Impact of External Influences (Edexcel A-Level Business): Revision Notes

The Changing Competitive Environment

Introduction to competition

Competition refers to the rivalry between firms when they try to sell goods in a particular market. The level of competition varies significantly across different markets. Some markets are highly competitive with thousands of businesses fighting for customers, while others have minimal competition with just one or two dominant firms.

Understanding the competitive environment is crucial for businesses because it affects their ability to set prices, earn profits, and make strategic decisions.

The structure of markets

Markets can be classified according to their structure. At one end of the spectrum are highly competitive markets with many firms, and at the other end are uncompetitive markets dominated by one or a few large businesses.

Competitive markets

In a competitive market, several key characteristics exist:

- Large number of buyers and sellers: No single buyer or seller dominates the market

- Close substitutes: Products sold by different businesses are very similar, making them easy to switch between

- Low barriers to entry: New firms can enter the market relatively easily without facing significant obstacles

- Limited price control: Businesses cannot set prices far above competitors without losing most customers. If a firm tries to charge significantly more than rivals, it will lose nearly all its business

- Free flow of information: Consumers and producers have access to information about products, prices, availability, and production costs

Real-World Example: London's Restaurant Market

The restaurant market in London demonstrates high competition, with over 5,500 restaurants competing for customers. Each restaurant must carefully consider its pricing and quality to attract and retain diners. This creates an environment where consumers benefit from choice, competitive prices, and businesses constantly striving to improve their offerings.

Uncompetitive markets

Some markets have very limited competition due to the dominance of one firm (monopoly) or a few large firms (oligopoly).

Monopoly

A monopoly exists when just one business supplies the entire market. This single supplier faces no direct competition.

Examples of monopolies include:

- Thames Water: The sole supplier of tap water in London

- ScotRail: The only train operator on the Glasgow to Edinburgh route

- Village shops: In rural areas, a single shop may serve the whole community without any local competition

Consumer Protection Concerns

Monopolies can potentially exploit consumers because of their market power. They may charge higher prices than would exist in competitive markets and can prevent new competitors from entering by erecting barriers to entry. Due to these concerns, government regulators closely monitor monopolies to protect consumer interests.

Oligopoly

An oligopoly is a market dominated by a few very large producers. While many smaller businesses may exist in the market, a small number of large firms control the majority of sales.

For example, a market might contain 2,000 businesses, but if just three of these firms share 70% of the market between them, the market is classified as an oligopoly.

Key features of oligopolistic markets:

Interdependence: This is a crucial characteristic of oligopolies. The actions of one business directly affect other businesses in the market. If one firm gains an extra 4% market share, other firms must have collectively lost that 4%. This creates a delicate balance where firms must carefully consider how competitors will react to their decisions.

High barriers to entry: New firms find it difficult to enter oligopolistic markets due to various obstacles such as high start-up costs, established brand loyalty, and economies of scale enjoyed by existing large firms.

Economies of scale: The larger firms in oligopolies can exploit economies of scale, giving them significant cost advantages over smaller competitors.

Price stability: Because of interdependence, prices tend to remain stable for extended periods. All firms fear triggering a price war where competitors match price cuts, ultimately reducing profits for everyone in the market.

Non-price competition: Rather than competing on price, oligopolistic firms typically focus on advertising, promotion, product differentiation, and brand building. This allows them to maintain higher prices while differentiating themselves from competitors.

UK Oligopoly Examples

Several major UK industries demonstrate oligopolistic market structures:

- Car industry: Dominated by major manufacturers like Ford, Volkswagen, and Toyota

- Confectionery industry: Firms like Cadbury, Nestlé, and Mars control most of the market

- Potato crisp industry: Walkers, KP Snacks, and a few others dominate sales

In each case, a small number of large firms control the majority of market share, while smaller competitors struggle to gain significant traction.

The changing competitive environment

Markets are not static - they evolve over time. The structure and intensity of competition in a market can change significantly as new businesses enter, existing firms merge, or market conditions shift.

Since 1980, UK governments have actively tried to make markets more competitive by reducing regulation. For instance, bus services were deregulated - previously, only local councils could operate buses, but now any company can obtain a licence and provide services on any route. This policy aims to increase consumer choice and drive down prices through greater competition.

However, some markets have experienced consolidation, meaning fewer businesses now operate than before. This often results from takeover or merger activity where two or more firms combine operations.

Real-world examples of changing competitive environments

Supermarket Industry Transformation

Competition has intensified significantly since 2010. In the last four months of 2014, the traditional "big four" supermarkets (Tesco, Sainsbury's, Asda, and Morrisons) all lost market share to discount retailers Aldi and Lidl, as well as upmarket Waitrose. This forced the established players to reassess their pricing strategies and store formats.

The Online Shopping Revolution

Online shopping has dramatically increased competitive pressure on traditional high street retailers. Consumers can now compare prices and purchase products from businesses worldwide, not just local shops. This has created intense competition and forced many retailers to develop their own online presence.

Global Airline Industry Consolidation

Significant consolidation has occurred in the airline sector. In 2005, eleven US airlines shared 96% of the domestic market. By 2014, this had consolidated to just six airlines sharing 94% of the market. In Europe, national carriers merged - British Airways and Iberian Airlines formed IAG (now one of the world's largest carriers), while Air France merged with KLM, and Swiss Air merged with Lufthansa.

Mobile Telephone Industry Mergers

The number of operators continues to fall. In 2015, Hutchison Whampoa acquired O2 for \£10.25 billion, reducing UK operators from four to three. This consolidation reduces consumer choice but may allow remaining firms to invest more in network infrastructure.

Impact on businesses of a changing competitive environment

The Critical Need to Adapt

Markets are dynamic, and businesses must monitor changes carefully and respond appropriately. Failure to adapt to a changing competitive environment can damage performance and, in extreme cases, threaten survival.

Response to new entrants

When competition strengthens due to new entrants, existing businesses must reconsider their strategies and operations.

The growth of online shopping provides a clear example. Many traditional retailers have been forced to develop their own online shopping platforms to compete with online-only retailers and maintain relevance with consumers. Failure to compete online has proven fatal for numerous businesses.

High Street Retail Decline

Between 2013 and 2014, an average of 16-18 shops per day closed in the UK. Casualties included building societies, video rental shops, pawnbrokers, mobile phone shops, and fashion retailers. While not all closures resulted solely from online competition, retailers without an online presence increasingly struggle to survive.

The message is clear - businesses must adapt to new competitive realities or face decline.

Response to new products

When innovative products appear in the market, existing businesses may need to make significant changes to remain competitive. Possible responses include:

- Product adaptation: Modifying existing products to match or exceed new offerings

- Price adjustments: Lowering prices on existing products to maintain competitiveness

- Aggressive marketing: Investing heavily in advertising and promotion to defend market share

- Innovation: Developing their own new products to stay ahead

Banking Industry Response to P2P Lending

The banking industry has seen new entrants offering peer-to-peer (P2P) lending platforms. Traditional banks have responded by either partnering with existing P2P platforms or, like Royal Bank of Scotland, developing their own P2P services to prevent losing customers to these innovative competitors.

Response to consolidation

When consolidation occurs, the number of market competitors decreases, but some remaining businesses grow larger and more powerful. These enlarged organisations pose greater threats because they:

- Can reduce costs through economies of scale

- Control larger market shares

- Have more resources for innovation and marketing

Other businesses in the market might respond through:

- Defensive mergers or takeovers: Combining with other firms to increase their own size and competitiveness

- Product development: Investing in innovation to differentiate offerings

- Diversification: Entering new markets or product categories to reduce dependence on increasingly competitive core markets

- Cost reduction: Finding efficiencies to maintain profitability despite competitive pressures

- Accepting lower margins: Continuing similar operations but acknowledging reduced profitability

Active Response is Essential

The critical point is that businesses must respond actively to changes in their competitive environment. Passive approaches that ignore market evolution will likely lead to declining performance and potentially business failure.

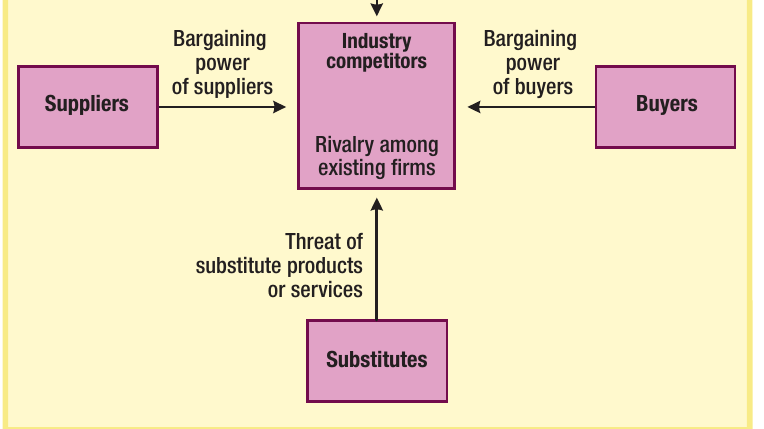

Porter's Five Forces

Michael Porter developed an influential framework for analyzing competitive environments in his book "Competitive Advantage: Creating and Sustaining Superior Performance" (1985). He identified five forces that determine the profitability of an industry and a firm's competitive position.

Porter argued that the ultimate aim of competitive strategy is to cope with these forces and ideally change them in the business's favor. Where the collective strength of the five forces is favorable, businesses can earn above-average returns on capital. Where forces are unfavorable, businesses face low or wildly fluctuating returns.

The framework consists of five competitive forces:

Bargaining power of suppliers

Suppliers, like any business, want to maximize profits from their customers. The more power a supplier has, the higher the prices it can charge, effectively transferring profit from the customer to itself.

Limiting supplier power improves a business's competitive position. Strategies to achieve this include:

Strategies to Manage Supplier Power

-

Backward vertical integration: Growing the business vertically by acquiring a supplier or establishing an in-house supply operation. This eliminates dependence on external suppliers.

-

Creating supplier competition: Seeking out multiple suppliers to increase competition among them, which tends to reduce prices and improve terms.

-

Finding substitutes: Engaging in technical research to identify alternative inputs that can replace those from powerful suppliers, thereby broadening the supply base.

-

Limiting information sharing: Minimizing information provided to suppliers prevents them from fully understanding their power over the customer.

Bargaining power of buyers

Just as suppliers want maximum prices, buyers want to pay the lowest possible prices. When buyers have considerable market power, they can force suppliers to reduce prices.

Buyer Power in the Automotive Industry

Major car manufacturers have successfully pressured component suppliers to lower prices because of their enormous buying power and the relatively small number of major car manufacturers globally.

Strategies to manage buyer power include:

Strategies to Reduce Buyer Power

-

Forward vertical integration: Extending into buyers' markets by setting up operations that sell directly to end consumers. For instance, a car manufacturer might establish its own dealership network.

-

Encouraging new buyers: Supporting the entry of new businesses into customers' markets to reduce the power of existing large customers.

-

Creating switching costs: Making it expensive or difficult for customers to switch to alternative suppliers. Gaming console manufacturers do this by making games technically incompatible across different console systems, which helps maintain higher prices and royalty payments.

Threat of new entrants

When businesses can easily enter and exit an industry, existing firms find it difficult to charge high prices and earn substantial profits. They face constant pressure knowing that high profits will attract new competitors who may undercut their prices.

Businesses can counter this threat by erecting barriers to entry:

Strategies to Deter New Entrants

-

Intellectual property protection: Applying for patents and copyright to protect innovations and prevent other businesses from using them.

-

Brand building: Creating strong brands that generate customer loyalty, making customers less price-sensitive and more resistant to switching to new entrants.

-

Heavy advertising: Large advertising expenditures represent significant sunk costs that deter new entrants who would need to match this spending to gain market share.

-

High sunk costs: Requiring substantial upfront investments that cannot be recovered if the business exits the industry. These costs deter new entrants who face greater financial risk.

Threat of substitutes

The more substitute products available for a particular item, the fiercer the competitive pressure. Conversely, products with few or no substitutes allow businesses to charge higher prices and earn greater profits.

Strategies to reduce substitute threats include:

Strategies to Minimize Substitute Threats

-

Research and development: Developing potential substitutes first and then patenting them to prevent competitors from bringing them to market.

-

Acquiring substitute patents: Sometimes businesses purchase patents for new inventions from third parties and deliberately choose not to develop them, simply preventing the substitute product from reaching the market.

-

Defensive pricing: Using aggressive pricing strategies to drive out new competitors. For example, a local newspaper might use predatory pricing if a new competitor enters its market, making it unprofitable for the newcomer to continue.

Rivalry among existing firms

The degree of rivalry among current market competitors significantly affects prices and profits for individual firms.

When rivalry is fierce, businesses may reduce competition through:

Strategies to Manage Competitive Rivalry

-

Cartels and anti-competitive practices: Firms may collude to fix prices or divide markets. While this is illegal in UK and EU law, such practices still occur. These arrangements allow firms to maintain high prices by avoiding competition.

-

Horizontal integration: Buying rival businesses to reduce the number of competitors. Competition law may prevent some mergers, but most horizontal mergers proceed without regulatory intervention.

-

Non-price competition: In industries with few businesses, firms often avoid price competition to maintain profitability. Instead, they compete through new product development and advertising, creating strong brands. While this increases costs, it also allows firms to charge higher prices than in more competitive markets, generating higher profits overall.

Remember!

Key Takeaways

-

Competition intensity varies across markets from highly competitive (many firms, low barriers) to uncompetitive (monopoly or oligopoly with few firms, high barriers)

-

Monopolies involve a single supplier dominating an entire market, while oligopolies feature a few large firms dominating with interdependence between competitors

-

Markets are dynamic and change over time through new entrants increasing competition or consolidation reducing the number of competitors

-

Businesses must respond to competitive changes through strategies like going online, product innovation, mergers, or cost reduction - failure to respond risks decline or business failure

-

Porter's Five Forces provides a framework for analyzing competitive position by examining supplier power, buyer power, threat of new entrants, threat of substitutes, and rivalry among existing firms - managing these forces improves profitability and competitive advantage