Forms of Business (Edexcel A-Level Business): Revision Notes

Forms of business

Introduction to business forms

In the UK, businesses vary significantly in their size, ownership and legal structure. Understanding different forms of business is essential for entrepreneurs when deciding how to structure their enterprise. Each form has distinct advantages, disadvantages and legal requirements that affect how the business operates and grows.

The main forms of business include sole traders, partnerships, limited companies (private and public), franchises, social enterprises, lifestyle businesses and online businesses. Choosing the right structure depends on factors such as the amount of capital needed, liability concerns, control preferences and growth ambitions.

The choice of business structure is one of the most important decisions an entrepreneur will make, as it affects taxation, personal liability, control, and the ability to raise finance. This decision should be based on careful consideration of both current needs and future growth plans.

Sole traders

A sole trader (also called a sole proprietor) represents the simplest form of business organisation. This structure has one owner but can employ any number of workers. Sole traders operate across all sectors of the economy:

- Primary sector: farmers, fishermen

- Secondary sector: small building firms, manufacturing businesses

- Tertiary sector: retailers, web designers, tutors, hairdressers, taxi drivers, garden maintenance services

Setting up as a sole trader

Setting up is straightforward because there are no legal formalities required to register the business. However, sole traders must meet certain legal responsibilities:

- Pay income tax and National Insurance contributions on profits

- Register for VAT once turnover reaches a certain threshold (though some register voluntarily to reclaim VAT paid on purchases)

- Obtain trading licences for specific activities (e.g. selling alcohol, taxi services, public transport)

- Seek planning permission when necessary (e.g. converting premises for different use)

- Comply with business legislation including providing safe working conditions for employees

Unlimited liability

All sole traders have unlimited liability. This critical feature means that if the business fails, the owner can lose more than the original investment. The owner may be forced to sell personal possessions and use personal wealth to pay off business debts. This represents the biggest financial risk of being a sole trader.

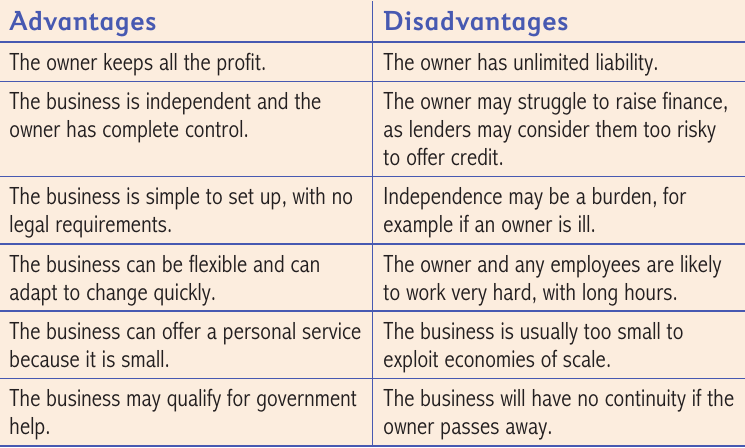

Advantages and disadvantages of sole traders

The owner retains complete independence and control over decision-making. All profits belong to the owner, providing strong motivation to succeed. The business can respond quickly to market changes and offer personalised customer service due to its small size. Government support schemes may also be available to help sole traders.

However, unlimited liability creates substantial risk. Raising finance proves difficult as lenders often view sole traders as high-risk borrowers. The burden of independence can be overwhelming, particularly during illness. Long working hours are common, and the business typically cannot achieve economies of scale due to its size. Additionally, the business lacks continuity if the owner dies or becomes unable to work.

Key Points About Sole Traders:

- Simplest form of business with one owner

- No legal formalities needed to set up

- Owner has unlimited liability (personal assets at risk)

- Complete control but all responsibility falls on one person

- Difficult to raise finance and achieve economies of scale

Partnerships

A partnership is defined by the Partnership Act 1890 as the "relation which subsists between persons carrying on business with common view to profit". Simply put, a partnership has more than one owner who jointly run the business and share profits.

Partnerships are particularly common in professional services such as accountants, doctors, estate agents, solicitors and veterinary surgeons. After sole traders, partnerships represent the most common type of business organisation in the UK. Partners typically specialise in different aspects of the business, allowing the firm to serve diverse client needs.

Deed of partnership

While no legal formalities are required to form a partnership, partners often draw up a Deed of Partnership. This legal document states partners' rights and helps resolve disputes. It typically covers:

- Capital contribution from each partner

- Profit and loss sharing arrangements

- Procedures for ending the partnership

- Control and decision-making authority

- Rules for admitting new partners

Without a Deed of Partnership, arrangements between partners follow the Partnership Act. For example, the Act states that profits must be shared equally if no other agreement exists.

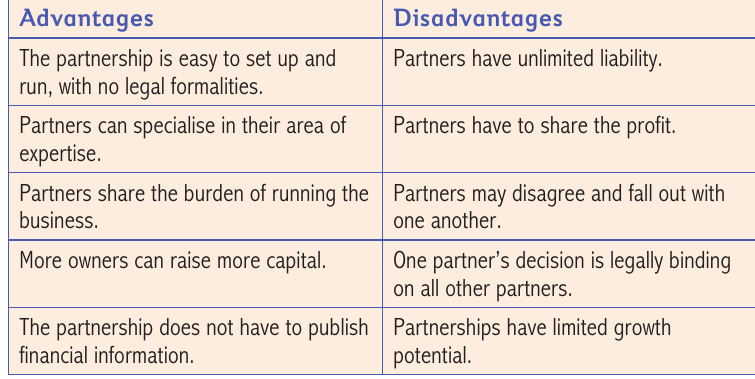

Advantages and disadvantages of partnerships

Partnerships are easy to establish with no legal formalities required. Partners can specialise according to their expertise, improving service quality. The burden of running the business is shared, reducing stress on individuals. Multiple owners can raise more capital than a single owner. Partnerships also maintain privacy by not having to publish financial information.

However, partners face unlimited liability, exposing personal assets to business risks. Profits must be shared among all partners, reducing individual returns. Disagreements between partners can create conflict and affect business performance.

One partner's decisions legally bind all other partners, creating potential liability issues. This means you can be held responsible for business debts arising from decisions made by other partners, even if you disagreed with those decisions.

Partnerships also face limited growth potential compared to limited companies.

Limited partnerships

The Limited Partnerships Act 1907 allows businesses to become limited partnerships, though this remains rare. In this structure, some partners (called sleeping partners) provide capital but take no part in management. These partners have limited liability – they can only lose their original investment and cannot be forced to sell personal possessions to meet business debts.

However, even in a limited partnership, at least one partner must have unlimited liability. This type of partnership can have more than 20 partners.

Limited liability partnerships

The Limited Liability Partnership Act 2000 created limited liability partnerships where all partners have limited liability. To set up this structure, the business must comply with regulations including filing annual reports with the Registrar of Companies. This provides greater protection for partners but requires more transparency and administration.

Limited companies

A limited company has a separate legal identity from its owners. This means the company itself can own assets, form contracts, employ people, sue and be sued. This legal separation creates important protections for owners.

The concept of separate legal identity is fundamental to understanding limited companies. The company exists as a legal person distinct from its owners, which provides crucial protection for shareholders' personal wealth.

Common features of limited companies

Share capital: Limited companies raise capital by selling shares. Each shareholder owns a portion of the company and enjoys voting rights on important decisions. Shareholders receive dividends from profits. Those with more shares have greater control and receive larger dividends.

Limited liability: Unlike sole traders or partnerships, shareholders have limited liability. If the company has debts, owners can only lose their original investment. Personal wealth remains protected from business debts.

Directors: Limited companies are run by directors elected by shareholders. The board of directors, headed by a chairperson, is accountable to shareholders and runs the company according to their wishes. Directors who perform poorly can be removed at an annual general meeting (AGM).

Corporation tax: Limited companies pay corporation tax on profits, unlike sole traders and partnerships who pay income tax.

Forming a limited company

To form a limited company, entrepreneurs must follow a legal procedure by sending important documents to the Registrar of Companies:

Documents Required for Formation:

Memorandum of Association: This document sets out the constitution and company details including:

- Company name

- Registered office address

- Business objectives and nature of activities

- Amount of capital to be raised

- Number of shares to be issued

Articles of Association: This document covers internal company running including:

- Shareholder rights based on share type

- Procedures for appointing directors

- Length of director service before re-election

- Timing and frequency of company meetings

- Arrangements for auditing company accounts

Once these documents are accepted, the company receives a Certificate of Incorporation allowing it to trade as a limited company. Shareholders have legal rights to attend AGMs and must receive written notice of dates and venues.

Setting up a limited company has become easier with online services providing templates for required documents.

Private limited companies

Most private limited companies are small or medium-sized businesses, though some grow to rival public limited companies in size. Private limited companies have distinctive features:

Company name: Business names end in Limited or Ltd

Share transfer: Shares can only be transferred privately between individuals. All shareholders must agree on transfers, and shares cannot be advertised for sale.

Ownership structure: Often family businesses owned by family members or close friends

Director involvement: Directors typically own shares and actively participate in running the business

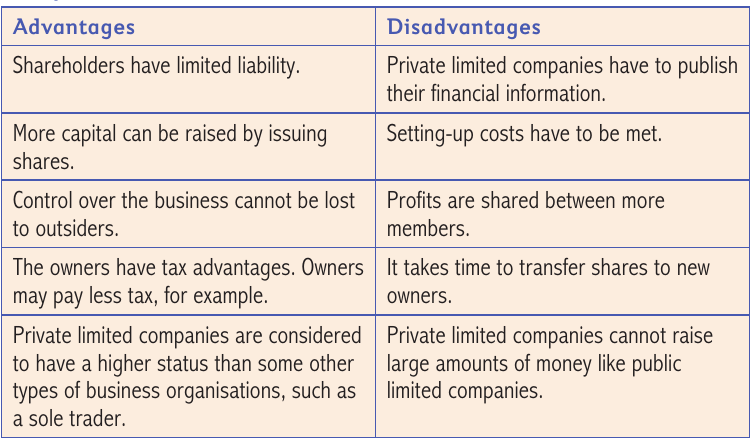

Advantages and disadvantages of private limited companies

Shareholders benefit from limited liability protection for personal assets. The company can raise more capital by issuing shares to additional members. Control cannot be lost to outsiders since share transfers require approval. Owners may pay less tax compared to sole traders. Private limited companies also have higher status than sole traders, which can help with credibility.

However, private limited companies must publish financial information, reducing privacy. Setting up costs must be paid for legal procedures and documentation. Profits are shared among more members than in sole proprietorships. Transferring shares to new owners takes time and requires agreement. Private limited companies also cannot raise capital as easily as public limited companies.

Private Limited Companies (Ltd) – Key Features:

- Limited liability protection for all shareholders

- Shares cannot be publicly traded or advertised

- Often family-owned or closely held businesses

- More formal structure than sole traders or partnerships

- Must publish accounts but retain more privacy than public companies

Franchising

Starting a business carries substantial risk – most new start-ups fail within five years. Franchising offers a way to reduce this risk by using proven business models.

How franchising works

The franchisor is a company that owns the franchise and has a successful track record. It allows another business, the franchisee, to use its business ideas and methods in return for various fees. Major UK franchise operations include Dairy Crest, Domino's Pizza, Dyno-Rod, McDonald's, SUBWAY and Tumble Tots.

How a Franchise Operates:

- Franchisor (e.g., McDonald's) develops a successful business model with proven products, systems, and brand recognition

- Franchisee purchases the right to operate under the franchise name and receives comprehensive support

- Franchisee pays fees including initial start-up costs and ongoing percentage of sales

- Both parties benefit: Franchisor expands without full capital investment; franchisee gains proven business model with support

Services provided by franchisors

Licensed product: Franchisees receive rights to make tried-and-tested products or services proven in the marketplace.

Brand recognition: The franchisor provides an established brand name that customers recognise and trust. This generates immediate sales when the franchise opens.

Start-up package: Franchisors provide comprehensive help including business setup advice, equipment, financing assistance and training for new franchisees.

Materials supply: Many franchises sell ingredients or materials to franchisees. Even when franchisors don't sell directly, they often negotiate bulk-buy deals with suppliers to reduce costs.

Marketing support: Franchisors typically run national advertising campaigns and provide marketing materials like posters and leaflets.

Ongoing training: Regular training ensures standards are maintained and franchisees learn about new products and developments.

Business services: Franchisors negotiate competitive rates on services such as insurance or vehicle leasing for all franchisees.

Exclusive areas: Many franchises operate exclusive area contracts, guaranteeing no other franchisee will operate in a particular geographical location.

Brand development: Franchisors continually develop the brand with new products to maintain customer appeal.

Fees paid by franchisees

Initial start-up fee: Covers advice costs, equipment provision and the right to use the franchise name.

Percentage of sales: Most franchisors charge a percentage of sales for ongoing management services and brand usage rights.

Supply profits: Franchisors make profit on materials and ingredients sold directly to franchisees.

One-off fees: Additional charges for specific management services like training courses.

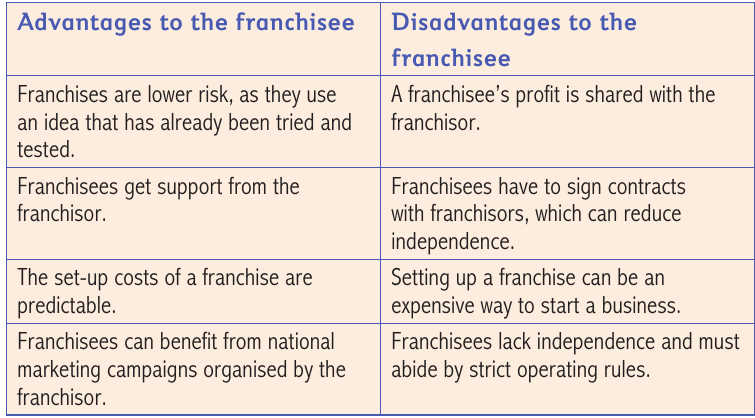

Advantages and disadvantages for franchisees

Franchises carry lower risk because they use proven business concepts that have already succeeded. Franchisees receive valuable support from experienced franchisors. Set-up costs are predictable, helping with financial planning. Franchisees benefit from national marketing campaigns without bearing full costs.

However, franchisees must share profits with franchisors, reducing returns. Contracts with franchisors reduce independence and limit decision-making freedom. Setting up a franchise can be expensive compared to starting independently. Franchisees must follow strict operating rules, limiting flexibility and creativity.

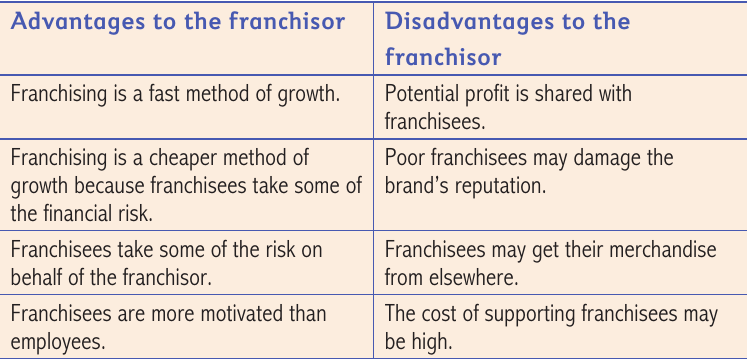

Advantages and disadvantages for franchisors

Franchising enables fast business growth without requiring full capital investment. The method is cheaper than opening company-owned outlets because franchisees share financial risk. Risk is distributed across many franchisees rather than concentrated with the franchisor. Franchisees are typically more motivated than employees because they own their business.

However, potential profits must be shared with franchisees rather than retained entirely. Poor franchisees can damage brand reputation across the entire network. Franchisees may source merchandise elsewhere, undermining quality control. Supporting franchisees with training and services creates significant ongoing costs.

Franchising Overview:

- Lower risk for franchisees through proven business models

- Support and training provided by experienced franchisors

- Profit sharing required – both parties sacrifice some potential profits

- Balance between support and independence – franchisees gain help but lose some control

- Benefits both parties when relationship works well

Social enterprises

Some businesses operate as social enterprises – organisations that trade with the aim of improving human and environmental well-being rather than making profit for external owners. These are sometimes called not-for-profit organisations.

Characteristics of social enterprises

Social enterprises generally share these features:

- Have clear social and/or environmental missions

- Generate most income through trade or donations

- Reinvest most profits into the mission

- Operate independently from government

- Are controlled to serve the social mission

- Maintain accountability and transparency

Social enterprises differ from traditional businesses because their primary purpose is social or environmental impact rather than profit maximisation. Any profits generated are reinvested to further the organisation's mission rather than distributed to external shareholders.

Types of social enterprises

Co-operatives: Most modern co-operatives operate as consumer or retail co-operatives. Members own and control these organisations. Members purchase shares giving them voting rights at AGMs. They elect directors to make overall business decisions and appoint managers for day-to-day operations. Co-operatives run in members' interests, distributing any surplus as dividends based on spending levels.

Worker co-operatives: These businesses are jointly owned by employees. Examples include wine-growing co-operatives or dairy farmer co-operatives. In worker co-operatives, employees typically:

- Contribute to production and participate in decision-making

- Share profits, usually equally

- Provide capital by buying shares in the business

Mutual organisations: Most UK building societies are mutual organisations owned by customers (called members) rather than shareholders. They offer financial services such as mortgages and savings products. Profits return to members through better and cheaper products rather than shareholder dividends. Friendly societies (also mutual organisations) began in the 18th and 19th centuries supporting working classes. Today they offer affordable financial services including savings schemes, insurance plans and income protection.

Charities: Charities exist to raise money for causes and raise awareness of disadvantaged groups' needs. Examples include Age UK (supporting older people), British Red Cross, Save the Children Fund and Mencap. Charities rely on donations for revenue and organise fundraising events like jumble sales, sponsored activities and raffles. Many charities also run business ventures such as charity shops.

Lifestyle businesses

A person running a lifestyle business aims to make enough money to sustain a particular lifestyle while maintaining flexibility for personal life. The business should support the desired lifestyle without requiring sacrifice of personal time.

Characteristics of lifestyle businesses

Small scale: Businesses are often small with a single owner

Personal interest: The entrepreneur's interests heavily influence the business nature, making work enjoyable

Multiple ventures: Owners may undertake various different activities. For example, a musician might earn income from live performances, teaching, busking, part-time college work and writing music for advertisements

Lower stress: Running the business creates less stress than traditional businesses

Home-based: Businesses typically operate from home

Similar to sole traders: Advantages and disadvantages resemble those of sole traders

Retirement alternative: Sometimes considered as an alternative to traditional retirement

Lifestyle businesses prioritise work-life balance and personal satisfaction over profit maximisation. The goal is to generate sufficient income to support a desired lifestyle while maintaining flexibility and pursuing personal interests.

Examples of lifestyle businesses

Typical examples include tradespeople (plumbers, electricians), consultants across industries, florists, small retail stores, bed and breakfasts, small lifestyle farms, and online services (web design, coaching, advisory, marketing).

Lifestyle businesses contrast with start-up businesses intended to maximise growth and profit. Because profit maximisation is not the objective, lifestyle business owners usually self-fund their ventures. External investors rarely fund businesses not aiming to maximise profits. However, exceptions exist – some successful entrepreneurs run large-scale lifestyle businesses while maintaining work-life balance.

Online businesses

Online businesses use the internet to trade and operate. Well-known examples include Amazon.com, MoneySuperMarket.com, Confused.com, eBay and Facebook. However, thousands of smaller online businesses exist including retailers, consultants, gaming companies, bloggers, share dealers, teachers, web designers and information providers.

Common features of online businesses

Internet access: Customers access businesses via the internet. All online businesses have websites providing product information, prices and company details.

Electronic payment: Online businesses collect payment electronically using credit cards, debit cards and PayPal as the most common methods.

Easy setup: No formal procedures or legal requirements exist for starting online businesses. However, traders must maintain secure websites with protection against technical breakdowns and fraud.

Low costs: Online businesses have low set-up costs. Traders can build websites for a few hundred pounds or purchase complete set-up packages including web design, domain name registration and website hosting. Many online businesses run from home, eliminating premises costs.

Advertising revenue: For many online businesses, paid or sponsored advertising provides the main revenue source. For example, Facebook generated most of its $7.87 billion revenue in 2013 from advertising despite offering free services to users.

Growth of online business

The internet has fundamentally changed how products and services are sold, developed, designed, produced and distributed. Even small businesses now access global markets, international suppliers and foreign employees.

Growth Statistics:

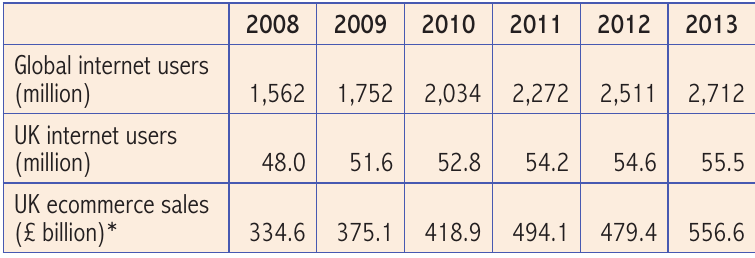

- Global internet usage grew rapidly from 1,562 million users in 2008 to 2,712 million in 2013

- UK internet usage growth has slowed because most people already use the internet

- UK ecommerce sales rose from $334.6 billion in 2008 to $556.6 billion in 2013, representing 66.3% growth over the period

This demonstrates the rapid expansion of online commerce.

Most businesses now have websites providing information about company history, products, services, aims and contact details. Many retailers including supermarkets, chain stores and independent retailers operate online sales alongside physical stores.

Remember!

Key forms of business:

- Sole traders have one owner, unlimited liability, and keep all profits but face difficulty raising finance

- Partnerships have multiple owners sharing profits and responsibilities, but partners have unlimited liability and decisions bind all partners

- Private limited companies (Ltd) provide limited liability protection, can raise capital through shares, but must publish financial information and share profits

- Franchises reduce risk through proven business models but require sharing profits with franchisors and following strict rules

- Social enterprises prioritise social/environmental missions over profit, including co-operatives, mutual organisations and charities

Critical concepts:

- Limited liability protects personal wealth – owners only lose original investment

- Unlimited liability puts personal assets at risk – owners can lose more than invested

- Separate legal identity means limited companies can own assets and form contracts independently

Business structure choices:

- Consider capital requirements, liability concerns, control preferences and growth ambitions

- Each structure has trade-offs between control, liability, capital-raising ability and administrative requirements

- Online businesses and lifestyle businesses can operate under various legal structures depending on owner objectives