Stakeholder Interest (Edexcel A-Level Business): Revision Notes

Stakeholder interest

Introduction to stakeholder interest

Financial statements provide valuable information to various stakeholder groups. The statement of financial position (balance sheet) offers different insights compared to the statement of comprehensive income, and stakeholders typically examine both documents together to form a complete picture of business performance.

Different stakeholder groups focus on specific aspects of financial statements based on their relationship with the business and their particular concerns. Understanding what each stakeholder looks for helps businesses manage their financial reporting effectively and maintain strong stakeholder relationships.

Each stakeholder group has unique priorities when analyzing financial statements. By understanding these different perspectives, businesses can communicate more effectively with their stakeholders and address their specific concerns.

Shareholders

Shareholders have multiple interests when examining a business's statement of financial position, focusing on three key areas: asset structure, capital structure, and business valuation.

Asset structure analysis

Shareholders examine how the business has invested the funds it has raised. The asset structure reveals where capital has been allocated and whether resources are being used effectively. For example, a business might have over 60% of its assets tied up in property, plant and equipment, indicating significant investment in fixed assets. This information helps shareholders assess whether management is making appropriate investment decisions aligned with the company's strategy.

Capital structure evaluation

The balance sheet shows the different sources of funding used by the business. Shareholders can identify what proportion of financing comes from equity versus debt. A business with 67% shareholder funding demonstrates strong equity backing, which reduces financial risk but may also limit growth if the business isn't leveraging debt financing effectively.

Solvency assessment

Shareholders use the balance sheet to evaluate whether the business can meet its short-term obligations. Solvency refers to a business having sufficient liquid assets to pay its bills when they fall due.

Working capital is a key indicator of solvency, calculated using the formula:

A business with working capital of only £1.7 million (£15.1 million current assets - £13.4 million current liabilities) might face solvency concerns because current liabilities are only just covered by current assets. Ideally, current assets should comfortably exceed current liabilities to provide a safety cushion.

Investment growth tracking

The value of net assets (total assets minus total liabilities) represents approximately the value of the business. Shareholders can track whether their investment is growing by comparing net asset values over time.

For instance, if net assets grow from £98.2 million to £108.7 million over one year, this indicates the business has increased in value by £10.5 million, directly benefiting shareholders through enhanced business value.

Managers and directors

Senior managers use the statement of financial position to maintain control over the business's financial health and make informed strategic decisions.

Monitoring financial position

Management teams must continuously monitor the firm's financial position to make sound operational and strategic decisions. The balance sheet provides a snapshot of the business at a specific point in time, showing what the business owns and owes.

Working capital management

Managers track working capital levels carefully to ensure the business doesn't overspend on current operations. Insufficient working capital can lead to cash flow problems, while excessive working capital might indicate inefficient use of resources. Regular monitoring helps maintain the right balance.

Financing decisions

When considering raising additional finance, managers must evaluate the existing capital structure before choosing an appropriate funding source. If the business already carries significant debt, taking on more borrowings might increase financial risk. In such cases, raising fresh equity capital could be a more suitable option, even though this dilutes existing shareholders' ownership.

Management must balance the benefits of different financing methods against the company's current financial position and strategic objectives. A highly leveraged business (high debt levels) should seriously consider equity financing to reduce financial risk, despite the dilution effect on existing shareholders.

Suppliers and creditors

Suppliers and lenders focus primarily on the business's ability to repay what it owes, making solvency their main concern.

Trade credit decisions

Suppliers assess working capital levels before offering trade credit terms. Businesses with limited working capital present higher risk because they may struggle to pay invoices on time. A company with small working capital might find it difficult to secure generous trade credit terms from suppliers.

However, suppliers also consider other factors beyond the balance sheet, including:

- The business's trading history

- Past credit record and payment patterns

- Relationship quality with the supplier

- Industry reputation

A long-standing relationship or excellent payment history might outweigh concerns about lower working capital levels.

Bank lending criteria

Banks and other financial institutions examine the balance sheet when making lending decisions. They evaluate:

- Current debt levels and gearing

- Asset values that could serve as security

- Working capital position

- Overall financial stability

Lenders use this information to assess credit risk and determine appropriate interest rates and lending terms.

Other stakeholders

Beyond the primary stakeholder groups, additional parties have legitimate interests in financial statements.

Employees

Workers may examine the balance sheet to assess:

- Whether the business can afford pay increases during wage negotiations

- Job security based on the company's financial strength

- The overall health and sustainability of their employer

Strong financial positions indicated by healthy working capital and growing net assets provide reassurance about employment stability.

Government bodies

The Office for National Statistics and other government agencies extract data from company accounts to compile national economic statistics. This information helps shape economic policy and provides insights into industry trends and economic performance across different sectors.

Tax authorities also scrutinize financial statements to ensure businesses correctly calculate and pay corporation tax and other tax obligations.

Working capital calculation

Understanding working capital calculations is essential for assessing a business's short-term financial health.

The formula

Working capital represents the funds available for day-to-day operations:

Components

Current assets typically include:

- Inventories (stock)

- Trade and receivables (money owed to the business)

- Cash and cash equivalents

Current liabilities typically include:

- Trade and other payables (money the business owes)

- Short-term borrowings

- Tax liabilities due within one year

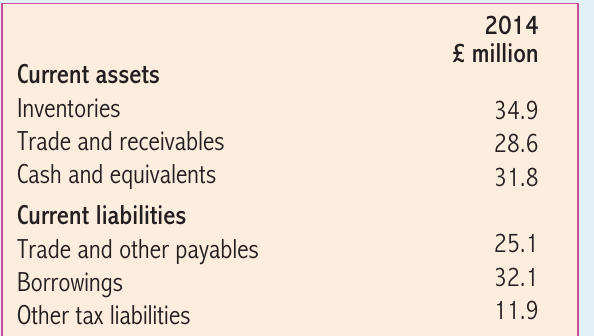

Worked example: Gallagher & Sons Ltd

Worked Example: Calculating Working Capital

Let's examine a practical calculation using data from a sweet and dessert manufacturer that supplies supermarkets and large retailers.

Using the figures from the table:

Current assets:

- Inventories: £34.9 million

- Trade and receivables: £28.6 million

- Cash and equivalents: £31.8 million

- Total current assets: £95.3 million

Current liabilities:

- Trade and other payables: £25.1 million

- Borrowings: £32.1 million

- Other tax liabilities: £11.9 million

- Total current liabilities: £69.1 million

Calculation:

Analysis:

Gallagher & Sons Ltd has £26.2 million in working capital. This appears adequate because current assets exceed current liabilities by approximately 1.4 times. This provides a reasonable cushion for meeting short-term obligations while maintaining operational flexibility.

A ratio of around 1.5:1 (current assets to current liabilities) is generally considered healthy, though this varies by industry. Manufacturing businesses often require higher working capital levels due to inventory requirements.

Exam guidance

Evaluation points:

When evaluating stakeholder interest in financial statements, consider:

- Context matters: What's adequate working capital for one business might be insufficient for another, depending on industry, business model, and growth stage

- Multiple perspectives: Different stakeholders prioritize different information - shareholders focus on returns, while suppliers prioritize payment capability

- Limitations: The balance sheet shows position at one point in time; trends over multiple periods provide better insights

- Qualitative factors: Financial position alone doesn't tell the whole story - reputation, market conditions, and management quality also matter

Command word application:

- Analyse: Break down stakeholder interests by explaining what specific groups look for and why it matters to them

- Evaluate: Weigh up whether financial position information alone provides sufficient basis for stakeholder decisions, considering limitations

- Assess: Judge the significance of working capital levels or capital structure in context of the specific business situation

Common exam mistakes to avoid:

- Confusing working capital with profit - working capital measures liquidity, not profitability

- Forgetting that adequate working capital varies by industry

- Ignoring that different stakeholders have different priorities

- Not applying financial concepts to the specific business scenario in the question

Remember!

Key Points to Remember:

- Working capital formula: measures short-term financial health

- Solvency means having sufficient liquid assets to pay bills when due - critical for business survival

- Different stakeholders use financial statements differently: Shareholders focus on asset and capital structure; suppliers focus on solvency; managers use it for operational decisions

- Capital structure shows funding sources - businesses heavily in debt should consider equity finance for expansion

- Net assets approximately equal business value, allowing shareholders to track investment growth over time