The Foreign Exchange Market and Exchange Rates (Edexcel A-Level Economics A): Revision Notes

The Foreign Exchange Market and Exchange Rates

Introduction to the foreign exchange market

The foreign exchange market operates like any other market, with forces of demand and supply determining prices. In this case, the 'price' is the exchange rate between currencies.

When international trade occurs, foreign exchange transactions become necessary. For example, if you as a UK resident want to buy goods from abroad, you need to purchase foreign currency (like euros) and supply pounds to do so. Similarly, when a French tourist visits the UK and buys British goods or services, the transaction needs to be conducted in pounds, creating demand for pounds.

How the market works

The market reaches equilibrium where demand for a currency matches its supply. This equilibrium position has a direct connection with the balance of payments. When demand for pounds exactly matches the supply of pounds, this indicates a balance between:

- Europeans' demand for UK goods, services and assets

- UK residents' demand for European goods, services and assets

In other words, the overall balance of payments is in balance.

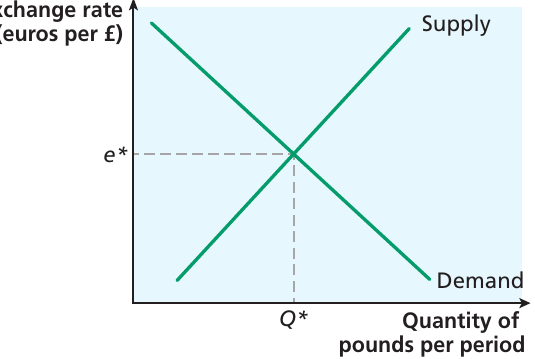

The diagram above illustrates the foreign exchange market for pounds and euros. The demand curve slopes downward because when the €/£ exchange rate is low, UK goods, services and assets become relatively cheap in euro terms, so demand is high. Conversely, when the €/£ rate is high, Europeans receive fewer pounds for their euros, making UK products more expensive and reducing demand.

The supply curve slopes upward. When the €/£ rate is relatively high, UK residents receive plenty of euros for their pounds, encouraging them to buy European goods, services and assets. They supply pounds to obtain the foreign exchange needed for these transactions. When the €/£ rate is low, European products become relatively expensive for UK residents, so fewer pounds are supplied.

The market reaches equilibrium at e*, where demand equals supply at quantity Q*. At this point, the currency market is in balance and no intervention is needed to maintain the exchange rate.

Fixed exchange rate systems

What is a fixed exchange rate?

A fixed exchange rate is a system where the government of a country agrees to fix the value of its currency in terms of another country's currency. Under this arrangement, the authorities intervene in the foreign exchange market to maintain the currency at the agreed level.

The Dollar Standard (Bretton Woods system)

Following the Second World War, the Bretton Woods conference established a system of fixed exchange rates known as the Dollar Standard. Under this system, countries agreed to maintain the value of their currencies in terms of US dollars. The system remained in place until the early 1970s.

Historical Example: Sterling Under the Dollar Standard

From 1950 until 1967, the sterling exchange rate was set at $2.80. The UK government committed to maintaining this rate through market intervention. Occasional changes were permitted after consultation if a currency was seen to be substantially out of line, as happened when the UK devalued sterling from $2.80 to $2.40 in 1967.

Maintaining a fixed exchange rate

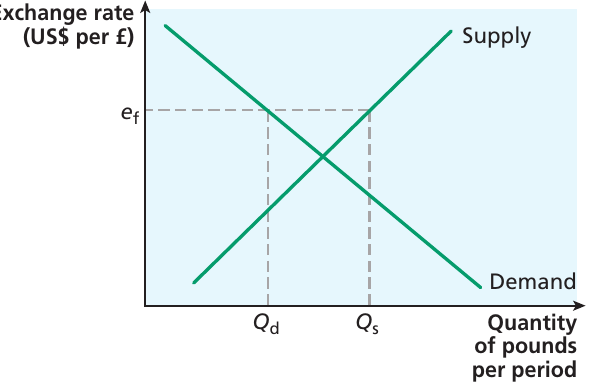

When authorities set an exchange rate at a particular level (ef), this level may not correspond to the natural market equilibrium. The diagram above shows a situation where, at the official rate ef, the supply of pounds exceeds demand.

This excess supply indicates that UK residents are trying to buy more American goods, services and assets than Americans are buying from Britain. In other words, there is an overall deficit on the balance of payments.

To maintain the fixed rate, the UK authorities must take action. Since UK residents have purchased excess goods, services and assets, the authorities need to sell foreign exchange reserves to balance the books. These reserves are stocks of foreign currency and gold owned by the central bank, held specifically to manage any mismatch between currency demand and supply.

Such transactions are recorded as 'official financing' in the financial account of the balance of payments.

Foreign exchange reserves

Foreign exchange reserves are crucial for operating a fixed exchange rate system. These are stocks of foreign currency and gold held by the central bank to enable it to meet any mismatch between the demand and supply of the country's currency.

When there is excess demand for pounds, the authorities can accumulate foreign exchange reserves. When there is excess supply of pounds (a balance of payments deficit), reserves must be sold to maintain the exchange rate.

Effects of changes in demand

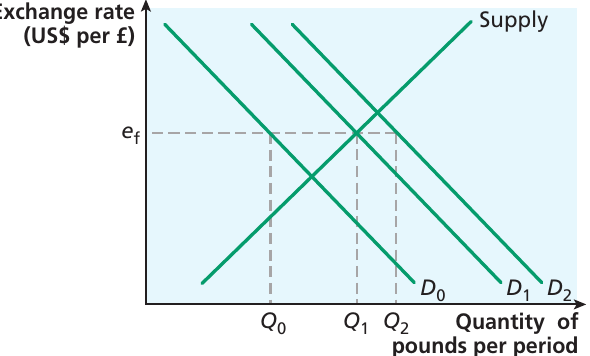

Suppose the supply curve remains fixed but demand shifts over time. Let ef be the officially chosen exchange rate. If demand is at D1, the exchange rate corresponds to market equilibrium and no intervention is needed.

However, if demand falls to D0 (perhaps because Americans develop a preference for Scotch whisky), there is excess demand for pounds. The UK monetary authorities need to buy up the excess supply by selling foreign exchange reserves.

Conversely, if demand for pounds is strong at D2, there is excess demand. The UK monetary authorities can supply additional pounds in return for US dollars, allowing foreign exchange reserves to accumulate.

Long-term sustainability

The system operates successfully only if the chosen exchange rate is close to the average equilibrium value over time. This ensures the central bank neither runs down its foreign exchange reserves nor accumulates them indefinitely.

Countries that try to hold their currency away from equilibrium indefinitely will find this problematic. In the early twenty-first century, China and some other Asian economies pegged their currencies against the US dollar at such low levels that they accumulated foreign exchange, particularly US government securities. The low exchange rate kept their exports highly competitive in world markets. However, this strategy relies on being able to continue expanding domestic production to meet high international demand, otherwise inflationary pressure will build.

Devaluation and revaluation

Under a fixed exchange rate system, persistent disequilibrium may need to be addressed by realigning the currency value. This involves either:

-

Devaluation: A process where a government reduces the price of its currency relative to an agreed rate in terms of foreign currency. This is used to tackle persistent current account deficits.

-

Revaluation: A process where a government raises the price of domestic currency in terms of foreign currency. This deals with persistent surpluses.

The Dollar Standard period in the UK

During the Dollar Standard period, the UK economy experienced what became known as a 'stop-go' cycle of growth. When the government tried to stimulate economic growth, the effect was to increase imports due to the high marginal propensity to import. This generated a deficit on the current account, which then needed to be financed by selling foreign exchange reserves.

This process had two negative effects:

- Selling foreign exchange reserves increased domestic money supply, putting upward pressure on prices and threatening inflation

- The Bank of England had finite foreign exchange reserves and could not allow them to be run down indefinitely

These constraints meant the government had to slow economic growth again, creating the 'stop-go' cycle. The UK eventually withdrew from the Dollar Standard in June 1972.

The USA's need to finance the Vietnam War meant the supply of dollar currency began to expand, accelerating inflation in countries fixing their currency to the dollar. This made it increasingly difficult to sustain exchange rates at fixed levels.

Effects of devaluation

During the stop-go period, there were extensive debates about whether devaluation should be implemented. Devaluation improves competitiveness by making exports cheaper and imports more expensive. At a lower currency value, you would expect increased demand for exports and reduced demand for imports. Does this offer a solution to a current account deficit?

The J-curve effect

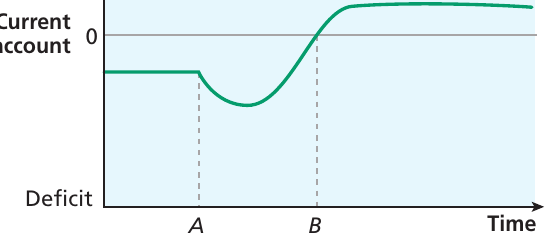

Unfortunately, devaluation does not necessarily lead to immediate improvement in the current account. The J-curve effect describes why this happens.

Time is measured on the horizontal axis, with the current account initially in deficit. A devaluation at time A initially pushes the current account further into deficit because of the inelasticity of domestic supply. Only after time B, when domestic firms have had time to expand their output to meet the demand for exports, does the current account move into surplus.

There are several reasons for this delayed response:

Supply-side factors: If domestic producers lack spare capacity or there are time lags before production for export can be increased, exports will be price inelastic in supply and will not expand quickly. The impact on exports will therefore be limited in the short run.

Import substitution: Similar arguments apply to producers of goods that are potential substitutes for imported products. This reinforces the sluggishness of adjustment, meaning the current account may initially worsen rather than improve despite the change in competitiveness.

Demand-side factors: The elasticity of demand for exports and imports also matters. If competitiveness improves but demand does not respond strongly, there may be a negative impact on the current account. When demand for exports is price inelastic, a fall in price leads to a fall in revenue.

Short-run behaviour: There is reason to expect demand for exports to be relatively inelastic in the short run. Exports may be supplied under contracts that cannot be immediately renegotiated. Furthermore, people and firms may wait to see whether the devaluation is permanent or temporary before revising their spending plans.

The Marshall-Lerner condition

The Marshall-Lerner condition states that devaluation will have a positive effect on the current account only if the sum of the elasticities of demand for exports and imports is negative and numerically greater than 1.

If there is a devaluation, there will be both a quantity effect and a price effect. At the new exchange rate:

- The quantity effect on the trade balance is positive because exports tend to increase and imports to decrease

- However, there is also a negative price effect, because export prices in terms of foreign currency have fallen and import prices in domestic currency have risen

The trade balance (measured in revenue terms) will improve only if the quantity effect fully offsets the price effect. This occurs only when the Marshall-Lerner condition holds true.

Competitive devaluation

Under a fixed exchange rate regime, there may be temptation for countries to improve their international position by engineering a competitive devaluation. This is a situation where one country attempts to gain an advantage by devaluing its currency, inducing a response from other countries.

The danger is that other countries would respond by introducing similar policies, negating the original effects. The eventual outcome would be to reduce world trade overall.

Fixed exchange rates and monetary policy

An important point emerges from this discussion: under a fixed exchange rate regime, intervention to maintain the exchange rate affects domestic money supply. This means the monetary authorities cannot pursue an independent monetary policy.

Money supply and the exchange rate cannot be controlled independently of one another. The money supply must be targeted to maintain the value of the currency. Governments may be tempted to use tariffs or non-tariff barriers to reduce a current account deficit, but this has been shown to be distortionary.

Floating exchange rate systems

What is a floating exchange rate?

A floating exchange rate is a system in which the exchange rate is permitted to find its own level in the market without government intervention. This means the overall balance of payments is automatically assured, and monetary authorities do not need to intervene to ensure this happens.

In practice, however, governments have tended to be wary of leaving the exchange rate entirely to market forces. There have been occasional periods when intervention has been used to affect the market rate.

The Exchange Rate Mechanism (ERM)

An example of a semi-fixed system was the Exchange Rate Mechanism (ERM), which was set up by a group of European countries in 1979 with the objective of keeping member countries' currencies relatively stable against each other. This was part of the European Monetary System (EMS).

Each member nation agreed to keep its currency within 2.25% of a weighted average of the members' currencies, known as the European Currency Unit (ECU). This was an adjustable peg system, with eleven realignments permitted between 1979 and 1987.

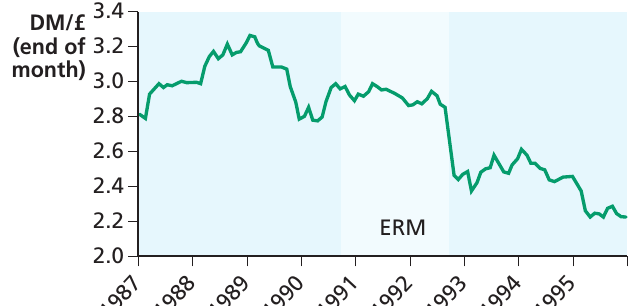

Case Study: The UK and the ERM

The UK opted not to join the ERM initially but started shadowing the Deutschmark in the mid-1980s, aiming to keep the rate at around DM3 to the pound. The UK became a full member in October 1990.

However, the rate at which sterling had been set against the Deutschmark was relatively high. The situation worsened due to German reunification, which led to substantial capital flows into Germany, reinforcing the overvaluation of sterling. Speculative attacks began, the Bank of England's foreign exchange reserves were depleted defending the pound, and interest rates were raised. In 1992, the pound left the ERM.

The graph shows the nominal DM/£ exchange rate from 1987-95. You can see the value of the pound fell rapidly after exiting the ERM.

Factors influencing floating exchange rates

When the foreign exchange market is left free to find its own equilibrium, it becomes important to consider what factors influence the level of the exchange rate. Will the exchange rate resulting from market equilibrium be consistent with the government's domestic policy objectives?

Key Factors Affecting Floating Exchange Rates:

- Relative interest rates and monetary policy

- Relative inflation rates

- Net investment in the UK

- Speculation

Interest rates and monetary policy

Financial flows into or out of the UK may be induced by the relative level of interest rates. If UK interest rates are high relative to elsewhere, this may attract an inflow of financial capital, putting upward pressure on the exchange rate and leading to appreciation.

Similarly, under quantitative easing, an increase in money supply could cause a depreciation through its effect on interest rates and outflows of hot money.

Hot money refers to stocks of funds that are moved around the world from country to country in search of the best return. The size of these stocks is enormous and can significantly affect exchange rates in the short run.

The returns to be gained from such capital flows depend on the relative interest rate in the country targeted and on the expected exchange rate in the future, which may in turn depend on expectations about inflation.

The significance of this is that changes in the stance of monetary policy will have an effect on the exchange rate under a floating system. These become an important part of the transmission mechanism of monetary policy.

Relative inflation rates

Exchange rate equilibrium also implies a zero overall balance of payments. If the exchange rate always adjusts to the level that ensures this, it might be argued that the long-run state of the economy is one in which the competitiveness of domestic firms remains constant over time.

You would expect the exchange rate to adjust through time to offset any differences in inflation rates between countries. The purchasing power parity theory of exchange rates argues that in the long run, the nominal exchange rate would adjust in such a way as to offset changes in relative inflation rates between countries. This implies the balance of payments will always return to equilibrium through the adjustment of the exchange rate.

The trade balance

The exchange rate in a free market is determined by demand and supply for the currency. Thus, changes in the balance between exports and imports can affect the exchange rate. An increase in the demand for exports implies an increase in the demand for sterling, which would lead to an appreciation of the currency (ceteris paribus).

Net investment in the UK

An increase in foreign direct investment would have similar effects. If the UK becomes an attractive prospect for foreign investors, this could lead to appreciation, or at least upward pressure on the exchange rate.

Speculation

In the short run, the exchange rate may diverge from its long-run equilibrium. An important influence on the exchange rate in the short run is speculation.

The discussion of the exchange rate has so far focused only on the current account of the balance of payments. However, the financial account is also significant, especially since regulation of the movement of financial capital was liberalised.

Some capital movements are associated with foreign direct investment. However, sometimes there are also substantial movements of hot money. These stocks of funds move around the globe from country to country in search of the best return.

The size of stocks of hot money is enormous and can significantly affect exchange rates in the short run. Returns depend on the relative interest rate in the country targeted and on the expected exchange rate in the future, which may depend on expectations about inflation.

Example: Hot Money Flows and Exchange Rates

Suppose you are an investor holding assets denominated in US dollars, and the UK interest rate is 2% higher than in the USA. You may be tempted to shift the funds into the UK to take advantage of the higher interest rate.

However, if you believe the exchange rate is above its long-run equilibrium and therefore likely to fall, this will affect your expected return on holding a UK asset.

Indeed, if investors holding UK assets expect the exchange rate to fall, they are likely to shift their funds out of the country as soon as possible, which may then push down the exchange rate. This may be a self-fulfilling prophecy.

However, speculators may react to news in an unpredictable way, so not all speculative capital movements act to influence the exchange rate towards its long-run equilibrium value.

The Asian Financial Crisis of 1997

Speculation was a key contributing factor in the Asian financial crisis of 1997. Substantial flows of capital had moved into Thailand in search of high returns. Speculators came to believe the Thai currency (the baht) was overvalued.

Outward capital flows put pressure on the exchange rate. Although the Thai central bank tried to resist, it eventually ran down its reserves to the point where it had to devalue. This then sparked off capital flows from other countries in the region, including South Korea.

A managed (dirty) float

Under a floating exchange rate system, the authorities do not intervene in the exchange market. However, exchange rates are notoriously volatile and there may be occasions when the authorities wish to intervene to try to stabilise the currency. When this happens, it represents a move away from a pure float to a managed floating exchange rate (sometimes known as a 'dirty' float).

For example, during the UK's period of membership of the ERM, the pound could float between upper and lower bands.

One way the authorities could influence the exchange rate under this system would be by using the interest rate to influence international financial flows. This is difficult to implement under inflation targeting, where the prime use of the interest rate is to ensure inflation remains within its target range.

A second way would be to buy or sell sterling to influence its price (the exchange rate). However, the official financing item in the balance of payments accounts in the UK has been relatively minor, indicating there has been little attempt to manage the exchange rate.

One rationale for attempting to manage the exchange rate would be to improve a country's competitiveness through depreciation. This strategy would clearly have an impact on other countries and could induce a response, becoming a form of competitive depreciation. This is likely to be counter-productive in the long run.

Comparing fixed and floating systems

In evaluating whether a fixed or floating regime is preferable, there are many factors to consider. Three key considerations are:

- The extent to which the respective systems can accommodate and adjust to external shocks

- The stability of each system

- Which system best encourages governments to adopt sound macroeconomic policies

Adjustment to shocks

Every economy must cope with external shocks that occur for reasons outside the control of the country. A key question in evaluating exchange rate systems is whether there is an effective mechanism that allows the economy to return to equilibrium after an external shock.

Under a floating exchange rate system: Much of the burden of adjustment is taken up by changes in the exchange rate. For example, if an economy finds itself experiencing faster inflation than other countries (perhaps because those countries have introduced policies to reduce inflation), then the exchange rate will adjust automatically to restore competitiveness.

Under a fixed exchange rate system: The authorities are committed to maintaining the exchange rate, and this takes precedence. The only way to restore competitiveness is by deflating the economy to bring inflation into line with other countries. This is likely to bring a transitional cost in terms of higher unemployment and slower economic growth. The burden of adjustment is on the real economy, rather than on allowing the exchange rate to adjust.

The Bretton Woods system operated for more than 20 years during a period when many economies enjoyed steady economic growth. However, in the UK the system brought about a stop-go cycle, where the need to maintain the exchange rate hampered economic growth because of the tendency for growth to lead to increased imports and thus a current account deficit. The increasing differences in inflation rates in different countries led to the final collapse of the system, suggesting it was unable to cope with such variation.

Furthermore, a flexible exchange rate system allows authorities to utilise monetary policy to stabilise the economy. Remember that under a fixed exchange rate system, monetary policy must be devoted to the exchange rate target.

Stability

When it comes to stability, a fixed exchange rate system has much to recommend it. If firms know the government is committed to maintaining the exchange rate at a given level, they can agree future contracts with confidence.

Under a floating exchange rate system, trading takes place in an environment where the future exchange rate has to be predicted. If the exchange rate moves adversely, firms may face potential losses from trading. This foreign exchange risk is reduced under a fixed rate regime.

In a climate where speculative activity creates volatility in exchange rates, international trade may be discouraged because of the exchange rate risk. The effects of such volatility can be mitigated to some extent by the existence of futures markets, where it is possible to buy foreign exchange at a fixed price for delivery at a specified future date.

Example: Using Futures Markets to Hedge Risk

Suppose a firm is negotiating a deal to buy component parts for a manufacturing process that will be delivered in 3 months' time. The firm can buy the foreign exchange needed to close the deal in the futures market. It then knows the contract will be viable, having negotiated a price for components based on the known exchange rate, rather than on the unpredictable rate that will apply at that future date.

The firm may have to buy the foreign currency at a price below the current (spot) exchange rate, but as the future rate has been built into the terms of the contract, this will not affect the viability of the deal. The process by which a firm avoids losses by buying forward is known as hedging.

However, even with hedging to reduce the risk, it is costly to engage in international trade when exchange rates are potentially volatile, so world trade is unlikely to be encouraged under such a system. Of course, the risk to firms is still present under a fixed exchange rate system, in the sense that a government may choose to realign its currency, with even greater costs to firms tied into contracts. However, such realignments were rare under Bretton Woods and are more predictable than the volatility that can occur on a day-to-day basis in the foreign exchange market.

The exchange rate and foreign direct investment

Flows of foreign direct investment may be influenced by the exchange rate and by expectations about future movements of the exchange rate. This will be one of the key factors that a firm considers when deciding where to locate its investment.

Macroeconomic policy

Critics of the flexible exchange rate system argue it is too flexible for its own good. If governments know the exchange rate will always adjust to maintain international competitiveness, they may have no incentive to behave responsibly in designing macroeconomic policy.

They may be tempted to adopt an inflationary domestic policy, secure in the knowledge that the exchange rate will bear the burden of adjustment. In other words, a flexible exchange rate system does not impose financial discipline on individual countries.

An example of this was seen in the UK in the early 1970s when the country first moved to a floating exchange rate regime. Money supply was allowed to expand rapidly, and inflation increased to almost 25%, aided by the oil price shock.

Reducing inflation under flexible exchange rates is costly. If interest rates are increased to reduce domestic aggregate demand and thus reduce inflationary pressure, the high return on domestic assets encourages an inflow of hot money, putting upward pressure on the exchange rate. This reduces the international competitiveness of domestic goods and services, and deepens the recession.

There may also be spillover effects on other countries. Suppose two countries have been experiencing rapid inflation, and one decides to tackle the problem. It raises interest rates to dampen domestic aggregate demand, which leads to appreciation of its currency. For the other country, the effect is a depreciation of the currency. (If one currency appreciates, the other must depreciate.)

The other country finds its competitive position has improved, and it faces inflationary pressure in the short run. It may then also choose to tackle inflation, which will in turn affect the other country. These spillover effects could be minimised if the countries were to harmonise their policy action.

Key distinctions: appreciation, depreciation, revaluation, and devaluation

It's important to distinguish between these terms:

- When a government under a fixed exchange rate system chooses to lower the exchange rate, this is known as a devaluation

- When the exchange rate falls under a floating exchange rate system, it is known as a depreciation

- An increase in the exchange rate initiated by authorities under a fixed exchange rate system is known as a revaluation

- Under a floating rate system, a rise in the exchange rate is known as an appreciation

The exchange rate and macroeconomic policy

The relationship between the exchange rate and macroeconomic policy is important. Under a fixed exchange rate system, the need to maintain the value of the currency is a constraint on macroeconomic policy, and forces the economy to adjust to disequilibrium through the real economy.

On the other hand, it does have the benefit of imposing financial discipline on governments.

Under floating exchange rates, the relationship with policy is less obvious. With a flexible exchange rate, authorities can use monetary policy to stabilise the economy, knowing there will be overall balance on the balance of payments.

Nonetheless, the government needs to monitor the structure of the balance of payments. When interest rates are set at a relatively high level compared with other countries, the financial account will tend to be in surplus because of capital inflows, with a corresponding deficit on the current account. This may not be sustainable in the long run.

Viewed in another way, if the current account is in deficit, the financial account will need to be in surplus to ensure there is overall balance.

International competitiveness

In analysing the UK's position within Europe and with its other trading partners, the relative competitiveness of UK goods and services is an important issue. The UK has persistently shown a deficit on the current account over a long period, particularly in the 2000s. Does this imply that UK goods are uncompetitive in international markets?

To investigate this and evaluate its importance, it is first necessary to examine how competitiveness can be measured and the factors that affect it.

Competitiveness of UK goods

The demand for UK exports in world markets depends on several factors. The demand for a good generally depends on:

- Its price

- The prices of other goods

- Consumer incomes and preferences

You can think of the demand for UK exports as depending on:

- The price of UK goods

- The price of other countries' goods

- Incomes in the rest of the world

- Non-UK residents' preferences for UK goods over those produced elsewhere

However, in international transactions, the exchange rate is also relevant, as this determines the purchasing power of UK incomes in the rest of the world.

Similarly, the demand for imports into the UK will depend on the relative price of domestic and imported goods, incomes in the UK, preferences for foreign and domestically produced goods, and the exchange rate. These factors will all come together to determine the balance of demand for exports and imports.

The exchange rate plays a key role in influencing the levels of both imports and exports.

Key Points to Remember:

-

The foreign exchange market operates through demand and supply, with the equilibrium exchange rate automatically ensuring an overall balance of payments of zero

-

Under a fixed exchange rate system, governments commit to maintaining the currency at a specified level by intervening in the market using foreign exchange reserves

-

The Dollar Standard (Bretton Woods system) operated from the end of World War II until the early 1970s, with currencies pegged to the US dollar

-

Devaluation under a fixed system can improve competitiveness but may be subject to the J-curve effect and requires the Marshall-Lerner condition to be satisfied for current account improvement

-

Under a floating exchange rate system, the currency value is allowed to find its own level, with factors including interest rates, inflation rates, trade balance, investment flows, and speculation determining the rate

-

Fixed systems provide stability and discipline but limit monetary policy independence and require adjustment through the real economy

-

Floating systems allow automatic adjustment to shocks and monetary policy flexibility but can be volatile and may not encourage policy discipline

-

The choice between systems involves trade-offs between stability, adjustment mechanisms, and policy autonomy