Money and interest rates (OCR A-Level Economics): Revision Notes

5.1 Money and interest rates

DEFINITIONS:

- Liquidity: when you turn an asset into cash easily and quickly without losing its value

- Narrow Money (MO): The physical currency in circulation and balances held in checking accounts and other forms of highly liquid assets.

- Broad Money (M4): Includes all of Narrow Money (MO) plus wholesale and retail transactions made with financial institutions

- The Credit Creation multiplier: a process by which an increase in money supply can have a multiplier effect on the amount of credit available in the economy.

Explain:

5.1.1 Functions and characteristics of money

Functions of Money:

- Medium of Exchange: Money is widely accepted in exchange for goods and services, facilitating transactions without the need for a barter system.

- Unit of Account: Money provides a standard measure of value, allowing individuals to compare the worth of various goods and services.

- Store of Value: Money can retain its value over time, enabling individuals to save and defer consumption until a later date.

- Standard of Deferred Payment: Money allows for transactions involving credit, where payment can be made in the future.

Characteristics of Money: 5. Durability: Money must withstand physical wear and tear so it can be used repeatedly. 6. Portability: Money should be easily transportable, allowing individuals to carry it and use it for transactions. 7. Divisibility: Money should be divisible into smaller units to facilitate transactions of varying sizes. 8. Uniformity: Each unit of money should be identical to others, ensuring consistent value. 9. Acceptability: Money must be widely accepted as a form of payment by people within the economy. 10. Limited Supply: To maintain its value, the supply of money must be limited and controlled.

5.1.2 The creation and supply of money

Money Creation:

- Central Banks: Central banks, such as the Bank of England, are primarily responsible for creating money. They do this through monetary policy tools like open market operations, where they buy government bonds, injecting liquidity into the banking system.

- Commercial Banks: When commercial banks issue loans, they create money. This process is known as fractional-reserve banking. Banks only keep a fraction of deposits as reserves and lend out the rest, creating new deposits and, thus, new money.

- Quantitative Easing: This is a policy used by central banks to increase the money supply by purchasing long-term securities from the open market, increasing the amount of money in circulation.

Money Supply:

- Monetary Aggregates: The supply of money is measured using different monetary aggregates like M0 (base money), M1 (cash and liquid assets), and M2 (M1 plus short-term deposits). These aggregates provide a view of the total money available in the economy.

- Money Multiplier Effect: The money multiplier effect describes how an initial deposit can lead to a greater final increase in the total money supply. It depends on the reserve ratio, the proportion of deposits banks must hold in reserve. A lower reserve ratio leads to a higher money multiplier.

- Interest Rates: Central banks influence the money supply through interest rates. Lowering interest rates makes borrowing cheaper, encouraging spending and investment, which increases the money supply. Conversely, raising interest rates has the opposite effect.

5.1.3 Narrow and broad money in terms of liquidity

Narrow Money (M0 or M1):

- Definition: Narrow money includes the most liquid assets in the economy. It comprises currency in circulation (notes and coins) and demand deposits (current accounts) that can be quickly and easily converted into cash.

- Liquidity: Highly liquid because these assets can be used immediately for transactions without any loss of value.

Broad Money (M2, M3, or M4):

- Definition: Broad money includes all the components of narrow money plus other less liquid assets. These can include savings accounts, time deposits, and money market mutual funds.

- Liquidity: Less liquid than narrow money because these assets may require some time or incur a cost to convert into cash. However, they still play a significant role in the money supply and can be used for transactions with some effort.

5.1.4 The relationship between the money supply and the price level; Fisher equation of exchange

In economics, the relationship between the money supply and the price level is primarily explained through the Quantity Theory of Money. This theory suggests that there is a direct relationship between the quantity of money in an economy and the level of prices of goods and services sold.

The Fisher equation can be represented by the equation:

where:

- is the money supply

- is the velocity of money (the rate at which money circulates in the economy)

- is the price level

- is the output or quantity of goods and services produced in the economy

According to this theory, if the velocity of money (V) and the output (Q) remain constant, an increase in the money supply (M) will lead to a proportional increase in the price level (P). This means that more money in the economy will result in higher prices, leading to inflation. Conversely, a decrease in the money supply will lead to deflation.

The Fisher equation emphasises that the price level is influenced by the money supply and the velocity of money, assuming that the volume of transactions remains constant. If M increases and V is stable, P will increase, leading to inflation. If M decreases, P will decrease, resulting in deflation, assuming Y and V remain constant.

The key insight from the Fisher equation is that it accounts for the total number of transactions in the economy, providing a more comprehensive understanding of how changes in the money supply affect the overall price level.

Explanation with the aid of a diagram

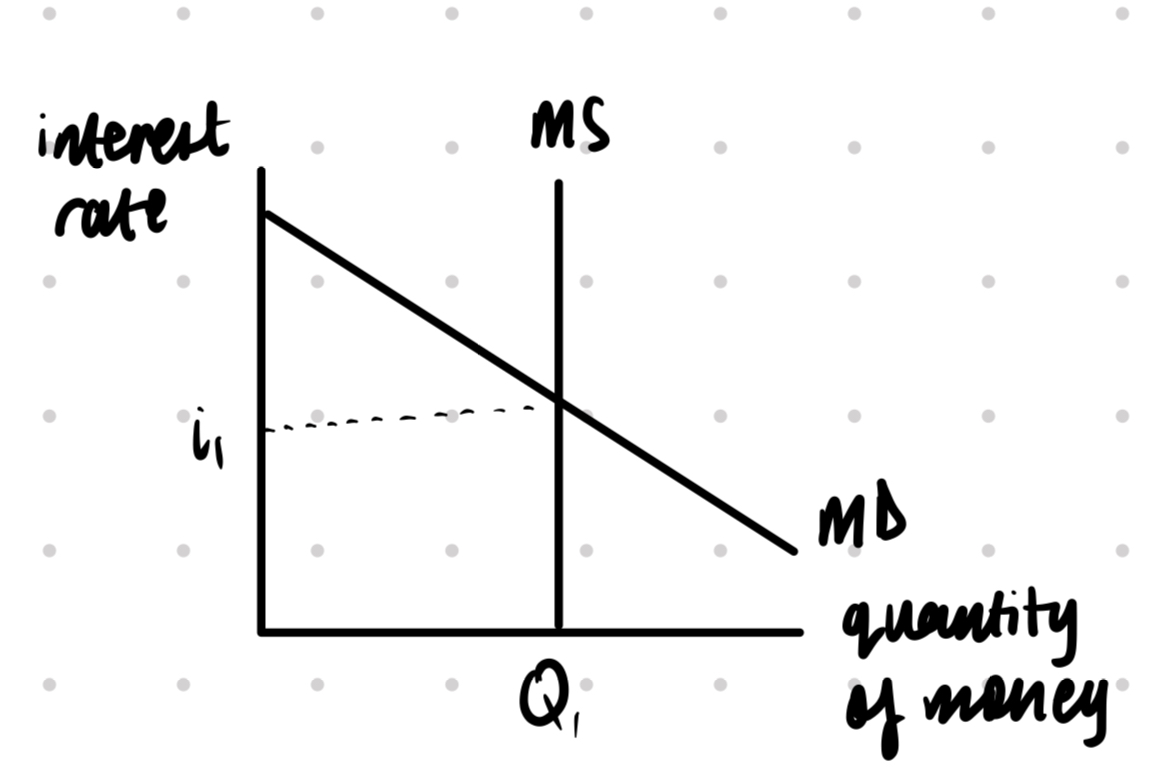

5.1.5 Determination of Interest Rates

Interest rates are determined by the interaction of demand and supply for loanable funds in the financial markets. The equilibrium interest rate is where the quantity of loanable funds demanded equals the quantity supplied.

Key Concepts:

- Demand for Loanable Funds: Borrowers demand loanable funds for investment purposes. The demand curve for loanable funds is downward-sloping, indicating that at lower interest rates, more funds are demanded.

- Supply of Loanable Funds: Savers supply loanable funds. The supply curve for loanable funds is upward-sloping, indicating that at higher interest rates, more funds are supplied.

Factors Affecting Demand:

- Investment Opportunities: More profitable investment opportunities increase demand for loanable funds.

- Economic Growth: Higher economic growth can lead to increased demand for funds as businesses expand.

- Government Borrowing: Increased government borrowing can shift the demand curve to the right.

Factors Affecting Supply:

- Savings Rate: Higher savings rates increase the supply of loanable funds.

- Monetary Policy: Central bank policies can influence the supply of money, thereby affecting the supply of loanable funds.

- Foreign Capital Inflows: Inflows of foreign capital can increase the supply of loanable funds.

Diagram:

- Interest Rate (i): The price of borrowing funds, typically represented on the vertical axis.

- Quantity of Loanable Funds (Q): The total amount of funds available for borrowing, represented on the horizontal axis.

- Demand Curve (D): Downward-sloping, indicating that lower interest rates lead to higher quantities of loanable funds demanded.

- Supply Curve (S): Upward-sloping, indicating that higher interest rates lead to higher quantities of loanable funds supplied.

- Equilibrium (E): The point where the demand and supply curves intersect, determining the equilibrium interest rate (i*) and quantity of loanable funds (Q*).

Summary:

The determination of interest rates involves the interaction of the demand and supply for loanable funds. Various economic factors can shift these curves, influencing the equilibrium interest rate. At equilibrium, the amount of loanable funds demanded equals the amount supplied, setting the interest rate in the market.