Public Expenditure and Taxation (AQA A-Level Economics): Revision Notes

Public Expenditure and Taxation

Introduction

Government spending and taxation are powerful fiscal policy tools that shape economic activity in the UK. When governments collect taxes, they obtain the revenue needed to fund essential public services like schools, hospitals, and roads. Without taxation, many of these services would either be underprovided or not provided at all.

Taxation serves multiple purposes beyond simply raising revenue. Taxes and subsidies can change the relative prices of goods and services, influencing what consumers buy and encouraging firms to invest in new capital goods. Governments also use fiscal policy to redistribute income and spending power between different groups in the economy. For example, progressive taxation takes a larger proportion from those with high incomes, whilst transfer payments channel resources to those on lower incomes or those experiencing hardship.

The relationship between taxation and government spending connects directly to policies designed to correct market failures (covered in earlier chapters) and policies aimed at reducing income and wealth inequality and poverty. Understanding this connection is essential for analysing how governments can address both allocative efficiency and equity concerns.

Types of and reasons for public expenditure

Government spending can be classified into several distinct categories, each serving different economic purposes.

Capital investment versus current spending

One important distinction is between capital investment and current expenditure. Capital investment refers to government spending on new infrastructure projects, such as building NHS hospitals, constructing state schools, or developing transport networks. This type of spending creates assets that will generate benefits over many years.

In contrast, current expenditure covers the annual running costs of public services. This includes paying teachers' salaries, funding the day-to-day operations of hospitals, and maintaining existing infrastructure. Whilst capital projects involve a one-off investment, current spending represents ongoing commitments that must be met year after year.

Transfer payments

A significant portion of government expenditure takes the form of transfers. Transfer payments redistribute income and spending power from taxpayers to recipients of state benefits and pensions. Unlike spending on capital projects or public services, transfers do not directly contribute to national output. Instead, they move resources from one part of the private sector to another.

Examples of transfer payments include:

- State pensions

- Unemployment benefits

- Housing benefit

- Universal Credit

The key characteristic of transfers is that they redistribute existing resources rather than creating new goods and services. When the government builds a hospital, it adds to national output. When it pays unemployment benefits, it transfers purchasing power from those in work to those temporarily out of work.

Interest payments on national debt

A third category of public spending is interest payments on the national debt. These payments go to individuals and institutions that have lent money to the government by purchasing government bonds. Interest payments increase when interest rates rise and when the government runs a budget deficit (spending more than it receives in tax revenue), which requires additional borrowing.

The level of interest payments depends on both the overall size of the national debt and prevailing interest rates in the economy. Monetary policy decisions by the Bank of England significantly influence the cost of servicing government debt.

Public spending on social protection, health and education

Let's examine how the UK government allocates its spending across different departments and services.

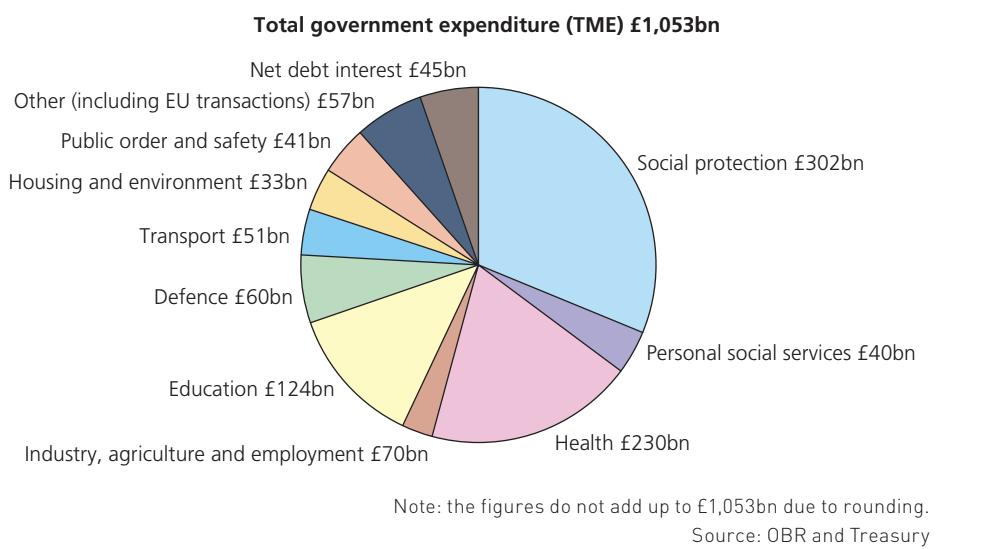

The chart above shows the breakdown of UK government spending for the 2021/22 financial year, with total managed expenditure (TME) of £1,053 billion. The largest areas of spending are:

- Social protection (£302bn) - This includes pensions and unemployment-related benefits, representing approximately 28.7% of total spending

- Health (£230bn) - Primarily NHS funding, accounting for around 21.8% of total expenditure

- Education (£124bn) - Covering schools and colleges, representing about 11.8% of spending

These three categories alone account for over 60% of all government expenditure. Other significant areas include defence (£60bn), transport (£51bn), and interest payments on the national debt (£45bn).

Social security and the 'triple lock'

Social security spending, which forms part of social protection expenditure, increased substantially after the 2008-09 recession. This occurred because the recession reduced incomes and increased unemployment, triggering higher benefit payments. Retired people now receive over half of all social security spending, and this proportion is forecast to continue rising.

The 'Triple Lock' Mechanism

The 'triple lock' guarantees that state pensions increase each year by whichever is highest:

- Wage increases

- CPI inflation

- 2.5%

This protection ensures pensioners maintain their purchasing power, but it also means that as the population ages, pension spending will consume an increasingly large share of the government budget.

The Office for Budget Responsibility (OBR) has noted that this triple lock, combined with the UK's ageing population, is pushing up government spending at a time when demographic pressures are intensifying.

During the Covid-19 pandemic, the government temporarily suspended the triple lock because artificially high wage increases (due to workers coming off furlough) would have led to an unsustainable increase in pension costs. The new government that took office in September 2022 reinstated the triple lock.

NHS and health spending

Health spending has grown significantly over recent decades. Between 2002 and the 2008-09 recession, Labour governments increased NHS spending to around 7% of national income. However, this was still below the average for Organisation for Economic Cooperation and Development (OECD) countries. Whilst other departments experienced budget cuts during the government's austerity programme after 2010, the NHS budget was protected but effectively frozen in real terms (meaning it increased at the same rate as inflation).

Despite a commitment in 2018 to increase NHS spending by £20 billion, several factors have prevented the health service from keeping pace with demand:

- Growing and ageing population

- Longer life expectancy

- Rising costs of new drugs and medical technology

Covid-19 Impact on NHS Spending

The Covid-19 pandemic further disrupted NHS spending plans. Significant increases in health expenditure became necessary to provide both immediate care for Covid patients and to develop treatments for the disease's long-term effects. To fund additional healthcare spending, the government increased employee national insurance contributions in 2022. However, this tax rise was announced when household budgets were already under severe pressure, leading many to call for its postponement. The September 2022 government reversed this decision.

Education spending

The education budget grew substantially under Labour governments from 2002 onwards. Like health and state pensions, spending on schools has been protected from the deepest cuts. However, other areas of education spending have not received the same protection. Higher education, in particular, has seen the largest reductions in public spending, though this has been offset by increased fees paid directly by students.

Historical trends in government spending

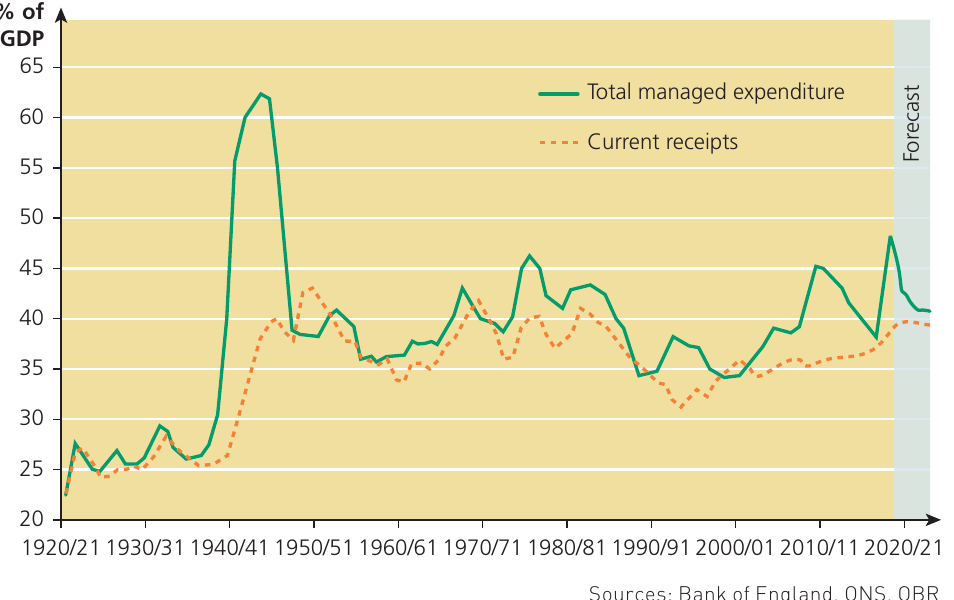

The chart above shows UK government spending and revenue as percentages of GDP from 1920 to 2021. Several patterns emerge:

The graph reveals a dramatic spike in government spending during World War II, when expenditure reached approximately 62% of GDP. More recently, spending increased during the early 1980s recession and again during the 2020-21 pandemic.

Government spending as a proportion of GDP tends to fluctuate with the economic cycle. During booms, when unemployment is low, spending on social security falls, reducing the cyclical component of the budget deficit. During recessions, the opposite occurs - unemployment rises, benefit payments increase, and the budget deficit widens.

Demand-led spending

Certain types of government spending are described as demand-led because they automatically respond to changes in economic conditions. The most significant example is spending on unemployment benefits.

Demand-led spending increases when unemployment grows and falls when unemployment drops. Although the government can adjust the rates at which benefits are paid and the eligibility criteria, the total spending automatically varies according to the phases of the economic cycle.

Similarly, spending on the state pension varies according to how long elderly people live. The government can change pension rates and the retirement age, but demographic factors - particularly the size and longevity of the elderly population - largely determine total pension expenditure.

Debt interest

Interest payments represent a transfer from taxpayers to holders of government bonds (the national debt). In 2021/22, interest payments were expected to reach £45 billion, representing just over 4% of total public spending.

This category of spending rises when interest rates increase and when the government runs a budget deficit. Budget deficits require new government borrowing, which adds to the national debt. The more the government borrows, the higher its future interest payments become.

Interest payments are heavily influenced by the Bank Rate set through monetary policy. When the Bank of England raises interest rates, the government's borrowing costs increase. In terms of fiscal policy, if the national debt (relative to nominal GDP) can be reduced, debt interest as a fraction of nominal GDP also falls - provided interest rates don't rise. Conversely, if national debt grows faster than nominal GDP, debt interest rises as a fraction of real GDP - provided interest rates don't fall.

How taxation affects the pattern of economic activity

Taxation is the primary source of government revenue. The UK government collects taxes to finance the provision of public goods and services. Let's examine the main sources of tax revenue.

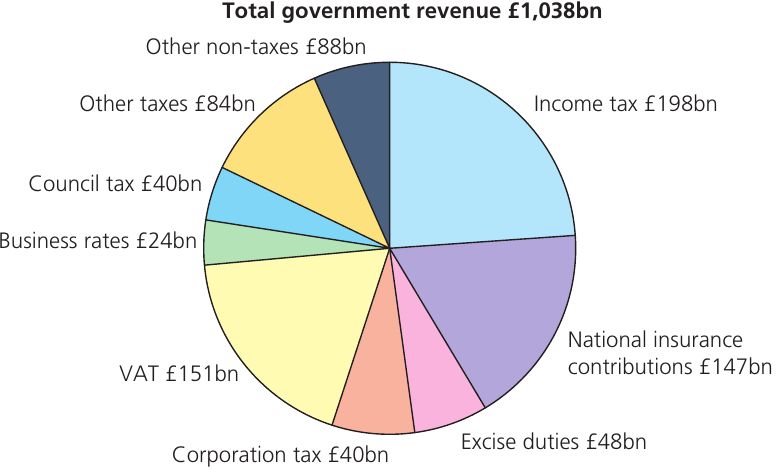

This pie chart shows that in 2021/22, the UK government expected to collect £1,038 billion in total revenue. The three main categories of taxation are:

- Taxes on income - Including income tax (£198bn), national insurance contributions (£147bn), and corporation tax (£40bn)

- Taxes on spending - Including VAT (£151bn) and excise duties (£48bn)

- Taxes on capital and wealth - Including council tax (£40bn) and business rates (£24bn)

The changing composition of UK tax revenue

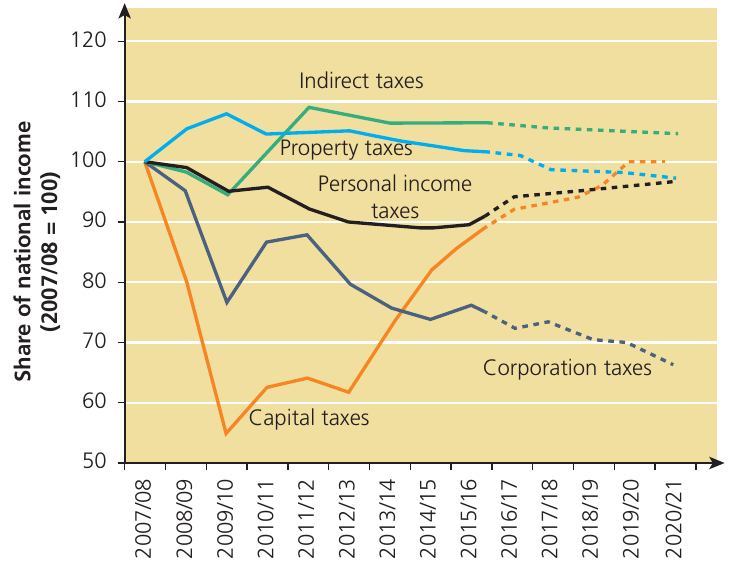

This chart shows how different types of taxes have performed as shares of national income from 2007/08 to 2020/21 (indexed to 100 in the base year 2007/08). Several trends are apparent:

- Indirect taxes have remained relatively stable

- Property taxes have declined from around 100 to approximately 65-70

- Personal income taxes have stayed fairly stable around 90-95

- Corporation taxes have fallen from around 75 to 65

- Capital taxes showed dramatic volatility, dropping sharply to around 55 in 2009/10 before recovering to around 100

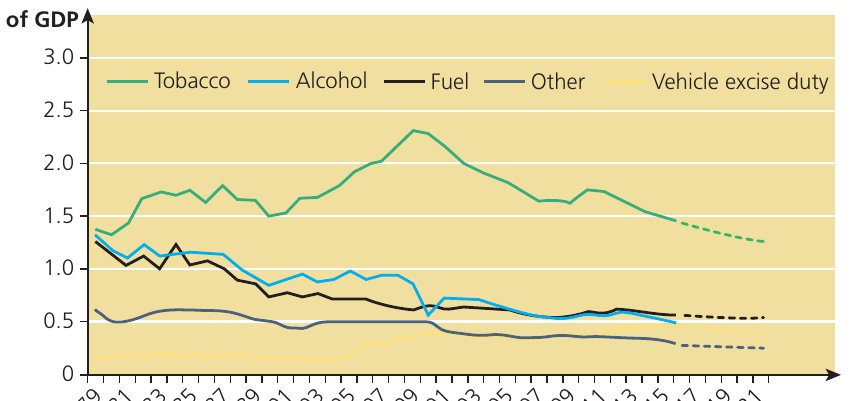

Declining revenue from excise duties

This graph tracks excise duty revenues as percentages of GDP over time. It shows:

- Tobacco duties have declined from a peak of around 2.3% of GDP

- Alcohol and fuel duties have both fallen from approximately 1.0-1.2% to 0.5-0.6% of GDP

- Other excise duties remain low and stable at around 0.3-0.5% of GDP

Revenue from excise duties has been falling as a proportion of national income. In 2018/19, the UK government raised £49 billion from excise duties. Looking ahead, with people choosing healthier lifestyles and moving away from combustion engines and fossil fuels, the government will need to find alternative sources of taxation. This challenge will become increasingly important, especially after the planned phase-out of petrol and diesel-powered cars by 2030 in the UK.

Types of and reasons for taxation

A tax is a compulsory levy imposed by government to pay for its activities. Taxes finance the different types of public expenditure we have described. Beyond raising revenue, taxation serves other economic objectives:

- Altering the distribution of income and wealth

- Managing aggregate demand

- Correcting market failures

- Influencing consumption patterns

Direct and indirect taxation

Understanding the distinction between direct and indirect taxes is fundamental to analysing fiscal policy.

Direct Taxes vs Indirect Taxes

Direct taxes cannot be shifted by the person legally liable to pay the tax onto someone else. Examples include:

- Income tax - The person who receives income is liable to pay the tax to the government

- Corporation tax - Companies pay tax on their profits

- National insurance contributions - Paid by both employees and employers

Indirect taxes can be shifted by the person legally liable to pay the tax onto someone else. Most taxes on spending fall into this category. Examples include:

- Value added tax (VAT)

- Excise duties on tobacco, alcohol, petrol, and diesel fuel

With direct taxes, the person or organisation earning the income bears the legal responsibility for paying the tax. They cannot pass this tax burden to someone else.

The key characteristic of indirect taxes is that although the seller of the good is legally liable to pay the tax to the government, they can raise prices to pass some or all of the tax burden to consumers. As discussed in earlier chapters, when firms face higher taxes, they attempt to recoup this cost by charging higher prices to customers. When this happens, buyers of the good indirectly pay some or all of the tax through these higher prices.

Progressive, regressive and proportionate taxation

Governments can use taxation and transfer payments to modify the distribution of income and wealth produced by free-market forces. The progressivity or regressivity of the tax system determines how effectively it can reduce inequality.

Progressive taxation

A tax is progressive when the proportion of income paid in tax rises as income increases. Until recently, all UK governments used progressive taxation combined with transfers to lower-income groups in a deliberate attempt to reduce inequalities in income distribution.

Progressive taxation works by taking a larger percentage from high earners than from low earners. When combined with transfers to lower-income groups, it reduces the spending power of the rich whilst increasing that of the poor. This helps address the market failure of inequality.

However, some taxes designed to reduce consumption of demerit goods (like alcohol and tobacco) are regressive and fall more heavily on the poor. This creates a policy conflict between the equity objective and the objective of discouraging harmful consumption.

Regressive taxation

A tax is regressive when the proportion of income paid in tax falls as income increases. Cigarette duty provides a clear example of regressive taxation.

Worked Example: Regressive Taxation

Consider two smokers:

- Person A earns £100 per week

- Person B earns £1,000 per week

Both smoke 20 cigarettes per week. In 2018, this cost £8.50, of which £6.98 was tax (both excise duty and VAT).

For Person A:

For Person B:

The low-paid person loses a much greater proportion of their income in tax than the rich person when buying cigarettes and alcohol.

VAT provides another example of a regressive tax. Although VAT is charged at the same percentage rate on most goods, lower-income households typically spend a higher proportion of their income on consumption (and therefore on VAT) than higher-income households, who save more.

The regressive nature of tobacco duty increases over time because tax on cigarettes usually rises faster than inflation. Many view this as acceptable given tobacco's status as a demerit good. Currently, tax accounts for 16.5% of the retail price of a pack of 20 cigarettes, plus an additional £5.33. With an average pack costing around £12, the majority of the retail price is tax.

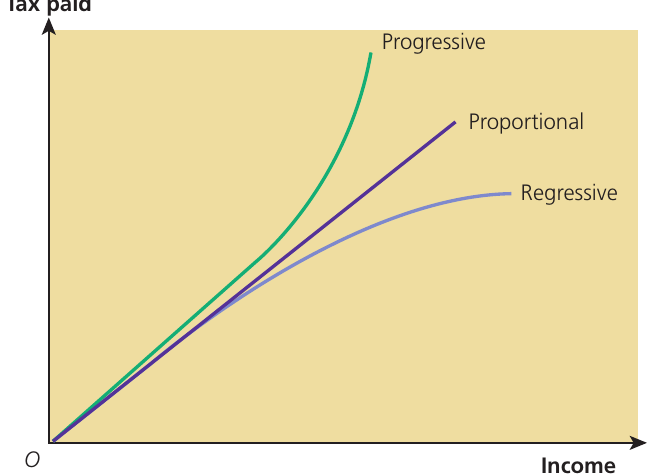

This diagram illustrates the three types of tax system:

- The steep teal line shows a progressive tax where tax paid rises more than proportionately with income

- The moderate purple line shows a proportional tax where tax paid rises in direct proportion to income

- The flattening blue curve shows a regressive tax where tax paid rises less than proportionately with income

Proportional taxation

In recent years, many economists and politicians have advocated introducing proportional taxation, sometimes called a 'flat tax'. In a proportional income tax system, everyone pays the same rate of income tax (for example, 10%).

A proportional income tax system significantly benefits high-income groups compared to the rest of society. The equity of a system that requires millionaires to pay the same rate of income tax as ordinary workers is highly questionable. Proportional taxation would result in governments facing significant budget deficits, which would eventually necessitate either reduced public expenditure or higher indirect taxes to shrink the deficit.

Relating taxation types to marginal and average tax rates

For particular taxes such as income tax or inheritance tax, we can identify whether the tax is progressive, regressive, or proportional by examining the relationship between the average rate and the marginal rate.

In a progressive tax system, the marginal tax rate exceeds the average tax rate. The marginal tax rate is higher than the average rate, which means that the average rate rises as income increases.

Conversely, in a regressive tax system, the marginal rate is less than the average rate. The two are equal in the case of a proportional tax.

For income tax, the average tax rate is calculated as total tax paid divided by total income:

The marginal tax rate is the tax paid on the last pound of income earned, calculated as the change in tax paid divided by the change in income:

The average tax rate indicates the overall burden of the tax on the taxpayer. However, the marginal rate may significantly affect economic choices and decision making. In the case of income tax, the marginal rate influences the choice between work and leisure when deciding how much labour to supply. It also influences decisions about whether to spend income on consumption or to save.

The principles of taxation

Taxpayers commonly view all taxes as 'bad' because they don't enjoy paying them, although most realise taxation is necessary to provide useful goods and services. A starting point for analysing whether a tax is 'good' or 'bad' is Adam Smith's four principles of taxation, also known as the canons of taxation.

Adam Smith suggested that taxation should be equitable, economical, convenient, and certain. To these principles we may add the principles of efficiency and flexibility. A 'good' tax meets as many of these principles as possible. Conversely, a 'bad' tax meets few if any of the guiding principles.

The Six Principles of Taxation

-

Economy - A tax should be cheap to collect in relation to the revenue it yields

-

Convenience and certainty - A tax should be convenient for taxpayers to pay and taxpayers should be reasonably sure of the amount they will be required to pay

-

Equity - A tax system should be fair, although there may be different and possibly conflicting interpretations of fairness. Specifically, a particular tax should be based on the taxpayer's ability to pay. This principle supports progressive taxation, since the rich have a greater ability to pay than the poor

-

Efficiency - A tax should achieve its desired objective(s) with minimum undesired side-effects or unintended consequences. The disincentive effect on effort can be thought of as an unintended consequence of high rates of income tax

-

Flexibility - A tax must be easy to change to meet new circumstances

The role and merits of different UK taxes

A large proportion of people's income goes to paying taxes. Tax accounts for around a third of the money people earn. Let's examine the main categories of UK taxation and evaluate their strengths and weaknesses.

Taxes on income

Looking back at the revenue chart, taxes on income represent the most important category of taxation in the UK. This category includes:

- Personal income tax

- National insurance contributions

- Corporation tax

These are all direct taxes, meaning the person or organisation earning the income is directly liable to pay the tax to the government. Failure to declare income constitutes tax evasion, which is illegal.

Advantages of income taxation

For most wage and salary earners, income tax is cheap to collect, convenient, and certain for the taxpayer. When the basic tax threshold is set at a relatively high level, people receiving very low incomes can be taken out of the 'tax net', thereby paying zero income tax.

For most wage and salary earners, income tax is collected through the 'pay as you earn' (PAYE) system. This makes personal income tax cheap to collect, as employers bear most of the administrative costs. When progressive, income tax is equitable in the sense that it reflects taxpayers' ability to pay.

Disadvantages of income taxation

However, income tax has been relatively easy to avoid and evade for some taxpayers. Tax avoidance exploits legal loopholes in the tax system, whilst tax evasion is illegal. People on relatively low incomes may work 'strictly for cash' (or 'cash in hand'), where physical money is exchanged for work carried out. This leaves no record of the transaction - no money is paid into a bank account and no receipt is issued. If substandard work is performed, the customer cannot prove the work was done.

Higher earners may evade tax through tax-efficient schemes provided by financial advisers. The opportunities for avoiding and evading tax are among the disadvantages of income tax.

Disincentive Effects of High Income Tax

A highly progressive income tax may lead to undesirable unintended consequences. For example, it may disincentivise hard work, risk taking, and entrepreneurial effort.

Despite these drawbacks, personal income tax has long been the main source of government revenue in the UK. This partly reflects the fact that for personal income tax, the 'tax base' is extremely wide - millions of people receive taxable income. Total government revenue from the taxation of income is considerably higher than revenue collected from personal income tax alone. Companies pay corporation tax on their profits, and most employees pay national insurance contributions (NICs) as well as personal income tax to the government.

Taxes on spending

After income taxes, VAT and excise duties make up the second most important group of taxes in the UK. VAT is an ad valorem tax (a percentage tax), whilst excise duties are almost always specific or unit taxes, levied not on a good's price but on the physical quantity of the good.

Advantages of taxes on spending

Excise duties can be used to encourage people to switch their spending away from goods deemed undesirable (demerit goods) to those regarded as 'good' for consumers (merit goods). Some economists, mainly of a free-market persuasion, believe this to be a disadvantage rather than an advantage. They dislike governments claiming to know better than ordinary individuals what is good for those they govern.

VAT, by contrast, is generally a neutral tax. It is levied on spending on most goods and services, with the result that a change in the VAT rate has little effect on patterns of expenditure.

Many economists believe that unless there is a good reason to affect people's choices through the tax system, taxation of goods should conform to the principle of neutrality. Reasons for taxing some products at a higher rate than others could relate to demerit goods and externalities. Another reason could be to influence income distribution - imposing zero tax on basic necessities and high taxes on luxury goods.

Disadvantages of taxes on spending

Using indirect taxes to encourage people to alter their expenditure patterns becomes less effective if more goods are taxed at the same rate. Although this widens the 'tax base', allowing the government to collect more revenue, the tax becomes less useful as a tool for influencing consumer spending patterns.

Indirect taxes can be evaded. For example, when a builder quotes a price excluding VAT to a householder, as long as the householder pays in cash, VAT evasion occurs. However, it is generally less easy to evade and avoid indirect taxes than direct taxes.

Taxes on capital and wealth

Taxes on capital and wealth are also direct taxes. Some wealth taxes can be avoided and evaded, but with others this is less easy. Wealth in the form of cash can be 'money laundered' when given from one person to another. This conceals the illegal or untaxed origin of money by converting it to a legitimate source, making it no longer appear suspicious.

Property wealth is less easily hidden. However, taxing property works best if the government maintains up-to-date property values, which is challenging given how quickly values change. Successive UK governments have shown little interest in updating property valuations. The last time houses were valued for council tax purposes (the main UK tax on property) was in 1991 (though later for Wales). Since then, house prices have risen rapidly in most UK regions, especially London and the southeast.

Some general comments on the structure of UK taxation

The financial crisis and 2008-09 recession caused government tax revenues to collapse and the budget deficit to increase sharply. Tax receipts from capital taxes (including stamp duties, capital gains tax, and inheritance tax) declined rapidly and have taken over a decade to recover.

Corporation tax revenues fell significantly during the recession and appear to be in long-term decline. Tax revenue from personal income (mostly income tax and national insurance) has struggled to recover from the crisis and is increasingly dependent on higher-income groups.

Similar patterns emerged during the 2020-21 pandemic. Large increases in government spending on support for individuals and businesses (such as the furlough scheme) were combined with rapid falls in taxation as spending on goods and services was restricted and remained low during the recovery period. However, the government's budget balance recovered more rapidly from the 2021/22 tax year onwards, mainly because prices rose quickly, which meant VAT receipts rose faster than expected.

Taxes on spending now constitute the main source of government tax revenue. VAT was 8% in the late 1970s but has gradually risen, reaching 20% since 2012. Similarly, property taxes (council taxes and business rates) have increased as a source of government revenue.

Overall, regressive taxes, which affect the disposable income of low-income groups, have increased since the recession.

The role and merits of taxes in affecting the distribution of income and wealth

In past decades, UK governments used taxation and public spending to attempt reducing inequality between rich and poor. More recently, although governments have been less concerned about reducing inequality, the combined effects of taxes and public spending have made income distribution much more equal than if governments did not intervene.

Under the influence of supply-side thinking, government policy has been affected by the conflict between two principles of taxation: efficiency and equity.

The efficiency versus equity trade-off

Efficiency requires greater incentives for work and enterprise to increase the UK's growth rate. However, when progressive taxation and transfers to less wealthy people are used to make income distribution more equitable, it can mean people have less incentive to work hard and take risks through entrepreneurial activity.

Moreover, the ease with which the poor can claim welfare benefits and the level at which they are available can create a situation where poor people choose unemployment and state benefits over work and low wages. This is not necessarily because people are lazy but may be a rational choice given:

- The loss in benefits when taking a job

- Extra costs such as transport to and from work

- Additional childcare costs incurred once working

The supply-side view

Many supply-side economists and politicians have argued that income tax rates and benefit rates should both be reduced. They believe that tax and benefit cuts would alter the work/leisure choice in favour of supplying labour, particularly for benefit claimants who lack the skills necessary for high-paid jobs.

The Supply-Side Argument

According to this view, to make everyone eventually better off, it is necessary to increase the gap between what people earn when working and what they receive when out of work. This means making those who are poor because they are unemployed worse off.

The supply-side argument suggests that increased inequality is necessary to create incentives to facilitate economic growth, from which all will eventually benefit. Through a 'trickledown' effect, the poor eventually end up better off in absolute terms. However, because inequalities have widened, they remain relatively worse off compared to the rich.

According to Office for National Statistics (ONS) data, inequality increased significantly in the 1980s and stabilised in the late 1990s. This was the intended outcome of government supply-side fiscal policy. In the first two decades of the twenty-first century, inequality has remained high, although it has narrowed in years following the financial crisis because high-income groups' incomes have fallen faster than those of low-income groups.

Nonetheless, the UK remains one of the most unequal countries in Europe in terms of disposable income. According to OECD data, in 2019 the UK's Gini coefficient was 37% compared to France and Germany's 29% and Italy's 33%.

Evaluating different taxes against the principles of taxation

When considering the merits and demerits of different types of taxation, a useful starting point is considering the extent to which a particular tax satisfies the various principles of taxation. A 'good' tax meets as many of these principles as possible, whereas a 'bad' tax meets few, if any, of the guiding principles.

Key Points to Remember:

-

Government spending is financed primarily through taxation and serves multiple purposes including providing public goods, redistributing income, and managing aggregate demand.

-

The three main categories of public expenditure are capital investment, current spending on public services, and transfer payments, with social protection, health, and education being the largest spending areas.

-

Taxes are classified as either direct (paid by the income earner) or indirect (paid by the seller but potentially passed to consumers), and as progressive (higher proportion paid as income rises), regressive (lower proportion paid as income rises), or proportional (same proportion at all income levels).

-

The principles of taxation (canons of taxation) provide criteria for evaluating tax systems: economy, convenience and certainty, equity, efficiency, and flexibility. A 'good' tax should satisfy as many of these principles as possible.

-

There is an inherent conflict between efficiency and equity in taxation policy - progressive taxes that promote fairness may reduce work incentives, whilst regressive taxes that maintain incentives may increase inequality. This trade-off significantly influences government fiscal policy decisions.