Structure of Financial Markets and Financial Assets (AQA A-Level Economics): Revision Notes

Structure of Financial Markets and Financial Assets

Introduction to the UK monetary economy

The UK operates as a monetary economy. This means that most goods and services produced are bought and sold using money as the medium of exchange. Understanding how money works, how financial markets are structured, and what types of financial assets exist is essential for understanding how the modern economy functions and how monetary policy operates.

A monetary economy is fundamentally different from a barter economy. In a monetary economy, money acts as an intermediary in all transactions, making trade far more efficient and enabling the specialization and large-scale production that characterize modern economies.

Assets and liabilities

To understand financial markets properly, you need to grasp the concepts of assets and liabilities.

An asset is a resource (physical or otherwise) that can be sold for money. Assets have value and can generate income or be converted into cash.

A liability is an amount owed by a business or individual. Liabilities can be current (short-term, due within one year) or non-current (long-term, due after more than one year).

The Dual Nature of Financial Instruments

The same financial instrument can be both an asset and a liability, depending on who owns it. This is a crucial concept in understanding financial markets.

For example, a £10 banknote is an asset for the person holding it because it gives them £10 worth of spending power. However, it is a liability for the Bank of England that issued it. In the past, when Bank of England notes were convertible into gold, the Bank had to meet this liability by converting banknotes into gold on demand if requested. This convertibility ended in 1931. Today, the Bank's liability is simply to replace old, worn notes with new ones.

The concept of assets and liabilities also applies to bank deposits and loans. When a commercial bank grants a loan to a customer, this creates an asset for the bank (the credit it extends). The borrower is liable to repay this loan with interest. However, when the bank creates this credit, it also simultaneously creates a bank deposit owned by the customer. This deposit is the customer's asset, but it is a liability for the bank, which must honour cash withdrawals and payments drawn on the deposit.

How Banks Create Money

When banks create loans, they create both assets (the loans themselves) and liabilities (customer deposits) at the same time. This process is fundamental to understanding how the banking system creates money in the modern economy.

The functions of money

Money plays a central role in modern economies. It is best understood by examining its two primary functions.

Medium of exchange (means of payment)

The economy we live in is a monetary economy. Goods and services are traded or exchanged through the use of money, rather than through barter (swapping goods directly). Before money existed, people had to rely on barter, which required a double coincidence of wants. This meant that someone wanting to trade a television for a refrigerator would need to find someone with a refrigerator who specifically wanted a television. This was highly inefficient.

The Problem with Barter

The double coincidence of wants created a significant obstacle to trade. Both parties in a transaction had to want exactly what the other was offering, at exactly the same time. This severely limited the scope and frequency of trade, making large-scale economic activity virtually impossible.

Money solves this problem by acting as a medium of exchange. When money is used to pay for goods or services, or to settle debts, it performs this crucial function. Money enables specialisation, trade, and large-scale production, all of which contribute to economic efficiency in modern monetary economies.

Store of value (store of wealth)

Money is also an asset that people own and value. People can store some of their wealth in the form of money rather than spending it immediately. This function allows money's purchasing power to be transferred to the future.

Money is often preferred as a store of value over other financial assets (such as shares) or physical assets (such as property) because it is the most liquid asset. However, over time, inflation may erode money's purchasing power, reducing its effectiveness as a store of wealth.

Other functions of money

Money also serves two additional, though less critical, functions:

-

A measure of value: Money provides a unit in which the prices of goods are quoted and in which accounts are kept. This allows us to compare the relative values of different goods even when we have no intention of actually buying them.

-

A standard of deferred payment: Money enables people to delay paying for goods or settling debts. Firms often sell goods on credit or establish contracts with money payments due at a later date. Money acts as the standard in which these future obligations are measured.

Together, these four functions are sometimes called the 'unit of account' function of money.

The characteristics and evolution of money

Understanding how money developed helps explain its essential characteristics.

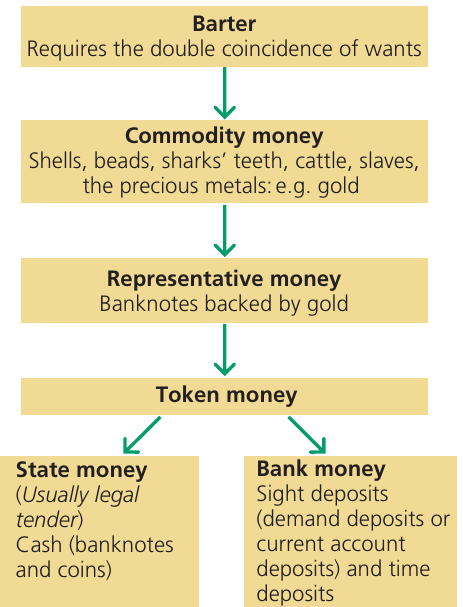

The evolution from barter to modern money

Money has evolved through several stages:

-

Barter: The direct swapping of goods and services. This required a double coincidence of wants and was highly inefficient.

-

Commodity money: Items that had intrinsic value were used as money. Examples include shells, beads, cattle, slaves, and precious metals (especially gold). These commodities could serve both as money and for their own utility (for example, gold for jewellery).

-

Representative money: Banknotes backed by gold. These notes represented ownership of gold held by banks and could be exchanged for gold on demand. This form of money was more convenient than carrying gold but still derived its value from the gold it represented.

-

Token money: Modern money with no intrinsic value. Token money has value only because people accept it as a means of payment. It divides into:

- State money (usually legal tender): Cash in the form of banknotes and coins issued by the government or its agent (the Bank of England)

- Bank money: Sight deposits (demand deposits or current account deposits) and time deposits created by the banking system

The Nature of Modern Money

Almost all modern money is token money with no intrinsic value. It functions as money only because people are confident that others will accept it as payment. This confidence, rather than any physical backing, is what gives modern money its value.

Characteristics that money must possess

For a commodity or token to function effectively as money, it needs certain characteristics:

- Relative scarcity: It must not be so abundant that it is unlimited in supply (otherwise it cannot be forged or counterfeited easily)

- Uniformity: Each unit must be identical to enable easy comparison

- Durability: It must last a reasonable amount of time without deteriorating

- Portability: It must be capable of being transported easily by individuals

- Divisibility: It must be capable of being divided into smaller units to facilitate transactions of different values

Why These Characteristics Matter

These characteristics help create confidence in money, which is essential for its acceptability. People must be confident that others will accept money as payment. This confidence is crucial in modern economies, where token money has no intrinsic value. People accept banknotes and coins because they are confident that these tokens will be accepted when they decide to spend them.

The development of representative and token money

As money evolved, gold and silver gradually replaced other forms of commodity money because they possessed the desirable characteristics to a greater degree. However, precious metals were vulnerable to theft and difficult to store securely. Wealthy individuals deposited their gold with goldsmiths for safekeeping.

Goldsmiths developed into banks, and the receipts they issued for gold deposits became the first banknotes or paper money. These notes were representative money, representing ownership of gold or silver. Early banknotes were acceptable as payment because they could be exchanged for gold or silver on demand. They were issued initially by privately owned banks rather than by the state.

Although worthless in themselves, banknotes functioned as money because people were willing to accept them, confident that notes could be exchanged for gold. Banknotes have an intrinsic value only in the sense that they are seen as valuable in themselves, rather than just being assigned a value.

Modern token money

Almost all modern money is token money with no intrinsic value of its own. It takes two main forms:

-

Cash (state money): Notes and coins issued by the Bank of England (in England and Wales). The Bank of England has a monopoly over issuing cash, although Scottish and Northern Ireland banks have limited ability to issue banknotes. However, cash is only the 'small change' of the monetary system.

-

Bank deposits (bank money): Money placed in banks to be stored for later use. Bank deposits created by the private banking system form by far the largest part of modern money.

Most modern money takes the form of bank deposits created by commercial banks through their lending activities.

The money supply

What is the money supply?

The money supply (or stock of money) refers to the stock of financial assets which function as money in the economy. In the past, when monetarism was the prevailing economic orthodoxy (1970s to mid-1980s), economists paid considerable attention to defining and controlling the money supply. Today, while still important, there is less focus on precise definitions.

Narrow money and broad money

Over the years, the Bank of England has used different definitions of the money supply. These divide into measures of narrow money and broad money.

Narrow money restricts the measure of money to cash and liquid bank and building society deposits. It reflects the medium of exchange function of money, namely money functioning as a means of payment. In the UK, narrow money is called M0 or M1.

Broad money includes cash and other liquid financial assets, but also includes some illiquid assets. Although these less liquid assets function as stores of value, they are too illiquid, at least for the time being, to function effectively as media of exchange. In the UK, the measure of broad money used by the Bank of England is called M4.

In the 1980s, different measures of the money supply were closely watched when macroeconomic policy was guided by monetarism. There were many measures, all with code names. For example, M0 and M1 were narrow money measures, while M3 and M4 focused on the broad money supply.

The concept of liquidity

Liquidity measures the ease with which an asset can be converted into cash without loss of value. Cash itself is the most liquid of all assets because it is already in the form required for transactions.

Understanding Liquidity

It is important to understand the meaning of 'liquidity' in the context of money and financial markets. Liquidity measures the ease with which an asset can be converted into cash without loss of value. Cash is the most liquid of all assets. Assets that generally can only be sold after a long, exhaustive search for a buyer (such as houses and cars) are known as illiquid.

Liquidity is also affected by whether the conversion can take place at a pre-known value. A share issued by a public limited company (PLC) is highly liquid in that it can quickly be sold on the stock exchange, but less liquid in the sense that the seller does not know the price the asset will fetch in advance of the sale. The value of a share can rise or fall depending on how desirable that share is at the time of sale.

Bank deposits are not quite as liquid as cash, but they are sufficiently liquid to be treated as money. The other financial assets shown in the spectrum of assets (which we will examine shortly) are less liquid than bank deposits, being examples of non-money financial assets in some cases near-money.

Equity and debt

Understanding the difference

Many people in the UK own possessions such as furniture, cars, or even houses. They may also own financial assets such as money, shares, and bonds. Even children may own equity in the form of toys or savings accounts given to them by grandparents.

Equity refers to all the assets (both physical and financial) that people own. It represents wealth.

Debt, by contrast, refers to people's financial liabilities, or the money that they owe. For many adults, this includes mortgages on their houses (money owed to a bank or building society) and credit card debt.

Shares

Shares are undated financial assets initially sold by a company to raise financial capital. Shares sold by public limited companies (PLCs) are marketable on a stock exchange, meaning they can be bought and sold on the secondary market. However, shares sold by private limited companies (Ltds) are not marketable in this way.

Unlike a loan, a share signifies that the holder owns part of the enterprise. Share ownership gives the holder certain rights, including the right to receive dividends (if the company makes profits) and the right to vote at company meetings.

Bonds

Bonds are financial securities sold by companies (corporate bonds) or by governments (government bonds) as a form of long-term borrowing. Bonds represent debt that must be repaid.

Bonds usually have a maturity date on which they are redeemed, with the borrower making a fixed interest payment (called a coupon) each year until the bond matures. When the bond reaches its maturity date, the face value is repaid to the bond holder.

Government bonds in the UK are known as gilt-edged securities or gilts. These are bonds issued by the government and sold as new issues to people who lend long term to the government. They can also be resold second hand on a stock exchange.

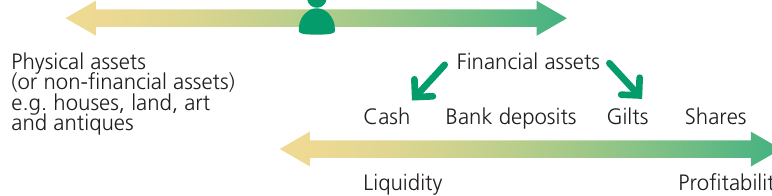

Portfolio balance decisions

People and institutions make decisions about the form of assets in which to hold their wealth. This involves portfolio balance decisions. When choosing assets, people balance between:

- Physical assets (non-financial assets): such as houses, land, art, and antiques

- Financial assets: such as cash, bank deposits, gilts, and shares

Financial assets themselves vary across a spectrum. At one end, cash is highly liquid but earns little or no interest. At the other end, shares and gilts are less liquid but generally hold out the prospect of providing a profit through capital gains and dividend or interest payments.

For most people, bank deposits offer a good balance - they are sufficiently liquid to be treated as money, providing accessibility for transactions, while also offering some return (though modest) on savings. The most liquid financial assets are cash and bank deposits. Other financial assets, including shares and government bonds, are marketable but less liquid than money.

Financial markets

What are financial markets?

Financial markets are markets in which financial assets or securities are traded. As with any market, financial markets are a voluntary meeting of buyers and sellers. Markets do not have to exist in a particular geographical location. Many financial markets have become truly global in recent years, facilitated by the internet, and function on a worldwide basis 24 hours a day, 7 days a week.

Some financial markets (such as capital and foreign exchange markets) function globally, including Lloyd's insurance market. At the other extreme, smaller financial markets (such as those for Treasury bills and commercial bills) are restricted largely to trading in the City of London, the financial centre containing many of the UK's financial markets.

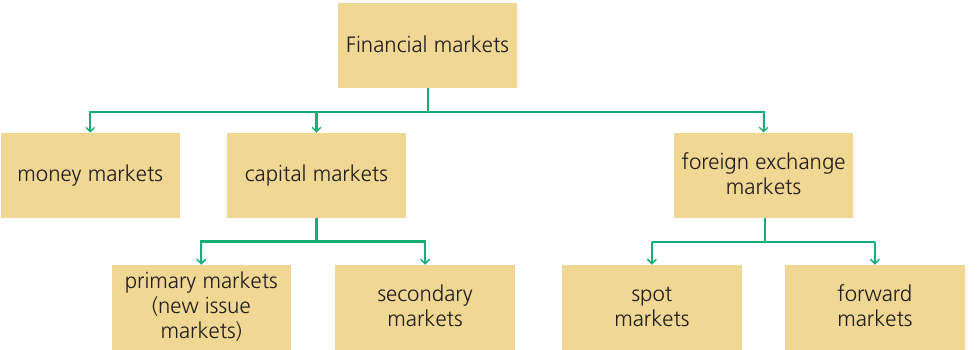

Classification of financial markets

Financial markets can be classified into three main categories:

- Money markets: for trading short-dated financial assets or securities

- Capital markets: for trading long-dated debts and shares

- Foreign exchange markets: for financial transactions requiring the use of foreign currency

Each of these main categories can be further subdivided. Capital markets divide into:

- Primary markets (new issue markets): where new securities are first sold

- Secondary markets: where existing securities are traded

Foreign exchange markets divide into:

- Spot markets: for immediate exchange of currencies

- Forward markets: for exchange of currencies at a specified future date

Money markets

Purpose and function

Money markets provide a means for lenders and borrowers to satisfy their short-term financial needs. The term 'money market' covers several markets, including those for Treasury bills and commercial bills.

The Role of Money Markets

Money markets enable financial institutions to manage their liquidity and profitability by trading highly liquid assets such as Treasury bills and commercial bills. These short-term financial instruments help banks balance their need for liquid assets with their desire to earn returns.

Treasury bills

Treasury bills are short-dated government debt instruments, usually maturing within three months. They are issued by the government as a way to borrow money for the short term. The holder is paid a fixed rate of interest until redemption (when the bill matures and is repaid).

Treasury bills provide the government with a source of short-term finance. For a firm, bill finance offers an alternative to a conventional bank loan. Bills are short-dated financial assets or securities, maturing within a year (and often within three months) of their date of issue.

Commercial bills

Commercial bills are short-dated debt instruments (usually maturing within three months) issued by private businesses. The holder receives a fixed rate of interest until the bill matures.

Commercial bills are sold by investment banks on behalf of client firms. They provide businesses with a method of financing short-term cash flow needs.

The London interbank market

A money market that has become extremely important in the operation of monetary policy is the London interbank market. In this market, the LIBOR interest rate is charged. LIBOR (London Interbank Offered Rate) is the rate of interest charged when banks lend to each other, usually for very short periods of time. This market plays a crucial role in determining short-term interest rates throughout the economy.

Comparing money markets and capital markets

The table below summarises the key differences between money markets and capital markets:

| Money markets (markets for short-dated financial assets or securities) | Capital markets (markets for undated and long-dated financial assets or securities) | |

|---|---|---|

| The private sector raising finance | Sale of commercial bills | Sale of new issues of shares Sale of new issues of corporate bonds |

| Central government raising finance | Sale of Treasury bills | Sale of new issues of government bonds (in the UK also known as gilt-edged securities or gilts) |

Money markets supply both private-sector commercial firms and the government with short-term finance. Capital markets, by contrast, provide long-term finance through the sale of shares and bonds.

Capital markets

Purpose and function

Capital markets are markets where securities such as shares and bonds are issued to raise medium- to long-term financing. They enable companies and governments to raise funds for long-term growth and investment.

In contrast to money markets, capital markets provide mechanisms for long-term borrowing and investment. Public limited companies (PLCs), which are usually the largest business organisations in the UK, use capital markets to raise funds to finance their long-term growth.

The bond market, which is part of the capital market, also performs a critical role in government finance. It enables governments to finance budget deficits by borrowing long term from investors.

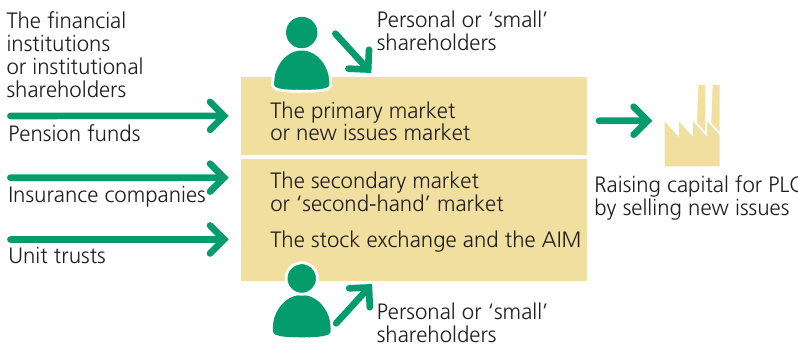

Primary markets and secondary markets

Capital markets consist of two parts:

Primary vs Secondary Markets

Primary markets (or new issue markets) are where new securities are first sold to the public. This is where the actual raising of new capital or long-term finance takes place. Companies and governments issue and sell new marketable securities in primary markets.

Secondary markets are where previously issued securities are bought and sold second hand. In the UK, the London Stock Exchange (LSE) functions as the main secondary market. There are, however, other secondary markets, including the Alternative Investment Market (AIM), which is run by the LSE mainly for small PLCs.

The role of secondary markets

The principal function of secondary markets is to increase the liquidity of second-hand securities (bonds and shares), making it easier for buyers to manage their investments and sell these securities when required.

Without the existence of a second-hand market, public companies and governments would find it difficult, if not impossible, to sell new share issues. Shares issued by private companies, which do not have a stock market listing, are generally illiquid and difficult to sell. But shares issued by listed public companies can be sold second hand on the stock exchange, enabling shares to be converted quickly into cash.

The stock exchange enables surplus funds from those willing to buy new issues of shares and bonds to flow into companies and government. This facilitates expansion in the economic activities of PLCs and government spending programmes.

Capital Markets vs Stock Exchanges

It is important not to confuse the capital market with the stock exchange. The stock exchange is an important part of the capital market, but it is only a part. The terms 'capital market' and 'stock exchange' are not interchangeable. Stock exchanges are venues where previously issued shares and bonds are sold second-hand as part of the secondary market.

Securities traded on capital markets

Three main types of security are traded on capital markets:

Shares represent equity ownership in a company. When you buy shares, you become a part-owner of that company. Shares are undated - they do not have a maturity date when they must be redeemed. Share prices fluctuate based on supply and demand, company performance, and broader economic conditions.

Corporate bonds are debt securities issued by companies and sold as new issues to people who lend long term to the company. They can also be resold second hand on a stock exchange. Corporate bonds have a maturity date and pay regular interest (coupon) payments.

Government bonds (gilt-edged securities or gilts) are debt securities issued by governments. In the UK, government bonds are known as gilts. Like corporate bonds, they have a maturity date and pay regular coupon payments. They are generally considered less risky than corporate bonds because governments are less likely to default on their debts.

The inverse relationship between bond prices and interest rates

Understanding bonds

A bond is a form of long-term borrowing. When issued, a bond has several key features:

- Issue price: the price at which the bond is first sold (often $100)

- Maturity price: the price at which the bond can be redeemed at maturity (also often $100)

- Maturity date: the date when the bond matures and is repaid

- Coupon: the guaranteed fixed annual interest payment, often divided into two six-month payments

- Issue date: when the bond is first issued

Gilts and corporate bonds are fixed-interest securities. This means that the government (or company) promises to pay the bearer of the bond a guaranteed annual interest payment. The guaranteed interest (or coupon) earned each year is paid in two instalments at six-month intervals.

The inverse relationship explained

The See-Saw Effect

There is an important inverse relationship between interest rates and bond prices. This means that:

- When interest rates rise, bond prices fall

- When interest rates fall, bond prices rise

This relationship is crucial for understanding bond markets and monetary policy.

Worked Example: Understanding Bond Prices and Yields

Suppose a government sells a new issue of 30-year gilt-edged securities with a nominal (face) value of $100 and a guaranteed yearly interest payment (coupon) of $5. This means the initial yield on the bond is 5% ($5 as a percentage of $100).

However, after the bond has been sold on its day of issue for $100, its second-hand price on the London Stock Exchange or bond market might rise to $200. This would cause the bond's yield to fall to 2.5% ($5 as a percentage of $200).

The bond's yield is effectively the long-run rate of interest earned by the holder. It is determined primarily by the coupon and the current market price paid for the bond.

Calculating yield

The yield is the annual interest on a bond expressed as a percentage of the bond's current market price.

The formula for calculating yield is:

Alternatively, we can rearrange this to find the bond's current market price:

Worked Example: Calculating Yield

If a bond has an annual coupon of $2.50 and its current market price is $50:

This shows that even though the bond only pays $2.50 per year, if you can buy it for $50 (rather than its original $100 face value), you're effectively earning a 5% return on your investment.

Capital gains and losses

Changes in bond prices create opportunities for capital gains (profits made on buying and selling assets) or capital losses (losses made on buying and selling assets).

Suppose the current bond price is $100, but speculators expect the price to rise shortly to $150. If the bond can be bought now at or near its current price of $100, and its price does indeed shortly rise, speculators who buy the bond earlier can make a capital gain when selling the bond later - for example, selling for $150. If a sufficiently large number of speculators decide to buy the bond at or near the price of $100, increased demand puts up the market price until eventually it may reach $150.

Conversely, a fear that the bond price will fall, say to $50, will induce speculative selling of the bond. This in turn causes the bond's price to fall. Provided a sufficiently large number of speculators behave in the same way, speculative buying and selling, in the hope of making a capital gain or avoiding a capital loss, becomes an important determinant of short-run changes in bond prices.

Share prices are affected in a similar way. Expectations of capital gains and the fear of suffering capital losses are important determinants of short-term changes in bond and share prices.

Foreign exchange markets

Foreign exchange markets (also known as forex, FX or currency markets) are global, decentralised markets for the trading of currencies. They are the largest markets in the global economy.

Over the last 60 years or so, foreign exchange markets have become increasingly important in facilitating the growth of international trade and capital movements between countries. International trade has been the main driver of economic growth in the world as a whole.

How foreign exchange markets work

Foreign exchange markets are financial markets in which different currencies are bought and sold. International trade means that exporters and importers need to convert the funds they use to finance trade from one currency to another. For example, UK exporters need to convert pounds sterling into euros, dollars, yen, rupees, and other currencies.

Foreign exchange can be traded on either:

- Spot markets: for immediate exchange of foreign currency

- Forward markets: for exchange of foreign currencies at a specified time in the future

Spot transactions involve the immediate exchange of foreign currency. Forward markets are used by, for example, exporters and importers to protect themselves against exchange rate risks. By agreeing a price today for a transaction that will occur in the future, businesses can reduce uncertainty about currency fluctuations.

The vast majority of foreign exchange deals in the modern globalised economy finance international capital investment rather than payments for exports and imports, though international trade itself has grown significantly.

Commercial banks and investment banks

The difference between commercial and investment banks

The main aim of almost all banks is to make profits for their owners. The Bank of England, the country's central bank, is an exception since its aims are primarily to oversee the financial system and to implement monetary policy.

The most commonly used way of classifying banks (other than the central bank) is into commercial banks and investment banks.

Commercial banks

A commercial bank (also known as a retail bank or high street bank) is a financial institution that aims to make profits by selling banking services to its customers.

Commercial banks are often also known as retail banks or 'high street' banks because they have branches on high streets serving retail customers. Examples in the UK include Barclays and HSBC. International examples include Deutsche Bank (in Germany) and JPMorgan Chase (in the USA).

Commercial banks provide services such as:

- Current accounts and savings accounts

- Loans and mortgages

- Credit cards and debit cards

- Foreign exchange services for personal customers

- Business banking services for small and medium-sized enterprises

Money Creation by Commercial Banks

Commercial banks create the majority of the money supply through their lending activities. When they grant loans, they simultaneously create bank deposits, which form the largest part of the modern money supply.

Remember!

Key Points to Remember:

-

Money has two key functions: as a medium of exchange (enabling trade without barter) and as a store of value (preserving wealth over time).

-

Modern money is token money: it has no intrinsic value but is accepted because people are confident others will accept it as payment.

-

Financial markets are classified into three types: money markets (short-term), capital markets (long-term), and foreign exchange markets (currency trading).

-

There is an inverse relationship between bond prices and interest rates: when interest rates rise, bond prices fall, and vice versa. This affects the yield on bonds.

-

Assets and liabilities are two sides of the same coin: a bank loan is an asset for the bank but a liability for the borrower; a bank deposit is an asset for the customer but a liability for the bank.