reducing deficits: Deflation (expenditure-reducing), Direct controls (expenditure-switching), and Devaluation (expenditure-switching). Each has different effects and limitations.

-

Devaluation effectiveness depends on elasticities: The Marshall-Lerner condition states that the sum of export and import price elasticities must exceed 1 for devaluation to improve the current account. The J-curve effect means the current account may worsen before it improves.

-

Long-term solutions require supply-side policies: Sustainable improvements in the current account depend on enhancing productivity and quality competitiveness through investment in R&D, education, and infrastructure. Export-led growth is more sustainable than consumption-led growth, which tends to increase imports and create unsustainable debt.