Perfectly Competitive Labour Markets (AQA A-Level Economics): Revision Notes

Perfectly Competitive Labour Markets

Introduction

In a perfectly competitive labour market, the forces of supply and demand work together to determine wage rates and employment levels. Understanding how these markets operate provides a theoretical foundation for analysing real-world labour markets, even though perfect competition rarely exists in practice.

What is a perfectly competitive labour market?

A perfectly competitive labour market would need to satisfy several strict conditions simultaneously. These conditions mirror those required for perfectly competitive goods markets:

- Large number of buyers and sellers: Many employers (buyers of labour) and many workers (sellers of labour) operate in the market

- No individual influence on wages: No single employer or worker can affect the ruling market wage through their own actions

- Perfect information: All employers and workers have complete knowledge about wage rates, working conditions, and job opportunities

- Free entry and exit: Workers and employers can enter or leave the labour market in the long run without barriers

- Homogeneous labour: Workers possess identical skills and productivity levels

In reality, perfectly competitive labour markets do not exist. However, some markets come close to meeting these conditions. For example, the market for fruit pickers in a region with many orchards may approximate perfect competition, though it still falls short of being truly perfectly competitive.

Key terminology

Understanding two important cost concepts is essential for analysing firm behaviour in labour markets:

Average cost of labour (ACL): This represents the total wage costs divided by the number of workers employed. It tells us the average wage paid per worker.

Marginal cost of labour (MCL): This is the additional cost a firm incurs when employing one more worker. In a perfectly competitive labour market, this equals the wage rate because each additional worker receives the same wage.

How the ruling market wage affects perfectly competitive firms

In a perfectly competitive labour market, individual firms behave very differently from how they might in less competitive markets. Each firm acts as a passive price-taker at the ruling market wage. This means the firm must accept the wage determined by market forces and cannot influence it through its own actions.

Just as a firm in a perfectly competitive goods market faces a perfectly elastic demand curve, a firm in a perfectly competitive labour market faces a perfectly elastic supply curve of labour. This horizontal supply curve exists at the ruling market wage rate.

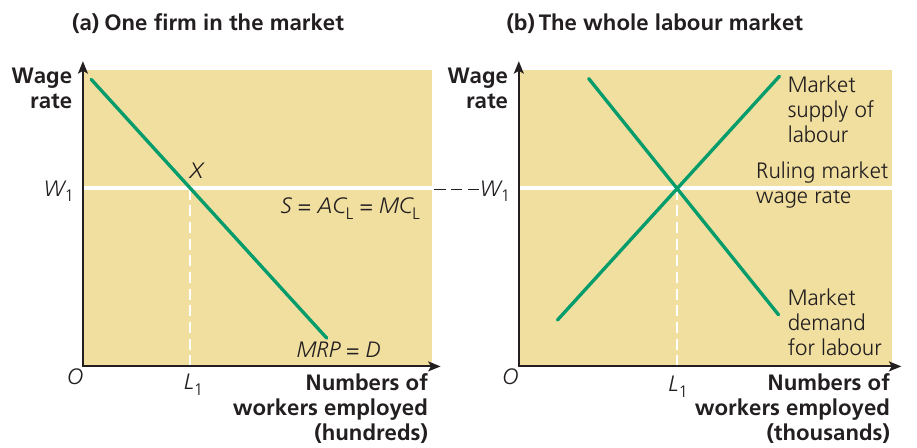

Understanding the Two Perspectives

The diagram above illustrates a key distinction between the individual firm's perspective and the whole market perspective:

-

Panel (a) shows one firm in the market. The firm faces a horizontal supply curve at wage , meaning it can hire as many workers as it wishes at this wage rate. The firm cannot influence the wage - it either pays or cannot attract workers. This horizontal line represents both the average cost of labour (ACL) and the marginal cost of labour (MCL) for the firm.

-

Panel (b) shows the whole labour market. Here, the upward-sloping market supply curve intersects the downward-sloping market demand curve to determine the equilibrium wage . This is the wage that all individual firms must accept.

In this market structure, each firm can buy as much labour as it wants at the ruling market wage. The firm chooses the quantity of labour to employ, but not the price (wage) it pays.

Equating MRPL with the wage rate

To maximise profit, firms must make careful decisions about how many workers to employ. The key principle involves comparing the benefits and costs of hiring additional workers.

The profit maximisation condition

A profit-maximising firm will demand labour up to the point where:

The Profit Maximisation Rule

The addition to sales revenue from employing an extra worker = The addition to production costs from employing an extra worker

This can be expressed more formally as:

Where:

- MRPL = Marginal revenue product of labour (the extra revenue generated by hiring one more worker)

- MCL = Marginal cost of labour (the extra cost of hiring one more worker)

In a perfectly competitive labour market, the marginal cost of labour always equals the wage rate paid to workers. Therefore, the profit-maximisation condition becomes:

Decision rules for employment

This profit-maximisation condition leads to three important decision rules that guide employment decisions:

- If MRP > W: The firm should hire more workers because each additional worker adds more to revenue than to costs, increasing total profit

- If MRP < W: The firm should employ fewer workers because additional workers add more to costs than to revenue, reducing total profit

- If MRP = W: The firm is employing the optimal number of workers consistent with profit maximisation

Understanding these rules helps explain why firms choose particular employment levels. A firm will continue hiring workers as long as each additional worker contributes more to revenue than their wage cost.

The role of market forces in determining relative wage rates

In a perfectly competitive labour market, market forces establish the equilibrium wage that all employers must pay. Once the market determines this wage, individual employers become passive wage-takers at the market-determined rate.

Market equilibrium

Looking at panel (b) of the diagram, the equilibrium wage occurs where the market supply curve of labour intersects the market demand curve for labour. Market forces operating across the whole labour market establish this ruling wage rate. Each worker in the market then becomes a passive wage-taker at this market-determined wage.

The law of one price

The Law of One Price in Labour Markets

An important principle applies here: identical goods should sell for the same price in two separate markets, assuming both markets are close to perfect competition. Applied to labour markets, this means workers with the same skills performing similar tasks should receive the same wage rates.

However, in the real world, this rarely happens. Real-world markets are imperfectly competitive to varying degrees. Even if most conditions of perfect competition were met, differences in skills and productivity, combined with changes in demand for different groups of workers, mean wage rate differences persist.

Remember!

Key Points to Remember:

-

A perfectly competitive labour market requires many buyers and sellers, no individual influence on wages, perfect information, and free entry in the long run - conditions that rarely exist in reality

-

Individual firms in perfect competition are passive wage-takers facing a perfectly elastic labour supply curve at the market-determined wage

-

The profit maximisation condition for employment is MRPL = W, where firms hire workers up to the point where marginal revenue product equals the wage rate

-

Market equilibrium occurs where market supply and demand for labour intersect, determining the ruling wage that all firms must accept

-

In theory, workers with identical skills should receive the same wage (law of one price), but real-world imperfections mean wage differences persist