Investment Appraisal (Edexcel A-Level Business): Revision Notes

Investment Appraisal

What is investment?

Investment refers to spending money today with the expectation of generating greater returns in the future. In business, this typically means purchasing capital goods that will be used repeatedly over time to produce other goods or services. For example, a construction company investing in cement mixers, scaffolding, lorries, computers and office equipment is making capital investments.

Investment can also include expenditure on intangible projects that should yield future benefits. A business might invest \£20 million in research and development for a new product, or \£10 million on a promotional campaign. In each case, money is spent now in anticipation that it will generate larger returns later.

Understanding investment is crucial because these decisions involve substantial sums of money and carry significant risk. Making the wrong investment choice can damage a business financially, while successful investments drive growth and profitability.

Understanding investment appraisal

Investment appraisal is the process businesses use to objectively evaluate whether an investment project is likely to be profitable. It provides a systematic way to compare different investment options using quantitative techniques.

Key Elements in Investment Appraisal

All investment appraisal methods involve comparing two key elements:

Capital cost: This is the amount of money required to set up the new venture or purchase the asset. It represents the initial outlay or investment.

Net cash flow: This is calculated as cash inflows minus cash outflows. It shows the actual money generated by the investment over time.

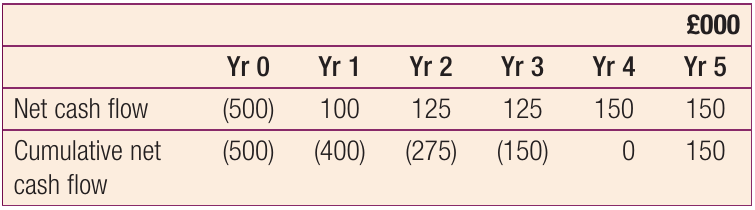

The table above shows a typical pattern of net cash flows over an investment's lifetime. Notice the large negative figure in year 0 (the initial capital cost) followed by positive cash flows in subsequent years.

Simple payback method

What is payback?

The payback period measures how long it takes for an investment project to recover its initial cost. This is one of the simplest and most widely used appraisal methods.

How to calculate payback

There are two approaches to calculating the payback period:

Method 1: Adding up net cash flows

Simply add together the annual net cash flows until they equal the initial investment. For example, if machinery costs \£500,000 and generates \£100,000 in year 1, \£125,000 in year 2, \£125,000 in year 3, and \£150,000 in year 4, the payback period is four years (\£100,000 + \£125,000 + \£125,000 + \£150,000 = \£500,000).

Method 2: Using cumulative net cash flow

Calculate the running total of cash flow including the initial investment. The cumulative net cash flow starts at the negative capital cost and gradually becomes less negative as income arrives, eventually reaching zero when the investment is paid back.

Calculating partial year payback

When payback occurs partway through a year, use this formula:

Worked Example: Calculating Partial Year Payback

If \£10,000 remains to be recovered and year 3's cash flow is \£20,000:

So the payback period is 2 years and 6 months.

Worked example: comparing payback periods

When choosing between projects using payback, select the one with the shortest payback time.

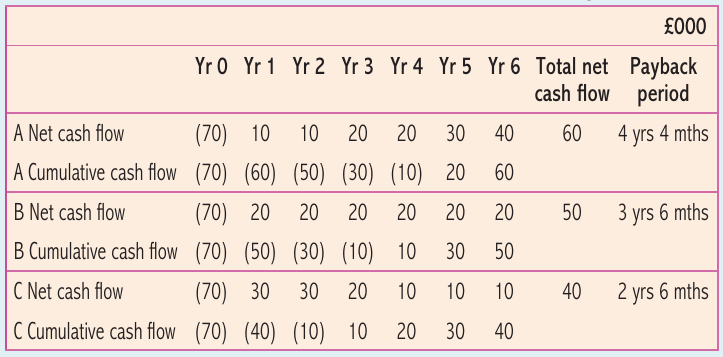

Worked Example: Comparing Three Investment Options

The table shows three investment options, each costing \£70,000.

Analysis:

- Project C has the shortest payback period at 2 years 6 months, making it the preferred choice using this method

- Notice that Project C actually generates the lowest total cash flow (\£40,000) over six years, but this isn't considered in simple payback calculations

Advantages of the payback method

Speed and simplicity: Payback is straightforward to calculate and easy for non-financial managers to understand. This makes it practical for quick decision-making.

Useful when technology changes rapidly: In industries like agriculture or IT where equipment quickly becomes obsolete, recovering costs quickly is essential. A shorter payback period reduces the risk of technology making your investment worthless.

Helpful for businesses with cash flow problems: Companies facing liquidity issues need to recover their investment quickly to maintain financial stability. Payback helps identify projects that will return cash fastest.

Average Rate of Return (ARR)

What is ARR?

The Average Rate of Return (also called Accounting Rate of Return) measures the net return each year as a percentage of the capital invested. Unlike payback, ARR directly measures profitability.

ARR formula

How to calculate ARR step-by-step

Step 1: Calculate total net profit

Step 2: Calculate annual net profit

Step 3: Calculate ARR percentage

Worked example: ARR calculation

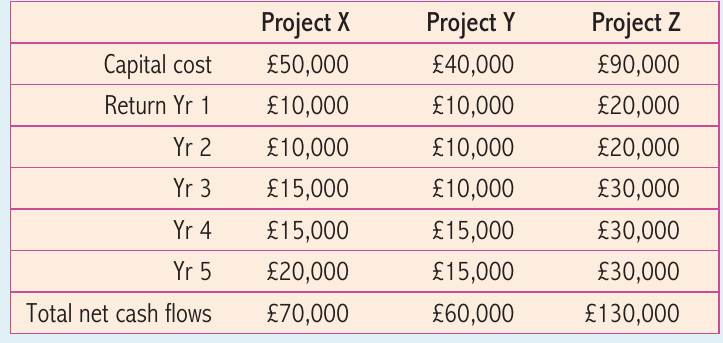

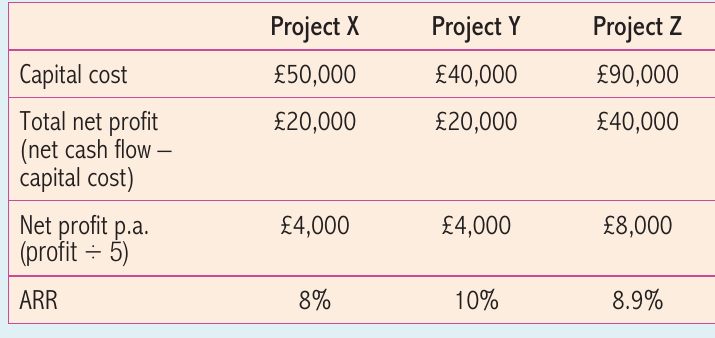

Worked Example: Calculating and Comparing ARR for Three Projects

Looking at the three projects in the table:

Project X:

- Total net profit = \£70,000 - \£50,000 = \£20,000

- Annual profit = \£20,000 ÷ 5 = \£4,000

- ARR = (\£4,000 / \£50,000) × 100 = 8%

Project Y:

- Total net profit = \£60,000 - \£40,000 = \£20,000

- Annual profit = \£20,000 ÷ 5 = \£4,000

- ARR = (\£4,000 / \£40,000) × 100 = 10%

Project Z:

- Total net profit = \£130,000 - \£90,000 = \£40,000

- Annual profit = \£40,000 ÷ 5 = \£8,000

- ARR = (\£8,000 / \£90,000) × 100 = 8.9%

Decision: Project Y would be selected because it has the highest ARR at 10%, even though Project Z generates more total profit. This is because Project Y requires less initial capital investment.

Advantages of the ARR method

Shows profitability clearly: ARR directly measures how profitable an investment is as a percentage, making it easy to compare different projects and assess which offers better returns.

Enables comparison with alternative investments: The percentage return can be compared with other uses for funds, such as bank interest rates. If a bank offers 12% interest, a company might postpone a project with 10% ARR until rates fall.

Helps identify opportunity cost: By showing the rate of return, businesses can better assess what they're giving up by choosing one investment over another.

Discounted Cash Flow and Net Present Value (NPV)

Understanding the time value of money

Money available today is worth more than the same amount in the future. This fundamental principle drives discounted cash flow analysis.

Consider this example: \£100 invested today at 10% compound interest would grow over five years as follows:

After five years, the \£100 becomes \£161. Working backwards, this means \£161 received in five years' time is worth only \£100 today. This is the concept of present value.

Critical Note on Discounting

Discounted cash flow accounts for the effect of interest rates on investment decisions. It does NOT account for inflation, which is a separate effect on money's value.

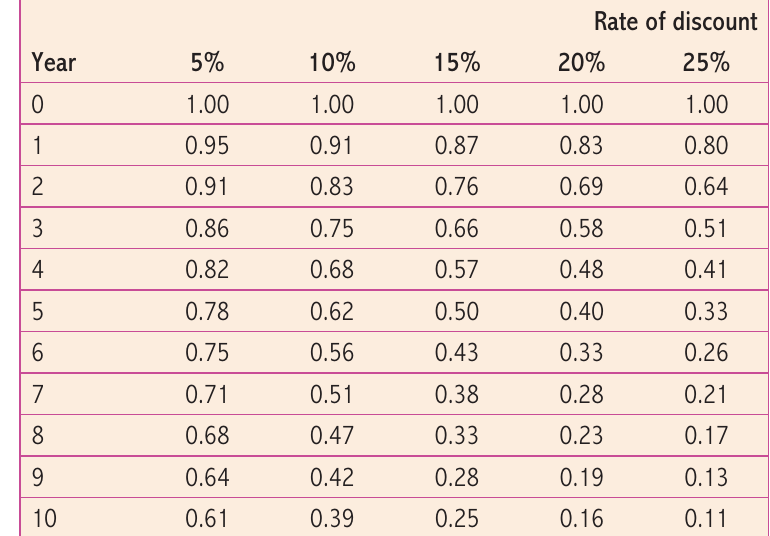

What are discount tables?

Discount tables show by how much a future value must be multiplied to calculate its present value at different interest rates.

To use a discount table:

- Find the relevant year (row)

- Find the discount rate (column)

- Multiply the future cash flow by the discount factor

Worked Example: Using Discount Tables

\£10,000 received in three years at 10% discount rate:

Key features of discounting

Two Critical Patterns in Discounting

The discount table reveals two important patterns:

Higher discount rates reduce present value more: At 5% discount, \£1,000 in five years is worth \£780 today. At 25% discount, it's worth only \£330. Higher interest rates mean future money is worth less in present terms.

More distant cash flows have lower present value: \£1,000 received in one year at 20% discount is worth \£830 today. The same \£1,000 received in ten years is worth only \£160 today. Time significantly erodes the value of future money.

Calculating Net Present Value (NPV)

NPV is the present value of all future cash flows from an investment minus the initial cost. A positive NPV indicates a profitable project.

NPV formula:

Worked example: NPV calculation and comparison

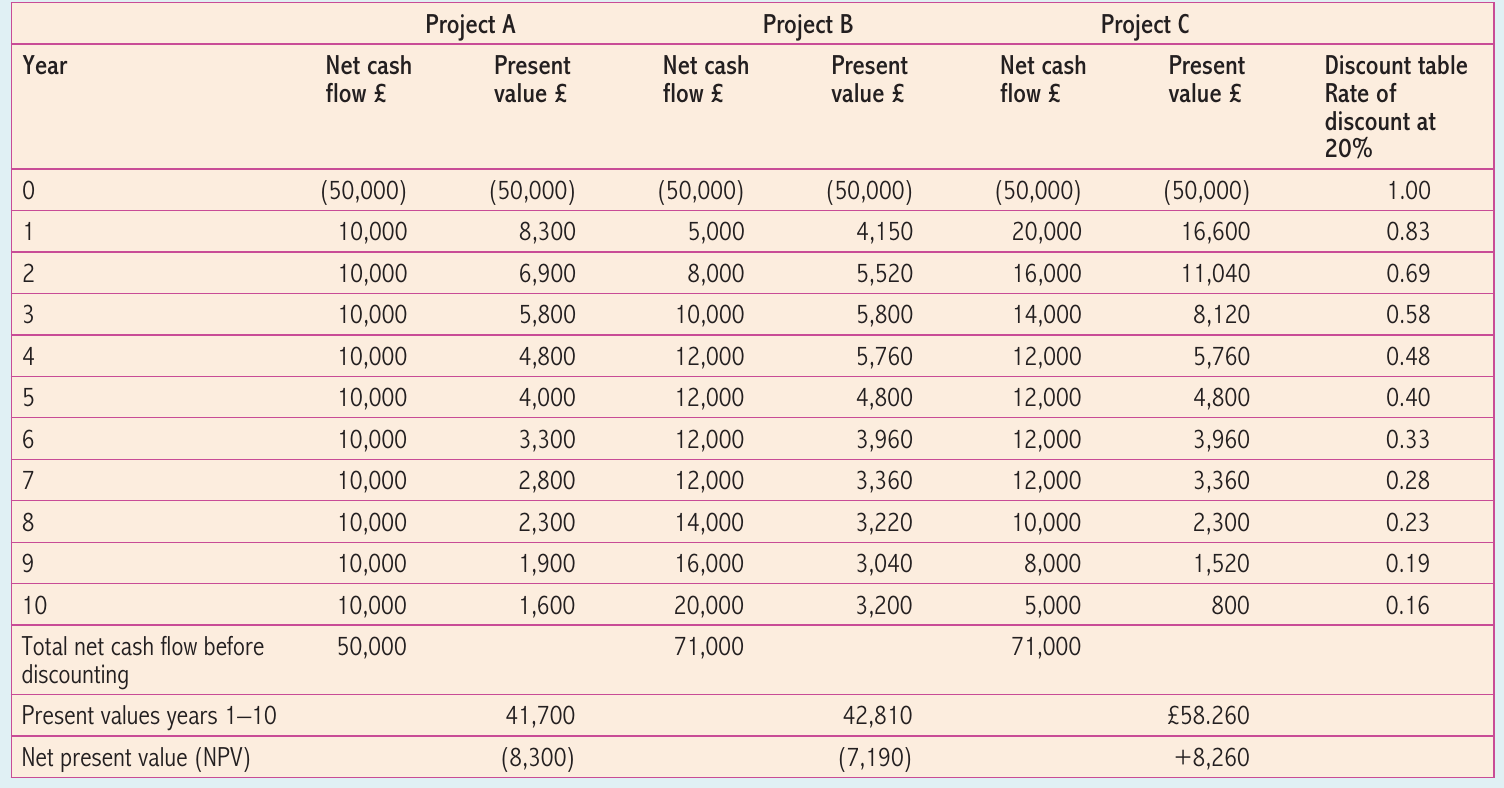

Worked Example: NPV Calculation and Comparison

This table compares three projects, all costing \£50,000, discounted at 20%:

Project A:

- Generates steady \£10,000 annually

- Total undiscounted cash flow: \£50,000

- Total present values (years 1-10): \£41,700

- NPV = \£41,700 - \£50,000 = :-£8,300 (unprofitable)

By year 10, the \£10,000 cash flow has a present value of only \£1,600 due to discounting.

Project B:

- Generates increasing cash flows (\£5,000 rising to \£20,000)

- Total undiscounted cash flow: \£71,000

- Total present values: \£42,810

- NPV = \£42,810 - \£50,000 = :-£7,190 (unprofitable)

Despite higher total cash flow, Project B remains unprofitable because larger returns come later when they have less present value.

Project C:

- Generates decreasing cash flows (\£20,000 falling to \£5,000)

- Total undiscounted cash flow: \£71,000

- Total present values: \£58,260

- NPV = \£58,260 - \£50,000 = +\£8,260 (profitable)

Key Insight: Project C is profitable because higher cash flows arrive earlier, maximizing present value. This shows why timing of returns matters significantly in investment decisions.

Decision rule: Accept any project with positive NPV. When comparing projects, choose the one with the highest NPV. In this case, only Project C should proceed.

Advantages of the discounted cash flow method

Accounts for time value of money: Unlike payback and ARR, DCF correctly recognizes that money received sooner is worth more than money received later. This provides a more accurate assessment of investment value.

Flexible to changing conditions: The discount rate can be adjusted as economic conditions change. During the 1990s, business borrowing costs fell from over 15% to 7-8%, allowing lower discount rates. Since 2008, rates have been even lower. This flexibility means the method remains relevant across different economic environments.

Risk adjustment: Higher discount rates can be used for riskier projects, building risk assessment directly into the appraisal calculation.

Limitations of investment appraisal techniques

While these quantitative methods are valuable, each has significant weaknesses that businesses must recognize:

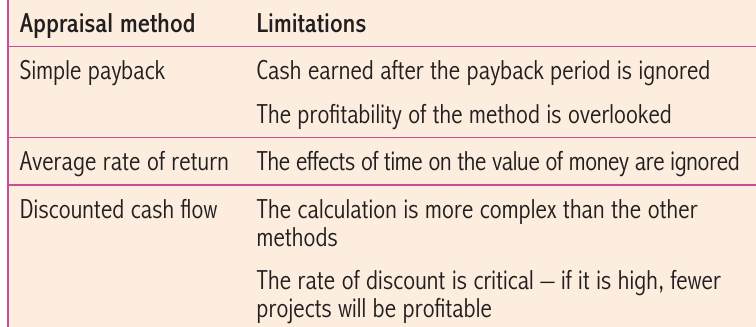

Payback limitations

Ignores cash after payback: Any cash flow generated after the payback period is completely ignored. A project might generate enormous profits in later years, but payback wouldn't consider this.

Overlooks profitability: Payback only measures speed of cost recovery, not total profitability. A project with quick payback might actually generate less profit overall than a slower-payback alternative.

ARR limitations

Ignores time value of money: ARR treats \£1,000 earned in year 1 the same as \£1,000 earned in year 10. This fundamental weakness means ARR can mislead decision-makers about true investment value.

Doesn't show timing of returns: Two projects with identical ARR could have vastly different cash flow patterns, making them incomparable in practical terms.

DCF/NPV limitations

Calculation complexity: NPV calculations are more complex than other methods, requiring discount tables and careful computation. This can make the method less accessible to non-financial managers.

Discount rate sensitivity: Small changes in the discount rate can dramatically affect results. If the rate is too high, fewer projects appear profitable. Choosing the appropriate rate is critical but often subjective.

Relies on accurate forecasts: Like all methods, NPV depends on reliable predictions of future cash flows. In uncertain markets or with new technologies, these forecasts may be highly unreliable.

Qualitative factors in investment decisions

Investment decisions shouldn't rely solely on financial calculations. Several non-financial factors significantly influence whether investments succeed:

Human relations impact

Some investments dramatically affect employees. Plant automation might eliminate jobs and create mass redundancies. Even if financially attractive, businesses may postpone such investments if they believe the damage to staff morale and industrial relations would be too severe. Maintaining positive workplace relationships often outweighs short-term financial gains.

Ethical considerations

Modern businesses increasingly consider ethical implications of investment decisions. A chemicals manufacturer might choose a plant location that doesn't minimize financial costs but does reduce environmental damage. This decision reflects corporate values and can enhance the company's reputation as a responsible "corporate citizen". Ethical investments may not optimize short-term profits but protect long-term brand value and stakeholder relationships.

Risk assessment

Multiple factors affect investment risk beyond what financial calculations show:

Key Risk Factors to Consider

-

Financial position: Companies with weak cash reserves face higher risk from any investment failure.

-

Economic conditions: The state of the economy and specific markets affects how likely projected returns are to materialize.

-

Payback period: Projects with longer payback periods are inherently riskier because more can go wrong over extended timeframes. Technology might change, markets might shift, or competitors might respond.

Availability of funds

Many financially viable projects never proceed because businesses cannot raise necessary capital. This particularly affects small businesses that struggle to convince investors and lenders to provide finance. Banks may reject loan applications even for projects with strong financial projections if they consider the risk too high.

Business confidence

Entrepreneurs and managers have different personalities and attitudes that profoundly influence investment decisions. Some decision-makers are cautious and risk-averse, seeing potential problems and obstacles. Others are optimistic and confident, viewing the future positively.

This psychological difference has crucial practical impact. Cautious managers may delay or abandon investment projects that confident managers would authorize immediately, even when analyzing identical financial information. The deeply held attitudes of decision-makers thus become an important qualitative factor in investment appraisal.

Exam technique tips

Tips for Exam Success

For 'calculate' questions: Show your working clearly. Even if your final answer is wrong, you can gain marks for correct method. Always include units (\£, %, years) in your answer.

For 'explain' questions about method choice: Consider the business context. Technology companies might prefer payback due to rapid obsolescence. Established manufacturers might use NPV for more accurate profitability assessment.

For 'analyse' questions: Consider both advantages and limitations of the method used. Explain how the method's characteristics suit (or don't suit) the specific business situation.

For 'evaluate' questions: Balance quantitative analysis with qualitative factors. The "best" financial option might not be best overall when considering ethics, human relations, or risk.

Remember!

Key Points to Remember

-

Investment appraisal uses three main quantitative methods: payback (speed of cost recovery), ARR (profitability as percentage), and NPV (present value of returns)

-

Key formulas to memorize:

- ARR (%) = (Net profit per annum / Capital cost) × 100

- NPV = Present values - Initial cost

-

Each method has strengths and weaknesses: Payback is simple but ignores profitability; ARR shows returns but ignores time value; NPV is accurate but complex

-

Discounted cash flow accounts for interest rates, NOT inflation: This is a common exam mistake

-

Qualitative factors matter: Human relations, ethics, risk, funding availability and business confidence all influence real investment decisions beyond financial calculations

-

In the exam, context is crucial: The "right" appraisal method depends on the business situation, industry characteristics, and strategic priorities