Perfect Competition (AQA A-Level Economics): Revision Notes

Perfect Competition

Introduction to perfect competition

Perfect competition is a theoretical market structure that rarely exists in the real world. However, it serves an important purpose in economics. It provides a benchmark or yardstick against which we can measure the desirable and undesirable properties of actual markets.

While no real-world market meets all six conditions of perfect competition simultaneously, the model helps economists to:

- Judge whether monopolies function efficiently or inefficiently

- Assess the extent of resource misallocation in different market structures

- Evaluate how well markets serve consumers

By understanding perfect competition, you can better analyse the three other main market structures: monopoly, monopolistic competition, and oligopoly.

The invisible hand of the market

In 1776, economist Adam Smith introduced the concept of the 'invisible hand' in his book An Inquiry into the Nature and Causes of the Wealth of Nations. Smith argued that individuals pursuing their own self-interest in competitive markets would unintentionally promote the public good.

Smith wrote that an individual:

intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was no part of his intention.

This means that when individuals act in their own economic interest within competitive markets, they are guided—as if by an invisible hand—to produce outcomes that benefit society as a whole.

Key argument: In free and competitive markets, the pursuit of individual self-interest leads to lower prices and higher profits being competed away. This benefits consumers more than if markets were dominated by a few large firms.

Self-interest in competitive markets

Traditional economic theory assumes that everyone is motivated by self-interest. This applies equally to firms in competitive markets as it does to monopolies. However, in perfectly competitive markets, competitive forces and market information channel self-interest into socially beneficial outcomes.

Entrepreneurs in competitive industries want to:

- Make life easier for themselves

- Earn bigger profits

- Potentially eliminate competition and become monopolies

But in perfect markets, the invisible hand of the market—combined with the absence of barriers to entry and exit—prevents this from happening. Market forces ensure that:

- Technical breakthroughs that reduce costs create temporary profits

- Information spreads quickly to all firms and consumers

- New entrants are attracted by short-term abnormal profits

- Lower prices ultimately benefit consumers

- Competition prevents any single firm from dominating

This illustrates why highly competitive markets are considered optimal, even if they cannot achieve the socially benign motives that might drive some entrepreneurs.

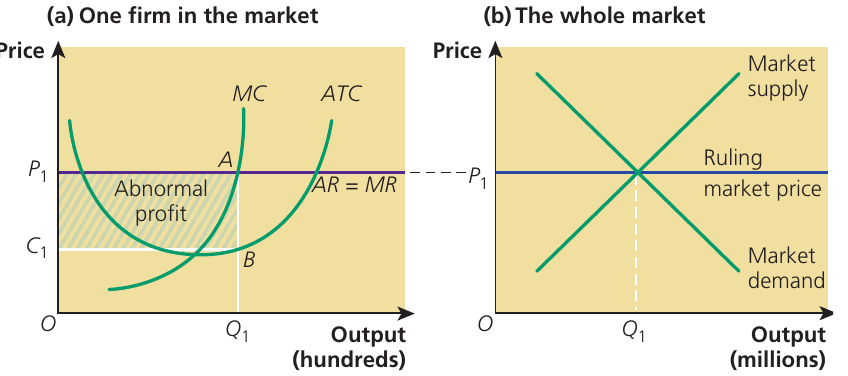

Short-run profit maximisation in perfect competition

In the short run, firms in perfect competition can make abnormal profits (also called supernormal profits). This occurs when the market price is high enough that it exceeds the firm's average total cost.

How firms maximise profit in the short run

A perfectly competitive firm is a price-taker. This means it must accept the ruling market price determined by supply and demand in the whole market. The market price becomes the firm's average revenue (AR) and marginal revenue (MR), which are equal and represented by a horizontal line.

Profit Maximisation Rule

To maximise profit, the firm produces at the output level where marginal revenue equals marginal cost:

At this point, the firm cannot increase profit by producing more or less output.

Understanding the diagram:

- Panel (a) shows an individual firm

- Panel (b) shows the whole market

- The ruling market price is determined where market supply meets market demand

- This price becomes the firm's line

- The firm produces at (hundreds of units) where

- The shaded area between price and cost represents abnormal profit

- Abnormal profit =

Why abnormal profit occurs

Abnormal profit exists in the short run because:

- Price is greater than average total cost (ATC) at the profit-maximising output

- The firm covers all its costs and has revenue left over

- Barriers to entry (in the short run) prevent new firms from immediately entering the market

- The firm produces efficiently at the output where

However, this situation cannot continue indefinitely in a perfectly competitive market.

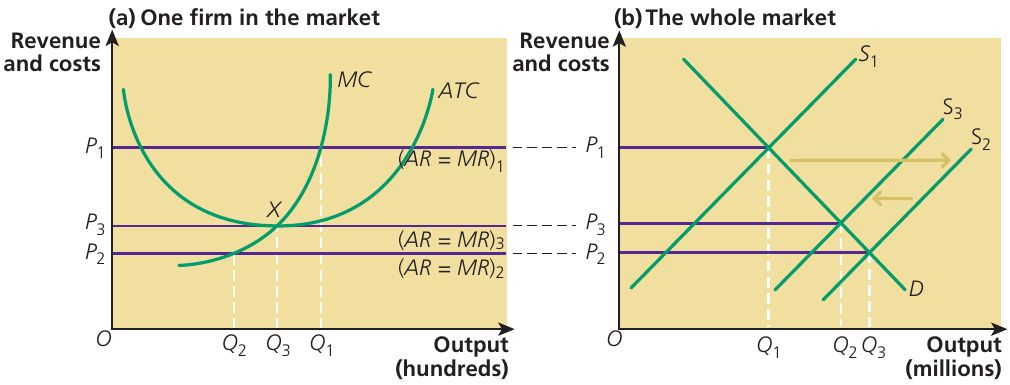

Long-run profit maximisation in perfect competition

In the long run, abnormal profits are eliminated through the entry of new firms into the market. This is because perfect competition assumes freedom of entry and exit in the long run.

The adjustment process from short run to long run

When firms make abnormal profits in the short run, this signals to firms outside the market that profits are available. New firms then enter the market, causing the following chain of events:

The Entry and Exit Mechanism:

- New firms enter attracted by abnormal profits

- Market supply increases as more firms produce (supply curve shifts right from to to )

- Market price falls from to to eventually

- Abnormal profits decrease as price falls closer to average total cost

- Entry continues until price equals ATC and only normal profit remains

Conversely, if firms make subnormal profits (losses), the opposite happens:

- Firms exit the market

- Market supply decreases (shifts left)

- Price rises back toward ATC

- Losses are eliminated

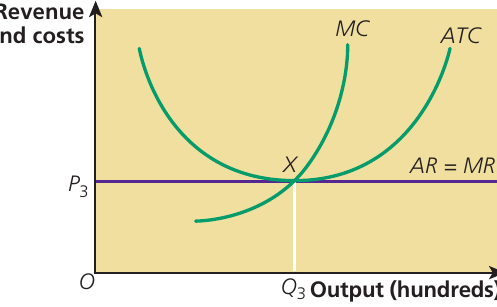

Long-run equilibrium: normal profit only

In long-run equilibrium, surviving firms make normal profit only. Normal profit occurs when:

- Price (P) equals average total cost (ATC)

- Total revenue exactly covers all costs of production

- There is no incentive for firms to enter or leave the market

- The firm produces at output where

Important point: Normal profit is treated as a cost of production. It represents the minimum return necessary to keep factors of production (including entrepreneurship) in their current use. Since only normal profit is made, there is no incentive for entry or exit.

Why firms are price-takers

A perfectly competitive firm can be described as a passive price-taker. This means:

- The firm has no control over the market price

- It must accept the ruling market price determined by market supply and demand

- If it tries to charge above the market price, it will sell nothing (consumers can buy identical products elsewhere)

- If it charges below the market price, it loses revenue unnecessarily

- The firm can sell all its output at the market price

In the short run, a price-taking firm can make abnormal profits if the market price is high. In the long run, entry of new firms drives the price down until only normal profits remain.

Perfect competition and the efficient allocation of resources

Perfect competition achieves two important types of economic efficiency: productive efficiency and allocative efficiency. Understanding these concepts is essential for evaluating market performance.

Productive efficiency in perfect competition

Productive efficiency occurs when a firm produces at the lowest possible cost per unit of output. This happens at the minimum point on the average total cost (ATC) curve.

In perfect competition, firms achieve productive efficiency in long-run equilibrium because:

- Firms produce at output (immediately below point X on the cost curve)

- This is the lowest point on the ATC curve

- Average cost per unit is minimised

- No waste of resources occurs in production

- Competition forces firms to eliminate unnecessary costs to survive

For the whole economy, productive efficiency means it is impossible to produce more of one good without producing less of another. All points on the economy's production possibility frontier demonstrate productive efficiency.

Exam tip: When firms produce at the bottom of their ATC curve (the minimum point), they achieve productive efficiency. This is sometimes called cost minimisation.

Allocative efficiency in perfect competition

Allocative efficiency occurs when it is impossible to improve overall economic welfare by reallocating resources between markets. This requires that price equals marginal cost () in every market.

Why P = MC indicates allocative efficiency

Understanding allocative efficiency requires examining what price and marginal cost represent:

Price (P) measures:

- The value in consumption that buyers place on the last unit consumed

- The utility or satisfaction obtained at the margin

- The opportunity cost in consumption (what buyers sacrifice when purchasing)

Marginal cost (MC) measures:

- The value of resources used to produce the last unit

- The opportunity cost in production (the value of resources in their best alternative use)

The Allocative Efficiency Condition

When across all markets:

- The value consumers place on the last unit equals the cost of resources to produce it

- Resources are optimally allocated

- Consumer welfare is maximised

- No reallocation could improve overall welfare

How perfect competition achieves allocative efficiency

In long-run equilibrium, perfectly competitive firms are both productively and allocatively efficient because:

- Firms produce where (price equals marginal cost)

- Firms also produce at minimum ATC (productive efficiency)

- These two conditions occur simultaneously at the long-run equilibrium point

However, this conclusion requires several important qualifications:

- All firms must benefit from all available economies of scale

- Perfect competition must exist for all goods and services (including future markets)

- must hold simultaneously in every market throughout the world

- No externalities (positive or negative) can exist

Since these conditions are impossible to achieve in reality, perfect competition serves as a theoretical ideal rather than a practical outcome.

Allocative inefficiency explained

Allocative inefficiency occurs when resources are poorly allocated between markets, causing welfare loss.

Two scenarios create allocative inefficiency:

Scenario 1: When P > MC (price exceeds marginal cost)

- Too little of the good is produced and consumed

- The value consumers place on additional units exceeds the cost of producing them

- Welfare would increase if more resources were allocated to this market

- This situation is under-production

Scenario 2: When P < MC (price is less than marginal cost)

- Too much of the good is produced and consumed

- The cost of producing the last units exceeds the value consumers place on them

- Welfare would increase if fewer resources were allocated to this market

- This situation is over-production

Resources should be reallocated from markets where to markets where . As reallocation proceeds:

- Prices fall in markets receiving more resources (moving into which resources shift)

- Prices rise in markets losing resources (moving from which resources shift)

- Eventually, is achieved in all markets, establishing allocative efficiency

Important note: Allocative efficiency assumes the distribution of income and wealth remains constant. The outcome maximises welfare given the initial distribution, but different distributions would produce different efficient outcomes.

Limitations of perfect competition as a model

Although perfect competition is valuable as a theoretical benchmark, it has significant limitations when compared to real-world competitive markets.

Competition beyond price

In perfect competition, the only form of competition available to firms is price competition. Firms cannot engage in:

- Advertising campaigns

- Product differentiation

- Brand development

- Packaging improvements

- After-sales service

- Quality variations

These forms of competition would destroy the conditions of perfect competition, particularly:

- Homogeneous products (all products must be identical)

- Perfect information (consumers must view all products as identical)

- Large number of firms (branding creates market power)

However, in real-world imperfectly competitive markets, firms use these methods extensively. This suggests that non-price competition may benefit consumers through:

- Greater product choice

- Innovation and quality improvements

- Better information about products

Cost-cutting competition and technical progress

One questionable aspect of perfect competition is the incentive for cost-cutting research. In a perfectly competitive market:

- Each firm has an incentive to reduce costs to make abnormal profit

- However, perfect information means all firms instantly know about cost reductions

- Other firms quickly adopt the same techniques

- New firms are attracted to the market by temporary abnormal profits

- Abnormal profits from innovation are only temporary

The problem: Why would firms finance research and development into cost-cutting technology when:

- They cannot maintain any competitive advantage

- Other firms have instant access to the same information

- Any abnormal profits resulting from innovation are quickly competed away

This raises doubts about whether perfect competition truly encourages technical progress and innovation.

The nature of choice in perfect competition

From a consumer's perspective, perfect competition offers a paradox:

- The choice appears "very broad and very narrow" simultaneously

- Consumers have maximum choice in the number of firms or suppliers (many firms exist)

- However, consumers have no choice at all in terms of product differentiation

- Each firm supplies an identical good or service at exactly the same price

- There is no meaningful choice between suppliers if products are truly homogeneous

In this sense, perfect competition eliminates real consumer choice between differentiated products, brands, or service quality—the very things consumers often value in actual markets.

Key Points to Remember:

-

Perfect competition is a theoretical model used as a benchmark to judge real-world markets, though no actual market meets all six conditions simultaneously.

-

In the short run, perfectly competitive firms can earn abnormal (supernormal) profits when price exceeds average total cost, producing where .

-

In the long run, the entry of new firms eliminates abnormal profits, driving price down until firms earn only normal profit (where ).

-

Productive efficiency is achieved when firms produce at the lowest point on their average total cost curve, minimising cost per unit.

-

Allocative efficiency requires that price equals marginal cost () in every market, ensuring optimal resource allocation. Perfect competition achieves this in long-run equilibrium, subject to significant qualifications.

-

Perfect competition assumes price competition only—no advertising, branding, or product differentiation—which limits its relevance to real-world competitive markets where these forms of competition are prevalent.