Finance and Banking (Edexcel A-Level Economics A): Revision Notes

The Role of the Central Bank

Introduction

The central bank plays a crucial part in a country's financial system and economy. In the UK, the Bank of England serves as the central bank, performing various essential functions that help maintain both monetary and financial stability. This chapter examines how central banks operate, the policy tools they use, and how their role has evolved in response to financial crises and economic challenges.

Understanding the central bank's role is vital for comprehending how governments and monetary authorities manage inflation, support economic growth, and respond to financial emergencies. The Bank of England's responsibilities have expanded significantly since gaining operational independence in 1997, particularly following the 2008 financial crisis.

Functions of the central bank

Almost every country has a central bank that carries out several important functions within the financial system. The central bank acts as the banker to the government and performs a variety of roles that can include issuing currency, managing government finances, providing liquidity to commercial banks, and regulating the financial sector.

Key term: Central bank - The banker to the government, performing a range of functions, which may include issue of coins and banknotes, acting as banker to commercial banks and regulating the financial system.

Issuing notes and coins

One of the traditional functions of the central bank is controlling the supply of physical money in the economy. In the UK, the Bank of England has responsibility for issuing banknotes and coins, though it does not have a complete monopoly. Commercial banks in Scotland and Northern Ireland can also issue banknotes, but this is regulated by the Bank of England to ensure that money supply remains appropriate and does not fuel inflation.

However, issuing physical currency is less significant today than in the past. Modern economies use many different types of financial assets and payment methods, so controlling notes and coins alone does not give the central bank full control over the money supply. Electronic payments, credit cards, and digital banking have transformed how transactions occur in the twenty-first century.

Banker to the government

The Bank of England provides banking services to the government, handling tax revenues and government spending transactions through government accounts held at the Bank. Historically, the Bank also managed the government's borrowing programme by issuing Treasury bills. However, this function was transferred to the Debt Management Office (an executive agency within the Treasury) when the Bank was granted independence to set interest rates in 1997, ensuring separation between monetary policy decisions and government financing needs.

Banker to commercial banks

Commercial banks and other participants in the Sterling Monetary Framework (SMF) hold deposits at the Bank of England in the form of reserve balances and cash ratio deposits. These reserves serve multiple purposes: they act as liquid assets that banks can access quickly, and they help facilitate clearing operations between different banks.

The clearing function works by equalising imbalances in daily transactions between major banks. In normal circumstances, the Bank of England agrees an average level of overnight reserves that SMF participants should hold for the month ahead. If a bank needs to borrow beyond its agreed reserve level, it faces a charge. Conversely, deposits above the agreed average earn interest below Bank Rate. This system encourages banks to maintain appropriate reserve levels and helps keep the interbank rate close to Bank Rate.

Managing the exchange rate

The Bank of England manages the UK's gold and foreign currency reserves on behalf of the Treasury. In recent years, direct interventions in foreign exchange markets have been rare, with the pound generally allowed to find its own level in the market. This reflects a policy of allowing exchange rates to be determined primarily by market forces rather than through active central bank intervention.

Monetary and financial stability

Beyond the specific functions outlined above, the Bank of England's overarching mission is to promote the good of the people of the United Kingdom by maintaining monetary and financial stability.

Key terms:

- Monetary stability - A situation in which there is stability in prices relative to the government's inflation target

- Financial stability - A situation in which there is a sufficient and efficient flow of liquidity in the economy

- Lender of last resort - The role of the central bank in guaranteeing sufficient liquidity is available in the monetary system

The Dual Objectives of Central Banking:

Monetary stability means maintaining low and predictable inflation, consistent with the government's inflation target. Financial stability requires ensuring adequate liquidity flows through the economy and that UK financial institutions operate soundly. These core activities have significant implications for money and credit availability throughout the economic system.

The challenge for central banks is balancing these two objectives, particularly during crises when pursuing one objective might conflict with the other.

The efficient flow of funds requires sufficient liquidity in the economy. Financial institutions must have enough liquid assets to conduct their business. Traditionally, the Bank of England fulfilled this by acting as lender of last resort, prepared to lend to banks that could not obtain funds elsewhere, though at a penalty rate. Events during the 2008 financial crisis demonstrated the limitations of this traditional approach, as we shall explore later.

Inflation targeting and policy measures

The inflation target framework

A major change in UK monetary policy occurred in 1997 when the incoming Labour government granted the Bank of England operational independence. The Bank was given responsibility for using interest rates to achieve the inflation target set by the government, representing a fundamental shift in how monetary policy was conducted.

This change aimed to enhance the credibility of government policy. By removing discretionary control over interest rates from politicians, it signalled a pre-commitment to controlling inflation. This was expected to improve expectations about the future path of the macroeconomy, reducing the temptation to use short-run policy measures to create a "feel-good" factor before elections.

Key term: Monetary Policy Committee (MPC) - Body within the Bank of England responsible for the conduct of monetary policy.

The Monetary Policy Committee (MPC) has primary responsibility for maintaining monetary stability by meeting the inflation target. However, it also has a secondary responsibility to support the government's broader economic policy, including objectives for growth and employment. This means the MPC cannot pursue the inflation target if doing so would excessively endanger growth or employment.

The challenge during the inflation targeting period has been balancing the needs of monetary stability (meeting the inflation target) with ensuring financial stability (maintaining adequate liquidity provision). An independent central bank pursuing the inflation target reinforces government credibility, but the risk is that this could be pursued at the expense of economic growth.

An inflation target

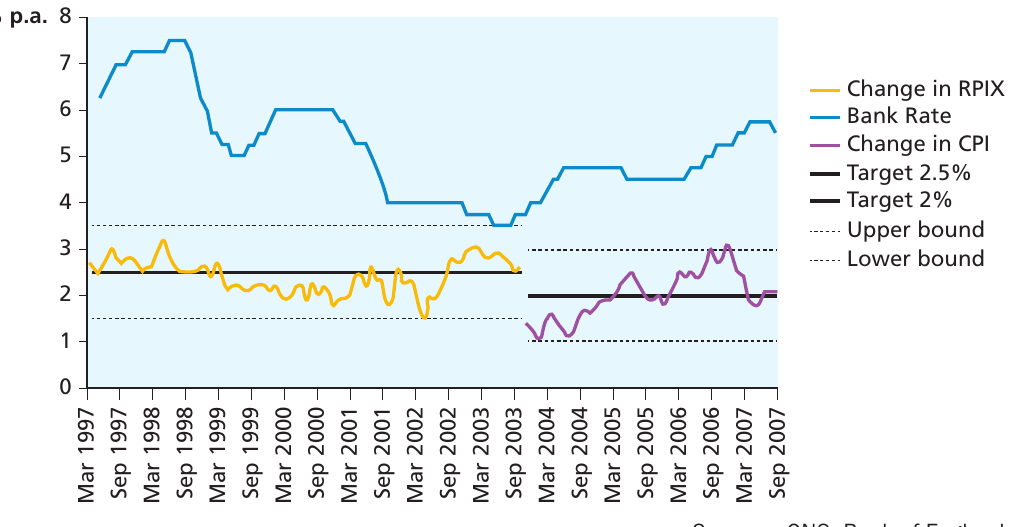

In 1997, the Bank of England was tasked with keeping inflation within 1 percentage point of the target, initially set at 2.5% as measured by the retail price index (RPIX). From January 2004, the target was reset using the consumer price index (CPI), with its rate of change required to fall within 1 percentage point of 2%.

The "Great Moderation" Period:

The period from 1997 to 2007 was characterised by relative stability. The chart above shows how Bank Rate and inflation moved during this time. Inflation remained within the specified 1 percentage point target range for most of the period, with only one brief exception in March 2007 when it rose to 3.1%. Economic growth was steady, and there were no obvious problems with liquidity provision. This period is sometimes referred to as the "Great Moderation."

Bank Rate and open market operations

The Bank of England targets inflation primarily by adjusting the interest rate. Financial markets contain many different interest rates reflecting various degrees of risk, loan lengths, and other factors. However, these rates are interconnected, allowing the Bank to influence the overall structure of rates by changing the rate it charges on short-term loans to domestic banks.

Key terms:

- Bank Rate - The rate of interest charged by the Bank of England on short-term loans to other banks

- Open market operations - Intervention by the central bank to influence short-run interest rates by buying or selling securities

This key rate is known as Bank Rate. Changes in Bank Rate affect interest rates throughout the financial system, as shown in the previous figure. These changes ultimately influence aggregate demand and inflation in the economy.

Interest rates also respond to market conditions. The Bank of England can intervene to ensure short-run interest rates align with Bank Rate through open market operations - buying or selling securities to influence short-run interest rates.

How Open Market Operations Work:

Suppose liquidity becomes scarce in the financial system. Financial institutions need to borrow to improve their liquidity position, putting upward pressure on interest rates and creating a risk that rates will move away from Bank Rate.

The Bank's Response: The Bank can intervene by providing liquidity through purchasing securities (Treasury bills or gilts) in the open market.

The Opposite Scenario: Conversely, if excess liquidity exists, interest rates may fall, and the Bank can prevent this by selling securities in the open market.

This mechanism allows the Bank to maintain control over short-term interest rates even when market conditions change.

Banks in difficulty and the financial crisis

Even by 2007, it was becoming apparent that several banks were facing difficulties, having expanded their lending substantially relative to their capital base. The response was to reduce lending, sell assets, and seek new capital. Property-backed lending was a root cause, as expectations of continuing house price rises had encouraged mortgage lending. When US house prices stalled in 2005-06, defaults rose, putting pressure on lenders. Some institutional failures triggered recession fears, and globalisation meant financial markets were interconnected across national boundaries.

The "Too Big to Fail" Problem:

A significant problem with bank failures is their effect on confidence in the financial system. During the crisis, it was perceived that some banks were "too large" to be allowed to fail. The collapse of a major financial institution would have such severe effects on expectations that the entire financial system might be questioned.

This prompted moves by the UK and other governments to bail out banks in difficulty, despite the impact on public finances. This created a moral hazard problem that would need to be addressed through future regulation.

Shortage of liquidity and quantitative easing

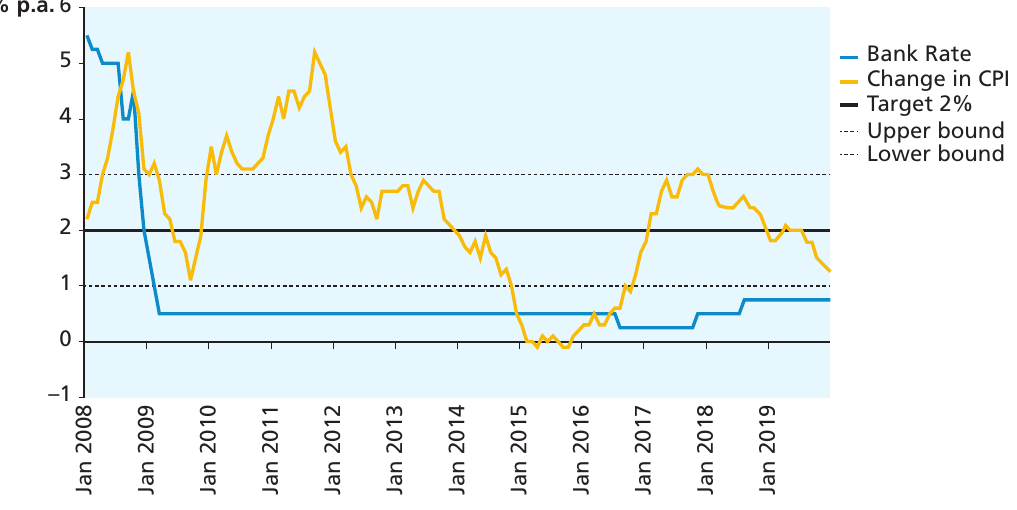

In the UK, the crisis manifested in the interbank market, where liquidity shortages put upward pressure on the interbank rate. By March 2009, Bank Rate had been reduced to 0.5%, the lowest possible sustainable level, though it was subsequently reduced to 0.1% in March 2020 and maintained until December 2021. With Bank Rate at such low levels, the reserves averaging regime could no longer function effectively. Instead, the Bank introduced quantitative easing in 2009.

Key term: Quantitative easing - Process by which liquidity in the economy is increased when the central bank purchases assets from the commercial banks.

Quantitative easing is essentially a method of increasing money supply. The foundations were established in January 2009 by creating the Asset Purchase Facility (APF), a subsidiary of the Bank of England that conducts the necessary transactions. By mid-2016, the APF had purchased £445 billion of assets through central bank reserves creation. The MPC decides the level of quantitative easing jointly with decisions on Bank Rate.

The Bank of England faced a dilemma: inflation needed to be controlled, but simultaneously the reluctance of banks to lend was affecting investment and real economic growth, threatening prolonged recession. Expectations were weak, risking extended recession. The UK was not alone in facing these challenges, with other central banks adopting similar strategies. Inflation rose above its target again in 2010-11, but then returned to closer to normal levels in the late 2010s.

Recovery from the crisis

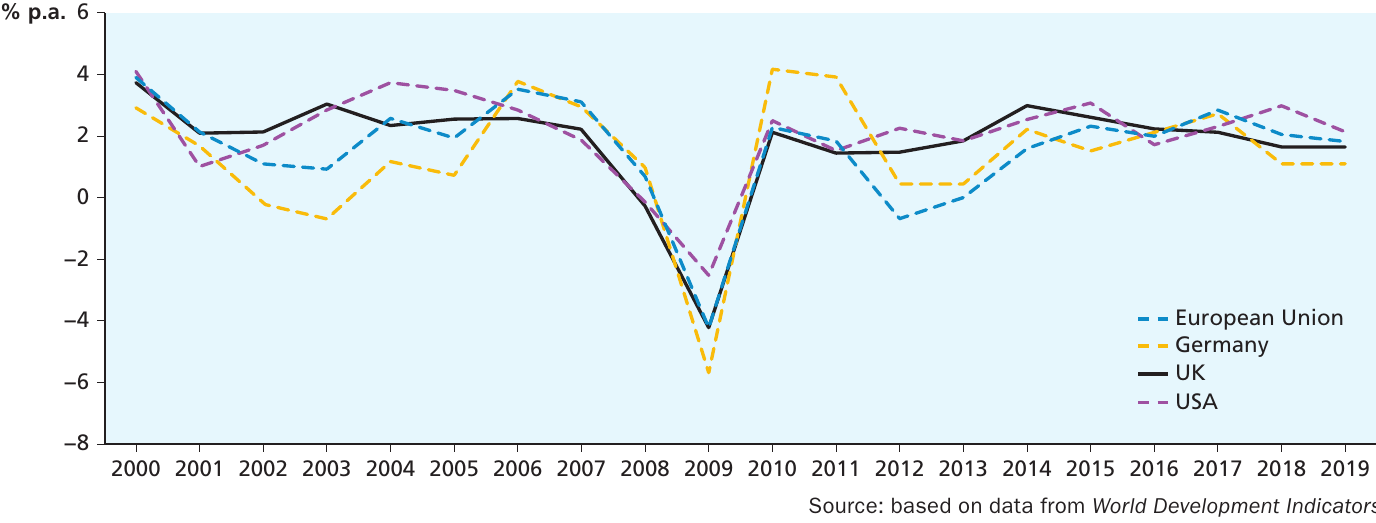

The chart above illustrates how several countries followed similar paths for economic growth. The sharp fall in growth during the financial crisis is clearly visible. Having labelled the financial turmoil as the worst since the 1930s, governments were determined to avoid repeating the mass unemployment of that earlier period. This was prevented, but recovery was not rapid. It is challenging to determine the extent to which recovery resulted from the policy stance adopted by governments and central banks.

Financial regulation

One commonly held view was that inadequate regulation of financial institutions was a key factor leading to the 2008 crisis. Banks had built up lending portfolios that carried excessive risk beyond what their capital could cover. Although central banks like the Bank of England had structures to achieve monetary stability, the regulatory framework had not provided the same degree of control over financial stability.

The new regulatory framework

A new regulatory framework came into operation in April 2013 to remedy this situation and avoid repetition of the financial crisis. Two new statutory decision-making bodies were created as part of the Bank of England to address both microprudential and macroprudential regulation.

Key terms:

- Prudential Regulation Authority (PRA) - The decision-making body in the Bank of England responsible for microprudential regulation of deposit-takers, insurers and major investment firms

- Microprudential regulation - Financial regulation intended to set standards and supervise financial institutions at the level of the individual firm

- Financial Policy Committee (FPC) - The decision-making body of the Bank of England responsible for macroprudential regulation

- Macroprudential regulation - Financial regulation intended to mitigate the risk of the financial system as a whole

- Financial Conduct Authority (FCA) - A body separate from the Bank of England responsible for conduct regulation of financial services firms

Understanding the Three-Pillar Regulatory Framework:

The Prudential Regulation Authority (PRA) is responsible for microprudential regulation, operating at the individual firm level to promote the safety and soundness of deposit-takers, insurers and major investment firms.

The Financial Policy Committee (FPC) is responsible for macroprudential regulation, with the mandate of "identifying, monitoring and taking action to remove or reduce systemic risks with a view to protecting and enhancing the resilience of the UK financial system. And, subject to that, supporting the economic policy of the Government, including its objectives for growth and employment."

The Financial Conduct Authority (FCA) was given responsibility for ensuring that relevant markets function well, with responsibility for financial services firms not supervised by the PRA, including asset managers, hedge funds, broker-dealers and independent financial advisers.

The intention was to improve the resilience and stability of the financial system by filling a perceived regulatory gap that had allowed the seeds of the crisis to develop. The USA and other EU countries established similar new bodies to perform comparable tasks, crucial given the interconnectedness of financial markets following globalisation.

Powers and responsibilities

The FPC has authority to make recommendations. For example, it can recommend that the PRA and FCA take action to safeguard financial stability. These bodies must comply or explain why this is not appropriate. The FPC can use the countercyclical capital buffer, under which banks, building societies and large investment firms can be required to hold additional loss-absorbing capital. The FPC can also impose sectoral capital requirements, requiring firms to meet additional capital requirements where the FPC perceives risk to the financial system as a whole. Furthermore, the FPC can recommend changes to the boundary between regulated and non-regulated activities.

These measures aim to reduce the likelihood of future financial crises by monitoring activity more closely and providing early warning of emerging problems. The FPC and PRA can then take action to mitigate crisis risks. Given globalisation's impact, there is recognition of the need for international coordination of financial regulation.

Evaluation of the response to the crisis

The financial crisis highlighted the importance of the financial system for the real economy. Prior to the crisis, the system had been performing well, with the inflation target being met and economic growth proceeding steadily. However, inadequate regulation led to a build-up of pressure that erupted in financial instability, with spillover effects for the real economy, resulting in recession and rising unemployment.

The main consequence was the failure of liquidity. The Bank of England resorted to expansion of money supply through quantitative easing to supply liquidity while keeping inflation within its target range. The need for financial stability was addressed by creating new decision-making bodies responsible for maintaining financial stability through enhanced regulation of the financial system and monitoring developments in financial markets.

In maintaining both monetary and financial stability objectives, the Bank of England must balance these with its secondary objective of supporting the government's overall macroeconomic policy stance. This has proven challenging, particularly when the need to bail out failing banks left a legacy of high public debt, made worse by increased national debt from COVID-19 pandemic measures and the reappearance of inflation.

The international context

The financial crisis was not just a UK problem but affected most advanced economies. Indeed, some European countries faced more severe conditions than the UK. The Bank of England's actions should therefore be viewed in the context of international financial system oversight by the Bretton Woods institutions.

Globalisation has created the need for coordination of financial markets across countries. Deregulation increased the interconnectedness of financial markets, and technological advances allowed financial transactions to occur smoothly and instantaneously. This improved market efficiency but also heightened the possibility of contagion - the rapid spread of crises between countries.

Three key organisations contribute to international coordination of financial markets and regulation: the Bank for International Settlements (BIS), the International Monetary Fund (IMF), and the World Bank. Each fulfils a specific function in the global financial system.

The Bank for International Settlements

Key term: Bank for International Settlements (BIS) - An institution that acts as a bank for central banks and sets standards for regulation of banks that are accepted globally.

The Bank for International Settlements (BIS) was originally established in 1930 to settle the then-controversial issue of reparation payments imposed on Germany after the First World War. The onset of the Great Depression changed its focus, which switched to activities involving technical cooperation between central banks. The Bretton Woods conference called for the BIS's abolition on the grounds it would be rendered redundant by the IMF and World Bank. However, instead it refocused on European monetary and financial issues, becoming a forum for European monetary cooperation.

After the collapse of the Dollar Standard in the early 1970s, the need for international cooperation in financial market operation became apparent. In 1982, a group of central bankers (known as G10) created the Basel Committee on Banking Supervision, which played a key role in financial regulation. The debt crisis affecting several Latin American countries in the early 1980s highlighted the need for measures to provide regulation and avoid the possibility of sovereign default (where nations fail to meet their international debt obligations).

The Basel Committee established a credit risk measurement framework that became a globally accepted standard. This has been refined over time, with the latest agreement being the Basel III agreement, which specifies internationally agreed capital adequacy requirements for banks. These are administered by central banks. In the UK, Basel III capital requirements are built into the Bank of England's regulatory framework. The requirements were due to be complete by 2019, with gradual phasing in to avoid slowing recovery. However, full implementation was delayed by the COVID-19 pandemic. In March 2022, the Bank of England indicated that the new regulations would become effective in January 2025.

In this way, it is hoped that the likelihood of financial instability spreading across countries will be reduced, as central banks impose similar regulation on their respective financial systems.

The International Monetary Fund

In the twenty-first century, the IMF continues to play an important role in maintaining the stability of the interconnected global financial system. In particular, it has provided loans to prevent sovereign default. An example is the loan provided to Greece in 2010. The IMF has also provided loans to governments needing to bail out private banks that had become insolvent due to exposure to risky loans. More recent examples include loans to the governments of Ireland, Latvia and Hungary.

Evaluation of international cooperation

Globalisation has increased the interdependence of countries. This allows people around the world to share in economic success and gain mutual advantage through trade. However, it also allows financial crises to spread more rapidly, creating a need for international cooperation in regulating financial markets to reduce the likelihood of financial problems occurring.

The BIS, IMF and World Bank have contributed by providing a global framework within which financial markets can be coordinated and common regulations agreed. However, this has not been sufficient to prevent crises from occurring, such as the Asian financial crisis of 1997 and the credit crunch of the late 2000s. In earlier years, the debt crisis of the 1980s gave warning that serious problems could occur when markets are not carefully monitored.

During the 1980s debt crises, there was considerable criticism that the response measures, such as debt rescheduling for developing countries, were designed to safeguard the global financial system but not to provide a permanent remedy for that debt. Only with the HIPC Initiative did the World Bank agree to allow debt forgiveness for developing countries - and even then under strict conditions. This may have impeded development in some countries, especially in sub-Saharan Africa, where debt put strain on resources. Some progress has now been made in promoting growth and development in developing countries, and measures have been put in place to improve global financial system stability in future. Less encouraging is the disruption caused by the COVID-19 pandemic and the war in Ukraine.

The impact of COVID-19 and the war in Ukraine

The global economic landscape changed dramatically in the early 2020s, first with the spread of the COVID-19 pandemic in 2020, and later with the invasion of Ukraine in 2022. These events required drastic action from governments and central banks.

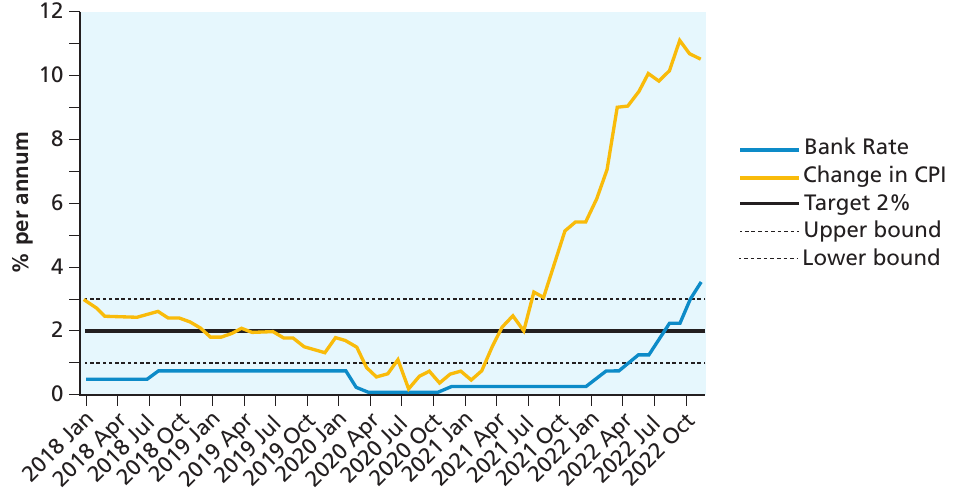

During 2018 and 2019, inflation seemed well under control, although the transition to Brexit had caused some supply chain issues. The COVID-19 pandemic hit the UK in early 2020, with lockdown impositions severely affecting GDP. Inflation fell below its target, and the Bank of England reduced Bank Rate to just 0.1%. From March 2020, the Bank introduced quantitative easing to help cushion the pandemic's impact.

An additional £200 billion of bond purchases was undertaken in March 2020, followed by a further £100 billion in June and another £150 billion in November, bringing the total to £895 billion, almost all from government bond purchases. When Russia invaded Ukraine in 2022, inflation began to accelerate, as shown in the chart below. The Bank then began to raise Bank Rate to try to mitigate the impact.

The Cost-Push Inflation Challenge:

The emergence of this cost-of-living crisis highlights a key challenge. The Bank could not prevent the acceleration of inflation solely by using Bank Rate, partly because the inflation resulted from cost-push factors. Therefore, restraining aggregate demand would not be enough to keep price rises under control.

This illustrates the fundamental tension between the Bank's objectives: raising interest rates to control inflation could harm economic growth and employment, while keeping rates low to support growth would allow inflation to accelerate further.

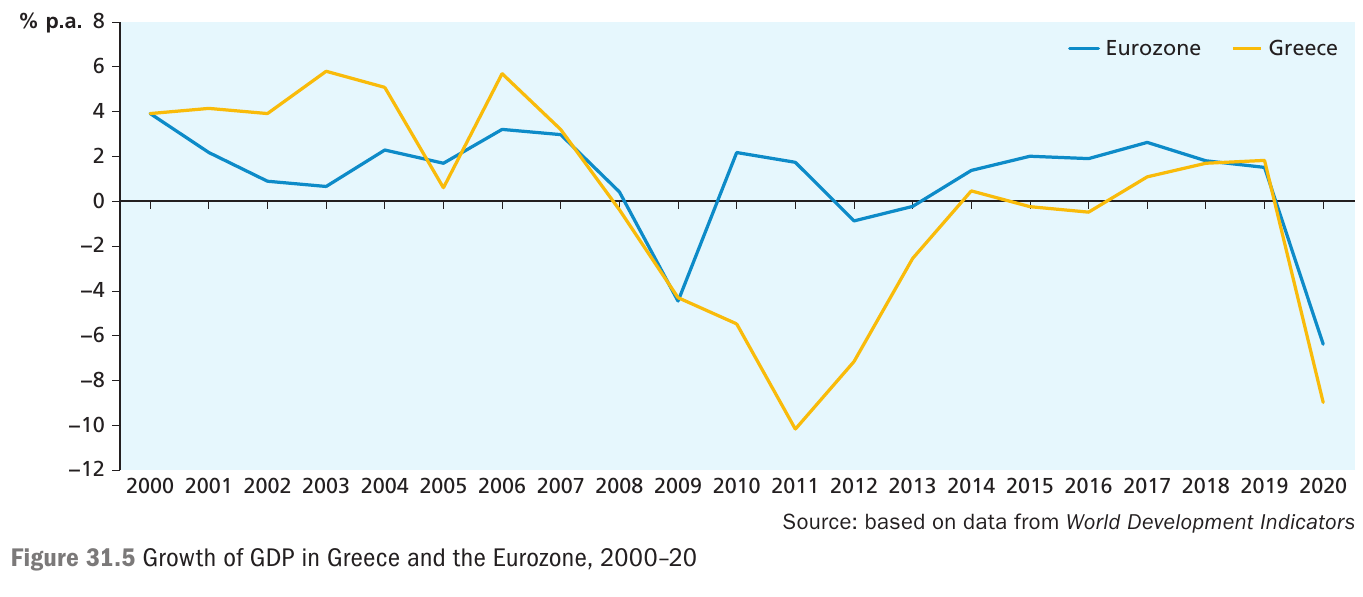

Case study: The bailout of Greece in 2010

Case Study: The Greek Sovereign Debt Crisis

In May 2010, the EU and IMF announced a €110 billion bailout loan for Greece. Traditionally, the IMF made loans to help countries overcome balance of payments problems or to stabilise their currency. But does that apply to this example?

The Real Purpose: In this case, there was only one reason for the IMF to lend money to Greece: to prevent a Greek sovereign default. Prior to the credit crunch, highly indebted governments could borrow cheaply. Governments such as Greece took advantage of low borrowing costs by using debt to finance better public services. The recession following the 2008 crash dented confidence, leading to increased cost of borrowing. In Greece, government debt servicing costs climbed, creating an even bigger fiscal deficit. The government was in a debt spiral, and a Greek sovereign default seemed imminent.

Who Really Benefited?: However, this was not a bailout for the Greek people. Ordinary Greeks did not receive their share of the loan to reduce hardship or support German banks. Instead, the money borrowed was used by the Greek government to pay its bondholders. These bondholders were French and German banks. According to research by the Bank for International Settlements at the end of 2010, 96% of Greek government bonds were held by European banks. German banks alone held €22.7 billion of Greek debt. The Greek "rescue package" was really designed to save the German and French banking system, which would have collapsed if Greece had defaulted.

The Long Road to Recovery:

The chart above shows how long it took for Greece to begin recovering from the recession that followed the financial crash. GDP growth did not turn positive until 2014, and then growth was not secure. The onset of the COVID-19 pandemic in 2020 pushed Greece back into negative growth.

Remember!

Key Points to Remember:

Central Bank Functions:

- The central bank performs multiple critical functions including issuing currency, acting as banker to the government and commercial banks, managing exchange reserves, and regulating the financial system

Operational Independence and Inflation Targeting:

- The Bank of England was granted operational independence in 1997 to set Bank Rate to meet the government's inflation target (currently 2% CPI ±1%)

- The MPC has primary responsibility for monetary stability but must also support broader economic objectives

Crisis Response and Quantitative Easing:

- During the 2008 financial crisis, traditional policy tools proved insufficient

- When Bank Rate reached its effective lower bound, the Bank introduced quantitative easing to inject liquidity into the financial system, ultimately purchasing £445 billion of assets by mid-2016

Post-Crisis Regulatory Reforms:

- Post-crisis regulatory reforms created a new framework with three bodies:

- PRA (microprudential regulation of individual firms)

- FPC (macroprudential regulation of systemic risk)

- FCA (conduct regulation of financial services)

- This aimed to prevent future crises by enhanced monitoring and supervision

International Cooperation:

- International cooperation through institutions like the BIS (setting global banking standards) and the IMF (providing emergency loans) is essential in an interconnected global financial system

- However, crises can still spread rapidly across borders, as demonstrated by the 2008 crisis and subsequent European debt problems

Recent Challenges:

- Recent challenges including COVID-19 and the Ukraine war have tested the Bank's ability to balance monetary and financial stability

- The Bank cut rates to 0.1% and implemented £895 billion of quantitative easing during the pandemic, but then faced difficult choices when cost-push inflation emerged in 2022