Central Banks and Monetary Policy (AQA A-Level Economics): Revision Notes

Central Banks and Monetary Policy

Introduction to central banks

A central bank is a national institution that provides financial and banking services to its country's government and banking system. It also implements the government's monetary policy and issues the national currency.

In the UK, the Bank of England serves as the central bank. The Bank of England was established in 1694 as a private company. However, it was nationalised in 1946, meaning its profits now go to the state. In 1997, the Bank was granted 'operational independence', freeing it from direct political control when setting monetary policy. Despite this independence, the UK government still 'owns' the Bank of England.

Understanding Operational Independence

The 1997 grant of operational independence was a significant turning point for UK monetary policy. It meant that elected politicians could no longer directly influence interest rate decisions, reducing the temptation to manipulate rates for short-term political gain. However, the government still sets the inflation target that the Bank must achieve.

The European Central Bank (ECB) implements monetary policy for countries using the euro as their official currency.

The main functions of a central bank

Central banks have two primary functions: maintaining macroeconomic stability and ensuring financial stability within the monetary system.

Macroeconomic stability

The Bank of England's main task is to deliver price stability. This means keeping inflation at the government's target rate. The current inflation target is 2% as measured by the Consumer Price Index (CPI). The government sets this target, not the Bank itself.

It's important to understand the difference between macroeconomic stability and macroeconomic performance:

- Macroeconomic stability means achieving stable growth, stable employment, a stable price level, and stability in the current account of the balance of payments

- Macroeconomic performance refers to the extent to which these desirable objectives are actually being achieved

The Inflation Target Band

The inflation target has a margin of flexibility. If inflation moves outside a band of 1% above or below the 2% target (that is, if it goes above 3% or falls below 1%), the Governor of the Bank of England must write an open letter to the Chancellor explaining why this has happened. This accountability mechanism ensures transparency whilst allowing some flexibility in achieving the target.

While price stability is the primary focus, the Bank must also support the government's wider economic objectives, including promoting growth and employment. This is particularly important during economic downturns, as happened during the 2008-09 recession when controlling inflation was temporarily placed on the back-burner to focus on economic recovery.

Financial stability

The central bank achieves financial stability partly by acting as lender of last resort to the banking system. This function is standard practice for central banks worldwide.

The lender of last resort function means the central bank stands ready to lend money to commercial banks that are solvent (fundamentally sound) but facing short-term liquidity problems (difficulty accessing cash quickly). By providing these emergency funds, the central bank protects depositors and, in extreme cases, helps prevent a systemic crisis in the financial system.

Other central bank functions

Beyond these core roles, central banks also:

- Control the note issue (printing and distributing banknotes)

- Act as the bankers' bank (commercial banks hold accounts at the central bank)

- Serve as the government's bank

- Buy and sell currencies to influence the exchange rate

- Liaise with overseas central banks and international organisations

The Bank of England used to act more directly as the government's banker. However, since 1998, the Debt Management Office (DMO) has issued government bonds (gilts) on behalf of the Treasury. In 2000, the DMO also took over responsibility for issuing Treasury bills and managing the government's short-term cash needs.

Implementing monetary policy

What is monetary policy?

Monetary policy is the part of economic policy that uses monetary instruments to achieve the government's macroeconomic objectives. These instruments include controls over bank lending and interest rates.

Before 1997, the Bank of England and the Treasury worked together on monetary policy decisions. The Bank 'consulted' with the Treasury, which had the final say over interest rate changes. They were known as the monetary authorities. However, in 1997, the government made the Bank of England operationally independent and the sole monetary authority.

Objectives and instruments of monetary policy

To understand monetary policy properly, we need to distinguish between policy objectives and policy instruments:

- A policy objective is the target that policymakers aim to hit

- A policy instrument is the tool used to achieve that objective

Policy objectives can be divided into ultimate objectives (the final goals) and intermediate objectives (stepping stones towards the final goals). Policy instruments can be separated into those that directly affect the supply of new deposits that commercial banks create, and those that influence the demand for loans or credit.

The Monetary Policy Committee (MPC)

For over 35 years, controlling inflation has been the main objective of UK monetary policy. The government sets the inflation target to create conditions that support improved economic welfare.

Since 2003, the inflation target has been 2% CPI inflation (with a margin of error of plus or minus 1%). The Chancellor instructs the Bank of England's Monetary Policy Committee (MPC) to operate monetary policy to 'hit' this target.

The MPC was established in 1997 to set interest rates at the level needed to achieve the government's inflation target. The committee meets eight times per year. Its members include various Bank of England officials (including the Governor) and independent experts. The composition can change over time.

MPC Decision-Making

The MPC decides whether to increase, decrease, or maintain interest rates at their current level. It also sets other aspects of monetary policy, such as quantitative easing. Each member votes on the decision, and the vote is made public, promoting transparency and accountability in monetary policy decisions.

Monetary policy instruments

Monetary policy instruments are the tools used to achieve monetary policy objectives. In the UK, these can involve the Bank of England taking action to influence interest rates, the supply of money and credit, and the exchange rate.

Before 2009, UK monetary policy relied almost exclusively on the MPC's use of Bank Rate to manage the demand for bank loans. Since 2009, quantitative easing and other aspects of monetary policy have become increasingly important.

Bank Rate as the main monetary policy instrument

Bank Rate (also called the base rate) is the rate of interest that the Bank of England pays to commercial banks on their deposits held at the Bank of England.

Managing the demand for credit through Bank Rate

In normal circumstances, monetary policy is used to manage aggregate demand in the economy. To understand how this works, recall the aggregate demand equation:

Where:

- = consumption

- = investment

- = government spending

- = net exports (exports minus imports)

Fiscal policy affects aggregate demand by changing government spending (). Monetary policy affects the other components: consumption (), investment (), and net exports .

Factors considered by the MPC when setting Bank Rate

When deciding whether to raise, lower, or maintain Bank Rate, the MPC considers several key factors:

- The current rate of inflation

- Whether inflationary or deflationary pressure exists

- Consumer and business confidence levels

- The economy's growth rate

- Employment and unemployment levels

- Other economic indicators

The MPC currently has flexibility of 1% above and below the 2% CPI inflation target. If inflation moves outside this 1-3% band, the Governor must write an open letter to the Chancellor explaining the reasons.

The symmetrical approach (before 2008-09)

For several years before the 2008-09 recession, monetary policy operated symmetrically:

- The Bank of England stimulated aggregate demand (raising inflation) whenever inflation was expected to fall below the target rate

- It decreased aggregate demand (to reduce inflation) whenever inflation was expected to exceed the target

However, during the 2008-09 recession, this approach changed. Negative economic growth and rising unemployment meant that controlling inflation took a back seat. Instead, monetary policy aimed to increase aggregate demand and stimulate recovery from recession. The Bank's primary price stability objective was temporarily subordinated to supporting growth and employment.

How monetary policy affects the economy

Contractionary monetary policy

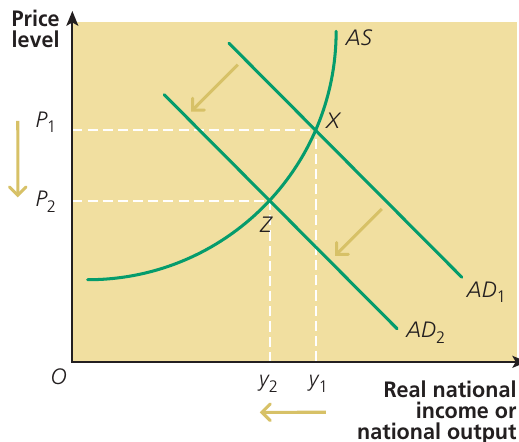

In contractionary monetary policy, the Bank of England raises interest rates to take demand out of the economy.

Higher interest rates shift the aggregate demand (AD) curve to the left. The extent to which the price level falls (or more realistically, the rate of inflation falls) and real output falls depends on the shape of the economy's aggregate supply (AS) curve.

The diagram shows how increasing Bank Rate in a contractionary monetary policy shifts the AD curve leftward from to . This causes both the price level and real output to fall, from to and from to respectively.

The Trade-Off in Contractionary Policy

This illustrates why contractionary monetary policy, which aims to control inflation, might also push the economy into recession. This risk is especially high if the policy triggers a large multiplier effect that shifts the AD curve significantly to the left. Policymakers must carefully balance the benefits of lower inflation against the costs of reduced output and employment.

Expansionary monetary policy

Expansionary monetary policy operates in the opposite way. When the Bank of England cuts Bank Rate, it discourages saving whilst stimulating borrowing, consumption, and investment. Lower interest rates also cause the exchange rate to fall, making exports more price competitive and imports less competitive. The AD curve shifts to the right, with the size of the shift depending on the multiplier.

The extent to which real output increases or the price level rises depends on the shape and slope of the economy's AS curve. When the economy produces well below its normal capacity level, the AS curve is relatively 'flat'. In these circumstances, expansionary monetary policy is likely to increase real output (and jobs), whereas the increasing 'steepness' of the AS curve as normal capacity utilisation approaches means that stimulation of real output gives way to price inflation.

How an increase in interest rates decreases aggregate demand

Monetary policy shifts the AD curve in the economy rather than the AS curve. This reflects its role in managing aggregate demand.

There are three main ways that higher interest rates decrease aggregate demand:

Higher interest rates reduce household consumption (C)

Higher interest rates affect consumption in several ways:

-

Saving becomes more attractive: Higher interest rates encourage people to save more, leaving less income available for consumption.

-

Borrowing costs increase: Higher interest rates mean borrowers pay more in interest on mortgages and credit card debt. They have less money available to spend on consumption because more of their income goes towards interest payments.

-

Asset prices fall: Higher interest rates may cause asset prices (such as house prices and share prices) to fall. These falling prices reduce personal wealth, which reduces consumption. Lower house and share prices also reduce consumer confidence, further deflating consumption.

-

Confidence effects: Falling asset prices independently reduce consumer confidence, leading to lower spending.

How Higher Interest Rates Affect a Homeowner

Consider a homeowner with a $200,000 mortgage:

- At 2% interest rate: Annual interest payment = $4,000

- At 5% interest rate: Annual interest payment = $10,000

- Difference: $6,000 less available for consumption per year

This homeowner now has $6,000 less to spend on goods and services. If this happens across millions of households, the aggregate effect on consumption () becomes substantial, shifting the AD curve to the left.

Higher interest rates reduce business investment (I)

Investment means the purchase of capital goods (such as machinery) by firms. When interest rates rise, businesses postpone or cancel investment projects because higher borrowing costs make purchasing capital goods unprofitable. This effect is likely worsened by falling business confidence and increased business pessimism.

Higher interest rates affect exports and imports (X - M) via the exchange rate

Higher interest rates increase demand for pounds by attracting capital flows into the currency. The increased demand for sterling causes the pound's exchange rate to rise, making UK exports less price competitive in world markets and imports more competitive in UK markets. The UK's balance of payments on current account worsens, which shifts the AD curve leftwards.

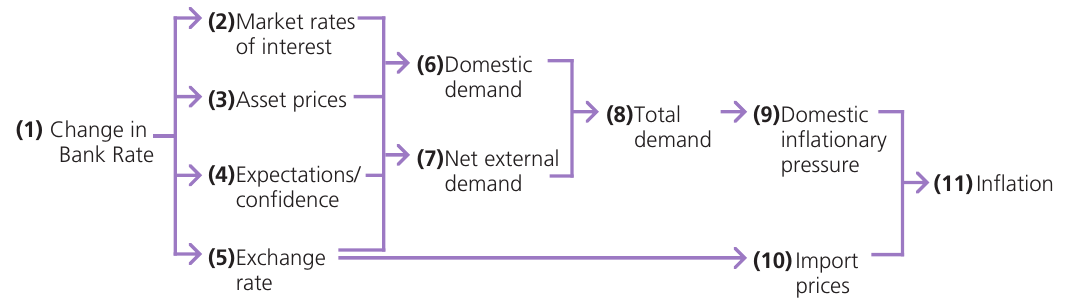

The transmission mechanism of interest rate policy

The Bank of England explains that changes in Bank Rate affect aggregate demand and inflation through several channels. These channels form the transmission mechanism of Bank Rate policy.

The flowchart shows the routes through which changes in Bank Rate (the instrument of monetary policy, shown at point 1) eventually affect inflation (the objective of monetary policy, shown at point 11).

Understanding the Transmission Mechanism

The transmission mechanism describes the complex pathway through which monetary policy decisions affect the real economy. It's not a simple, direct relationship but rather a series of interconnected effects that work through multiple channels simultaneously.

Official Bank Rate decisions (point 1) affect market interest rates (point 2), such as mortgage rates and bank deposit rates set by commercial banks and other financial institutions. At the same time, policy actions and announcements affect expectations about the future course of the economy and the confidence with which these expectations are held (point 4). They also affect asset prices (point 3) and the exchange rate (point 5).

A rise or fall in the exchange rate changes import prices (point 10), which in turn affect the rate of inflation.

These changes affect aggregate demand in the economy (point 8). This comprises domestically generated demand (point 6) and net external demand (point 7), determined by export and import demand.

Domestic demand results from the spending, saving, and investment behaviour of individuals and firms within the economy. Lower market interest rates increase domestic demand by encouraging consumption rather than saving by households, and investment spending by firms. Conversely, higher market interest rates depress domestic spending. If Bank Rate falls, asset prices rise and people feel wealthier and more confident about the future, resulting in increased consumption.

Changes in aggregate demand affect domestic inflationary pressures (point 9). An increase in aggregate demand that exceeds the economy's ability to increase supply creates demand-pull inflationary pressures.

Changes in the exchange rate arising from interest rate changes also affect short-run aggregate supply. Changes in import prices lead to changes in production costs, affecting cost-push inflationary pressures.

Time lags in the transmission mechanism

The Bank of England estimates a time lag of up to two years between an initial change in Bank Rate (point 1) and the resulting change in inflation (point 11). Output is affected within one year, but the fullest effect on inflation occurs after a lag of two years. The Bank believes a 1% change in its official interest rate affects output by about 0.2-0.35% after about a year and inflation by around 0.2-0.4% per year after two years.

Why Time Lags Matter

These time lags create significant challenges for policymakers. When the MPC changes Bank Rate today, it must predict what inflation will be in two years' time, not what it is today. This forward-looking approach means monetary policy decisions are based on economic forecasts, which can be uncertain. If forecasts prove incorrect, policy may be too tight or too loose, leading to either unnecessary recession or excessive inflation.

Unconventional monetary policy

In recent years, the monetary policy approach of raising or lowering Bank Rate to manage aggregate demand has become known as 'conventional' monetary policy. In the UK, this policy worked well for most of the first decade of the twenty-first century. However, it struggled during the financial crash and credit squeeze of 2007 and the recession that began in 2008.

The zero lower bound

When Bank Rate falls to a very low level (at or close to 0%), a floor is reached. This floor is called the zero lower bound (ZLB). Once the zero lower bound is reached, it becomes impossible, in the Bank of England's view, to cut Bank Rate any further. This means that 'conventional' monetary policy of reducing interest rates to stimulate aggregate demand becomes ineffective.

The liquidity trap

Related to the zero lower bound is the liquidity trap. This describes a situation when cutting interest rates below a certain level fails to stimulate consumer spending. In a deep recession, it's likely that however low Bank Rate is set, consumers refuse to borrow and banks are too nervous to lend. Fear grips households and businesses, and spending in the economy dries up. A very low Bank Rate traps the country in a situation where further cuts have little or no effect on aggregate demand.

When Conventional Policy Fails

Both the zero lower bound and the liquidity trap represent situations where conventional monetary policy reaches its limits. At this point, simply cutting interest rates further cannot stimulate the economy. This is when central banks must turn to unconventional tools like quantitative easing to maintain their influence over aggregate demand.

Quantitative easing (QE)

The main form of 'unconventional' monetary policy is called quantitative easing (QE).

In 2009, the Bank of England's MPC began to use QE to influence commercial banks' ability to supply new loans to their customers. Quantitative easing, also known as the Asset Purchase Scheme, involves the Bank of England buying financial assets (usually government bonds or gilts) with newly created money that the Bank has electronically created.

The hope is that financial institutions (banks, pension funds, and insurance companies) which sell the bonds to the Bank of England will then lend the newly created money to businesses and individuals. These borrowers can then invest and spend more, hopefully increasing economic growth.

Many monetary economists regard QE as simply a new name for an old policy called 'expansionary open market operations', which was used as far back as the 1930s.

How quantitative easing works

To understand quantitative easing, you should be aware that monetary policy can operate in two contrasting ways: on the demand for money, or on the supply of money.

Unlike changes in Bank Rate, which primarily affect the demand for money and consequently aggregate demand, the main aim of quantitative easing is to increase the money supply directly. When QE started in the UK in 2009, the Bank of England hoped that the new money would be quickly spent by households and firms who received it, thereby reviving consumer and investment spending and stimulating economic growth.

People often think that QE increases the money supply through printing new banknotes. Indeed, when QE started in 2009, the metaphor of a central bank using a helicopter with newly printed banknotes was popular. The image suggested dropping the 'helicopter money' on the general public, who would then spend it.

However, QE is not as simple as this. As explained in the chapter on bank deposits, cash makes up only a small part of the money supply. QE increases the deposits that commercial banks hold at the Bank of England, and these deposits form part of the money supply. At the next stage, holding more deposits at the Bank of England increases the commercial banks' ability to lend to the general public.

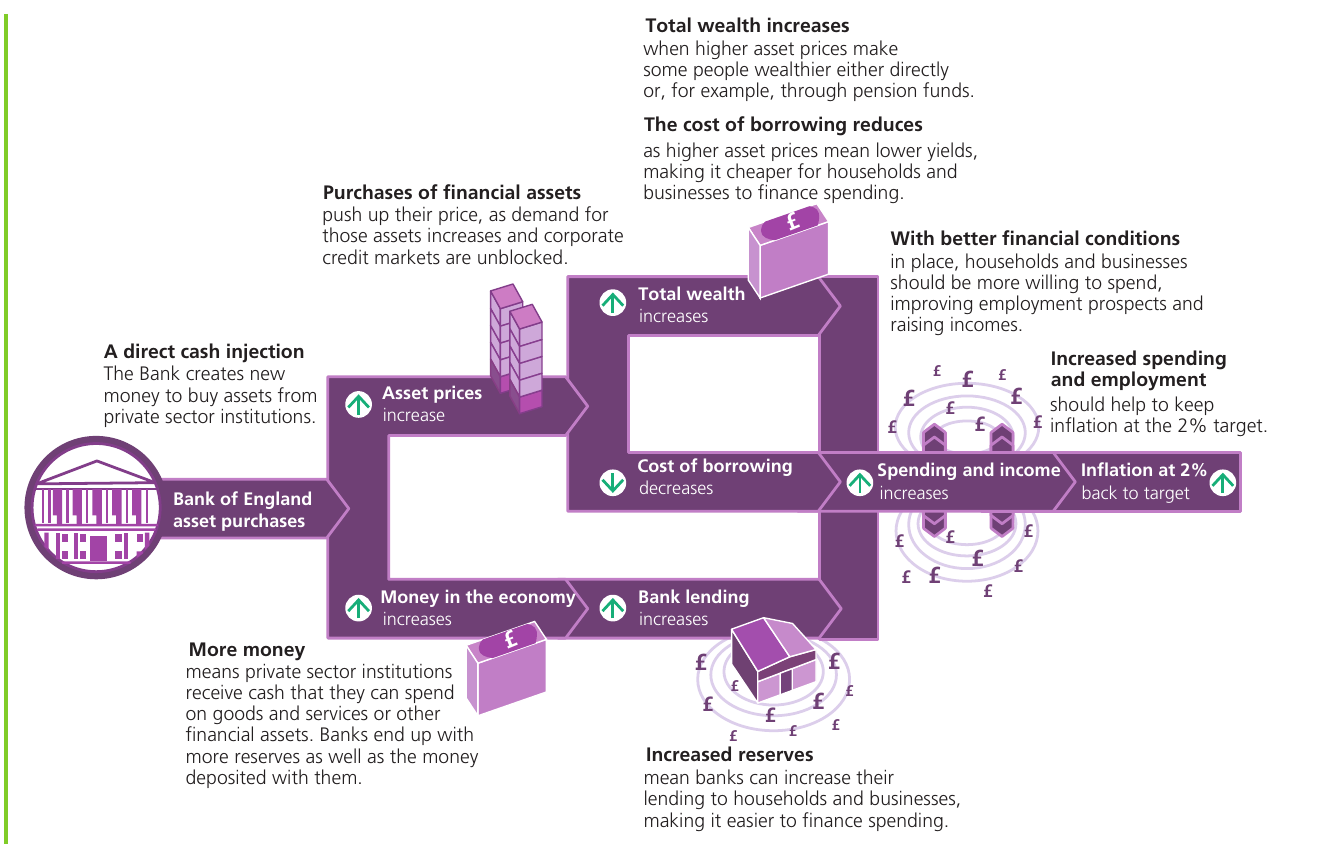

The various stages through which QE proceeds are illustrated in the transmission route diagram published by the Bank of England.

The Bank of England's Explanation of QE

Explaining the flowchart, the Bank wrote:

Direct injections of money into the economy, primarily by buying gilts, can have a number of effects. The sellers of the assets have more money so may go and spend it. That will help to boost growth. Or they may buy other assets instead, such as shares or company bonds. That will push up the prices of those assets, leaving the people who own them (either directly or through their pension funds) better off. So they may go out and spend more. And higher asset prices mean lower yields, which brings down the cost of borrowing for businesses and households. That should provide a further boost to spending.

In addition, banks will find themselves holding more reserves. That might lead them to boost their lending to consumers and businesses. So, once again, borrowing increases and so does spending. That said, if banks are concerned about their financial health, they may prefer to hold the extra reserves without expanding lending. For this reason, the Bank of England is buying most of the assets from the wider economy rather than the banks. Normally, central banks do not intervene in private sector asset markets by buying or selling private sector debt. But in exceptional circumstances, such intervention may be warranted — for example, when corporate credit markets became blocked as the financial crisis intensified towards the end of 2008.

Bank of England purchases of private sector debt can help unblock corporate credit markets by reassuring market participants that there is a ready buyer should they wish to sell. This should help bring down the cost of borrowing, making it easier and cheaper for companies to raise finance which they can then invest in their business.

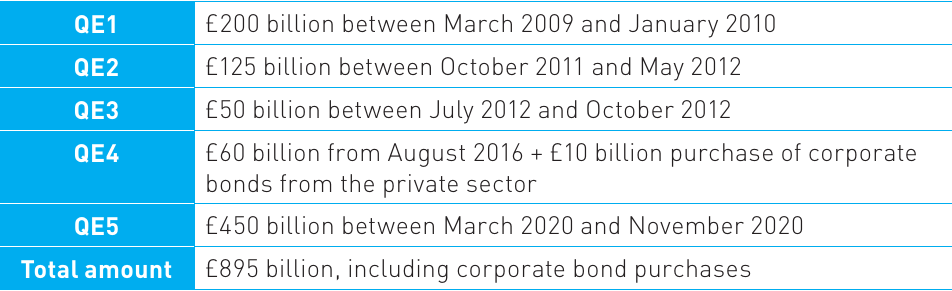

QE1, QE2, QE3, QE4 and QE5

Quantitative easing was started by the Bank of England in March 2009, though the USA had begun QE a few months earlier (and Japan had used QE earlier to stimulate its own economy between 2001 and 2006).

In the UK, there were initially three periods of quantitative easing:

- First in March 2009 (QE1)

- Then in October 2011 (QE2)

- Finally in February and July 2012 (QE3), ending in November 2012

In these first three periods, £200 billion, then £75 billion, and finally £100 billion of 'new money' was unleashed into the banking system, making a total of £375 billion.

In August 2016, the Bank of England announced it would buy an additional £60 billion of UK government bonds (plus £10 billion of private-sector corporate bonds) to address uncertainty over Brexit and worries about productivity and economic growth. Some economists called this QE4.

In March 2020, an emergency meeting on the response to the emerging Covid-19 pandemic led to the Bank announcing £200 billion of purchases of government bonds. As the pandemic continued, a further £100 billion was announced in June 2020 and then another £150 billion in November 2020. This meant that a total of £895 billion of 'new money' had been released into the UK economy.

In recent years, there has been some discussion about the Bank of England reversing or 'unwinding' quantitative easing by selling back to the public some of the government bonds it accumulated during expansionary quantitative easing. This would be a form of contractionary monetary policy, taking demand out of the economy. However, with the uncertainty brought about by the Covid-19 pandemic, the war in Ukraine, and the cost-of-living crisis of 2022, a reversal of QE has not yet taken place.

Has quantitative easing been successful?

It can be argued that QE1 worked in the sense that it prevented the 2008-09 recession from developing into a full-blown depression as a result of collapsing aggregate demand. However, it's debatable whether the later periods of quantitative easing had much effect in bringing about recovery from recession.

From 2010 onwards, the growth rate in the UK economy remained unchanged, staying very close to zero. When in 2013 a more substantial recovery did occur, further QE was not being implemented in the UK — at least until the Brexit referendum in 2016.

It was also the case that, until early 2015, the continuation of QE in the USA stimulated growth in other countries, including the UK. (It is worth noting that QE was also started by the European Central Bank in 2015 to try to offset the danger of negative growth returning to the eurozone economies.)

Several criticisms have been made of QE:

- QE, along with 0.5% Bank Rate, was partly responsible for inflation being higher than it otherwise would have been

- The increased bank lending made possible by quantitative easing went not into cheap loans to small businesses and households, but into speculative activities undertaken by the banks themselves and by large corporations

- House and land prices went up

- Asset-owning wealthy people did much better out of quantitative easing than those who were less wealthy and owned fewer assets

The Distributional Effects of QE

By reducing long-term interest rates and raising bond prices, QE also benefited the UK government. This was because QE made it much cheaper for central government to borrow to finance its large budget deficit and to pay interest on the national debt. House buyers also benefited from the cheap mortgage loans made possible by the 0.5% Bank Rate and quantitative easing.

On the other hand, savers and workers contributing to private pension schemes suffered, although recent government policy has tried to address this. This highlights the uneven distributional effects of QE across different groups in society.

The Bank of England Quarterly Bulletin published in quarter 4, 2012 estimated that the £375 billion of QE up to that point had increased the supply of broad money in the UK by about £220 billion, or 15%, which in turn increased nominal GDP by nearly 6%. If this is true, then quantitative easing was indeed a factor causing recovery from recession.

However, in an article titled 'Monetary impact of UK QE much smaller than claimed by BoE', published in January 2013, Simon Ward, chief economist at Henderson Global Investors, argued that the first £375 billion of QE had delivered a monetary boost of only £78 billion.

Forward guidance

A second 'unconventional' part of monetary policy became known as forward guidance. The policy, introduced by Mark Carney (the former governor of the Bank of England) shortly after taking up his appointment as governor, attempted to send signals to financial markets, businesses, and individuals about the Bank of England's interest rate policy in the months and years ahead.

An aim of forward guidance was to increase the credibility of monetary policy. By using forward guidance, the Bank of England aimed to calm uncertainty in otherwise uneasy financial markets. If markets fear that low interest rates will move higher, interest rates on bonds and other credit instruments and agreements will rise and begin to discourage people and companies from taking out loans or spending money. But if the Bank of England signals that it intends to keep rates low, the Bank hopes to engineer an outcome in which interest rates are indeed kept low.

By altering expectations favourably, forward guidance aims to improve the credibility of monetary policy, thereby enabling households and businesses to feel calmer about their future economic prospects. According to the Bank, forward guidance means companies and mortgage borrowers can estimate how long low interest rates will be around. If this is achieved, forward guidance converts low short-term interest rates into lower long-term interest rates.

Criticisms of forward guidance

Mark Carney received considerable criticism for his attempts to 'pre-warn' households, businesses, and markets that changes in monetary policy were likely. It was felt that these hints sent confusing signals that increased rather than decreased uncertainty.

When first announcing forward guidance in August 2013, Mark Carney said that the Bank would not consider raising Bank Rate from its low of 0.5% until the unemployment rate fell to 7% or below, which the Bank forecast would happen in 2016. The forecast was wrong and unemployment fell much faster than predicted. But the MPC did not increase Bank Rate despite the unemployment rate falling below 7% in early 2014.

The Challenge of Forward Guidance

If financial markets believed what Carney and the MPC were saying, the forward guidance strategy could have been knocked off course by events such as a house price speculative bubble hitting the UK economy (as happened), or faster than expected fall in unemployment.

Second, if markets believed that a bubble was going to occur, then whatever the Bank of England's official policy, market operators might ignore the forward guidance strategy and raise interest rates anyway. Either way, if traders in financial markets perceived the strategy to be 'wishful thinking', forward guidance could damage rather than increase the credibility of the Bank of England in its management of the UK economy.

Forward guidance also loses credibility if the Bank of England repeatedly 'moves the goal posts' — that is, changes policy every few months in response to unexpected events hitting the economy. This happened in early January 2014, when UK borrowing costs rose sharply in expectation of a rise in Bank Rate, after the fall in unemployment had proved larger than Carney had expected.

Several days later, Carney signalled the end of his forward guidance linking interest rates to the unemployment rate, adding that the UK economy was in a different place from where it had been in the previous summer. Thus, the Bank of England had overhauled its forward guidance strategy less than six months after it was first implemented.

Carney said that, instead of just considering the unemployment rate, the next phase of forward guidance would be determined by a range of 18 different indicators, including productivity and the size of the output gap. The Bank argued that a lack of inflationary pressure, spare capacity, and 'headwinds' (a slowing down of economic progress) at home and abroad meant that Bank Rate might be expected to remain at low levels for some time to come.

The current governor of the Bank of England, Andrew Bailey, was appointed to the position in 2020. He faced criticism over comments he made that some people thought were forward guidance but which were later clarified as merely 'commentary' on likely events. Bailey had led some to believe that interest rates would rise in November 2021 when he made comments about the risk of inflationary expectations and how the Bank might need to take action (that is, raise interest rates). When interest rates did not rise as some expected, he made a statement about how the difference between 'guidance' and 'commentary' was unclear. Many now understand this clarification to mean that forward guidance will no longer be used as part of the Bank's approach to monetary policy.

The relationship between changes in interest rates and the exchange rate

A fall in UK interest rates causes financial capital to flow out of the pound and into other currencies in search of better rates of return. This reduces demand for pounds and increases the supply of pounds on the foreign exchange market, which in turn causes the pound's exchange rate to fall.

Changes in export and import prices brought about by a fall in the exchange rate affect inflation in two ways:

-

Import price effects: A falling exchange rate increases the prices of imported food and consumer goods. This increases the rate of inflation in the UK. At the same time, increased prices of imported raw materials and energy create cost-push inflationary pressures in the UK (import-push inflation).

-

Export competitiveness effects: A falling exchange rate reduces UK export prices whilst raising the price of imports. This feeds into the inflationary process by increasing demand for UK exports and persuading some UK residents to buy more home-produced goods and fewer imports. This adds to demand-pull inflationary pressures. It's also likely to improve the UK's balance of payments on current account.

Calculating real interest rates

It's important to distinguish between nominal and real interest rates. The real rate of interest is calculated using this formula:

Calculating Real Interest Rates

In May 2022, Bank Rate was 1.0% and CPI inflation was 7.0%. The Bank Rate expressed in real terms was:

This means savers were losing purchasing power despite earning interest on their deposits. Even though nominal interest rates were positive at 1%, inflation eroded the real value of savings by 6% per year. This demonstrates why high inflation is problematic for savers and why the Bank of England prioritises price stability.

Remember!

Key Points to Remember:

- The Bank of England is the UK's central bank, made operationally independent in 1997 to implement monetary policy and maintain financial stability

- The Monetary Policy Committee (MPC) meets eight times per year to set Bank Rate, aiming to achieve the government's 2% CPI inflation target (with a 1% margin of flexibility)

- Bank Rate is the key monetary policy instrument that affects aggregate demand through three main channels: consumption, investment, and net exports (via the exchange rate)

- Contractionary monetary policy raises interest rates to reduce aggregate demand and control inflation, whilst expansionary monetary policy cuts rates to stimulate demand and economic growth

- The transmission mechanism shows how changes in Bank Rate work through the economy, with time lags of up to two years before the full effect on inflation is felt

- When conventional monetary policy reaches its limits (the zero lower bound), unconventional tools such as quantitative easing (QE) and forward guidance may be used. The UK implemented five rounds of QE between 2009 and 2020, totalling £895 billion

- The aggregate demand equation is:

- Real interest rate = nominal interest rate - rate of inflation