Exchange Rate Systems (AQA A-Level Economics): Revision Notes

Exchange Rate Systems

Introduction to exchange rates

An exchange rate is the external price of one currency expressed in terms of another currency. It tells us how much of one currency we can buy with another.

When countries trade internationally, they need to exchange currencies. Although domestic currencies are used for internal trade within countries, imports are typically paid for in the currency of the exporting country. For example, if a UK business wants to buy goods from the United States, it will need to obtain US dollars to pay for them.

Exchange rates are determined in the foreign exchange market, which is now a global, 24-hour electronic market. This market never closes, and trading takes place continuously around the world through computer systems.

How exchange rates are measured

In the UK, we typically express the exchange rate as how much foreign currency one pound sterling will buy. For example, if the exchange rate is £1 = €1.18, this means that one pound will buy 1.18 euros.

When the exchange rate rises, the pound buys a larger quantity of foreign currency. This is called currency strengthening or appreciation. When the exchange rate falls, the pound buys less foreign currency. This is called currency weakening or depreciation (or devaluation in fixed exchange rate systems).

Worked Example: Converting Exchange Rates

If the exchange rate is £1 = $1.50, what would $1 be worth in pounds?

Solution: To convert this, we need to find the reciprocal of the rate:

Therefore, $1 = £0.67 (to the nearest penny).

The sterling exchange rate index

The sterling exchange rate index (ERI) provides a broader measure of the pound's value. Rather than measuring the pound against just one currency, the ERI is a trade-weighted average of the pound's exchange rate against multiple leading trading currencies. This calculation reflects the importance of each currency in the UK's international trade.

As the UK's trade patterns change over time (such as after Brexit, with potentially less trade with the EU and more with other countries), the ERI adjusts to reflect these new trading relationships. This makes it a more comprehensive measure of currency strength than comparing against a single currency.

| Year | Exchange rate index (2021 = 100) |

|---|---|

| 2020 | 96 |

| 2021 | 100 |

| 2022 | 106 |

| 2023 | 102 |

This table shows how the pound's value changed over a four-year period. With 2021 as the base year (index = 100), we can see the pound was weaker in 2020 (index = 96), stronger in 2022 (index = 106), but then weakened slightly by 2023 (index = 102).

Nominal vs real exchange rates

The exchange rates we have discussed so far are nominal exchange rates - the actual market prices we see quoted. However, these don't account for differences in inflation between countries.

The real exchange rate measures the value of a currency adjusted for inflation. It's calculated using this formula:

The real exchange rate is important because it measures a country's competitiveness. If the domestic price level rises by 10% but the foreign price level remains unchanged, and the nominal currency depreciates by 10%, the real exchange rate stays unchanged. The country hasn't gained any competitive advantage because the fall in the exchange rate has been exactly offset by higher domestic inflation.

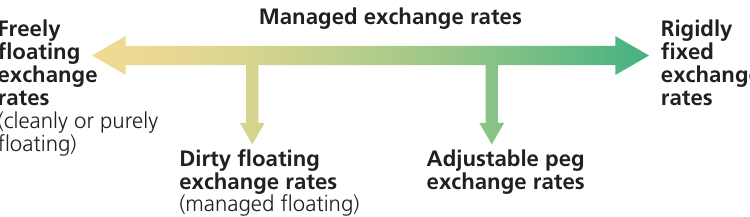

The different types of exchange rate system

There are several ways countries can manage their exchange rates. These systems exist on a spectrum from complete market freedom to complete government control.

The two extreme types are:

- Freely floating exchange rates (also called cleanly or purely floating) - where market forces alone determine the exchange rate

- Rigidly fixed exchange rates - where the government or central bank maintains the exchange rate at a specific value

Between these extremes lie managed exchange rates, which take two main forms:

- Adjustable peg exchange rates - similar to fixed rates but the central peg can be changed from time to time through devaluation or revaluation

- Dirty floating exchange rates (or managed floating) - officially floating but with central bank intervention to influence the rate

Freely floating exchange rates

How floating exchange rates work

In a freely floating exchange rate system, the external value of a currency is determined entirely by market forces - the demand for and supply of the currency on foreign exchange markets. There is no government or central bank intervention.

To understand how floating rates work, we first need to simplify by assuming that currencies are demanded and supplied purely for trade purposes. While this isn't entirely realistic in today's world (where capital flows and speculation are hugely important), it provides a clear foundation for understanding the basic mechanism.

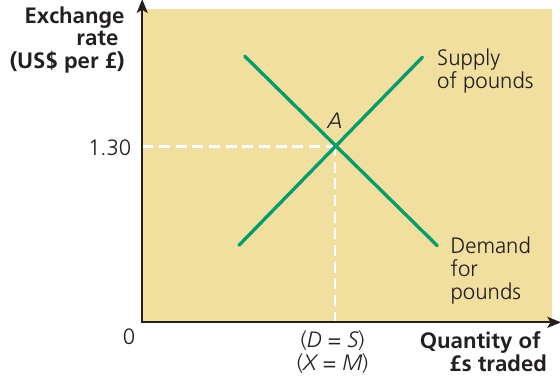

The demand and supply curves for pounds

Why demand for pounds slopes downward:

When the pound's exchange rate falls, UK exports become more price competitive in overseas markets. The volume of UK exports increases, creating greater demand for pounds from foreign buyers who need sterling to purchase these exports. This explains the downward-sloping demand curve - at lower exchange rates, more pounds are demanded.

Why supply of pounds slopes upward:

As the pound's exchange rate rises, fewer pounds are needed to buy any given amount of foreign currency. This means the sterling price of imports falls. UK consumers respond by buying more imports (assuming demand is price elastic), leading to a greater total quantity of sterling being supplied to foreign exchange markets to pay for these imports. This creates the upward-sloping supply curve - at higher exchange rates, more pounds are supplied.

Exchange rate equilibrium

Exchange rate equilibrium occurs at the market-clearing rate where the demand for pounds equals the supply of pounds on foreign exchange markets. In the diagram above, this happens at point A, where the exchange rate is $1.30 to the pound.

At this equilibrium exchange rate, the money value of exports (paid in sterling) equals the money value of imports (paid in foreign currencies). Assuming exports and imports are the only items in the current account, this means the current account of the balance of payments is in balance - there's no surplus or deficit.

Once the balance of payments reaches equilibrium, there's no pressure for the exchange rate to rise or fall. The market is in a stable position.

This assumes we're ignoring capital flows. In reality, exchange rate equilibrium means balance of payments equilibrium on both the current account and capital/financial accounts combined.

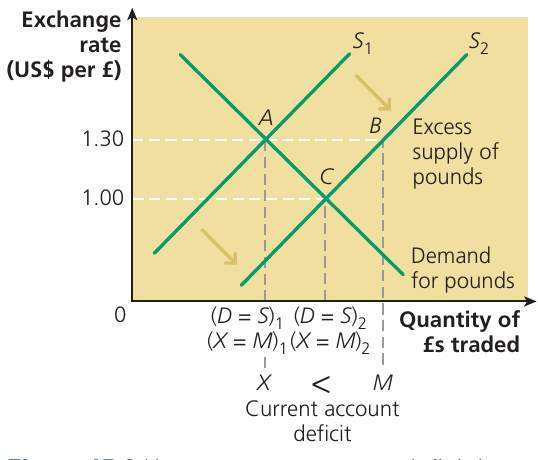

The adjustment process to a new equilibrium

What happens when something disturbs this equilibrium? Let's consider an example where the quality of foreign-produced goods improves, causing UK residents to demand more imports.

In this diagram, the increase in demand for foreign goods to pay for imports causes the supply curve of pounds to shift rightward from to . At the original exchange rate of $1.30, there's now an excess supply of pounds (shown by the distance from point A to point B). The current account has moved into deficit because (exports are less than imports).

The market mechanism now works to restore equilibrium:

- The excess supply of pounds causes the exchange rate to fall

- As the rate falls, UK exports become more price competitive while imports become more expensive

- UK residents buy fewer foreign goods, reducing the supply of pounds

- Foreign buyers purchase more UK goods, increasing the demand for pounds

- The process continues until a new equilibrium is reached at point C, where the exchange rate is $1.00 to the pound

At this new equilibrium, the current account is back in balance (), but at a lower exchange rate. Both the physical quantities of exports and imports have increased, but their money values are once again equal.

The opposite process occurs if UK goods or services improve in quality. The demand curve for pounds shifts rightward, creating a current account surplus. This causes the exchange rate to rise or appreciate until balance is restored at a higher exchange rate.

Advantages of floating exchange rates

Economists generally agree that floating exchange rates offer several important advantages, assuming there are no distorting capital flows:

Automatic balance of payments adjustment:

The exchange rate should move up or down automatically to correct any payments imbalance. If market adjustment works smoothly, currencies should never be significantly overvalued or undervalued for long periods.

An overvalued currency is one where the market exchange rate is above its long-term purchasing power parity (PPP) level. This causes export uncompetitiveness and a payments deficit. With floating rates, market forces should quickly push the exchange rate down towards its equilibrium, restoring balance.

Similarly, an undervalued currency should be corrected by an upward movement of the exchange rate. This automatic adjustment mechanism is a key advantage - it means the balance of payments "takes care of itself."

This depends on trade being the main determinant of exchange rates. In today's world, many currency transactions are for speculative purposes (short-term "hot money" flows) rather than trade. This can mean a country has both a rising current account deficit and a rising or stable currency at the same time.

Improving resource allocation:

For the world's resources to be efficiently allocated between competing uses, exchange rates must be correctly valued. Market prices need to accurately reflect shifts in demand and changes in competitive advantage from technical progress, new resource discoveries, and other developments.

A freely floating exchange rate should respond and adjust to these changes quickly. By contrast, a fixed exchange rate may gradually become overvalued or undervalued as demand patterns and competitive advantages shift between countries. Different inflation rates between countries also cause fixed exchange rates to lead to resource misallocation over time.

Freedom to achieve domestic policy objectives:

When the exchange rate floats freely, balance of payments surpluses and deficits are no longer a policy problem for the government. Market forces automatically "look after" the current account. This frees the government to focus on domestic economic policy objectives such as full employment and economic growth.

If inflation is higher domestically than in other countries, the exchange rate simply falls in a floating system to restore competitiveness. The government doesn't need to intervene.

Making it easier to control inflation:

A floating exchange rate can help insulate a country against "importing inflation" from the rest of the world. If inflation rates are higher globally, a fixed exchange rate would force the country to import this inflation through rising import prices.

By contrast, with a floating exchange rate, the currency appreciates when foreign inflation is higher. This lowers the domestic price of imports, protecting the economy from external inflationary pressures.

Ability to pursue an independent monetary policy:

With a floating exchange rate, monetary policy can be used purely to achieve domestic objectives like controlling inflation. This is called independent monetary policy or "monetary sovereignty."

With a fixed exchange rate system, interest rates may be determined by external factors - particularly by capital flows in and out of currencies - rather than by domestic economic needs. To maintain a fixed rate, interest rates may need to be raised to prevent the exchange rate from falling, even if this conflicts with domestic policy objectives.

In a fixed system, domestic policy objectives are often sacrificed to maintain the exchange rate target. But with floating rates, monetary policy remains independent and can be assigned to domestic goals.

Disadvantages of floating exchange rates

Despite their advantages, freely floating exchange rates have some significant drawbacks, particularly in the modern globalised economy where financial capital is highly mobile:

The adverse effects of speculation and capital flows:

The argument that floating rates are never significantly overvalued or undervalued depends on currencies being bought and sold only to finance trade. This assumption is unrealistic. Today, over 90% of foreign exchange transactions are capital flows and speculative trades, not trade-related.

In the short run, exchange rates are extremely vulnerable to speculative capital movements or "hot money" flows. Just like a fixed rate, a floating rate can become overvalued or undervalued when speculation dominates. This means it doesn't accurately reflect the competitiveness of the country's goods and services.

Speculators buy currencies they perceive to be undervalued to make capital gains when rates rise later. They sell currencies they think are overvalued to avoid losses when rates fall in the future.

Arguably, fixed exchange rates are even more vulnerable to speculation. This is because speculators can enjoy a "one-way option" - they can profit by buying back the currency at a lower rate if devaluation occurs, but if devaluation doesn't happen, they can buy it back at roughly the same rate. This was a key factor in the pound being forced out of the European Exchange Rate Mechanism in 1992.

International trading uncertainty:

Some argue that fixed exchange rates create conditions of certainty and stability that help international trade prosper and grow. The volatility and instability of floating rates may slow or even damage international trade.

The prospect of frequent exchange rate changes means companies cannot be sure how much domestic currency they'll need to pay for imports or receive from exports. This uncertainty may deter them from trading internationally, leading to misallocation of resources and reduced living standards.

In reality, hedging - buying or selling currency in the forward market in advance of actual delivery - reduces trading uncertainties from floating rates. However, fixed and managed rates can also create uncertainty when over- or undervaluation leads to expectations of devaluation or revaluation.

Floating exchange rates may cause cost-push inflation:

Floating exchange rates can contribute to cost-push inflation if a country has higher inflation than its trading partners:

- Trade competitiveness and the current account worsen, causing the exchange rate to fall

- This triggers a vicious downward spiral of faster inflation and exchange rate depreciation

- The falling exchange rate raises import prices, increasing domestic cost-push inflation

- Workers demand higher wages to restore their eroded real wages

- Higher inflation further erodes export competitiveness initially gained from the rate fall

- This causes another fall in the exchange rate, and the cycle continues

- The downward spiral can destabilise the economy, causing unemployment and reduced growth

Floating exchange rates may also cause demand-pull inflation:

Floating rates can trigger demand-pull inflation alongside cost-push inflation. With a floating rate, there's no need to deflate the domestic economy to deal with a balance of payments deficit.

If many countries simultaneously increase aggregate demand, this can lead to excess demand globally, fuelling inflation. This happened in the 1970s when worldwide demand expansion created conditions for oil and primary goods producers to raise prices while still selling in world markets. For countries like the UK, this appeared to be import cost-push inflation from rising energy and raw material costs.

However, the true cause was excess demand from the simultaneous effects of demand expansion and floating exchange rates, which prevented world supply from increasing to meet the surge in global demand. Floating rates allowed individual governments to over-inflate their economies without the exchange rate falling to discipline them.

By contrast, commitment to a fixed exchange rate prevents a government from adopting excessively expansionary monetary policy, because the resulting inflation would cause the balance of payments to deteriorate and put downward pressure on the rate. To prevent this, interest rates must be raised, dampening inflationary pressures.

Fixed exchange rates

What is a fixed exchange rate?

With a freely floating system, a currency's external value rises or falls to eliminate balance of payments surpluses or deficits. With a rigidly fixed exchange rate, the currency's external value remains unchanged while the internal price level (or level of domestic economic activity and output) adjusts to eliminate balance of payments disequilibrium on current account.

There are few examples of truly fixed exchange rates today. Modern "fixed" exchange rates are better thought of as adjustable peg exchange rates - we'll explain this shortly.

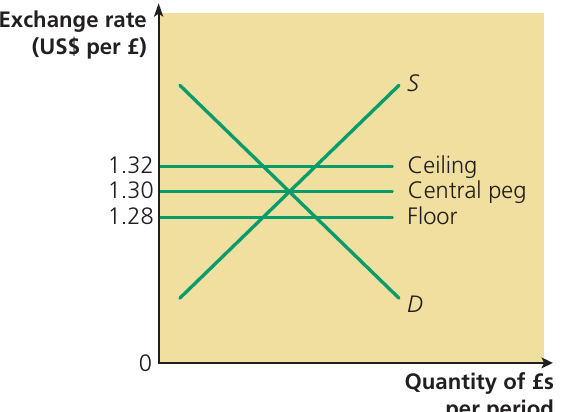

Key features of a fixed exchange rate

This diagram illustrates how a fixed exchange rate system operates:

-

The government or central bank announces the exchange rate is being fixed at a particular rate (the central peg, central rate, parity or par value)

-

The central bank simultaneously announces ceiling and floor limits just above and below the central peg

-

Market forces (supply and demand) determine the day-to-day exchange rate within this band

-

Provided the rate stays between the ceiling and floor, central bank intervention isn't needed

-

If market forces push the rate towards the ceiling or floor, the central bank intervenes to prevent it breaking through these limits

Worked Example: Understanding Exchange Rate Bands

If the pound's central peg is $1.30, the ceiling might be $1.32 and the floor $1.28. As long as the rate stays within this band, the system works without intervention.

How governments intervene to maintain fixed exchange rates

Central banks have two main methods to maintain fixed exchange rates:

Method 1: Exchange equalisation

If the exchange rate threatens to rise above the ceiling, the central bank sells its own currency on the foreign exchange market. This offsets excess demand for the currency that would otherwise push up the rate.

If the rate threatens to fall below the floor, the central bank buys its own currency on the market. By creating artificial demand, this prevents excess supply from pushing the rate below the floor.

This policy of buying and selling currencies to support an exchange rate is called exchange equalisation.

Method 2: Interest rate changes

The second method uses interest rates. To keep the pound's exchange rate between a ceiling and floor (say $1.32 and $1.28), the Bank of England adjusts domestic interest rates.

Lower interest rates might cause international holders of pounds to sell sterling and buy other currencies, putting downward pressure on the pound's exchange rate. If this threatens to push the rate below the floor, interest rates are raised to attract "hot money" capital inflows back into the pound.

Conversely, higher interest rates attract short-term capital inflows, raising demand for pounds and potentially pushing the rate above the ceiling. Lower interest rates can then discourage these inflows.

The Bank of England intervenes frequently to manage the sterling exchange rate.

In reality, both intervention methods are likely to be used together, especially during exchange rate crises when large capital flows threaten to destabilise the fixed rate.

A crucial point: When supporting a fixed exchange rate, the central bank may not be able to change interest rates to achieve purely domestic macroeconomic objectives like economic growth and low unemployment. Monetary policy freedom is sacrificed to maintain the exchange rate target.

The freedom to use monetary policy for domestic objectives is sacrificed for supporting a fixed exchange rate. This is probably why fixed exchange rates are rare today and why floating rates have become the norm.

In 2023, around 30 countries still maintained formally or informally fixed exchange rates - most pegged to either the euro or the US dollar (particularly in Latin America).

Advantages of fixed exchange rates

The advantages and disadvantages of fixed rates closely mirror those of floating rates:

- Fixed rates attempt to achieve certainty and stability in foreign exchange markets

- They impose anti-inflationary discipline on a country's domestic economic management and on workers' and firms' behaviour

Disadvantages of fixed exchange rates

The principal disadvantages are:

- Fixed rates may increase uncertainty rather than create certainty, particularly if devaluation or revaluation is expected in the near future

- If significantly overvalued, a fixed rate may impose severe deflationary costs of lost output and unemployment unless corrective action (devaluation) is taken

- If significantly undervalued, inflation may be imported from the rest of the world unless corrective action (revaluation) is taken

- An independent monetary policy cannot be implemented

- There may be recurrent balance of payments or currency crises if the currency is overvalued

- Resources are tied up in official reserves (needed to support the fixed rate) that could be used more productively elsewhere

- Both overvaluation and undervaluation can lead to resource misallocation

Managed exchange rates

Between the extremes of freely floating and rigidly fixed exchange rates lie managed exchange rates - systems where governments intervene in foreign exchange markets to influence the currency's value, but don't maintain a completely rigid peg.

Adjustable peg exchange rates

An adjustable peg exchange rate is similar to a rigidly fixed rate, except the central bank can alter the rate's central peg through devaluation or revaluation.

These systems combine characteristics of fixed rates with some flexibility from floating rates. They lie closer to rigidly fixed rates than to freely floating rates on the exchange rate spectrum.

Adjustable pegs are more flexible than old fixed exchange rate systems (like the nineteenth-century gold standard). The exchange rate can be adjusted upward (revaluation) to correct undervaluation, or downward (devaluation) to correct overvaluation.

Nevertheless, adjustable pegs are less flexible than freely floating rates. Over time, exchange rates are likely to become over- or undervalued as countries experience different inflation rates. An upward revaluation corrects an undervalued rate, while a downward devaluation corrects overvaluation.

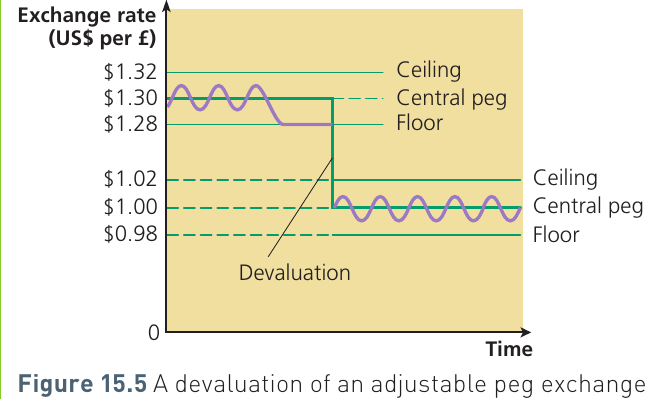

This diagram shows devaluation in an adjustable peg system. The exchange rate is initially fixed at a central peg of $1.30 (with a ceiling of $1.32 and floor of $1.28).

The rate remains within the permitted band at first. But persistent support for the currency means it's overvalued, condemning the country to overpriced exports, underpriced imports and a persistent current account deficit.

With a rigidly fixed system, the country would have to deflate the domestic economy and/or impose import controls, since devaluation and revaluation aren't permitted.

However, this diagram shows the Bank of England devaluing the exchange rate to a new central peg of $1.00 (with ceiling $1.02 and floor $0.98) to correct the fundamental imbalance. This illustrates the key difference between adjustable peg and rigidly fixed systems.

If a country makes frequent changes to the central peg, the benefits of a fixed rate are lost. The exchange rate becomes similar to a freely floating rate in its effects.

Managed-floating or dirty-floating exchange rates

Fixed and adjustable peg systems have been largely abandoned globally. Most exchange rates now float, though there's a difference between "clean floating" and "dirty floating."

Clean floating is the same as freely floating - no central bank intervention to manipulate the rate.

Managed floating or dirty floating occurs when the exchange rate is officially floating, but monetary authorities intervene unofficially behind the scenes, buying or selling currency to influence the rate.

Countries worldwide admit they "manage" their floating rates. Currently no countries operate a truly free-floating system with no central bank intervention at all.

At the time of writing (July 2022), it's probably true to say that for the period since September 1992 (when the pound left an adjustable peg system within the European Union), the pound's exchange rate has floated more or less freely. Nevertheless, the Bank of England intervenes daily as part of a "smoothing operation" to iron out temporary fluctuations in the pound's exchange rate.

In recent years, the UK has experienced two major currency crises. After the 2008 financial crisis, sterling lost approximately 25% of its value against the US dollar; and after the Brexit referendum on 23 June 2016, the pound lost approximately 15% of its value against the dollar.

Currency unions, the euro and the eurozone

Currency unions

The United Kingdom comprises multiple countries, but all use the pound as a common currency. Likewise, the 50 US states plus the District of Columbia all use the US dollar.

Both the UK and USA are examples of currency unions - groups of countries using or sharing a single currency. A currency union is often called a monetary union.

A currency union is an agreement between a group of countries to share a common currency, and usually to have a single monetary and foreign exchange rate policy.

The euro and the eurozone

In the 1990s, the UK (then an EU member state) was given the choice of keeping its own currency or adopting the common European currency. If the UK had chosen the latter, it would have replaced the pound with the euro and joined what became known as the eurozone.

The euro came into existence on 1 January 2002 when euro notes and coins entered circulation. However, economists usually date the euro's introduction as 1 January 1999, because this was when the exchange rates of the 12 countries that became the first eurozone members were irrevocably fixed against each other.

The Treaty of the European Union (Maastricht Treaty) in the early 1990s began the process of creating monetary union within the eurozone. At the time, monetary union was considered necessary for two reasons:

-

Although the Single European Act had created almost completely free internal trade in goods and services, the need to exchange national currencies increased transaction costs. A single currency was deemed necessary to complete the single market.

-

To function effectively, a currency union typically requires a single monetary and foreign exchange rate policy. When countries join a monetary union, they lose control of their own independent monetary policy.

Case study: Devaluation of the pound and UK economic performance

Currency devaluation can be used by governments to reduce current account deficits and stimulate economic growth. In recent decades, three significant devaluations of the pound have occurred, each affecting UK economic performance differently.

The pound's ejection from the Exchange Rate Mechanism in 1992

The Exchange Rate Mechanism (ERM) was a system of adjustable peg exchange rates set up by the European Union in 1979, preparing for eventual economic union within the EU.

Having initially opposed ERM membership, the UK joined the system in 1990 at a substantially overvalued exchange rate. On 16 September 1992, the UK government was forced to abandon its economic policy and withdraw the pound from the ERM - a currency system designed to stabilise exchange rates among member countries.

When the pound joined the ERM in 1990, the objective was to eliminate inflation from the economy by forcing UK firms to make efficiency savings and become price competitive in world markets. However, this harmed the UK economy in two painful ways:

-

The strong currency made imports cheap but exports expensive. Although this helped reduce UK inflation, firms struggled to survive in world markets.

-

The Bank of England raised interest rates to attract "hot money" flows and maintain the high exchange rate. This put households with high mortgage debt under tremendous pressure and restricted consumer spending.

When market forces compelled the UK government to devalue the pound in 1992, the economy was in deep recession, largely caused by the pound's overvaluation. The forced devaluation was seen as a national humiliation - the day it occurred (16 September 1992) was nicknamed "Black Wednesday." The rising influence of "Euro-scepticism" dates from this era.

However, immediately after devaluation, the economy began to grow. The low exchange rate made UK exports price competitive, and in following years the UK's unemployment rate fell and the current account deficit was eliminated. Between 1992 and 1997, ONS statistics show exports increased by 53% and the economy grew by 15.2%.

The departure from the ERM also had significant implications for UK monetary policy. The Bank of England no longer needed to maintain high interest rates to support a fixed exchange rate, so interest rates fell significantly, reducing borrowing costs for firms and households. Looser monetary policy created better conditions for increased consumer spending and business investment.

The Great Recession, 2008 and 2009

In summer 2008, the dollar exchange rate was £1 = $2.00. Then the banking crisis shook the world. The UK's banking system was at the centre of the worst economic crisis since the 1930s, and the pound crashed. "Hot money" flowed out of the pound seeking safety in other currencies. By January 2009, the exchange rate had fallen to £1 = $1.30.

To stimulate the domestic economy, the Bank of England slashed Bank Rate to 0.5%, and in 2009 it started the unorthodox monetary policy of quantitative easing. The fall in the exchange rate and record low interest rates with massive injections of electronic money into the economy should, according to conventional economic theory, have stimulated the economy.

However, it took seven years for the UK economy to recover from the recession. After 2009, economic growth was weak and UK firms failed to experience increased demand in export markets. The current account deficit remained high, only reducing to 2% of GDP in 2011, two years after devaluation. Fiscal austerity at home and the eurozone crisis abroad were major reasons why UK recovery was so weak. However, the devaluation of sterling eventually stimulated the economy similarly to the earlier devaluations.

After the Brexit referendum in 2016

Following publication of the 2016 Brexit referendum result, the pound's exchange rate fell against both the dollar and the euro. In January 2016, the rate was £1 = $1.45. A year later in January 2017, it had fallen to £1 = $1.20.

The devaluation had two predictable outcomes: cost-push inflation squeezed living standards (CPI inflation in the two-year period after devaluation increased to over 3% a year), but the current account deficit changed very little.

External shocks and the fall in the value of the pound

Many financial investors view the US dollar as a "safe" investment - it's still seen as the global reserve currency that can be held as a safe store of financial capital (the dollar generally holds its value and is highly unlikely to lose value over short time periods).

As a result, when there's a global external shock, the dollar generally rises as investors seek the safe currency for short-term capital holdings. This increase in the dollar's value automatically means other currencies lose value against it.

In early 2020 as Covid-19 news emerged, and in 2022 due to the Ukraine crisis, the pound lost about 10% of its value against the dollar. It recovered the loss after the first occasion, but at the time of writing has not yet recovered from the second shock.

Some conclusions

The devaluations of 2008 and 2016 affected UK economic performance differently from the earlier 1992 devaluation. In 1992, export competitiveness rapidly improved, export-led growth occurred, and the economy recovered quickly. By contrast, the falls in the pound's value in the later cases didn't lead to strong export-led growth or elimination of the current account deficit.

This difference was partly because the nature of global capitalism in the twenty-first century has changed. Modern global supply chains now require that goods and services which UK firms export are priced in US dollars and euros, not in UK pounds.

As a result, a fall in the pound's value has limited effect on the price competitiveness of UK exports. The 2008 and 2016 devaluations or depreciations of the pound didn't significantly boost exports or decrease imports. The evidence appears to show that these devaluations brought limited gains for UK exporters, while inflicting painful imported inflation on UK households.

Key Points to Remember:

-

Exchange rates can be freely floating (determined by market forces), fixed (maintained by central bank intervention), or managed (somewhere between these extremes).

-

Floating exchange rates automatically adjust to correct balance of payments imbalances through changes in the currency's external value. They offer policy freedom but can be volatile and vulnerable to speculation.

-

Fixed exchange rates attempt to provide stability and certainty, but require governments to sacrifice independent monetary policy. They can become overvalued or undervalued, requiring eventual devaluation or revaluation.

-

Central banks intervene in fixed systems through exchange equalisation (buying or selling currency) and interest rate changes. In modern managed floating systems, intervention occurs unofficially to smooth out fluctuations.

-

Currency unions like the eurozone involve countries sharing a common currency and monetary policy. Member countries lose the ability to use exchange rate changes or independent monetary policy to respond to economic challenges, which can be both an advantage (stability) and disadvantage (lack of flexibility).