Business Growth (Edexcel A-Level Business): Revision Notes

Mergers and takeovers

Mergers and takeovers represent important external growth strategies that allow businesses to expand rapidly. When firms join together through these methods, they create a single organisation that may be more competitive and efficient than the separate entities. Understanding why businesses pursue these strategies, how they differ, and what challenges they present is crucial for analysing corporate decision-making.

What are mergers and takeovers?

Mergers and takeovers both involve businesses combining, but there are important differences between them.

A merger occurs when two or more businesses voluntarily agree to join together and operate as one organisation. These are typically 'friendly' arrangements where both companies' management teams support the union. The new business often takes a name that combines elements of both original companies.

Example: LafargeHolcim Merger

When Swiss cement producer Holcim Ltd merged with French company Lafarge SA in 2014, they formed LafargeHolcim, creating the world's largest cement producer with annual sales exceeding $40 billion. The primary motive was to reduce costs and better manage overcapacity in the market.

A takeover (also called an acquisition) happens when one business purchases another. The acquiring company (sometimes called the predator) buys control by purchasing at least 51% of the target company's shares. Once complete, the acquired business loses its separate identity and becomes part of the acquiring organisation.

Example: Three's Acquisition of O2

In 2015, mobile operator Three bought O2 for £10.5 billion, creating the UK's largest mobile operator with approximately 32 million customers.

Takeovers can be either friendly or hostile. A hostile takeover occurs when the target company's board of directors resists the acquisition, trying to convince shareholders that remaining independent serves their interests better.

Example: Pfizer's Hostile Bid for AstraZeneca

In 2014, pharmaceutical giant Pfizer made a hostile £70 billion bid for UK rival AstraZeneca, which the board rejected, believing they could deliver better returns independently.

Conversely, struggling businesses may invite takeovers by a 'white knight' – a stronger company that can inject cash and resources to ensure survival.

Control Through Share Ownership

In public limited companies, takeovers are possible because shares are publicly traded. A predator can gain control by purchasing shares on the stock market and directly from existing shareholders. However, once a company acquires 3% of another company's shares, they must legally declare this to the stock market, ensuring transparency for existing shareholders.

Private limited companies cannot be taken over unless majority shareholders explicitly invite others to purchase their shares.

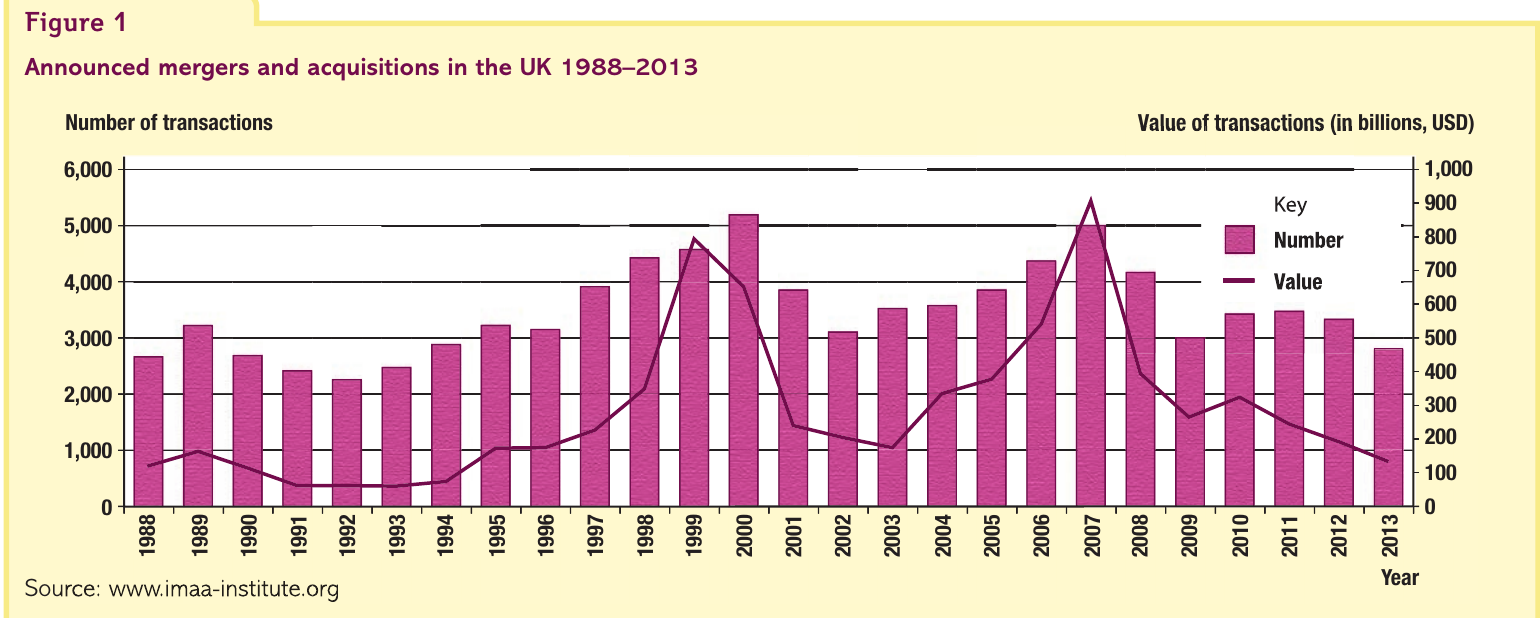

The chart above shows UK merger and acquisition activity from 1988 to 2013. Notice the peaks around 2000 and 2007, followed by sharp declines. The 2007-2008 financial crisis and subsequent recession significantly reduced both the number and value of transactions, demonstrating how economic conditions influence M&A activity.

Why businesses pursue mergers and takeovers

Businesses choose mergers and takeovers for numerous strategic reasons:

Exploiting synergies: One of the most significant motivations is achieving synergy – where the combined organisation becomes more powerful and efficient than the two separate businesses. This is often described as "the whole is greater than the sum of the parts" or "2 + 2 = 5". Synergies can arise from economies of scale, risk diversification, or management efficiencies that wouldn't exist if the businesses remained separate.

Understanding Synergy

Synergy represents the additional value created when businesses combine. The merged entity generates greater benefits than both companies could achieve independently, whether through cost savings, revenue enhancements, or strategic advantages.

Speed of expansion: Acquiring an existing business provides immediate growth. A supermarket chain wanting twenty new stores could buy a competitor with existing premises rather than spending years finding sites and constructing new buildings. This dramatically accelerates market presence.

Cost effectiveness: Buying an established business is often cheaper than organic growth. If internal expansion would cost £80 million but a suitable acquisition target is available for £55 million on the stock market, the takeover represents better value, even accounting for the price increases that typically occur during acquisition processes.

Utilising available cash: Cash-rich businesses may view acquisitions as an effective way to deploy surplus funds productively, potentially generating better returns than alternative investments.

Defensive positioning: Companies may merge to consolidate market position or avoid becoming takeover targets themselves. Increasing size through mergers provides protection against hostile bids.

Responding to economic changes: Businesses time mergers to align with economic shifts, such as the introduction of the euro in 1999 or EU expansion in 2004. These changes created opportunities for strategic consolidation.

Accessing foreign markets: Merging with businesses in different countries provides market entry while potentially avoiding trade barriers, import restrictions, or tariffs that would otherwise limit expansion.

Globalisation opportunities: The globalisation of markets encourages international mergers, allowing companies to operate worldwide rather than being confined to specific countries or regions.

Achieving economies of scale: Combining operations typically reduces unit costs through bulk purchasing, shared facilities, spreading fixed costs, and operational efficiencies that lower average costs as output increases.

Asset stripping: Some businesses (particularly certain private equity firms) acquire companies to sell profitable divisions, close unprofitable sections, and integrate valuable parts into existing operations. While controversial, this strategy can unlock hidden value.

Management objectives: Growth may be the primary objective for some management teams, who pursue acquisitions to increase company size regardless of whether this maximises shareholder value.

Types of integration

Integration refers to the process of businesses joining together through mergers or takeovers. There are different types depending on the relationship between the combining businesses.

Horizontal integration

Horizontal integration occurs when two businesses at exactly the same stage of production in the same industry join together. The Lafarge-Holcim cement merger exemplifies this – both were cement producers operating in the same competitive space.

Benefits of horizontal integration include:

- Shared industry knowledge: Both businesses understand the same markets, customers, and competitive dynamics, reducing learning curves

- Lower failure risk: Combining similar operations is less risky than merging different business types

- Compatible employee skills: Workforces possess similar expertise, facilitating integration

- Reduced disruption: Similar systems and processes mean less operational upheaval during integration

- Increased market share: The combined entity becomes a larger competitor with greater market power

- Enhanced economies of scale: Duplicated functions can be eliminated, reducing costs

Vertical integration

Vertical integration happens when businesses at different stages of the production chain join together. This can take two forms:

Backward vertical integration involves joining with a supplier from an earlier production stage. If a mountain bike manufacturer acquired a tyre supplier, this would represent backward integration. Key advantages include:

- Guaranteed supply of components and raw materials

- Greater control over quality and delivery schedules

- Elimination of supplier profit margins, reducing costs

- Protection against supply disruptions

Forward vertical integration means joining with a business at the next production stage. The same bike manufacturer acquiring retail bike shops would exemplify forward integration. Benefits include:

- Guaranteed distribution outlets for products

- Control over how products are presented and sold to customers

- Elimination of retailer profit margins

- Direct access to customer feedback and market intelligence

Example: Morrison's Backward Vertical Integration

The UK supermarket Morrison's provides an excellent example of backward vertical integration. Unlike competitors, Morrison's owns multiple suppliers of fresh produce, including horticultural operations, meat-processing plants, and seafood facilities.

Benefits achieved:

- Enhanced control over quality and costs

- Reduced supply chain waste

- Improved lead times

- Supported image as a supporter of British farmers

Challenges faced:

- Requires substantial capital investment

- Complicates business management

- Reduces supply flexibility

- Stretches resources

Financial risks

While mergers and takeovers offer significant opportunities, they also carry substantial financial risks that businesses must carefully evaluate.

Regulatory intervention: The Competition and Markets Authority (CMA) in the UK scrutinises major mergers and takeovers to protect consumer interests. If the CMA believes a merger would reduce competition, it can order investigations, which cause delays and uncertainty. Following investigation, the CMA may block the merger entirely or impose conditions.

Example: LafargeHolcim Regulatory Conditions

The Lafarge-Holcim merger only proceeded after both companies agreed to sell significant assets:

- Lafarge divested all German and Romanian operations

- Holcim sold its Slovak business and most French activities

These forced asset sales and procedural delays created substantial costs and complexity.

Employee resistance: Mergers frequently result in job losses because combined organisations contain duplicated resources. Two merged companies rarely need two head offices, two finance departments, or two IT systems. When large-scale redundancies are announced, employees may resist through strikes, work-to-rule actions, or other disruptions that delay integration and increase costs. Managing workforce concerns requires sensitive communication and often significant severance payments.

Integration Costs Are Often Underestimated

Physically combining two organisations after agreement proves complex, expensive, and time-consuming. Integration expenses include:

- Organisational restructuring

- Personnel changes and redundancy packages

- Technical system integration

- Process harmonisation

- Extensive training programs

Businesses commonly underestimate these costs, encountering unexpected problems during implementation. Merging different organisational cultures presents particularly significant challenges, as employees from both businesses must adopt new working practices and values.

Bidding wars: When multiple businesses want to acquire the same target, competitive bidding drives up the purchase price significantly.

Example: Tyson Foods' Acquisition of Hillshire Brands

In 2014, Tyson Foods Inc. eventually paid $8.55 billion for American food company Hillshire Brands Co., but the initial offer from competitor Pilgrim's Pride was only $6.4 billion. Through successive counter-offers, the final price increased by 33.6% above the opening bid.

Such escalation makes acquisitions far more expensive than initially planned, potentially undermining the financial logic of the deal.

Financial rewards

Despite these risks, businesses continue pursuing mergers and takeovers because potential rewards are substantial.

Rapid growth: External growth delivers expansion far faster than internal development. Benefits such as increased market share, economies of scale, enhanced market power, and higher profitability materialise more quickly than through organic growth strategies. This speed benefits multiple stakeholders, including shareholders, employees, and customers.

Higher executive remuneration: Senior management typically receives salary increases after mergers or takeovers because they now oversee larger, more complex organisations. Performance-related bonuses tied to growth rates provide additional financial rewards for executives who successfully complete acquisitions.

Shareholder gains: Existing shareholders in acquired businesses often receive significant premiums when their companies are purchased.

Example: Steris Corporation's Acquisition of Synergy Health

When US company Steris Corporation acquired British outsourcing firm Synergy Health in 2014:

- Synergy shares were trading at £14 before the bid

- Steris offered £19.50 per share

- Shareholders received an immediate 39% gain upon completion

Such premiums incentivise shareholders to approve takeover offers.

Increased profitability: Successful mergers and takeovers boost long-term profitability through higher revenues (from increased market share) and lower costs (from economies of scale). Significantly larger businesses may even achieve market dominance, enabling premium pricing and exceptional profit margins that would be impossible for smaller competitors.

Problems of rapid growth

Businesses pursuing aggressive merger and takeover strategies must recognise that excessively rapid growth creates serious problems.

The 90% Failure Rate

According to industry research, approximately 90% of mergers and takeovers fail to meet their original objectives, highlighting the significant challenges involved in successful integration.

Resource drain: Major acquisitions require enormous financial resources. Three's £10.5 billion purchase of O2, Google's $12.5 billion Motorola acquisition, or Actavis's $66 billion purchase of Allergan represent massive capital commitments. Companies pursuing multiple acquisitions in quick succession may overstretch financial resources, impairing other business areas and leaving the organisation financially vulnerable.

Change Management Challenges

Integration requires substantial organisational change, with merging different corporate cultures presenting particular difficulties. Imposing new cultures on established businesses often meets resistance. Forcing changes through too quickly without proper consultation intensifies this resistance, reducing employee engagement and productivity. When growth is excessively rapid, businesses attempt to integrate multiple cultures simultaneously, compounding these problems.

Customer alienation: Companies growing too quickly may lose focus on customer needs, directing excessive attention and resources toward the growth process itself. Customer requirements become overlooked. Brand name changes following mergers can confuse consumers, who may struggle to understand what the new brand represents or what values it embodies. This confusion damages brand equity and may result in customer defection to competitors.

Control erosion: Excessively rapid expansion can create organisations that become too large too fast. Senior executives may lose effective control as additional management layers lengthen communication channels and complicate decision-making. Diseconomies of scale emerge as coordination costs increase, bureaucracy expands, and responsiveness declines.

Resource shortages: Rapidly growing businesses consume resources at unsustainable rates, potentially driving up resource prices. Skilled labour shortages are particularly problematic – when demand for specialist employees exceeds supply, wage inflation occurs, significantly increasing labour costs and reducing profitability.

Exam guidance

When analysing mergers and takeovers in exam questions, remember to provide balanced evaluations. While these strategies offer significant potential benefits, substantial risks and challenges exist. According to research, 90% of mergers fail to meet expectations – a statistic that should inform your analysis.

Understanding Command Words

Command words matter significantly in exam questions:

- Analyse questions require you to break down why businesses pursue mergers/takeovers, explaining causes and effects with developed chains of reasoning

- Evaluate questions demand judgements about whether specific mergers/takeovers are likely to succeed, considering both benefits and drawbacks before reaching a justified conclusion

- Assess questions need you to weigh up the importance of mergers/takeovers compared to alternative growth strategies

Link your answers to other business concepts wherever possible. Mergers and takeovers connect to market structure, competitive advantage, economies of scale, business culture, change management, stakeholder interests, and financial performance. Demonstrating these connections shows synoptic understanding.

Using Examples Effectively

Use current examples to support your analysis – the business environment constantly produces new merger and takeover cases that you can reference to strengthen answers. However, ensure examples are relevant to the specific question rather than simply describing deals you've memorised.

Key Points to Remember:

-

Mergers are voluntary agreements where two businesses join to form one organisation (friendly); takeovers involve one business purchasing another (can be hostile or friendly)

-

Synergy is the key concept – combined businesses should be more powerful and efficient than the sum of separate parts (2 + 2 = 5)

-

Horizontal integration joins businesses at the same production stage in the same industry; vertical integration joins businesses at different production stages (backward = previous stage, forward = next stage)

-

Financial risks include regulatory intervention, integration costs, bidding wars, and employee resistance that can make mergers more expensive and difficult than anticipated

-

Financial rewards include rapid growth, increased profitability, shareholder gains, and higher executive pay, but approximately 90% of mergers fail to meet original objectives

-

Problems of rapid growth through acquisitions include resource drain, change management difficulties, customer alienation, loss of control, and resource shortages that can undermine business performance